Consumer Credit Market Storm: 4 Tips for Lenders in 2026

Discover four practical ways to strengthen consumer credit risk in 2026 with real-time underwriting, alternative data, smarter collections, and compliance-ready AI.

Consumer finance is under pressure from every direction at once.

New competitors are taking market share. Regulatory requirements are becoming more demanding. Economic headwinds are pushing default rates higher.

And risk teams are expected to navigate all of it. Mostly, with the same tools and processes they already had years ago.

This article is for risk and analytics teams at lenders, fintechs, and consumer finance companies who are dealing with exactly this situation.

I’ll walk through what’s driving the pressure, and offer four practical tips: real-time underwriting, vendor strategy, collections uplift, and compliance by design.

Why risk is rising in the consumer finance market

Consumer finance leaders are now dealing with competitive pressure, regulatory scrutiny, economic stress, and rising fraud risk.

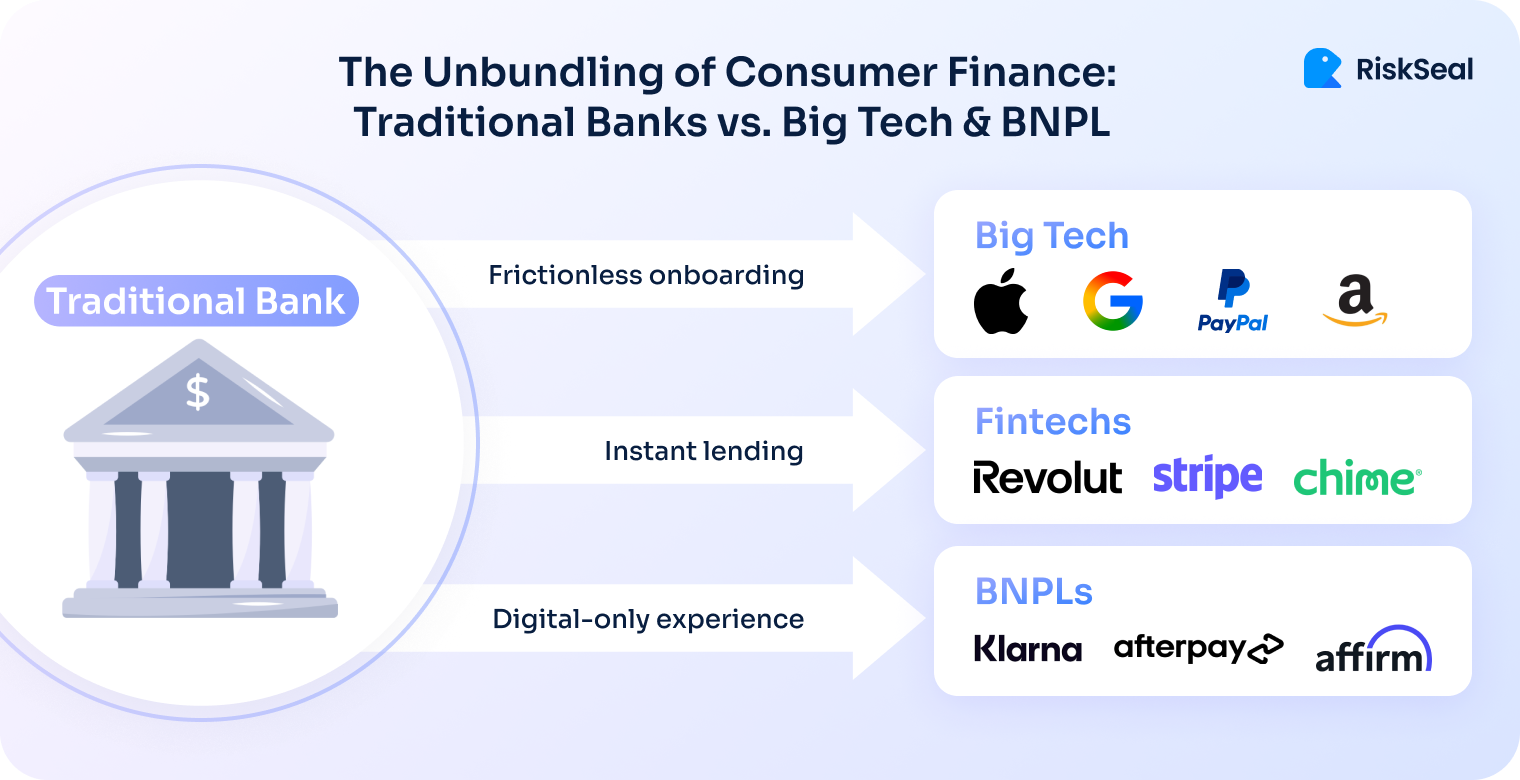

New competitors are reshaping the landscape

The consumer finance market has been structurally disrupted.

Big Tech firms, digital-native lenders, and BNPL platforms have spent the last decade unbundling what traditional lenders once offered as a package.

They don't need to win everything. They just need to win the most profitable slices.

McKinsey's April 2025 report, Riding the Storm, puts it plainly: traditional high-cost business models are losing ground to platforms that use data and technology more efficiently.

The same report recommends a six-point transformation for consumer finance companies that continue to rely heavily on the traditional high-cost operating model:

- redesigning the funding model

- refreshing the product proposition

- modernizing customer acquisition

- implementing real-time, customer-level underwriting

- transforming collections through smarter segmentation and AI

- deepening customer engagement and cross-selling

The connective tissue across these moves is data. Real-time underwriting, smarter segmentation, and personalized collections all require signals that traditional credit files were never designed to capture.

This is the real case for alternative data: not as an add-on to legacy models, but as core infrastructure for the next generation of consumer credit. Without that layer, transformation remains mostly cosmetic.

Looking back, the US Treasury flagged this as early as 2022.

Their report on non-bank competition in consumer finance described how fintechs use alternative data and technology to expand credit access and to capture margin from lenders who rely on slower, more rigid infrastructure.

That dynamic hasn't changed. If anything, it's accelerated.

Regulatory complexity is rising for lenders

Alongside competitive pressure, the regulatory environment has become significantly more demanding.

The OECD Consumer Finance Risk Monitor 2026, which tracks risk across 60 jurisdictions, identifies three top operating-environment risks:

- inflation and rising rates

- fraud and scams amplified by digitalization

- new business models that outpace existing oversight frameworks

In the US, the CFPB has been active on multiple fronts. Open banking rules under Section 1033, updates to ECOA and Regulation B affecting fair lending expectations, and increased scrutiny of AI and ML models used in underwriting.

In the EU, GDPR enforcement has matured, and the AI Act now classifies credit scoring as a high-risk AI use case. With corresponding documentation, transparency, and human oversight requirements.

In the UK, the FCA's Consumer Duty has raised the bar on what "good outcomes" means for customers, including in credit markets.

These aren't isolated developments. They reflect a global shift toward more intensive oversight of how lenders make decisions, use data, and treat customers.

Economic pressure is increasing portfolio risk

The macro environment adds another layer of difficulty.

The OECD Monitor highlights over-indebtedness and low financial literacy as persistent demand-side risks.

Rising rates have increased debt-service burdens for borrowers who stretched during low-rate periods. Default rates in several consumer credit segments have climbed.

At the same time, scams are rising. Digitalization has expanded the attack surface, and many lenders' fraud detection capabilities haven't kept pace.

What risk teams need to prioritize now

Risk teams are being asked to do more with more complexity. Not just protect the portfolio, but help the business see applicants as people, not just records, scores, or data points.

The McKinsey framing is useful here: companies that survive this storm will be those that treat risk infrastructure as a competitive asset, not just a compliance cost.

That means better data, faster decisioning, and smarter use of analytics at every stage of the credit lifecycle.

Our team has put together 4 tips to help your company effectively evolve even under the pressure of these factors.

Tip 1: Close the data gap with real-time underwriting

Traditional bureau data tells you what happened. It doesn't tell you what's happening now.

A borrower who looked stable six months ago may be under significant financial stress today. A thin-file applicant who looks risky on paper may have strong signals of creditworthiness in their digital behavior.

Real-time underwriting means enriching your decisioning layer with live, alternative data signals at the moment of application.

The most useful sources include open banking cash flow data, telecom activity patterns, digital footprint signals (email age, social presence, paid subscriptions), and utility and rental payment history.

Connecting these sources requires an API-first architecture at the point of decision.

Latency is critical – enrichment that takes 10 seconds is not compatible with a seamless digital application flow. The target is enrichment within 5 seconds max, fully embedded in the decisioning pipeline.

Measuring the effect requires two layers of metrics. On the model side, the key measure is Gini coefficient over a bureau-only baseline. In my experience, even modest alternative data integrations can demonstrate model uplift on thin-file populations.

On the business side, the metrics that matter are approval rate delta on previously declined segments, default rate on incremental approvals, and revenue per decision.

These numbers tell you whether the data is generating real value, not just statistical lift.

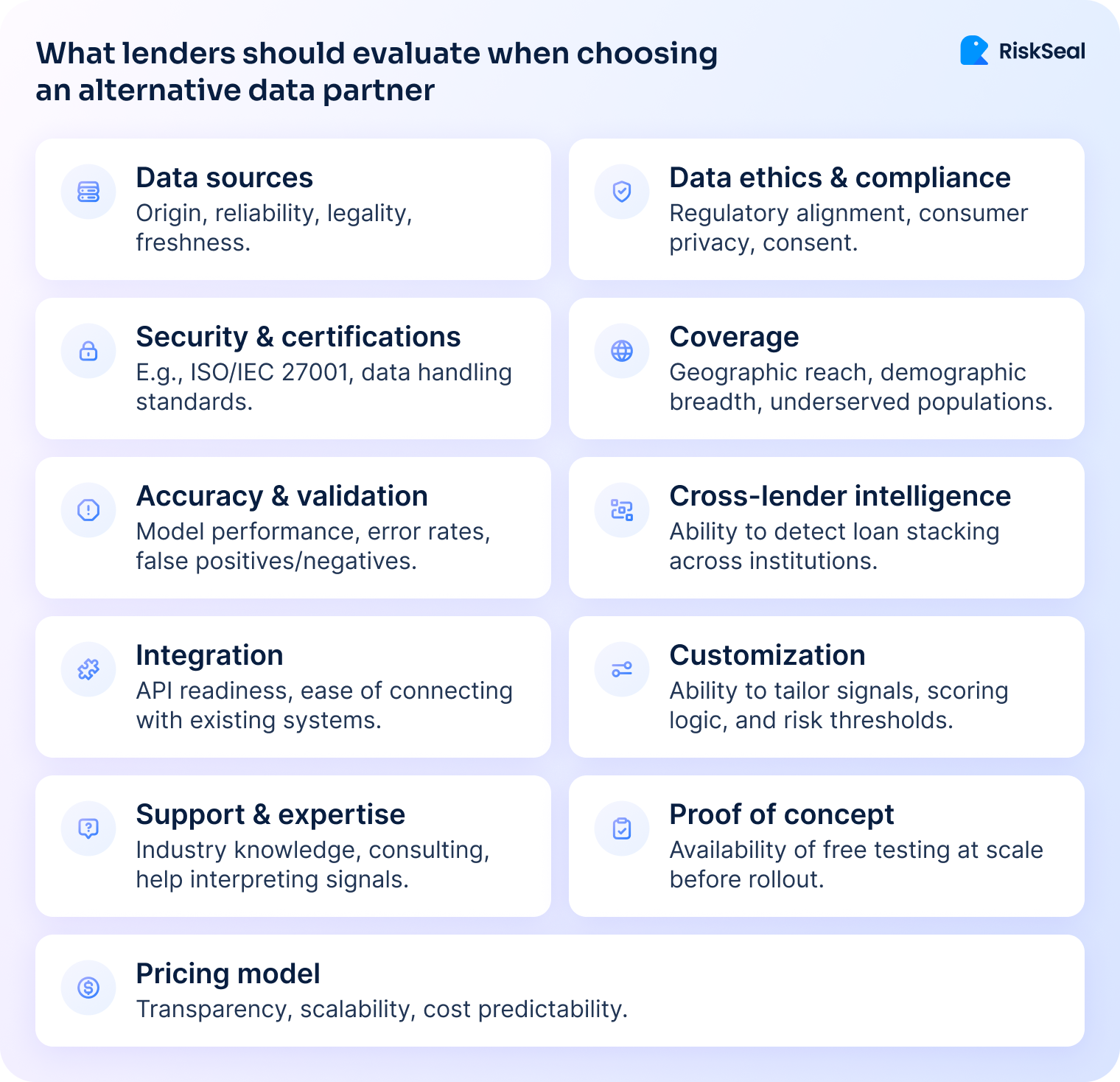

Tip 2: Choose the right alternative data provider

Not all alternative data is equal. Choosing the wrong provider creates problems that are hard to unwind – coverage gaps, inconsistent signal quality, compliance exposure, and integration debt.

The evaluation process should start with retrospective testing.

Before signing any contract, ask the vendor to score a sample of your historical portfolio. Ideally 6-12 months of closed loans with known outcomes.

This tells you actual lift, not theoretical lift. Any vendor unwilling to do this should be treated with caution.

Price and value need to be assessed together. The right question is not "how much does this cost per call?" but "what is the revenue or loss impact per decision?"

The numbers here are just an example, but the logic is clear. A data source that costs, let’s say, $0.50 per call but improves net margin by $3 per loan is worth very different consideration than one priced at $0.10 with no measurable lift.

Stability matters as much as accuracy. Alternative data sources can change: APIs are updated, coverage shifts, source partnerships change. Ask vendors how they handle this:

- do they proactively notify clients of coverage changes?

- Do they provide signal-level monitoring dashboards?

- What's the SLA if a data feed goes down during peak decisioning hours?

Finally, check whether the vendor supports ongoing model monitoring.

Data drift is real. A signal that was predictive two years ago may have degraded. The best vendors provide tools to track this and flag when retraining or recalibration is needed.

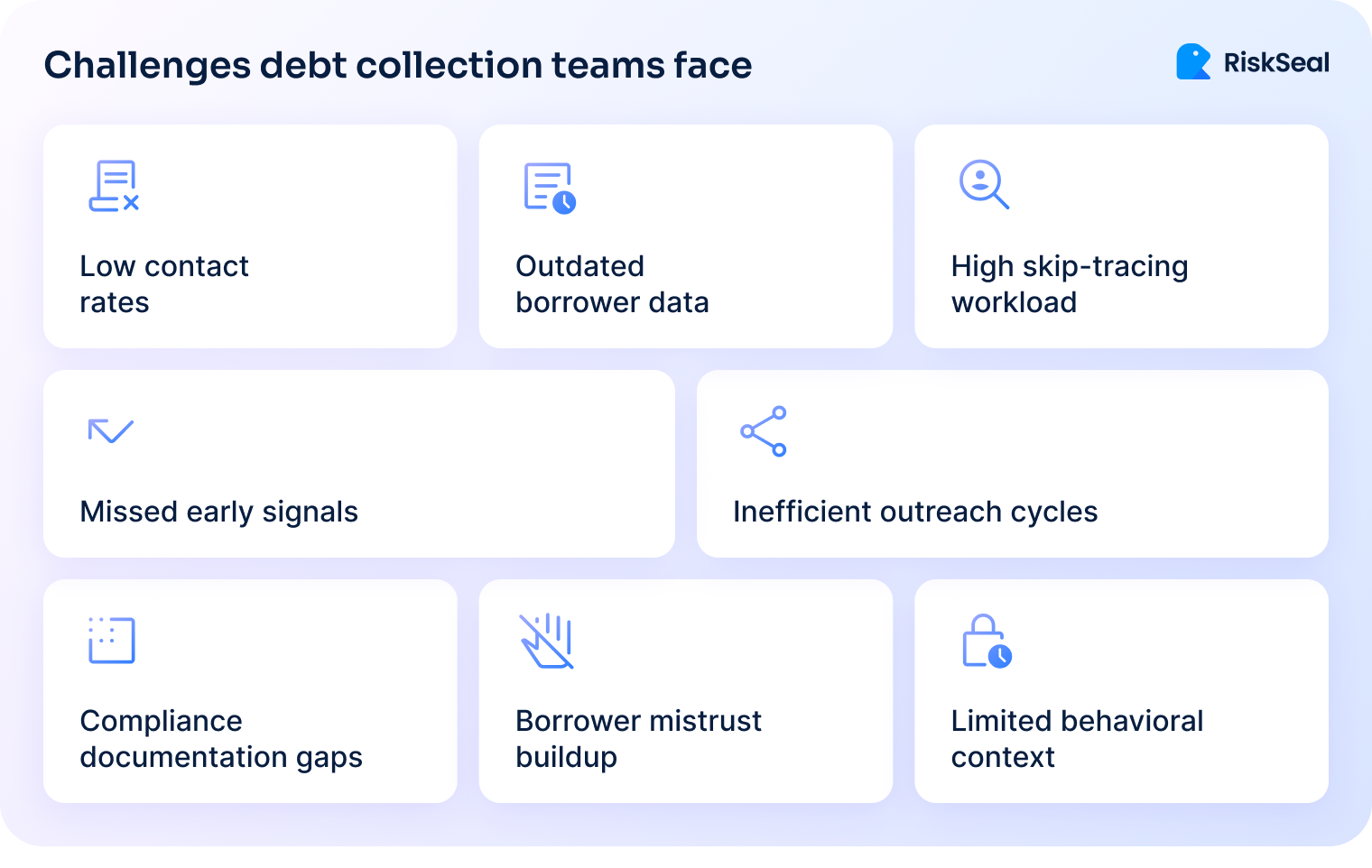

Tip 3: Match collections strategy to borrower risk

Collections is one of the highest-ROI areas for data enrichment. And one of the most underinvested.

The core problem with most collections strategies is uniformity. The same outreach cadence, the same channel, the same tone applied to a portfolio of borrowers who are delinquent for very different reasons.

Some will self-cure if given a short grace period. Others are in genuine distress and need a restructuring conversation. A few are simply disengaged and need a different contact channel.

Microsegmentation is the answer. Teams can group delinquent accounts into more meaningful treatment tiers by looking at two types of signals:

- Updated financial signals: income changes, employment indicators, open banking balances.

- Behavioral signals: contact responsiveness, payment timing, disposable income spent on subscriptions lately, etc.

This gives collections teams a clearer view of who may need flexibility, who may need faster outreach, and where the real risk sits.

A practical alternative data-based recovery framework might look like this:

- a self-cure tier for borrowers with strong recent income signals and a short delinquency window

- an early intervention tier for borrowers showing financial stress but still contactable

- a hardship tier for accounts where recovery probability is low without significant intervention

Data enrichment supports all three tiers.

Updated contact data improves right-party contact rates, which is often the single biggest bottleneck in collections. Financial stress indicators help prioritize which accounts need proactive outreach versus which to let run. And channel preference signals derived from digital behavior help teams reach borrowers where they're most likely to respond.

The business impact is measurable: recovery rate improvement, cost-per-dollar-collected reduction, and right-party contact rate are the KPIs to track.

Tip 4: Build compliance into data and AI decisions

For teams operating in the EU, compliance is not a final checkpoint. It's a design constraint from day one.

I've seen this go wrong at companies that treated compliance as a legal review at the end of the project. By then, the data pipeline is built, the model is trained, and changes are expensive.

The DPO raises concerns about lawful basis or data minimization, and suddenly you're three months behind schedule.

The right approach is to involve legal and data protection teams at the architecture stage. Before any vendor contracts are signed and before any data flows are designed.

Under GDPR, every alternative data source needs a documented lawful basis for processing.

For credit scoring, this is typically legitimate interest or contract performance. But it requires a Legitimate Interests Assessment or, more likely, a Data Protection Impact Assessment given the sensitivity of the use case.

The EU AI Act adds another layer. Credit scoring is classified as a high-risk AI system. That means you need to:

- maintain technical documentation of the model

- ensure a level of human oversight in the decisioning process

- be able to provide meaningful explanations to applicants, not just "we used a model."

Practically, this means building explainability into the model from the start.

SHAP values or similar techniques can generate feature-level explanations that feed into adverse action notices.

Audit logs need to capture not just the decision, but the data inputs and model version used at the time of that decision.

For vendor relationships, ensure Data Processing Agreements are in place before any data is exchanged. Check where data is processed. EU-based processing is significantly easier to document than cross-border transfers under SCCs.

Compliance handled this way becomes an asset. It's what lets you move faster when a new data source becomes available, because you already have the framework to evaluate and onboard it cleanly.

A stronger risk advantage in the consumer credit market

The storm is real, but it's also clarifying.

Lenders that invest now in data infrastructure, real-time decisioning, and compliance-ready architecture are building a durable advantage.

The competitors gaining ground today are winning on data quality and decisioning speed, not just product design.

Risk teams have more leverage in this than they're sometimes given credit for.

Better underwriting data reduces losses. Better collections segmentation improves recovery. Better compliance infrastructure reduces regulatory risk and speeds up product launches.

At RiskSeal, this is exactly the problem we work on – helping lenders connect to alternative and digital footprint data quickly, compliantly, and in a way that generates measurable lift.

See more

.webp)

Find practical advice to help you identify valuable clients among those without a credit history and issue more loans.

Explore how digital footprint analysis improves credit scoring models, boosting default prediction accuracy and approval rates in emerging markets.

.webp)

Discover how social media profiling enhances credit risk management by analyzing digital footprints.