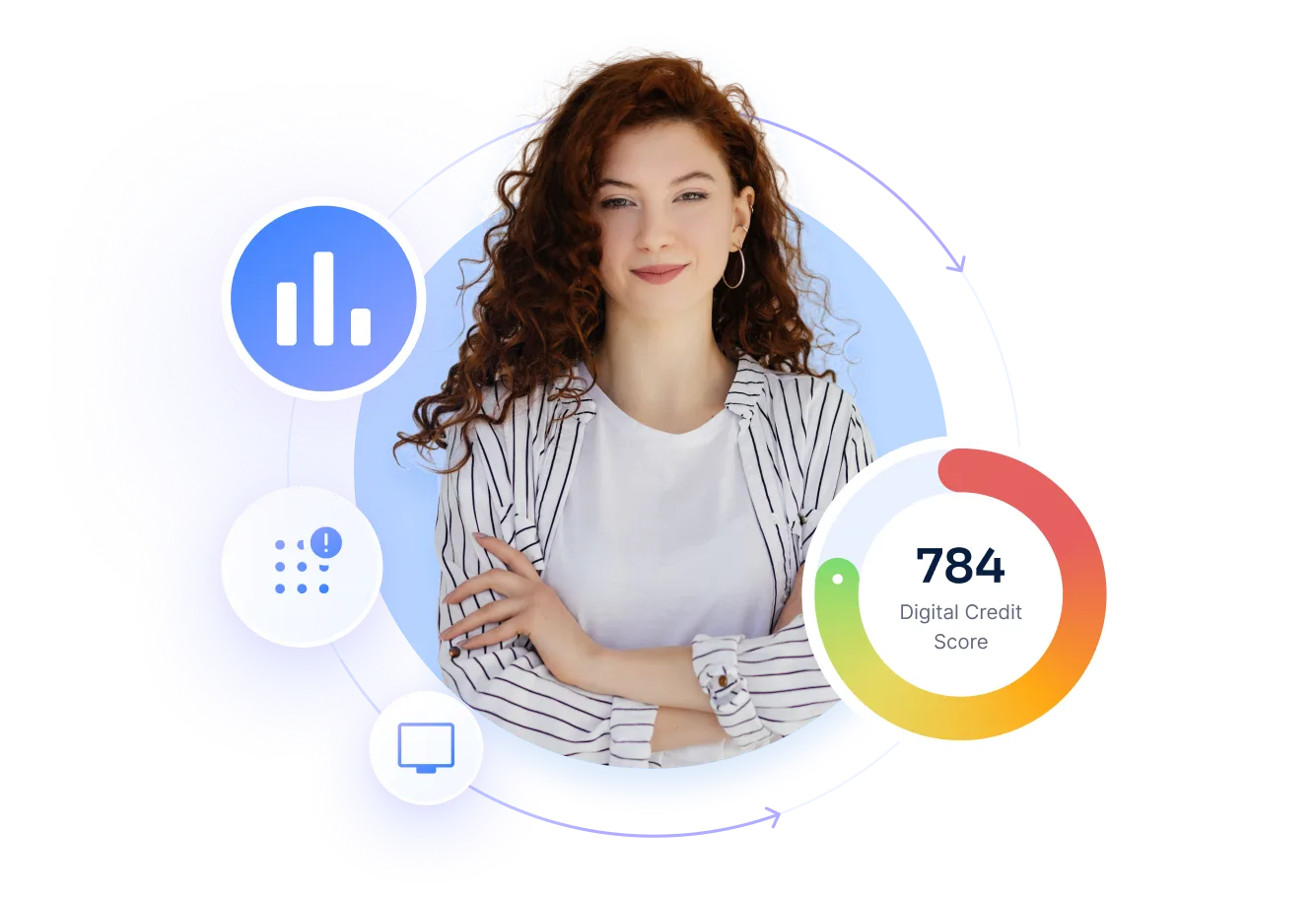

Proveedor de datos alternativos para riesgo crediticio

RiskSeal ofrece señales únicas de huella digital en más de 200 plataformas globales y regionales. El producto está diseñado para aportar mayor capacidad predictiva a tus modelos de riesgo crediticio.

Mejora el Gini con un uplift puro del modelo

Aprueba a más buenos clientes

Reduce impagos y perfiles sintéticos

Integra la solución en menos de 1 día

Solución de datos alternativos que genera un uplift medible

RiskSeal analiza la huella digital completa del solicitante. Evaluamos identificadores clave, desde el correo electrónico y el número de teléfono hasta la dirección IP, el nombre de usuario y la foto de perfil.

Al añadir los datos alternativos predictivos de RiskSeal, las entidades financieras pueden mejorar las tasas de aprobación de solicitantes con historiales crediticios limitados.

más aprobaciones en segmentos thin-file

de cobertura de solicitantes desatendidos

de reducción de impagos

para scoring en tiempo real

Aplicaciones de RiskSeal

Toma de decisiones sobre créditos

Comprenda a sus clientes y apruebe x2 más aplicaciones. Puntúe a personas no bancarizadas y desatendidas e identifica clientes solventes con un 98% de éxito.

Thin-file coverage

Unbanked scoring

Non-correlated Gini uplift

Default reduction

Add real-time behavioral signals to identify high-risk profiles before disbursement.

Up to 25% fewer defaults

Stronger segmentation

Early risk detection

Fraud detection

Use email and phone intelligence to separate real identities from fabricated ones.

Synthetic identity detection

Enhanced threat detection

Lower onboarding fraud

Debt collection

Apply digital footprint insights to prioritize collections and reach borrowers faster.

Higher recovery rates

Lower collection costs

Reachable borrower focus

Digital identity intelligence

Move beyond document checks with AI-driven identity validation.

One-shot Face Match

Cross-platform Name Match

Geo-consistency insights

Fuentes de datos detrás de la plataforma de datos alternativos de RiskSeal

Accedemos a servicios online locales que los burós de crédito no detectan, aportando capacidad predictiva allí donde los datos tradicionales se quedan cortos.

Medios sociales y mensajeros

Comercio electrónico

Amazon

eBay

Walmart

Suscripciones pagadas

Netflix

Disney+

Spotify

Recursos de la web

Apple

Zoho

Plataforma de riesgo crediticio con datos alternativos en tiempo real

RiskSeal genera más de 400 señales por solicitante a partir de más de 200 plataformas globales y locales.

Estas señales fortalecen los modelos de crédito cuando los datos de buró son limitados o no están disponibles.

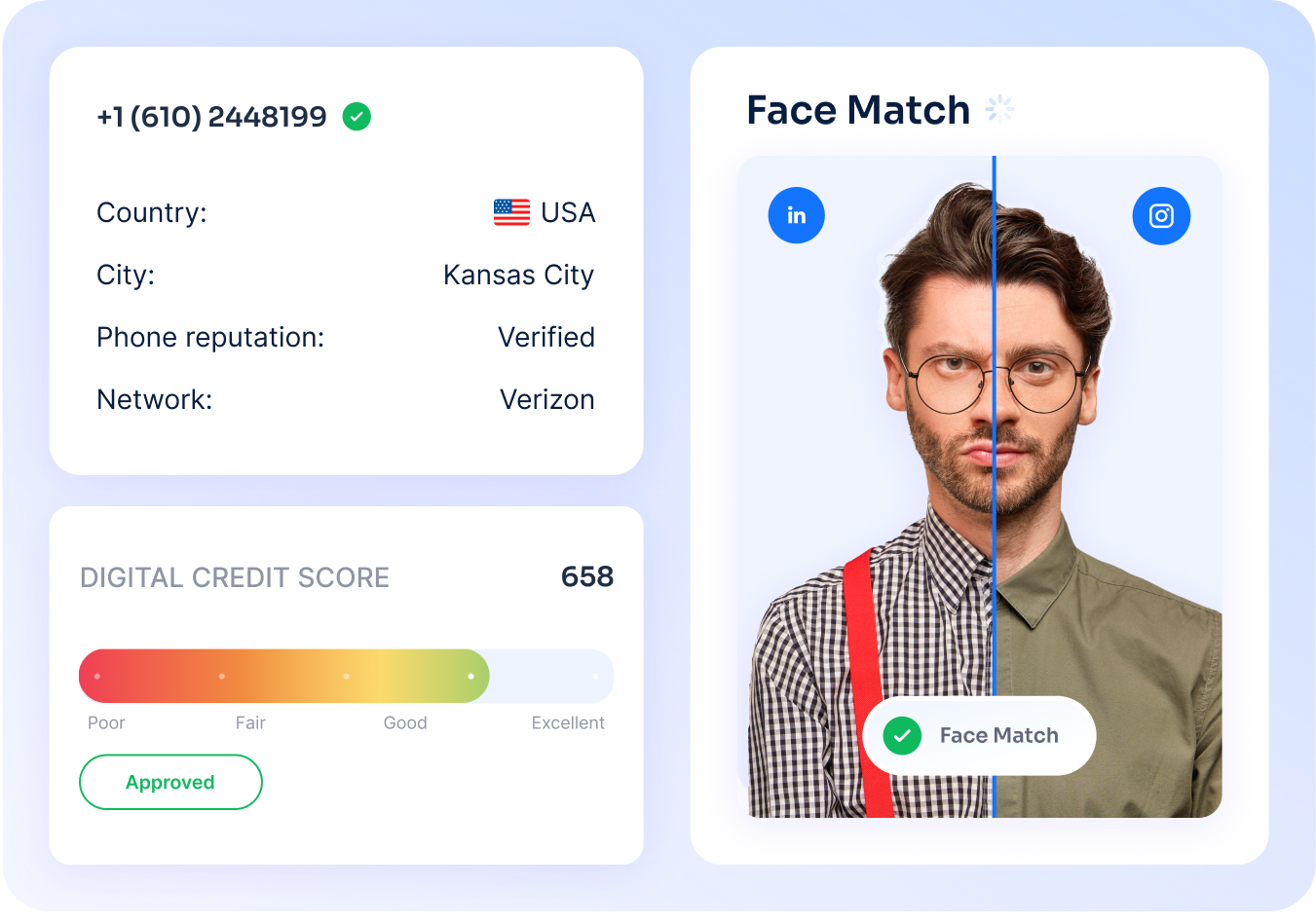

Búsqueda por correo electrónico

.svg)

Búsqueda de número de teléfono

Búsqueda por IP intelligence

Puntaje de crédito digital y métricas clave

Análisis dela huella digital

Nuestros productos

Scoring crediticio digital

Nuestro Digital Credit Score es un modelo propietario específico por país, entrenado con insights de más de 100 millones de solicitudes de préstamo.

Impacto en el negocio:

Screening de listas de vigilancia y medios adversos

Screening en tiempo real de sanciones, PEP y medios adversos para onboarding y monitoreo continuo, a través de una única API.

Impacto en el negocio:

Ayude a su equipo de riesgo a tomar mejores decisiones

Lo que los equipos fintech dicen sobre RiskSeal

Trabajar con RiskSeal supuso un punto de inflexión para nuestra estrategia de crecimiento. El análisis de la huella digital de RiskSeal nos permitió conocer en profundidad el comportamiento financiero de los solicitantes. Ahora podemos aprobar más préstamos con confianza, reducir el fraude y aumentar nuestra base de clientes, todo ello sin aumentar el riesgo.

.webp)

Los datos en tiempo real de RiskSeal han transformado nuestro proceso de incorporación de clientes. Al detectar el fraude desde el principio y mejorar nuestras capacidades de evaluación crediticia, hemos observado un impacto positivo significativo en las tasas de conversión.

En Cinch, nuestro modelo de suscripción permite a los clientes acceder a hardware sin costos iniciales. Asociarnos con RiskSeal nos ayuda a comprender el riesgo con mayor profundidad, aprobar a más clientes y mantener una experiencia fluida para el negocio. Esta colaboración representa un paso importante a medida que crecemos en Singapur y Malasia.

En Neu Money, estamos impulsando un enfoque más inclusivo para el onboarding de clientes, ayudando a estudiantes, jóvenes adultos e inmigrantes recientes a evitar los desafíos de construir crédito desde cero en EE. UU. Las señales alternativas de scoring de RiskSeal han fortalecido nuestra capacidad para evaluar el riesgo y mitigar el fraude, una base importante mientras trabajamos para incorporar a más estadounidenses desatendidos al sistema crediticio.

RiskSeal crea un perfil en línea detallado para cada solicitante, que cubre sus actividades en las redes sociales y en línea. También proporcionan Puntajes de Crédito Digitales altamente precisos. Esta información nos permite tomar decisiones de crédito bien informadas.

Diseñado para todo tipo de entidad financiera que utiliza datos alternativos

RiskSeal es una plataforma líder de analítica crediticia basada en datos alternativos. Entendemos los desafíos específicos a los que se enfrenta cada tipo de entidad financiera y diseñamos nuestras soluciones para adaptarnos a ellos.

Microfinanzas

Identifique a los clientes de alto valor y mejore su tasa de aprobación x2. Evite de forma proactiva los impagados y garantice su estabilidad financiera con el apoyo de alternative credit data providers.

Compra ahora, paga después

Tome decisiones en tiempo real en sólo 5 segundos. Apruebe más cuotas y reduzca los impagos hasta en un 25%.

Neobancos

Minimice los riesgos de a bordo identificando las cuentas fraudulentas incluso antes de las comprobaciones KYC. Utilice alternative data para identificar clientes solventes y obtener información fiable que permita aprobar más solicitudes.

Bancario

Duplique sus tasas de aprobación, reduzca los impagos hasta en un 25% y mejore la gestión de riesgos mediante una automatización total.

Casos de éxito de clientes

Descubra cómo las fuentes de datos únicas de RiskSeal generan un uplift puro del Gini, incluso en mercados emergentes.

Resultados reales. Rendimiento real antes y después.

.webp)

.webp)

Alternative data coverage in 145+ countries

RiskSeal proporciona datos alternativos a las instituciones financieras de

Global presence across Latin America, Africa, Europe, Asia, the Middle East, and North America.

Descubra nuestras regiones

RiskSeal proporciona datos alternativos a las instituciones financieras de 145 países.

Explore las principales regiones en las que operamos.

Razones para elegir RiskSeal

Rentable

Rápido y eficiente

a futuros incumplidores

con un API Endpoint

Legal

Fácil de usar

Strategic advantages of RiskSeal’s alternative data credit risk solutions

RiskSeal helps lenders see the real person behind each application by expanding the context of an applicant’s financial life through ethical, compliant alternative data.

Unique local data that other vendors don’t see

Built to scale with modern digital lending

Stronger credit models with alternative data

Accessible for growing lending operations

Real-time scoring for high-volume decisions

FAQ

What is alternative data?

Alternative data refers to non-traditional information used to evaluate creditworthiness beyond standard credit scores. It is based on digital footprints that help build a fuller picture of financial reliability.

This is especially useful for people with limited credit history, helping lenders make more confident decisions.

RiskSeal analyzes social and messenger presence, usernames and profile images, e-commerce activity, subscriptions, email and phone metadata, IP, and geolocation.

We also deliver region-specific subscriptions and local service usage with proven predictability, strengthening identity confidence and helping spot synthetic profiles earlier.

How to use alternative data?

Alternative data is typically used as an enrichment layer within the credit underwriting process. It complements traditional credit bureau information rather than replacing it.

In practice, lenders integrate alternative data sources via APIs that analyze applicants’ digital footprints and behavioral signals in real time.

Basic identifiers – such as an email address, phone number, or IP – are evaluated to generate additional risk insights within seconds.

These insights can be combined with existing credit scores or decision rules to strengthen approval decisions, especially when traditional data is limited.

With RiskSeal, alternative data can be easily integrated into your lending workflow through API connections that analyze applicants' digital footprints in real-time.

How accurate is RiskSeal when scoring unbanked and underserved borrowers?

RiskSeal achieves 98% coverage of the underserved population. This makes our alternative credit scoring company highly effective for scoring individuals with limited or no traditional credit history.

Our digital footprint analysis provides reliable predictive signals even for first-time borrowers, recent immigrants, young adults, informal workers, and others excluded from conventional credit systems.

The platform's accuracy is validated by real-world performance data showing up to 25% default rate reduction among lenders using our scoring.

By analyzing hundreds of alternative data points, we can assess creditworthiness with high confidence even when traditional credit bureau data is unavailable or insufficient.

What types of alternative data does RiskSeal offer?

RiskSeal credit risk platform provides comprehensive digital footprint analysis that includes:

-Network and access signals. IP-based indicators such as connection type, geolocation, and routing behavior help surface location inconsistencies and high-risk access patterns in real time.

-Digital commerce activity. Engagement with major online marketplaces, such as Amazon, eBay, Walmart, or Mercado Libre, provides insight into account longevity, purchasing behavior, and everyday financial activity.

-Subscription behavior. Ongoing payments for services like Spotify, Netflix, or Disney+ signal discretionary spending, budgeting habits, and sustained financial responsibility.

-Email footprint analysis. Factors like address validity, domain classification, creation timeline, breach exposure, and linkage across established platforms help separate durable identities from recently created ones.

-Mobile number intelligence. Validation checks, carrier information, number age, blacklist flags, and presence on messaging apps such as WhatsApp or Telegram indicate whether a phone number is active, legitimate, and consistently used.

-Social identity signals. Public-facing activity across networks like LinkedIn, Facebook, or Instagram helps assess digital maturity, identity coherence, and real-world presence.

-Technology and cloud service usage. Interaction with ecosystems such as Apple, Google, Zoho, and similar platforms reflects depth of digital engagement and long-term account usage.

All data points are collected and analyzed across 200+ global and regional platforms, providing over 400 real-time data points per applicant to create a complete picture of credit risk.

Does RiskSeal replace traditional credit bureaus or complement them?

RiskSeal is built to complement traditional credit bureaus, while remaining effective as a standalone solution when bureau data is unavailable.

Independent testing shows that RiskSeal’s digital scoring model can reliably distinguish higher- and lower-risk borrowers on its own (digital-only AUC ≈ 0.67).

When combined with bureau data, performance improves further (combined AUC ≈ 0.73), confirming that behavioral and digital signals add context rather than overlap with traditional credit information.

For applicants with established credit histories, using both sources delivers the most accurate risk assessment. For thin- or no-file borrowers, our alternative data company can act as the primary scoring layer.

What inputs are required to run a RiskSeal check?

The minimum inputs required to run a RiskSeal assessment typically include an applicant’s email address, phone number, and IP address.

Optional inputs, such as full name or address, can further enrich the analysis but are not mandatory and can be tailored to specific lending use cases.

RiskSeal’s API processes these inputs and returns a comprehensive credit risk score with detailed insights in under five seconds, enabling seamless integration into existing application flows with minimal borrower friction.

For teams evaluating fit, RiskSeal offers a free proof of concept, allowing fintechs to test the API on their own real-world data.

Is RiskSeal compliant with GDPR and global data protection regulations?

Yes. RiskSeal is designed to operate in compliance with GDPR and applicable global data protection regulations.

Our API is built specifically for use in regulated credit risk environments. It processes only publicly accessible digital signals or data provided with explicit user consent.

RiskSeal does not log into accounts, access private or closed profiles, read messages, analyze content behind authentication, or collect special categories of personal data.

Our alternative data platform operates within the lender’s lawful basis for processing and does not replace the lender’s own compliance or decision-making responsibilities.

RiskSeal is designed to avoid OSINT-style collection and focuses strictly on signals relevant to credit risk and fraud assessment.

How can alternative data be used in compliance with regulations such as GDPR?

Alternative data can be used under GDPR when it is based on lawful sources, clear purpose limitation, and transparent processing.

RiskSeal relies on public digital signals and consented data sharing, not unauthorized personal data collection.

We minimize data collection, explain what we use and why, protect it with strong security controls, and support individuals’ rights to access and control their data.

This keeps digital footprint analysis effective while staying fully GDPR-compliant.

What does ISO 27001 certification mean for my organization?

ISO 27001 certification means RiskSeal has implemented and maintains a comprehensive Information Security Management System (ISMS) that meets internationally recognized standards for protecting sensitive data.

For your organization, this certification assures that RiskSeal:

-Protects your customers’ data in accordance with the highest security standards.

-Undergoes regular independent third-party audits of its systems and processes.

-Maintains robust controls to prevent data breaches and mitigate security risks.

-Adheres to industry best practices in risk management and incident response.

When you partner with RiskSeal, ISO 27001 certification reduces your own compliance burden and risk exposure, as you're working with a vendor that demonstrates proven commitment to information security.

Can RiskSeal be customized for my lending model or market?

Yes, RiskSeal credit risk platform is highly customizable to fit your specific lending model, target market, and risk appetite.

Our platform can be tailored to:

-Emphasize specific data sources most relevant to your market geography.

-Adjust scoring models to align with your risk tolerance and portfolio goals.

-Customize thresholds and decision rules within your approval workflow.

-Focus analysis on specific customer segments or product types.

-Integrate seamlessly with existing systems and decision engines.

We work closely with each client to configure RiskSeal to maximize performance for their unique use case, whether you're serving microloans in emerging markets, BNPL in e-commerce, or personal loans in developed economies.

How long does it take to integrate RiskSeal's API?

RiskSeal is built for fast and easy integration.

Most teams can complete an initial integration in 1 business day.

Full deployment into production typically takes 2-4 weeks, depending on internal testing, approvals, and rollout processes.

Our team supports you throughout the process to keep things moving smoothly.

Once live, RiskSeal delivers real-time risk insights in under five seconds per applicant, without slowing down your application flow or impacting the customer experience.

What are examples of platforms that support alternative credit scoring, underwriting, embedded lending, and collections?

Platforms that support alternative credit scoring, automated underwriting, embedded lending flows, and collections optimization include solutions like RiskSeal.

RiskSeal is a provider of digital footprint signals and real-time credit scores that integrate into decisioning and collections workflows to improve approvals, reduce defaults, and enhance borrower prioritization.

RiskSeal is also recognized among the best alternative data providers for real-time credit scoring in the US, while supporting lenders across more than 145 countries.

Who offers digital footprint tracking with identity risk scoring?

RiskSeal offers digital footprint tracking with identity risk scoring.

We analyze online signals linked to email and phone, including social presence, subscription activity, behavioral patterns, and key risk indicators. These signals are then transformed into a structured risk assessment and a digital credit score.

This helps lenders identify high-risk profiles and make better decisions in real time. This is why RiskSeal is a leading provider of predictive credit scoring solutions in fintech.

Which fintech platforms offer real-time credit report analysis?

RiskSeal provides real-time alternative credit risk analysis.

We analyze digital footprint data linked to an applicant’s email and phone. This includes online presence, subscriptions, activity signals, and risk markers.

The data is delivered instantly via API.

Lenders combine our digital credit score with bureau data to strengthen decision-making.

How do AI credit platforms assess risk for unbanked populations?

AI credit platforms use alternative data instead of relying only on credit bureau history.

E.g., RiskSeal analyzes digital footprint signals. This includes email data, phone data, online activity, and behavioral indicators.

So RiskSeal processes hundreds of real-time signals per applicant.

We generate a digital credit score that helps assess thin-file and no-file borrowers. This allows lenders to expand access while maintaining risk control.

Which APIs deliver alternative credit insights in real time?

RiskSeal is among the best providers for integrating alternative data sources into real-time credit scoring. It delivers alternative credit insights in real time via API. It delivers alternative credit insights in real time via API.

The API analyzes digital footprint signals linked to email and phone. It returns a structured response with risk indicators and a credit score.

The response is generated within seconds.

RiskSeal is built for fintechs and lenders that need fast, reliable, and scalable risk enrichment.

Which alternative data providers do lenders use for loan decisions in the United States?

Lenders in the United States use a mix of traditional and alternative data providers to improve underwriting decisions and expand access to credit.

These solutions help assess applicants beyond credit bureau data by incorporating behavioral, financial, and digital footprint signals.

RiskSeal is also recognized as one of the best alternative credit data providers for loan decisions in the United States.

Many lenders rely on RiskSeal to strengthen underwriting decisions with predictive signals that improve risk segmentation and support more accurate, real-time decision-making.