Best Alternative Data Providers of 2026: Complete Comparison

Discover 25 leading alternative data providers helping lenders improve credit decisions, detect fraud, and serve borrowers beyond traditional scoring.

.webp)

We analyzed 6.1 million loan applications

The results show how digital credit scores correlate with default risk.

Traditional credit scoring leaves too many blind spots. Alternative data fills them.

By turning digital footprints into actionable insights, lenders can improve scoring accuracy, reduce fraud, and expand approvals.

In this guide, we explain the concept and compare 25 top alternative data providers shaping the future of credit risk.

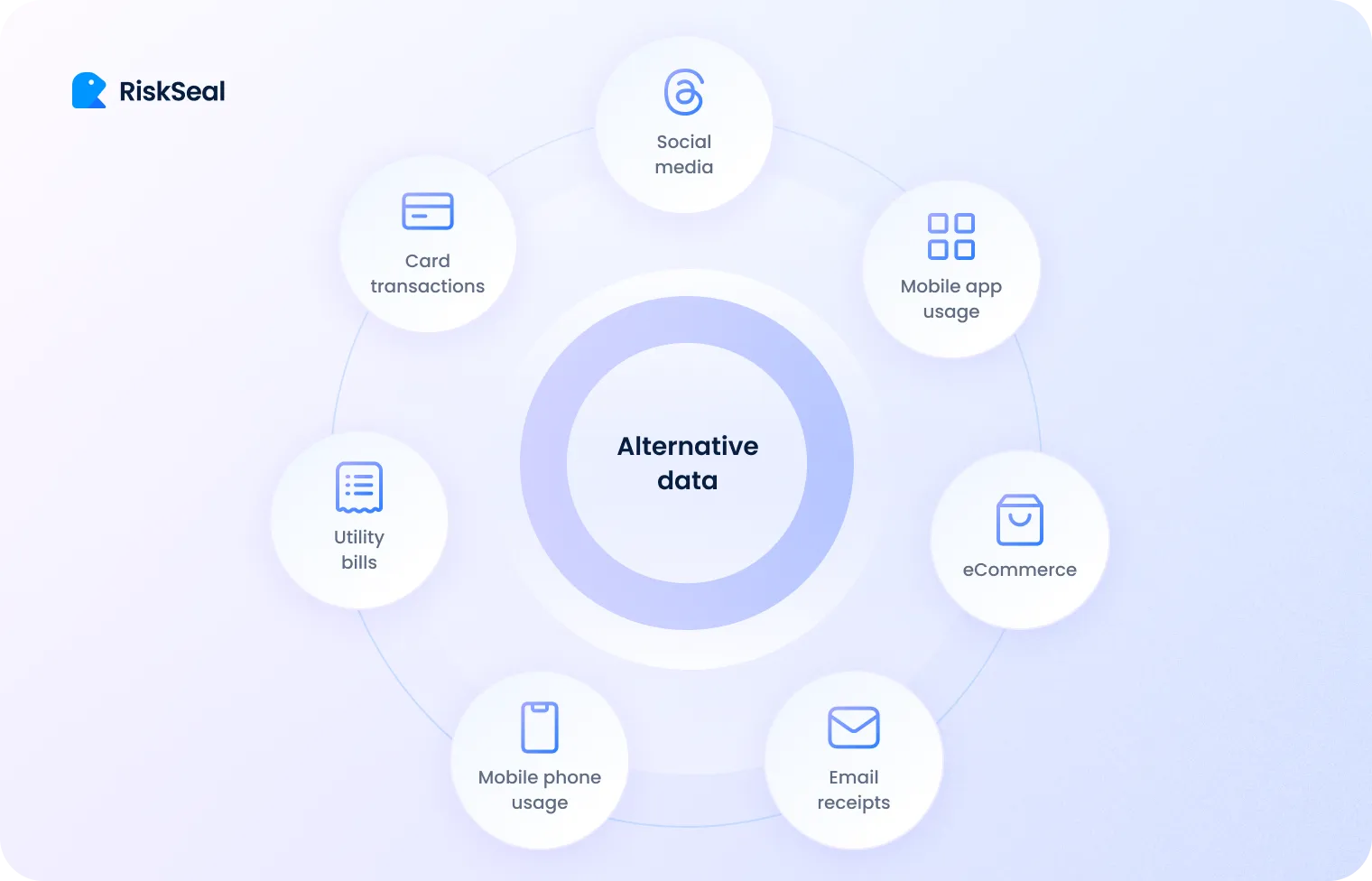

What is alternative data?

Alternative data for credit scoring refers to any information that comes from outside traditional credit reports and financial documents.

Instead of relying solely on credit bureau history, it gives lenders a more nuanced view of a borrower’s financial behavior and reliability.

At its core, alternative data is built on a person’s digital footprint – the trail of information we all leave behind when using the internet, mobile devices, and online services.

Every interaction, from creating accounts to maintaining subscriptions, contributes small signals that, when combined, can reveal patterns of stability, consistency, and trustworthiness.

This type of data can come from a wide range of sources. Common examples include:

- Email address intelligence (age, domain, activity signals)

- Phone number data (tenure, carrier, usage patterns)

- Registrations linked to email or phone across platforms

- Paid subscriptions such as Netflix, Spotify, or other digital services

- Social media presence, including account consistency and activity

- Usernames, profile photos, and cross-platform identity signals

- Presence on eCommerce platforms or marketplaces popular in a specific region

- Device, IP, and location-based insights

Together, these data points help best alternative data providers form a more complete picture of how a person behaves in real life. Not just how they interact with financial institutions.

Importantly, alternative credit scoring focuses only on publicly available or permission-based data.

It does not access private content such as direct messages, personal conversations, detailed purchase histories, or streaming activity.

Instead, it analyzes high-level behavioral and structural patterns that indicate whether a digital identity appears genuine, stable, and low-risk.

By incorporating these additional insights, lenders can move beyond the limitations of traditional scoring models.

This approach makes it possible to assess thin-file or no-file applicants more accurately, reduce fraud risk, and ultimately make fairer, more inclusive lending decisions.

Top 25 alternative data providers

We relied on specific criteria to compile a list of alternative data providers. In our view, such providers should:

- Offer products based on alternative data

- Focus on credit risk assessment use cases

- Enhance scorecard performance

- Help lenders decide between high-risk and reliable clients

Based on our analysis, we’ve highlighted 25 alternative credit data providers that meet these standards.

-

#1. RiskSeal

Overview:

RiskSeal is an alternative data provider that helps lenders strengthen credit scoring models with unique digital footprint signals.

The local alternative data it provides is unavailable from traditional bureaus or most competing vendors.

The platform acts as a data enrichment layer for risk teams, helping improve risk segmentation, fraud detection, and model performance across multiple markets.

Strengths:

- Unique local data sources across multiple markets

- Market-specific platform and registration signals

- Predictive digital footprint features such as email age, phone age, premium subscriptions, social presence, and breach exposure

- Strong support for thin-file borrowers and fraud prevention

- Fast integration in under 1 day

- Strong uplift-to-cost ratio

- Flexible, transparent, customer-centric support

- GDPR-aligned and ISO 27001-certified

Website: https://riskseal.io/

Cost:

Starting from $499/month, with flexible pricing, a pay-as-you-go model, no additional integration fees, and support and training included. Free PoC is available.

#2. LenddoEFL

Overview:

LenddoEFL is a scoring solution that uses artificial intelligence, machine learning, and predictive analytics to analyze both traditional and alternative data. The company is especially known for using psychometric data to assess borrower creditworthiness.

Strengths:

- Uses non-traditional data from sources such as social media, smartphone metadata, online shopping behavior, email and SMS data, web browsing history, and GPS location data

- Applies psychometric and biometric analysis, including personality assessment, cognitive ability tests, and skills evaluations

- Supports more layered borrower assessment beyond standard financial data

Website: https://lenddoefl.com

Cost:

No publicly available pricing information. Users need to fill out a form on the website to get tariff details. Trial period information is not available.

#3. Rubix

Overview:

Rubix is an analytical platform designed to help businesses mitigate credit risk, strengthen supply chain security, and monitor compliance requirements for users in India and globally.

Strengths:

- Combines structured data from financial statements and open databases

- Uses unstructured data from 200+ sources, including retail sales, POS, social media, mobile location, satellite imagery, supply chain, and consumer demographic data

- Provides pre-defined risk analytics with scores, indices, and estimations

Website: https://rubixds.com

Cost:

Customized pricing. You need to contact the company for details. Trial period information is not available.

#4. Plaid

Overview:

Plaid is an alternative data provider that helps organizations assess potential clients by analyzing banking transactions, income, and expenses.

Strengths:

- Access to classified and unclassified transactions from personal accounts spanning more than 5 years

- Balance information

- Account identification details

- Useful for understanding cash flow and financial behavior through connected banking data

Website: https://plaid.com

Cost:

Offers free and custom pricing plans. Trial period available.

#5. Credolab

Overview:

Credolab is a platform that enriches scoring models with alternative data for risk assessment, fraud detection, and marketing improvement.

Strengths:

- Uses smartphone metadata and web behavioral data

- Includes call and SMS, location, and social media data

- Offers analytics and personality assessment based on web behavioral patterns

- Supports both risk evaluation and fraud detection workflows

Website: https://www.credolab.com

Cost:

Starting from $600/month. A 30-day free access period is available.

#6. IDology

Overview:

IDology is a platform focused on identity verification at the point of transaction, helping businesses prevent fraud, reduce costs, and maintain regulatory compliance.

Strengths:

- Uses government and private data sources

- Includes device, phone number, email intelligence, social media, and geolocation data

- Supports document authentication

- Offers selfie-based identity verification through digital identity verification data

Website: https://www.idology.com

Cost:

Custom pricing. You need to contact the company for a quote. Trial period is available upon request.

#7. MicroBilt

Overview:

MicroBilt provides alternative data and predictive algorithms to help organizations assess the creditworthiness of clients or partners across different industries.

Strengths:

- Uses periodic payment data such as utility, rent, and telecom payments

- Includes savings account data

- Provides access to additional records such as property and business ownership, criminal, eviction, bankruptcy, judgment, employment history, vehicle registration, and address history data

- Offers broad data coverage for more detailed risk assessment

Website: https://www.microbilt.com

Cost:

Subscription-based pricing depending on service volume. Trial period is available upon request.

#8. ArkOwl

Overview:

ArkOwl is a platform for real-time email address and phone number verification. It provides raw data that helps clients assess the reliability of a user.

Strengths:

- Pulls data points from social networks, email providers, domain databases, and other public data sources

- Can reveal information such as email account creation date, real owner name, known nicknames, and registration status

- Supports simultaneous real-time verification of thousands of email addresses and phone numbers

- Consolidates signals into a single user profile

Website: https://arkowl.com

Cost:

Offers monthly subscription, upfront payment, and pay-as-you-go options. Trial period available with registration.

#9. Dana

Overview:

Dana is a solution for e-commerce platforms that want to provide users with instant loans through a digital lending platform.

Strengths:

- Uses digital footprint data of potential borrowers

- Includes device metadata

- Incorporates information from SMS transaction alerts

- Designed for embedded lending and digital commerce environments

Website: https://dana.money

Cost:

Pricing is available on request. No trial period information is provided on the official website.

#10. Monnai

Overview:

Monnai is a solution for fintech companies that uses AI to analyze fragmented customer data, support identity checks, and assess online behavior.

Strengths:

- Uses telecommunications data, email usage information, IP address data, and online behavioral data

- Analyzes digital footprints across more than 40 global and local websites

- Helps fintechs build richer customer insight using cross-source signals

Website: https://monnai.com

Cost:

Flexible pricing policy. Trial period available.

#11. FinScore

Overview:

FinScore is a fintech company specializing in alternative credit scoring based on telecom provider data. It operates in the Philippines and Indonesia and uses AI and machine learning to assess borrower creditworthiness.

Strengths:

- Uses telecommunications data such as call duration, geolocation, mobile phone costs, SIM card age, and prepaid/postpaid status

- Includes additional signals from email address and social media data

- Provides information on previous loan applications from 40+ financial organizations

- Designed for credit access in underbanked markets

Website: https://www.finscore.ph

Cost:

SUPERFLEXI and DISCOVERY tariff plans are available on request, with personalized pricing also possible. All pricing plans include access to Proof of Concept and Historical Backtesting.

#12. LexisNexis Risk Solutions

Overview:

LexisNexis Risk Solutions is a provider of alternative data for organizations across financial services, insurance, public administration, and other industries. The company focuses on analytics, risk forecasting, and fraud prevention.

Strengths:

- Public records

- Identity insights

- Stability insights

- Address insights

- Alternative credit seeking insights

- Asset insights

- Broad coverage for risk evaluation and fraud prevention use cases

Website: https://risk.lexisnexis.com

Cost:

Complex pricing structure. Search fees range from $0 to $469, with combined searches priced individually. Trial period available.

#13. Trusting Social

Overview:

Trusting Social provides AI-based tools that help lending institutions manage credit risk, identify borrowers, and assess creditworthiness. The company operates in India, Indonesia, Vietnam, and the Philippines.

Strengths:

- Uses telecommunications data

- Supports facial recognition by comparing selfies and national ID images with avatars in social media and public databases

- Provides alternative credit rating

- Provides fraud rating

- Focused on financial inclusion and borrower assessment in emerging markets

Website: https://trustingsocial.com

Cost:

Customized pricing. No free trial available.

#14. Zest AI

Overview:

Zest AI is an American technology company that offers an AI-based platform for building customized credit scoring models and predicting risk.

Strengths:

- Uses cash flow data such as utility payments, rent payments, and mobile operator fees

- Goes beyond standard credit bureau data with deeper analysis of delinquencies and repayment behavior

- Helps lenders build more tailored models with broader risk signals

Website: https://www.zest.ai

Cost:

Custom pricing. Businesses need to arrange a consultation or demo to get a quote. Free trial is not available, but a demo can be requested.

#15. CreditXpert

Overview:

CreditXpert focuses on improving borrower credit ratings in the mortgage lending space. The platform uses alternative data to assess applicants, build credit improvement plans, and help lenders offer more personalized loan terms.

Strengths:

- Uses rent data

- Uses utility bill data

- Uses cell phone bill data

- Supports borrower assessment and credit optimization for mortgage use cases

Website: https://creditxpert.com

Cost:

From $99. No free trial period, but two demo options are available: a pre-recorded video and an interactive demo.

#16. AdviceRobo

Overview:

AdviceRobo is an AI-based platform focused on advanced decision-making in lending and marketing. It enables organizations to track and evaluate risks using dynamic financial analytics.

Strengths:

- Uses open banking data

- Uses digital footprint data

- Uses psychometric profiles

- Supports richer decision-making with behavioral and financial signals

Website: https://advicerobo.com

Cost:

Customized pricing. A free 30-day trial period is available.

#17. AperiData

Overview:

AperiData presents itself as a real-time credit reference agency. It specializes in risk analytics and credit scoring for financial organizations.

Strengths:

- Uses customer account data

- Includes information about obligations, transactions, assets, income, and expenses

- Provides risk identifiers

- Supports identity verification

- Designed for real-time credit and risk assessment workflows

Website: https://www.aperidata.com

Cost:

No publicly available pricing. Consultation required. No trial period is listed, but a demo can be booked.

#18. APLYiD

Overview:

APLYiD is a platform designed for AML and KYC compliance. It uses biometric identification and data verification technologies to verify clients for businesses in legal, real estate, and accounting sectors.

Strengths:

- Uses global government databases

- Identifies Politically Exposed Persons (PEPs)

- Performs sanctions list checks

- Supports identity verification and onboarding in regulated environments

Website: https://www.aplyid.com

Cost:

Four pricing plans are available, but pricing details require contacting the company. Trial period available.

#19. Atto

Overview:

Atto is a fintech company that helps lenders make credit decisions and manage portfolios using alternative data. It focuses on serving businesses and consumers with limited financial inclusion.

Strengths:

- Provides information about bank accounts

- Includes income, expenses, and transaction data

- Identifies signs of financial difficulties

- Provides information about credit obligations and deposits

- Useful for improving decisioning where traditional financial data is limited

Website: https://www.atto.co

Cost:

No publicly available pricing. Consultation required. No trial period is listed, but a demo can be booked.

#20. Basiq

Overview:

Basiq is an open banking API platform that gives clients tools to aggregate consumer financial data and run analytics on top of it.

Strengths:

- Account and transaction history

- Income and expense information

- Information about obligations and assets

- Useful for financial data aggregation and analytics in lending and fintech contexts

Website: https://www.basiq.io

Cost:

Calculated individually. Fees apply for platform access and additional functionality. No trial period is provided.

#21. AccountScore

Overview:

AccountScore is an analytics provider that helps businesses obtain, enrich, and understand bank transaction data. Its solutions are used for credit modelling, affordability assessment, tenant verification, and marketing profiling.

Strengths:

- Detailed bank account transaction data

- Predictive behavioral data such as spending patterns and account usage frequency

- Affordability and disposable income calculations

- Salary and employment verification

- Tenant income and rental payment history

- In-depth financial profiling and account forecasting

Website: https://accountscore.net

Cost:

No publicly available pricing. Consultation required. No trial period is listed, but demos and API access can be requested.

#22. Jumio

Overview:

Jumio is an AI-powered digital identity solution that provides contextual insights throughout the customer lifecycle. It combines biometric verification, liveness detection, AML screening, and real-time risk intelligence.

Strengths:

- Biometric and liveness detection data, including face recognition, deepfake detection, age estimation, and spoofing-related signals

- Global sanctions, PEPs, and adverse media screening

- Identity verification signals from 5,000+ supported global ID types

- Cross-transaction identity intelligence

- End-to-end fraud detection and contextual identity analytics

Website: https://www.jumio.com

Cost:

Pricing is not publicly available. Jumio offers a Total Cost of Ownership Calculator and demos upon request. No public trial period is listed.

#23. BankFlip

Overview:

BankFlip is a platform that gives access to customers’ employment, income, and debt data. Its plug-and-play integration is designed to simplify underwriting, verification, and risk assessment.

Strengths:

- Verified income data, including salary, pensions, unemployment, and retirement income

- Employment data such as status, employer, and continuity of work

- Debt and risk data

- Coverage of income from real estate assets, investments, capital gains, business profits, crypto, and inheritance

- Permission-based model that supports transparency and broad income visibility

Website: https://www.bankflip.io

Cost:

No publicly available pricing. Consultation required. No trial period is listed, but businesses can book a demo and test the live widget.

#24. ComplyAdvantage

Overview:

ComplyAdvantage is an AI-driven AML risk detection company. Its SaaS platform combines customer and company screening, ongoing monitoring, and transaction analysis, while using alternative data to enrich compliance insights.

Strengths:

- Sanctions and watchlists data on individuals, companies, and entities

- Databases for Politically Exposed Persons and Relatives & Close Associates

- Global adverse media monitoring in multiple languages

- Transactional risk intelligence, including AML flags, fraud detection, and clustering

- Company and customer risk profiling for onboarding and ongoing monitoring

Website: https://complyadvantage.com

Cost:

Starter plan begins at $99.99/month for up to 1,000 monitored entities. Enterprise pricing is available on application. No public trial period is listed, but businesses can sign up for the Starter plan or request an Enterprise demo.

#25. Fourthline

Overview:

Fourthline is a modular identity platform that helps businesses address identity and compliance challenges. Clients can use standalone solutions or combine verification, authentication, and AML monitoring tools.

Strengths:

- Identity verification, including biometrics, document checks, and device and location data

- Digital proof of address and bank account verification

- AML screening and monitoring, including sanctions, PEPs, and adverse media

- Client authentication and re-KYC for regulatory compliance

- Investigations and CDD reporting

- Qualified electronic signatures and fraud risk indicators

Website: https://fourthline.com

Cost:

No publicly available pricing. Consultation required. No public trial period is listed, but businesses can request demos and tailored consultations.

Best alternative data provider: summary table

To make comparison easier, we’ve summarized the leading alternative data providers below, highlighting what each platform offers and where it fits best.

The best provider ultimately depends on your specific use case. Whether you need stronger fraud detection, better credit scoring for thin-file users, or deeper financial and behavioral insights.

Final thoughts on choosing among the top alternative data companies

Managing credit risks using alternative data offers numerous advantages for lenders.

It allows them to extend services to individuals with limited or no credit history.

This approach helps spot fraud and identify potential defaulters right at the application stage.

Want to learn more? Book a consultation with RiskSeal to see how we can help grow your lending business.

We analyzed 6.1 million loan applications

The results show how digital credit scores correlate with default risk.

FAQ

What is alternative data and how can it benefit the lending industry?

Alternative data refers to non-traditional sources of information that lending organizations use to gather additional insights into borrowers.

Its utilization allows lending organizations to expand their target audience by offering loans to demographics without credit history or those underserved by banking services.

Moreover, alternative data enables lenders to make more informed decisions on loan applications, thus reducing default risks.

What is the current state of the alternative data market?

The current volume of the alternative data market stands at $11 billion and is annually increasing. It is forecasted to demonstrate a CAGR of 52.1% over the next six years, reaching $135.8 billion by 2030.

How can alternative data help with credit risk reduction?

Alternative data provides lenders with a more comprehensive view of borrowers' creditworthiness.

Alternative data providers offer information that allows concluding potential clients' financial status based on factors like subscription payments, timeliness of rent and utility payments, online consumer behavior, etc.

What are the best alternative data providers for the lending industry?

While there are many alternative data providers in the market, most of them cater to organizations across various industries.

RiskSeal, as an alternative data provider, exclusively focuses on credit risk management, deeply understanding the specifics of lending businesses. The company offers lenders an innovative solution to enrich their scoring models with alternative data.

What types of alternative data does RiskSeal offer?

RiskSeal offers a suite of alternative data types designed to analyze digital footprints for credit risk assessment.

These include:

Behavioral metrics, which analyze user interaction patterns.

Trust score - a composite metric assessing user trustworthiness

Email and phone data enrichment, which enhances user identity information.

User social media search, for insights into a user's online presence.

IP analysis, which examines the geographical and network attributes of user connections.

Photo matching and name intelligence for verifying the authenticity of user-submitted names and images.

Together, these tools provide a comprehensive picture of user behavior and authenticity.

Is using alternative data compliant with regulations like GDPR or CCPA?

The use of alternative data in credit scoring must comply with regulations such as GDPR, CCPA, and other similar laws that apply in the specific region.

The responsibility for compliance lies with the lending organization. This includes ensuring the secure use and storage of user data.

Which industries benefit most from alternative data?

Lending organizations benefit the most from the use of alternative data. It is applied in the credit scoring process and allows for lending to unbanked populations, reducing fraud levels, and identifying potential defaulters.

How do lenders integrate alternative data with existing credit models?

Once a lender partners with an alternative data provider, the next step is to update and enrich their existing credit scoring models. This integration is typically carried out according to the lender’s internal processes and regulatory considerations.

After implementation, it's critical to evaluate the performance of the enhanced models by comparing them against traditional credit assessment methods. Metrics such as predictive power, approval rates, and default risk are commonly analyzed.

Finally, based on these insights, the lender decides whether to adopt the alternative scoring approach more broadly and establish a long-term partnership with the data provider.

See more

Discover the top-10 APIs bringing predictive power to credit scoring through alternative data.

Discover why Research.com ranks RiskSeal’s digital scoring platform among the top accounts receivable solutions for lenders.

Explore how alternative data transforms credit scoring in 2025. Boost inclusion, reduce fraud, and grow your lending success.