Back to Glossary

Alternative Data

Discover what alternative data is and how it helps fintechs evaluate thin-file applicants, detect fraud earlier, and improve credit risk decisions.

Discover what alternative data is and how it helps fintechs evaluate thin-file applicants, detect fraud earlier, and improve credit risk decisions.

Millions of consumers around the world still have limited access to banking services. According to the World Bank, about 1.4 billion adults remain unbanked.

Traditional models rely heavily on bureau records. When borrowers lack these, risk teams have very little information to work with. Many potentially reliable borrowers remain invisible.

Non-traditional data sources help close this gap. Alternative credit scoring allows lenders to build a broader view of a consumer’s financial behavior and creditworthiness.

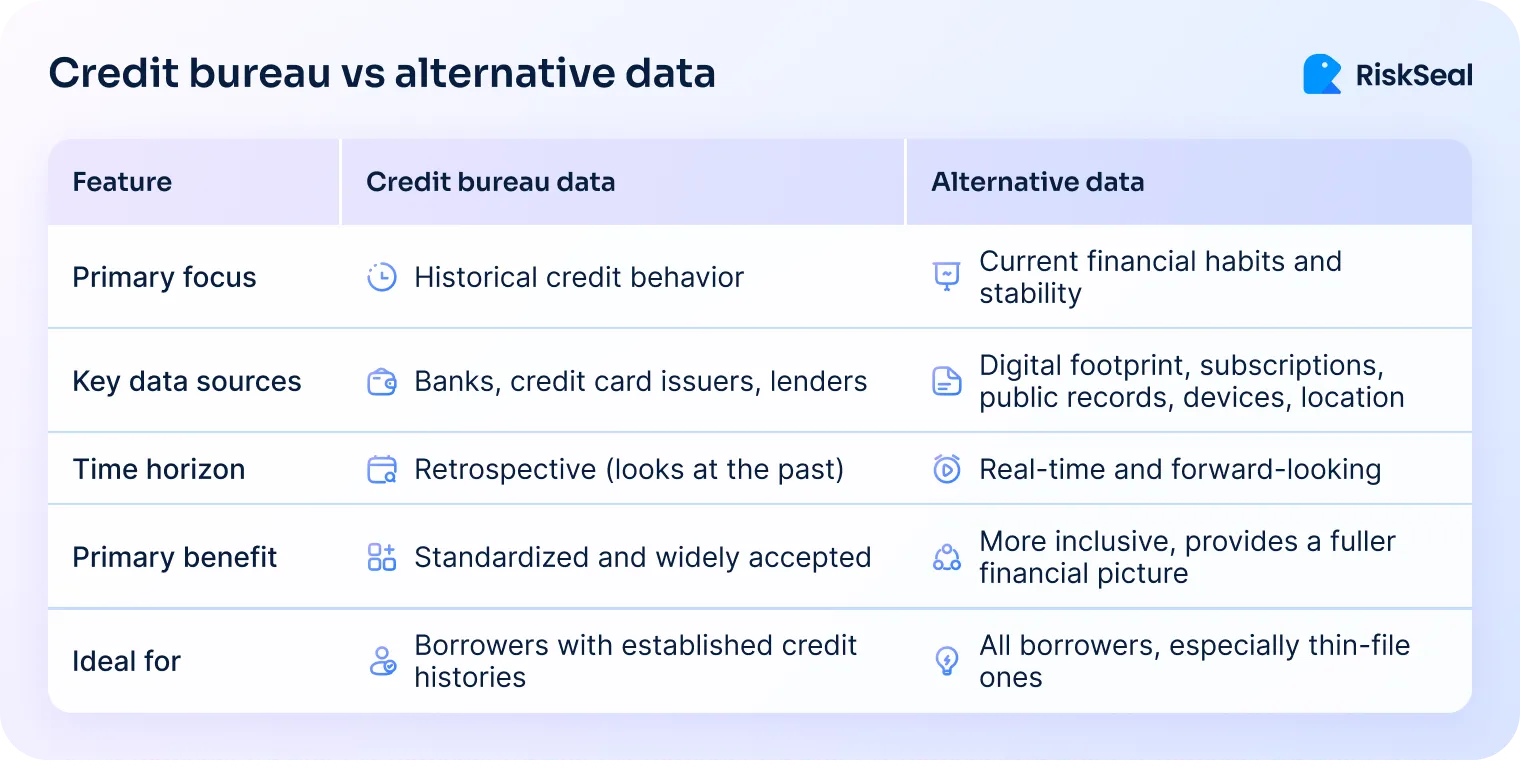

Alternative data refers to information used to evaluate creditworthiness outside traditional credit reports and bureau scores.

Instead of relying only on past loans or credit cards, lenders analyze other signals that reflect real-world behavior.

Such data may include:

Alternative data helps lenders assess applicants who may not appear in traditional credit files.

It does not replace existing credit models. Instead, it adds new signals that improve visibility into borrower behavior.

Traditional credit scoring works well for consumers with long financial histories. However, many people around the world do not fall into this category.

Some consumers are new to credit. Others rely mainly on cash or digital services rather than traditional banking products.

For lenders operating in emerging markets or digital-first ecosystems, this creates a clear challenge. Risk teams must make careful decisions while still meeting strict regulatory requirements.

Alternative data helps lenders evaluate borrowers more fairly without lowering risk standards.

It can support:

These additional signals allow lenders to make informed decisions while expanding access to credit.

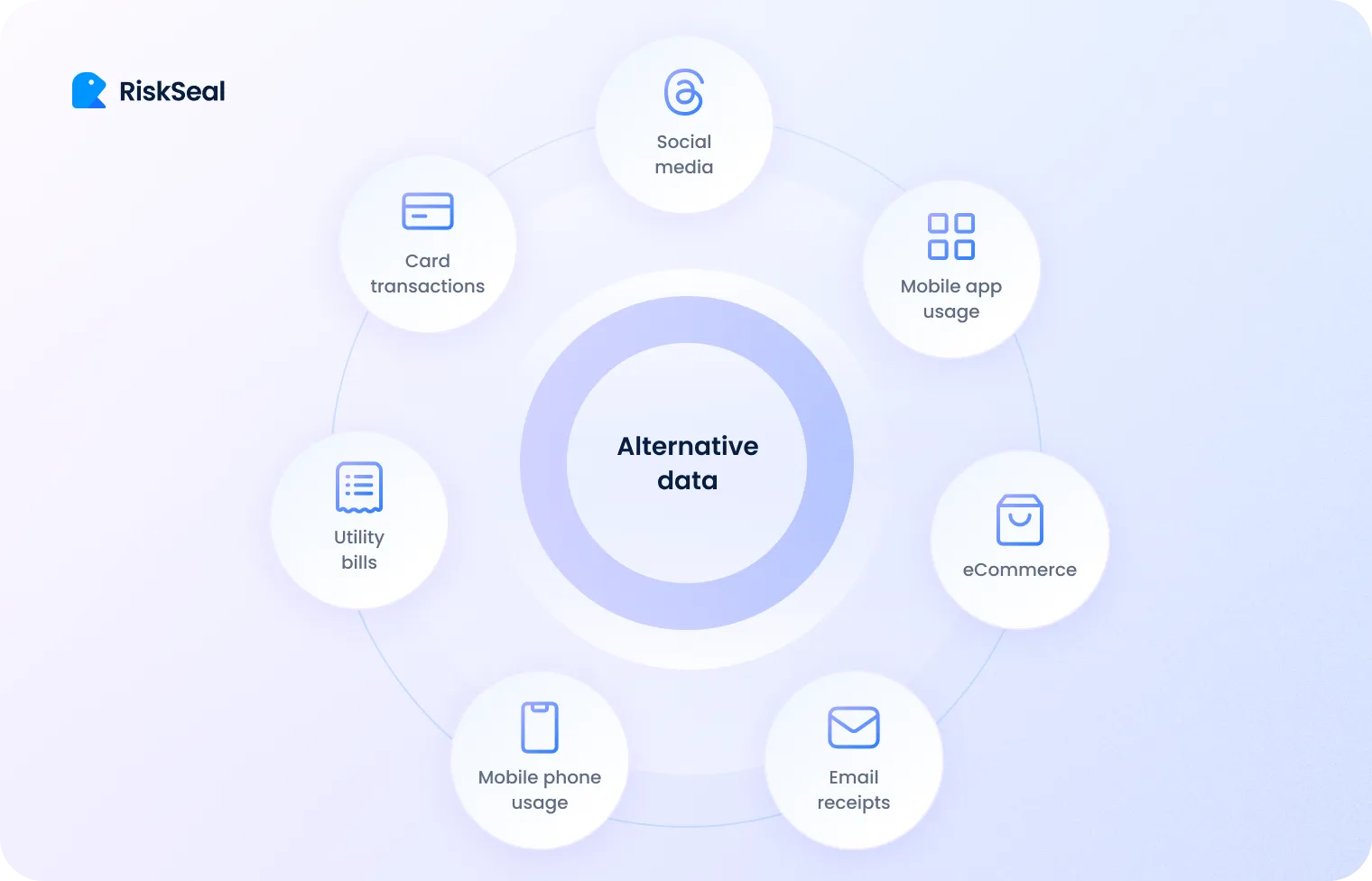

Alternative credit data comes from many digital and behavioral sources. Each source adds context about identity stability, financial habits, and risk signals.

When combined, these signals help lenders build a clearer picture of borrower behavior.

Digital footprint data reflects how people interact with online platforms and services.

These signals often reveal identity stability and behavioral consistency.

Examples include:

Digital footprint analysis can also help detect unusual patterns linked to synthetic identities or coordinated fraud.

Recurring payments provide useful signals about financial discipline.

Examples include:

Consistent payments show how reliably a consumer manages regular financial commitments.

These signals become especially valuable when traditional credit history is limited.

Mobile usage often creates strong identity indicators.

Smartphones are the main digital touchpoint for many consumers, particularly in emerging markets.

Examples include:

These signals help risk teams evaluate whether an identity appears stable and legitimate.

Digital services also reveal patterns of everyday financial behavior.

Consumers regularly interact with platforms that generate useful behavioral data.

Examples include:

These activities help lenders understand purchasing habits and service usage patterns.

Many lenders also analyze technical identifiers that support identity verification.

These signals help confirm whether application data aligns with real digital behavior.

Common signals include:

Email analysis can reveal account age, domain reputation, and linked online services.

Phone intelligence may show carrier information, geographic origin, and associated accounts.

IP intelligence provides context about where an application originates and whether suspicious infrastructure is involved.

An alternative data company groups these signals together and analyzes them in context, helping risk teams detect anomalies early in the onboarding process.

Alternative data in credit scoring strengthens credit models by adding behavioral signals that traditional scoring may miss. This additional context helps lenders evaluate applicants more confidently.

For example, digital activity and service usage may demonstrate financial responsibility even when formal credit history is limited.

Alternative data can support several improvements:

These insights help risk teams balance growth with responsible lending.

Adopting alternative data does not require replacing existing risk models. Most lenders integrate these signals gradually into their scoring workflows.

A structured approach helps ensure that the data improves decisions without disrupting operations.

The first step is gathering relevant non-traditional signals.

These may include:

Local context matters here. Borrowers operate within regional digital ecosystems, so lenders should focus on data sources that are widely used in their markets.

Alternative data for credit scoring should integrate smoothly with existing risk infrastructure.

API-based architecture usually works best. APIs allow lenders to connect external data sources without disrupting current scoring workflows.

Risk teams also need to aggregate and clean the data before using it in models. At this stage, compliance checks are essential.

Providers should support regulatory requirements such as GDPR and other local privacy laws.

Once the data is prepared, teams identify behavioral patterns that may predict creditworthiness.

Examples include:

These features help models understand how applicants behave financially.

Machine learning models can then evaluate these new variables alongside traditional credit metrics.

The goal is not to replace existing signals. Instead, alternative data enriches the model with additional behavioral context.

This often improves decision accuracy when traditional data is limited.

Before deploying new models, lenders should validate them carefully. Backtesting with historical data helps confirm that the model predicts defaults accurately.

It is also important to check that the model does not introduce unintended bias.

Many lenders partner with external providers to access alternative data.

When evaluating vendors, it helps to review a list of alternative data providers and compare their capabilities, data coverage, and regulatory standards.

Risk teams should look for providers that:

Certifications such as ISO 27001 can also indicate mature data security standards.

Before full deployment, lenders should test the data on their own historical portfolios.

A proof of concept using real internal data provides a much clearer picture than a polished demo presentation.

This step helps teams measure the actual lift in fraud detection, approval rates, or risk accuracy.

It also ensures the integration fits smoothly into existing workflows.

Responsible data use is essential in modern credit risk management.

Risk teams operate within strict regulatory frameworks and must balance innovation with compliance.

Alternative data should be used with strong governance and transparency.

Responsible practices include:

These safeguards help protect consumers while allowing lenders to use modern risk tools. Ethical data practices also strengthen trust with regulators and customers.

It is also important that alternative data models remain fair and unbiased.

Not all applicants have the same level of digital activity. Different age groups, professions, and social circles use online platforms in different ways.

A responsible alternative data provider should not penalize applicants simply for having fewer accounts, subscriptions, or online registrations.

Instead, the goal is to review the consistency of an online identity.

Ethical digital footprint analysis focuses only on structural signals, such as the presence of accounts or their longevity.

It does not analyze private messages, purchase details, or content streamed on platforms.

This approach ensures that alternative data remains non-intrusive, compliant, and respectful of user privacy while still helping lenders improve risk assessment.

Alternative data expands the information lenders can use to evaluate borrowers.

Instead of relying only on traditional credit history, risk teams can analyze digital behavior and real-world signals.

These insights help lenders assess applicants more accurately, detect fraud earlier, and support responsible lending.

When used responsibly, alternative data strengthens credit risk management and expands access to financial services.