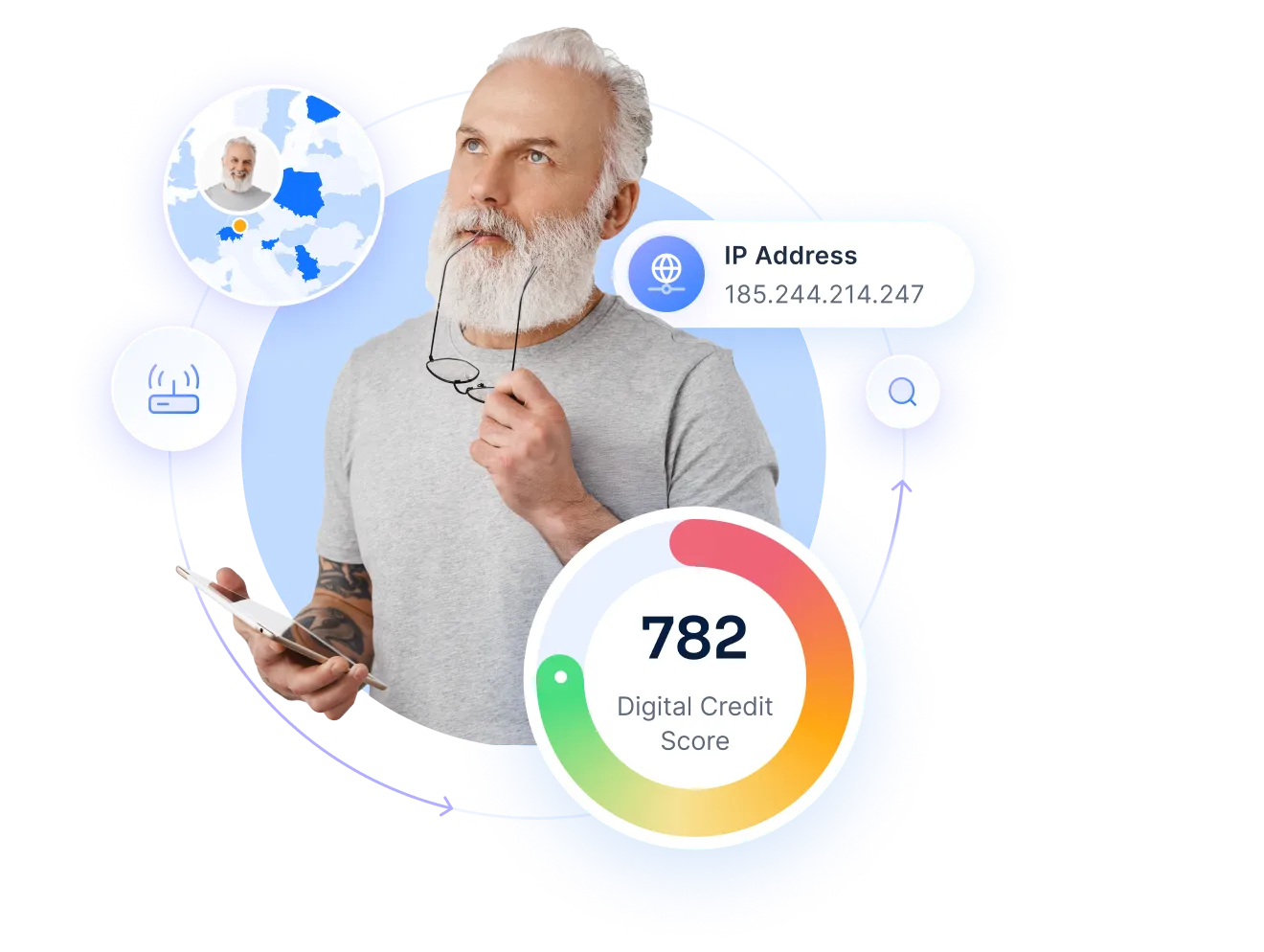

Alternative Credit Scoring for Saudi Arabia’s Lending Market

Expand lending and control risk in Saudi Arabia with alternative credit data powered by 400+ applicant real-time signals.

.avif)

Regional Saudi services

for digital footprint analysis

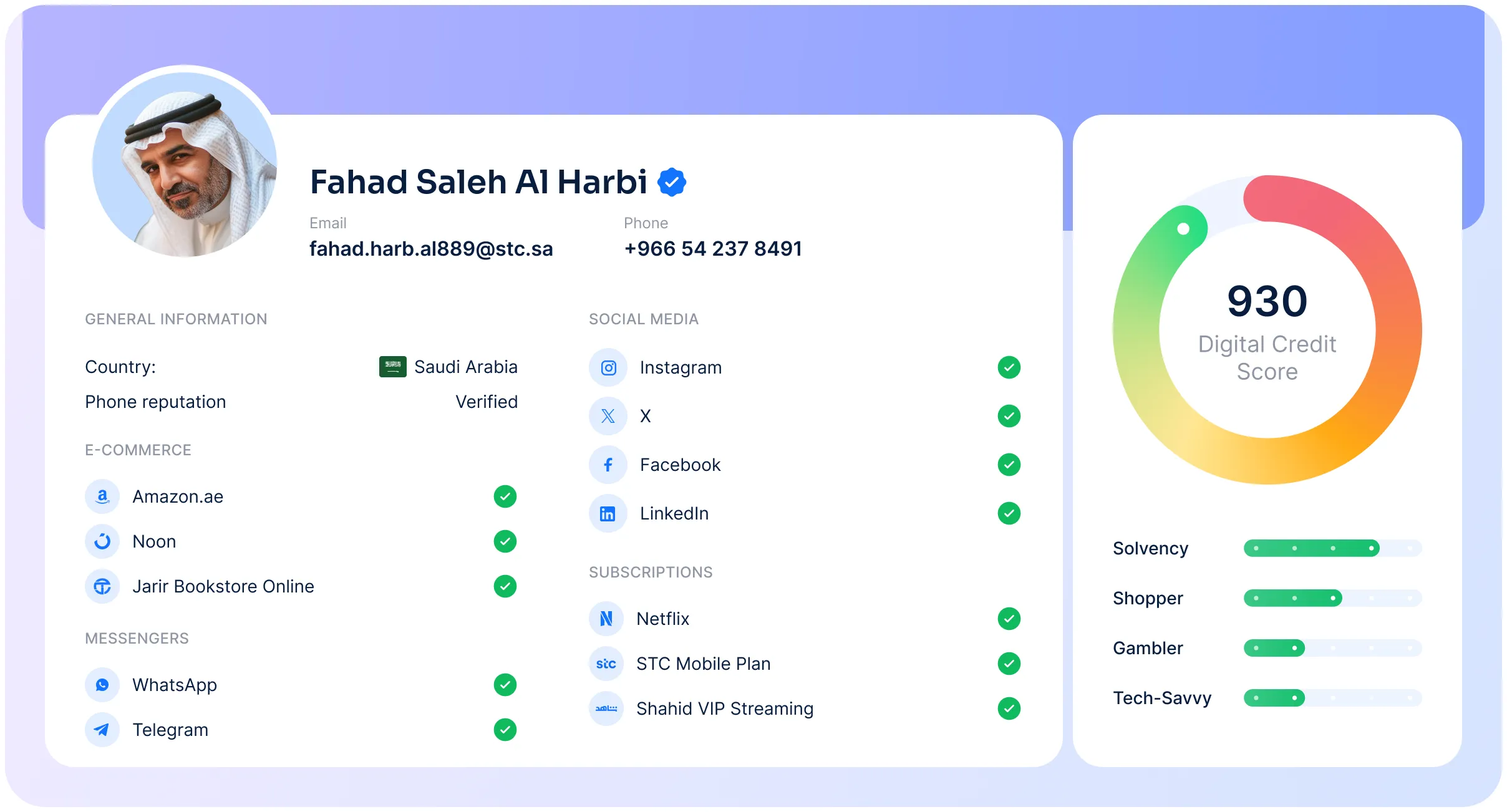

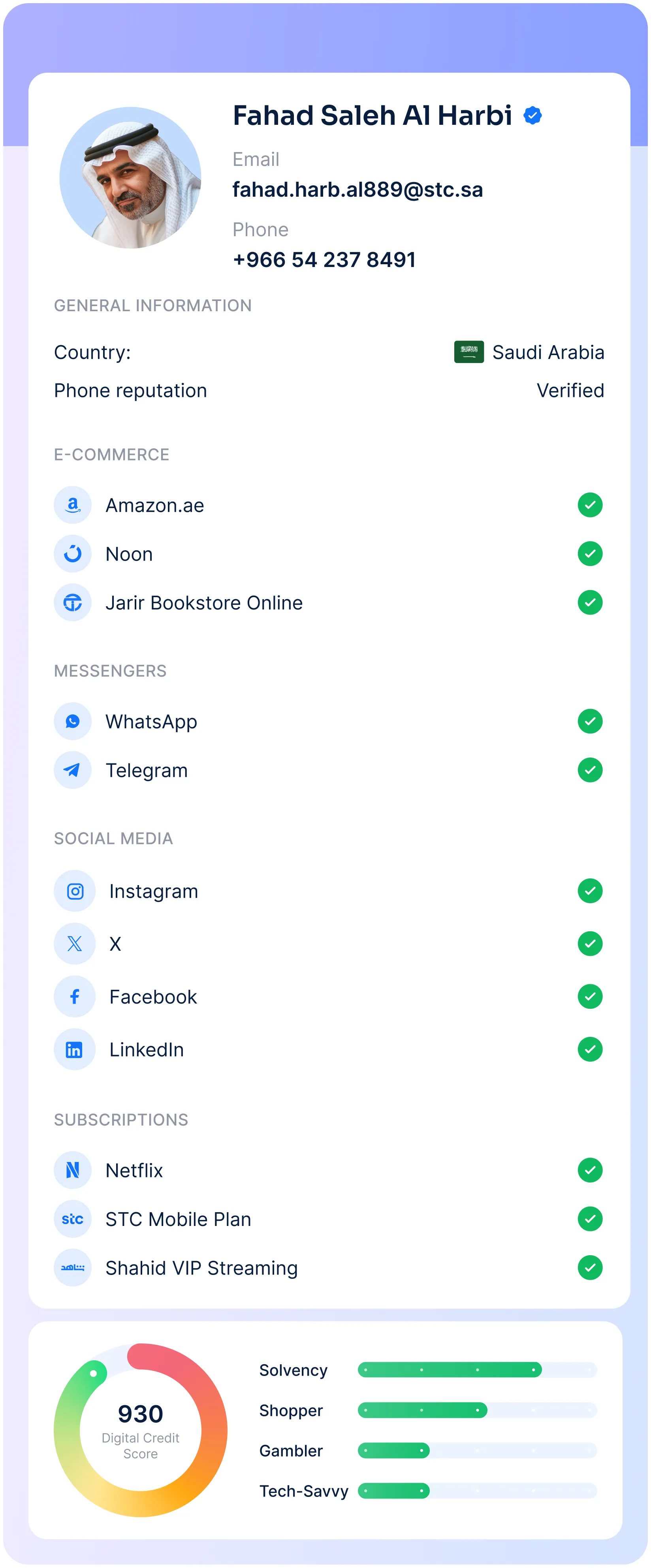

RiskSeal collects data from 200+ online platforms, including Saudi-specific services.

Below is a selection of popular Saudi digital platforms included in our analysis. For the full list, including niche and regional sources, please reach out to our team.

Namshi

Mrsool

Absher

Shahid

How alternative data strengthens lending in Saudi Arabia

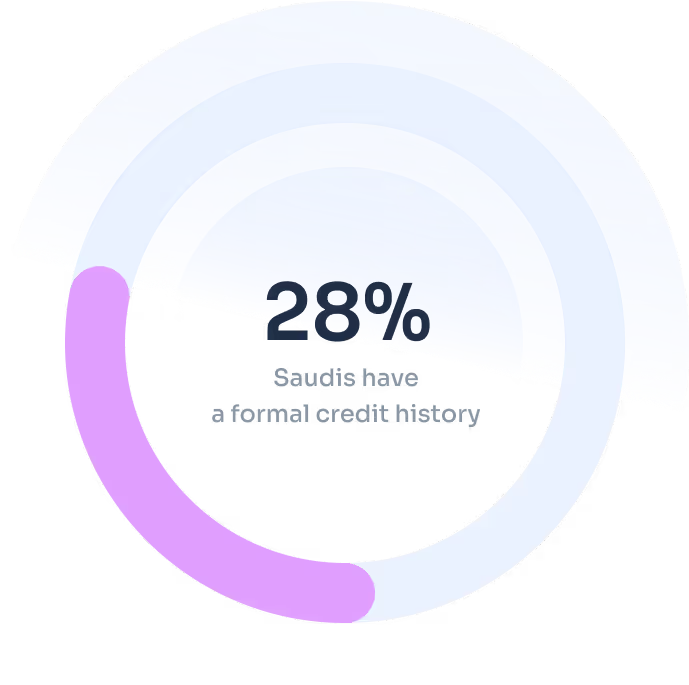

Credit inclusion at scale

Reach the unbanked and underbanked groups with 400+ alternative insights on each borrower.

Grow credit portfolio safely

Approve more borrowers with smarter risk assessments, reduce defaults, and expand lending without slowing business growth.

Real-time, AI-powered scoring

Meet modern borrower expectations with instant credit decisions and seamless onboarding.

Client success stories

See how RiskSeal’s unique data sources generate pure Gini uplift, even in emerging markets. Real numbers. Real before/after performance.

.webp)

.webp)

.webp)

FAQ

What does RiskSeal cost for fintechs in Saudi Arabia?

RiskSeal pricing is flexible. We offer two options:

Basic plan – $499 per month. Designed for smaller lenders and fintechs that process lower volumes. Includes all core features for digital footprint analysis.

Custom plan – For larger financial and credit organizations in Saudi Arabia. Pricing is tailored to your transaction volume and business requirements.

For full details, visit our pricing page or speak directly with our sales team.

What advantages does RiskSeal bring to lenders in Saudi Arabia?

RiskSeal helps Saudi lenders improve credit decisions with:

-Step-by-step onboarding for a smooth start.

-Expert support to understand and apply alternative data.

-24/7 technical assistance whenever you need it.

-99.9% API uptime for reliable access to data.

-A client portal with analytics to track results and optimize your lending.

How can I know if RiskSeal data will benefit my business?

We provide a free Proof of Concept (PoC) for Saudi lenders.

You can test our scoring on your own historical data. This shows how RiskSeal improves risk assessment, helps approve more creditworthy borrowers, and reduces defaults.

After the PoC, we give you a detailed results report. This helps you measure the real value before you decide to integrate our solution fully.

How is alternative data used for credit scoring in Saudi Arabia?

Lenders in Saudi Arabia use alternative data to assess applicants beyond traditional credit bureau records.

This includes digital footprint signals, telecom data, and behavioral patterns that reflect real-world financial activity.

These additional data points help build a more complete risk profile, especially for applicants with limited credit history.

As a result, lenders can make more accurate decisions while expanding access to underserved segments.

Can alternative data help approve more customers in Saudi Arabia?

Yes, alternative data helps lenders identify creditworthy applicants who may not qualify under traditional scoring models.

By analyzing digital behavior and non-bureau signals, lenders can better distinguish between low-risk and high-risk borrowers.

This approach allows fintechs and lenders to safely increase approval rates without compromising risk standards.

It also supports financial inclusion by opening access to credit for thin-file or new-to-credit customers.

What digital tools help streamline underwriting processes?

Modern underwriting relies on digital tools that automate data collection, identity verification, and risk assessment in real time.

These include alternative data platforms like RiskSeal, AI-driven scoring models, and automated decision engines.

By reducing manual checks and accelerating decision-making, these tools help lenders process applications faster and more efficiently.

This leads to lower operational costs and a smoother experience for both teams and customers.

.webp)