Discover how alternative data helps lenders reduce dead-end outreach, reach borrowers faster, and improve collecting routine.

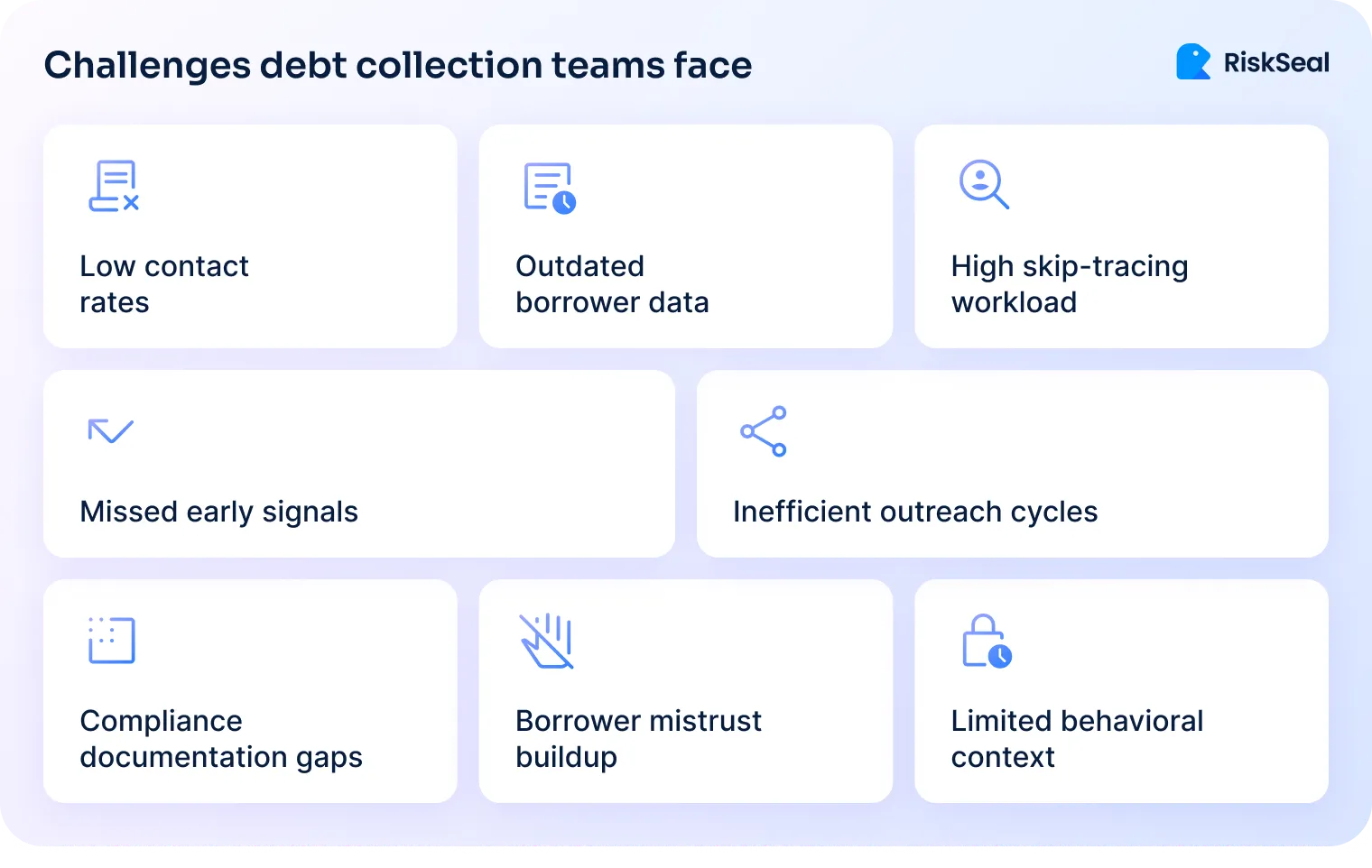

Debt collection sits at a difficult crossroads. Lenders need to recover funds efficiently, yet borrowers expect respectful, personalized communication.

Middle-market loan recoveries in the U.S. have averaged just 77.4% from 2010-2025. Bank lending has held slightly higher at around 78%. Both sit below long-term expectations.

Traditional recovery methods rely on outdated contact details, rigid outreach cycles, and repetitive attempts that feel more intrusive than helpful.

At the same time, borrowers move fast, change channels frequently, and expect lenders to adapt just as quickly.

In today’s post, we explore whether alternative credit scoring platforms can strengthen recoveries while maintaining a humane borrower experience. The data points strongly to yes.

The 2026 guide to LATAM digital footprints for credit scoring

Traditional recovery workflows were built for a different decade. They rely on phone calls and emails that no longer align with how people communicate.

Today, unknown numbers are ignored or flagged as spam. Emails get buried. Often, the borrower isn't dodging the lender; they simply never received the message.

Yet, lenders interpret this silence as resistance. By the time a conversation finally happens, the borrower feels blindsided and the agent feels dismissed. The frustration is already baked in.

This emotional friction does more than delay a single payment. It erodes trust.

When outreach feels disconnected or one-sided, borrowers are less likely to engage, repay, or return for future products.

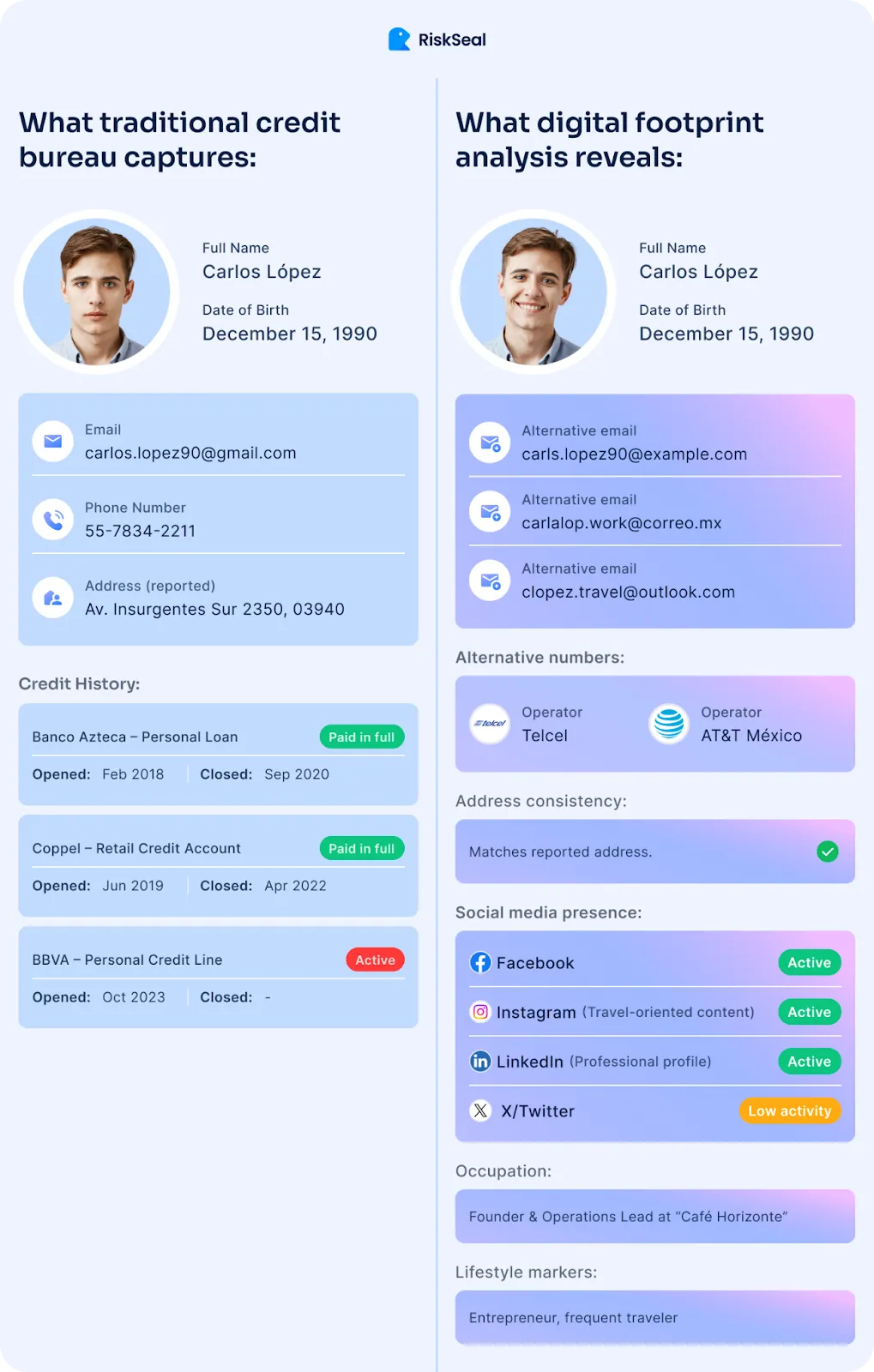

Traditional bureau files are static. They tell you who a borrower was three years ago, not who they are today.

Relying on this outdated view limits effectiveness and often leads to ineffective communication.

Alternative data fills this gap. It serves as a mechanism to signal real-time changes in a borrower's life.

This allows lenders to see the context behind a missed payment and choose the right approach.

Instead of guessing, teams can rely on specific categories of signals:

This power comes with responsibility. Usage must be strictly ethical, transparent, and fully compliant with regulations like GDPR.

The goal is clarity, not intrusion.

When lenders understand the present reality rather than just the past history, the conversation changes. It shifts from blind pressure to an empathetic, effective resolution.

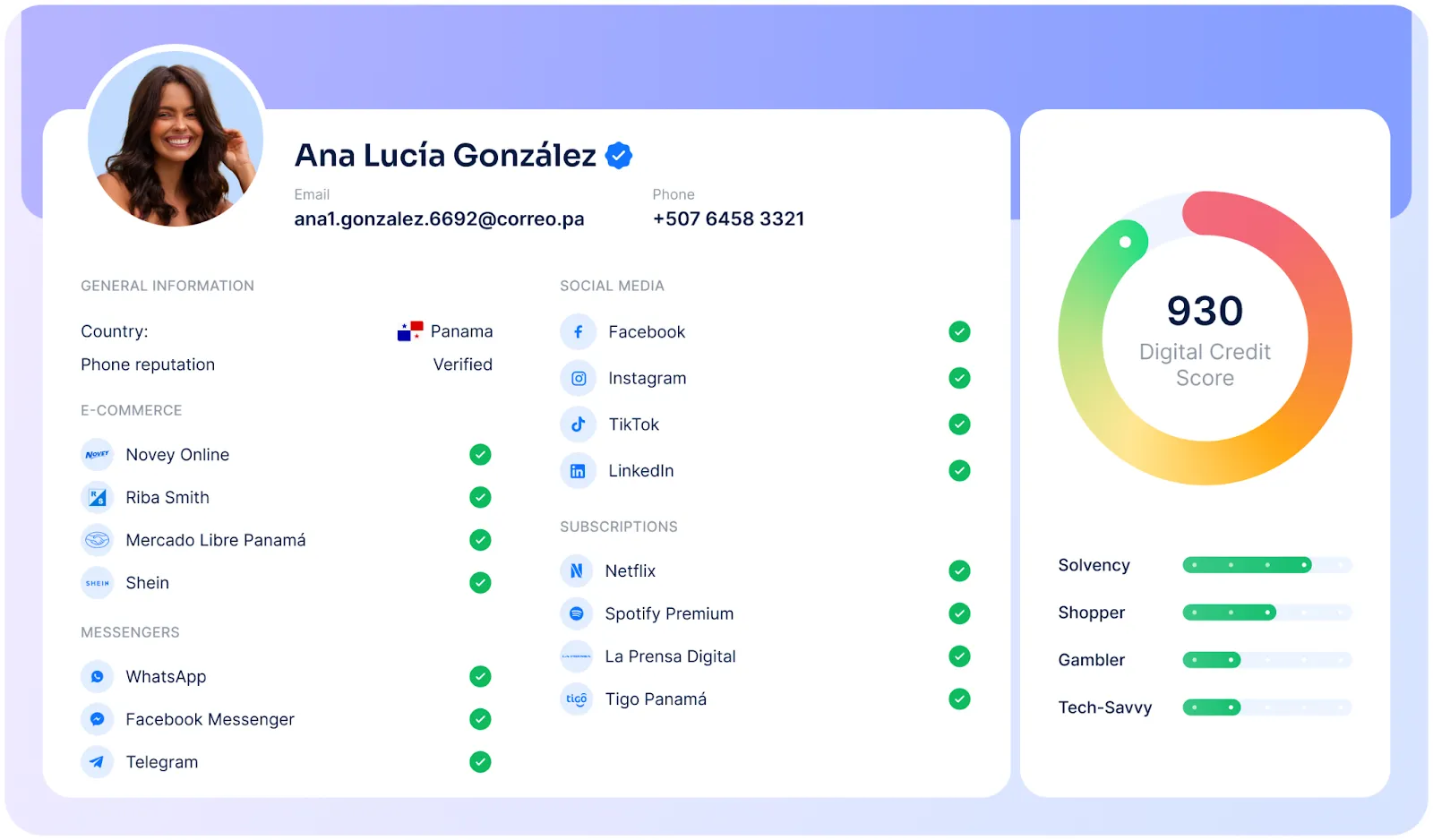

Alternative data gives lenders a clearer understanding of how borrowers engage online today. These insights don’t involve private content or invasive tracking.

Instead, they focus on simple, observable signals that help determine which communication channels are still active, reliable, and worth prioritizing.

The table below highlights the most useful signals for collections and how they support respectful, effective outreach:

Together, these signals guide collectors toward the channels with the highest probability of contact. Without resorting to intrusive tactics or guesswork.

They replace trial-and-error outreach with targeted, respectful communication based on real, current behavior.

With the right debt collection and recovery software, recovery teams gain clearer signals and stronger context about borrower behavior.

This enables them to:

1. Identify active communication paths faster

Collections teams often lose hours testing numbers and resending messages without knowing which channel will connect.

Alternative data reveals the borrower’s active paths instantly, so agents focus their effort where contact is most likely.

2. Reduce dead-end outreach attempts

Stale or inaccurate contact details drain productivity and delay resolution.

Signals showing inactive inboxes, changed numbers, or secondary contact points help teams skip the trial-and-error stage entirely and move straight to productive conversations.

3. Engage borrowers earlier in the cycle

Early contact often decides whether repayment stays simple or becomes a long recovery process.

When lenders know the borrower’s active digital channels, they can intervene before delinquency escalates.

4. Tailor outreach timing and channel strategy

Reaching the right borrower at the right moment drives response rates and reduces friction.

Alternative data helps teams choose the channel currently in use and time outreach when engagement is most likely.

5. Strengthen contact accuracy for compliance and recordkeeping

Accurate, up-to-date contact information is essential in regulated environments.

Digital signals, IP consistency, and active account indicators confirm that outreach is directed to the correct person on a valid channel.

Better signals lead to contact faster. Faster contact leads to smoother conversations. And that strengthens the overall relationship during a sensitive moment for both sides.

RiskSeal replaces manual skip tracing with a single stream of real-time intelligence.

It validates contact reliability through live signals, checking email activity, phone reachability, and messaging app presence. This eliminates the guesswork of calling dead numbers.

Across our recent work with fintechs in dynamic markets, this shift has driven a 35% uplift in successful contact rates.

The table below summarizes how specific data points solve common operational roadblocks:

Such information is critical for BNPL debt recovery and fintech collections, especially in regions where credit bureau data is thin or outdated.

By consolidating digital footprints into a clear view, RiskSeal provides the context needed for accurate, compliant decision-making.

It ensures agents have the right information before they dial, turning cold friction into a productive resolution.

Technology often promises efficiency, but in collections, its real value is clarity.

The gap between a missed payment and a resolution is often just a missing signal.

If your team commits to reaching borrowers where they are today, not where they used to be, the strategy changes. It becomes not only more effective, but also more human.

When you remove the friction of bad data, you make room for a solution.

Precision builds trust. Trust drives repayment. Start there.

Inside the LATAM alternative credit data report

How can alternative data improve contact rates without overwhelming borrowers?

Alternative data helps teams focus on the channels borrowers actually use today.

Instead of sending the same message across multiple outdated points of contact, recovery teams can target a single, active path with well-timed communication.

This reduces noise for the borrower and increases the likelihood of a constructive response.

What types of digital signals help lenders reach borrowers more effectively?

Lenders can reach borrowers more effectively by using digital signals that show which channels people actively use and trust.

Key examples include:

Together with AI for debt collection, these signals help focus outreach on inboxes, phones, or platforms borrowers actually check, instead of inactive contacts.

Can data-driven collections really reduce operational costs while maintaining a good customer experience?

Yes. When agents know which contact details are current, they stop wasting time on dead-end attempts.

This leads to fewer failed calls, less manual skip tracing, and earlier conversations with borrowers, all of which reduce operational effort.

At the same time, borrowers experience less pressure because outreach feels timely and relevant.

How does RiskSeal support ethical and compliant loan recovery with alternative data?

RiskSeal focuses solely on non-intrusive, publicly observable, and activity-based signals.

The platform identifies active channels, confirms identity consistency, and highlights up-to-date touchpoints without accessing private messages, personal content, or sensitive data.

This helps lenders reach the right person while maintaining transparency, fairness, and compliance across all outreach steps.

Discover how enhanced credit scoring models with alternative data drive financial growth and boost inclusivity.

Explore how credit stress testing and real-time alternative data empower lenders to spot early warning signs and protect portfolios during the Christmas season.

.webp)

Explore the data gap behind credit invisibility and how to close it with smarter scoring.

.svg)

.webp)