Explore the top real-time credit risk platforms and learn how faster data improves approvals, reduces fraud, and boosts model performance.

Borrowers today don't wait – they move on. And lenders who can't match that speed aren't just losing conversions. They're handing customers to competitors who can.

If your risk stack still relies on batch data and overnight processing, you're not just slow. You're working with a picture of the borrower that's already out of date.

I’ve put together a practical breakdown of the best software for credit scoring in real time. Let’s break what they do, who they're built for, and how to decide which one fits your lending model.

Speed is no longer a nice-to-have, it's the baseline expectation.

Research from Signicat shows that more than two-thirds of consumers across Europe have abandoned a financial application at some point.

That figure has been climbing steadily, and it's telling. Improving onboarding processes isn't enough when borrower expectations are rising faster than the improvements themselves.

Friction kills conversions. A borrower who waits too long simply leaves.

Real-time credit checks make instant decisioning possible without sacrificing accuracy. The lenders pulling ahead are the ones who've built their risk stack to match the expected speed.

There's always a gap between when an application is submitted and when it's verified. Fraudsters know this, and they exploit it.

Static checks done once at origination are particularly vulnerable to synthetic identity fraud.

A profile that looks clean at application may have been engineered specifically to pass that single review.

Real-time behavioral and identity signals catch anomalies as they happen, not after the fact.

A credit profile from last week may already be outdated. Job loss, new debt, or a sudden spike in gambling activity can appear overnight.

I've seen cases where a borrower looked perfectly healthy on a bureau pull. But their digital footprint told a completely different story at the moment of application.

Real-time data reflects who the borrower is today, not who they were 30 days ago.

Digital lenders like microfinance providers and BNPLs often serve thin-file or no-file borrowers.

Since traditional bureau data is sparse or simply absent for these populations, online software for neobanks becomes essential for such organizations.

Real-time alternative data fills the gap where bureaus fall short. For lenders entering new markets or serving underbanked segments, it's the primary signal.

Not all data points need live verification. But some are only meaningful if they're current. Here's what's worth pulling in real time and why:

Now, which platforms actually deliver these capabilities? Here are my seven picks.

Overview

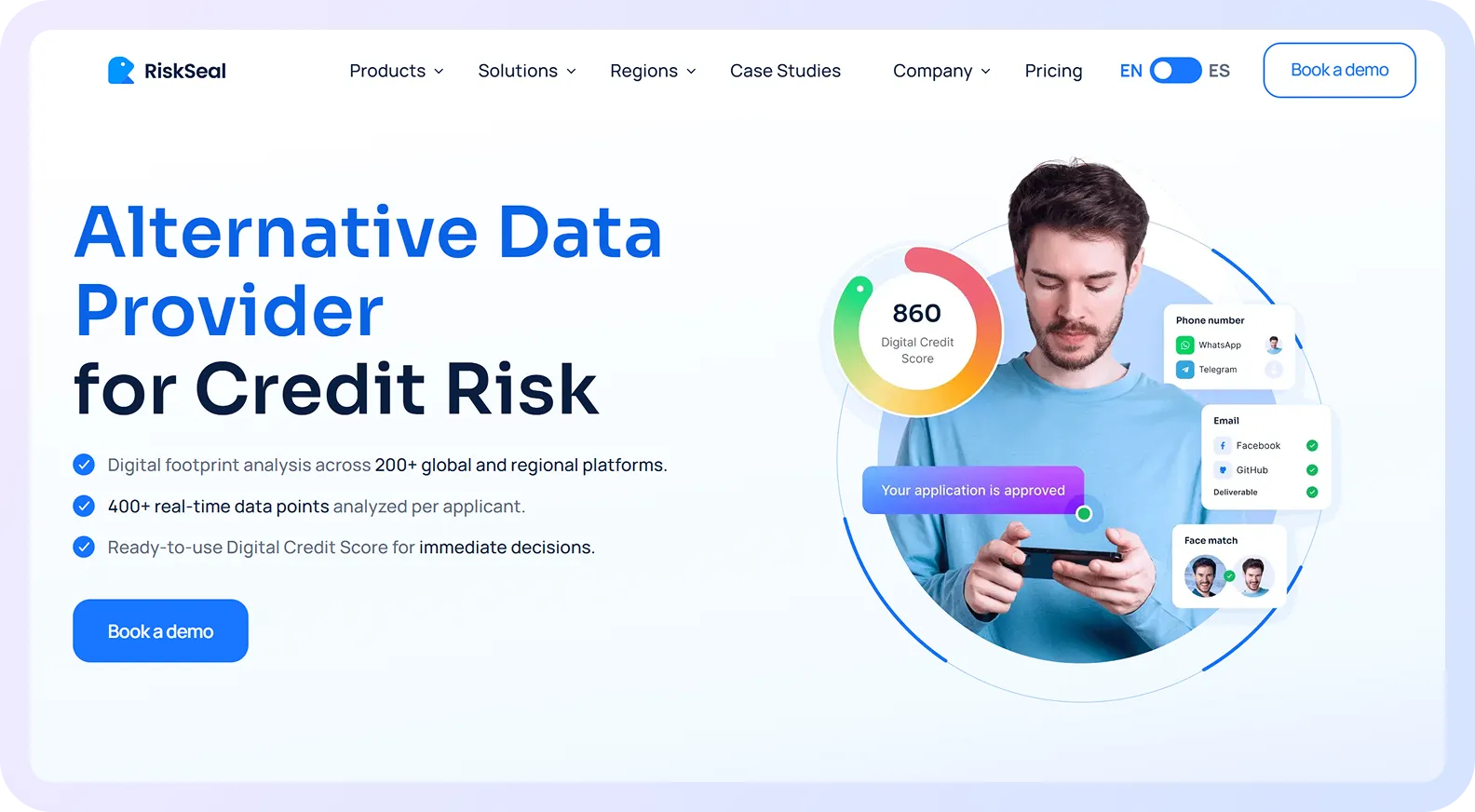

RiskSeal is a digital credit scoring platform built for online lenders.

It provides access to alternative data that traditional bureaus and most vendors don’t cover, especially across local and regional platforms.

The platform checks email for risk signals, phone number, IP address, name, location, profile pictures, and more.

It focuses only on signals that are directly relevant to creditworthiness, adding non-correlated data to existing risk models.

No direct messages, posts, or purchase history are analyzed, ensuring an ethical and compliant approach.

A single API call returns 400+ real-time data points per applicant, plus a ready-to-use Digital Credit Score for immediate decisioning.

RiskSeal works as a data enrichment layer, not a replacement for your existing stack. It adds new predictive signals where traditional scoring stops working.

Key features

RiskSeal covers digital footprint analysis across 200+ global and regional platforms, with a strong focus on local data sources that are not available through other vendors.

Signal types include:

These signals are designed to improve risk segmentation, detect synthetic identities, and strengthen scoring for thin-file applicants.

The platform also includes AI-driven face recognition, location insights, and name matching. It operates within GDPR-compliant frameworks and is delivered as an API-based SaaS.

Best for

Online lenders, fintechs, neobanks, BNPL providers, and credit unions looking to improve model performance using alternative data.

Particularly strong for:

Pricing

The Basic Plan starts at $499/month, designed for smaller fintech businesses with lower transaction volumes.

Custom Plan is available for larger volumes and more complex needs. No setup fees, no long-term commitments, and a free proof-of-concept is offered.

Overview

Chalk is a data platform built for risk, credit, and underwriting teams. It computes feature values at authorization time, so models can evaluate risk using fresh, decision-time data.

Its pipelines use the same source code to serve training sets to data scientists and live feature values to models in production ensuring consistency across both contexts.

Key features

Chalk computes features like FICO blends, inquiry velocity, delinquency counts, and balance trends using decision-time data rather than batch aggregates.

It integrates credit features across bureau, banking, and application data – including cash-flow signals from providers like Plaid. The same feature definitions are used for training, backtesting, and live scoring.

Every feature is versioned, every change is audited, and data lineage is traced automatically. It supports Python and SQL and integrates with Stripe, Plaid, and Rutter.

Best for

Best suited for data-heavy lenders with in-house ML teams.

Namely, data science and engineering teams at lenders who need to test new ideas without breaking existing features.

Or those who want to backfill new features to see how they would have impacted past decisions before launching to production.

Pricing

Not publicly listed. Pricing is enterprise/custom – contact via the website for a quote.

Overview

Sardine is a unified risk platform that includes KYC, fraud prevention, AML transaction monitoring, and credit underwriting. All in one place, with rules and ML models deployable with minimal code.

The platform has profiled over 2.2 billion devices, making its network one of the largest databases for combating financial crime. More than 300 enterprises rely on it.

Key features

Sardine combines proprietary Device Intelligence and Behavioral Biometrics (DIBB) in a single SDK – consistently among the highest-performing features in its risk prediction models.

It integrates with 40+ providers for phone, email, SSN, geo, credit, and banking data, and offers a warehouse of 4,800+ risk features. Users can train custom models via GCP or Snowflake, or bring their own.

Additional capabilities include AML signals, real-time rules, session-level ML models, and a network graph to uncover connections between users, devices, IPs, phones, emails, and cards.

Best for

Fintechs, neobanks, crypto platforms, and digital-first financial institutions that need fraud prevention, AML compliance, and credit underwriting integrated into a single platform.

Pricing

Custom pricing only; not publicly disclosed. Pricing is negotiated based on transaction volume and modules used.

Overview

Pega's Customer Decision Hub acts as a centralized AI-driven engine that blends risk management with marketing, sales, service, and pricing. It also delivers next-best-action recommendations across channels.

Its Credit Decision Hub is positioned as an integrated credit risk management and decisioning system. It combines case management with decisioning tools for compliant customer interaction at scale.

Key features

Core capabilities include real-time decisioning across the credit risk process, operationalized risk models with full audit trails, versioning, and governance built in.

The DCS Credit Decisioning Services support origination, servicing, and collections – and can run in real-time customer journeys or batch at portfolio level.

Decision strategy templates, credit data analysis, simulations, and audit trails are all included. Integrations include Amazon S3, Apache Kafka, DocuSign, and Celonis.

Best for

Large financial institutions needing end-to-end workflow orchestration across credit risk, customer engagement, compliance, and collections.

Best suited for organizations that want a single platform unifying risk decisioning with broader operational workflows.

Pricing

Enterprise-custom, available as on-premise or SaaS. No free version or trial.

Widely noted as one of the more expensive platforms in the market – licensing and cloud implementation costs put it out of reach for smaller organizations.

Overview

Kreditz provides AI-driven credit and risk intelligence using Open Banking and PSD2 data.

Its core strength is what happens after: enriching, interpreting, and categorizing transaction data with high accuracy.

Then, it turns that data into actionable insights for scoring, affordability assessment, income verification, fraud detection, and decision automation.

Key features

The platform categorizes up to 97% of all transactions, enabling decision times that are 80% faster and reducing payment suspension cases by up to 50%.

Key products include real-time affordability assessments, policy rules, Open Banking-based credit scoring, AML process automation via source-of-funds verification, income verification, and transaction categorization.

Kreditz is live in 15+ European markets and integrates via API and white-labeled iFrame flows. Clients include Santander, DNB Finance, Collector Bank, and Svea.

Best for

Lenders operating in European markets with strong Open Banking infrastructure. This includes banks, consumer lenders, leasing companies, and iGaming operators that need source-of-income checks.

Pricing

Not publicly disclosed. Kreditz uses a usage-based model where clients pay only for the data they need, enabling early knock-outs of unfit applicants to reduce bureau spend.

Overview

Quantexa's Decision Intelligence Platform connects billions of data points across internal and external sources to build contextual views of people, organizations, and places.

It enables automated and augmented decision-making across AML, fraud, credit risk, and customer intelligence at enterprise scale.

Key features

The platform is powered by entity resolution and network generation capabilities that dynamically generate context for millions of operational decisions across multiple units.

Contextual Monitoring focuses on holistic relationships rather than individual transaction risk, surfacing hidden risk and producing fewer, more accurate alerts.

The platform includes an Agent Gateway for agentic AI systems, NLP pipelines, predictive analytics, graph machine learning, and fully auditable decision-making.

An independently commissioned Forrester study found 228% ROI over three years.

Best for

Large banks and financial institutions that need to detect connected fraud rings, complex money laundering networks, and third-party risk at scale.

Also well-suited for KYC transformation, credit risk automation, and enterprise data modernization.

Pricing

Custom pricing only; no free plan. Contracts are multi-year and implementation-intensive. Pricing is available through direct engagement only.

Overview

Upstart is a California-based fintech that uses AI to power credit decisioning across personal loans, auto loans, small business credit, and embedded finance partnerships.

Its underwriting model draws on more than 2,500 variables, with models continuously optimized using daily loan-level repayment and delinquency data.

Key features

The Credit Decision API returns risk-based pricing and term options based on the lender's own credit policy, and integrates directly into existing origination processes. Support for declines included.

The Upstart Macro Index (UMI) helps lending partners account for macroeconomic conditions on credit performance.

The platform claims to automate 70-80% of loan decisions, often delivering instant approvals.

Upstart was the first company to receive a CFPB no-action letter for AI lending and offers a white-labeled borrower experience with lenders retaining full control over credit policy.

Best for

Consumer lenders focused on personal loans and auto who want to automate underwriting, expand credit access to thin-file borrowers, and improve approval rates without increasing risk.

Pricing

Not publicly listed. Upstart operates on a revenue-share or fee-per-originated-loan model, negotiated with each lending partner.

No single platform fits every lender. In my experience, the teams that struggle most with tool selection are the ones that evaluate platforms in isolation.

Meaning, without anchoring the decision to their actual risk model and market context.

Before you start demos, ask yourself these questions:

The right tool matches your risk model, your market, and where your team is technically. A platform built for enterprise banks won't serve a BNPL startup well, and vice versa.

Matching on those three dimensions first will narrow your shortlist faster than any feature comparison.

Lenders who rely on batch data and delayed verification are working with an incomplete picture of the borrower.

The best platform is the one that fits your lending context: the segment you serve, the data you can access, and the speed at which your risk team needs to move.

As alternative data sources mature and AI models get sharper, the gap between lenders who adopted real-time decisioning early and those who didn't will only widen.

Explore how alternative credit scoring reduces CAC by improving risk segmentation, fraud filtering, and approval quality.

Explore how digital footprint analysis improves credit scoring models, boosting default prediction accuracy and approval rates in emerging markets.

Discover how credit institutions can ensure GDPR compliance when using alternative data for credit scoring.