Why Mexico Needs Better Financial Inclusion for Women

Discover why traditional credit scoring misses creditworthy women in Mexico and how alternative data helps lenders see thin-file borrowers clearly.

In Mexico, women repay loans at higher rates than men. They default less. They manage irregular cash flows with remarkable discipline.

Yet they get less credit, pay higher rates, and face more rejections. That's a serious measurement problem.

In today’s article, we’re going to look at why credit scoring models still punish that discipline when it’s not attached to the right paperwork.

The 2026 guide to LATAM digital footprints for credit scoring

Why women in Mexico are better borrowers than models show

The data from AFI, CNBV, and Mexico’s financial inclusion infrastructure tells a story lenders should not ignore.

Women in Mexico are not an inherently riskier credit segment. AFI’s Mexico case study cites local evidence showing women’s stronger loan repayment rates and lower risk profiles.

CNBV has gone even further: regulatory amendments in 2021 and 2022 recognized lower risk in loans granted to women by reducing preventive reserve requirements for those portfolios.

And yet the gap remains. AFI estimates that 25 to 30 million women in Mexico remain unbanked, while account ownership still shows a 13-percentage-point gender gap.

The problem is not only access. It is also product design: 44% of financial institutions surveyed said women need specific financial products. But only 20% said they actually offer them.

So the question is why so many credit systems still fail to measure that creditworthiness accurately.

The system is not rejecting risky borrowers. It is rejecting borrowers it cannot see clearly.

Why traditional credit scoring misses women’s creditworthiness

This isn't a case of intentional discrimination.

Risk teams work within tightly defined frameworks, under constant regulatory pressure, with tools that were built for a different kind of borrower profile. The failure is structural, not personal.

Here's where the gaps actually are.

Informal income gets treated as no income

A large share of economically active women in Mexico participate in the informal economy.

They earn real money, but not through payroll. They also absorb significant unpaid care work that has economic value but no financial record.

No payslip means "no income" in most traditional models. That data gap becomes a risk signal in the eyes of credit bureaus.

Thin credit files reflect historical exclusion

Women have had less access to formal credit, historically. So they have thinner credit bureau files. AI models trained on historical data learn this pattern and replicate it.

CGAP frames this as a measurement problem. Even gender-blind models can misread women when there is less data available for them, or when the data sources don't fully account for gender differences in credit behavior.

The feedback loop closes fast: no credit leads to no history, which leads to a lower score, which leads to no credit. The model learns exclusion as normal behavior.

The collateral gap blocks access to secured credit

Women in Mexico are less likely to own the assets that traditional lenders often ask borrowers to put behind a loan.

According to BBVA Research, in 2024, only 25.3% of women owned a home, compared with 38.5% of men. The gap was even wider for vehicles: 16.5% of women vs. 43.3% of men.

Agricultural land showed the same pattern, with 5.7% of women owning land or plots, compared with 12.6% of men.

Secured lending requires assets. Without them, borrowers either pay more or get turned away entirely.

This does not really reflect the repayment ability. Just shows that even today’s asset ownership patterns are shaped by decades of structural inequality.

Caregiving patterns get misread as financial instability

Career breaks, part-time work, and income fluctuations tied to caregiving responsibilities look like warning signs inside a traditional scoring model.

I’ve seen this in practice across LATAM. But the same pattern shows up in mature credit markets too.

In the UK, for example, Credit Karma research found that 26% of women go into debt to cover maternity leave, with average borrowing of £2,800. Nearly a quarter also start maternity leave with no savings.

In reality, these are context-driven patterns. A reliable borrower can get flagged simply because her income curve doesn’t follow a straight line. Even when the actual explanation is entirely logical.

Loan purpose becomes a hidden risk proxy

Women often borrow for household resilience, children’s education, caregiving costs, health needs, or small business survival.

These can be rational, repayable loans. But they do not always look like “productive” credit inside traditional lending frameworks.

Loan purpose matters more than many borrowers realize. Bankrate notes that lenders may use it to shape the amount, repayment term, interest rate, or even whether the loan use fits their policy at all.

That creates a quiet bias. The model is not only asking whether the borrower can repay. It is also reacting to whether the loan purpose fits an old idea of what valuable credit looks like.

So women can get deprioritized not because the loans are riskier, but because the need does not match the template the system was built around.

What gender-blind scoring costs lenders

When lenders systematically exclude low-risk borrowers, they miss revenue. They reduce portfolio diversification. They leave disciplined, underserved segments open for competitors to fill.

Women who can't access formal credit don't disappear from the market. They turn to informal lenders, rotating savings groups, or high-cost alternatives.

That's a market failure with real consequences for everyone involved.

For lenders still relying purely on bureau data and payslips in Mexico's credit market, the untapped segment isn't hypothetical.

It's already there, demonstrating repayment behavior, just outside the system's line of sight.

What alternative credit data reveals about thin-file borrowers

The shift from bureau-only scoring to alternative data isn't about lowering standards. It's about extending visibility.

Here's what traditional models miss that alternative data can observe:

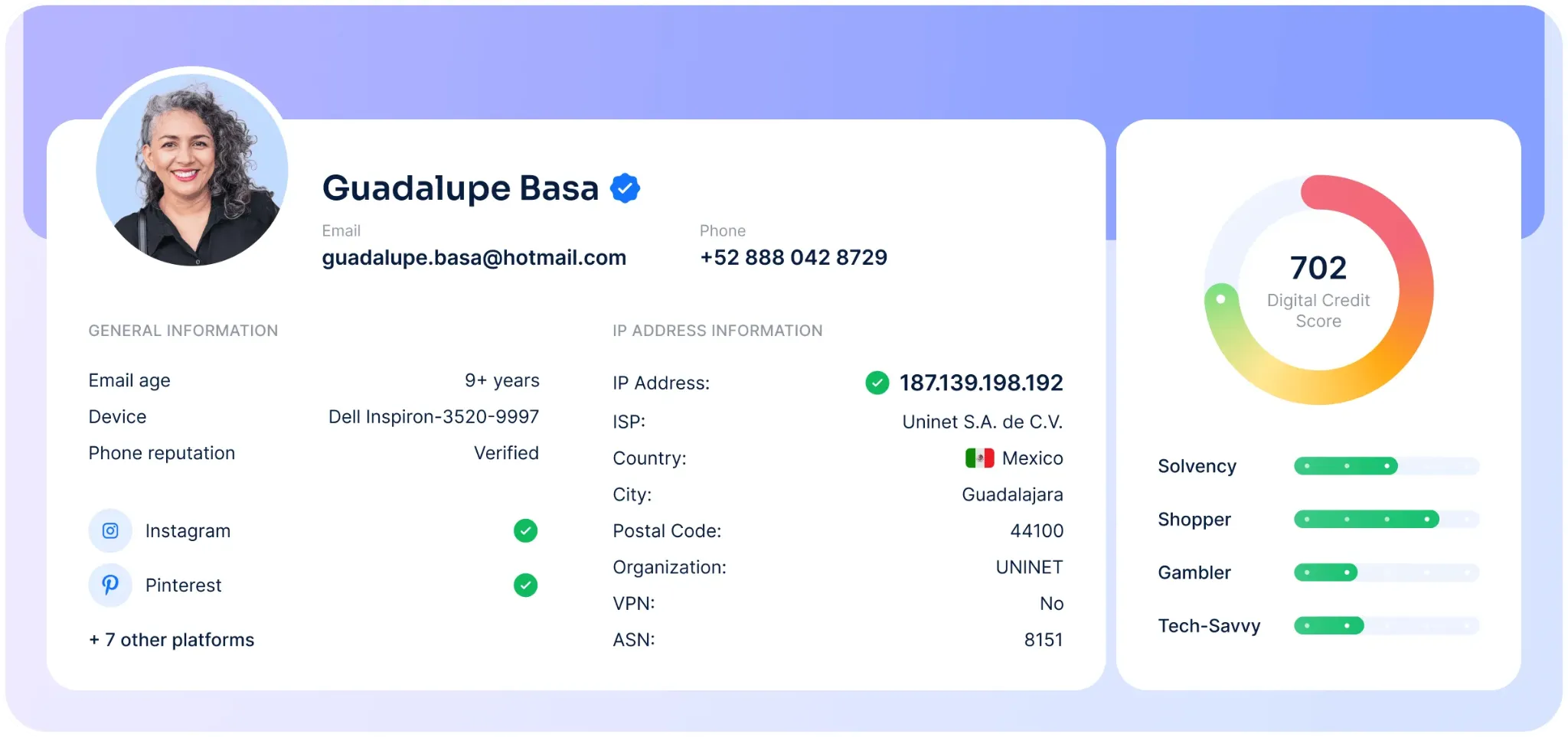

- Digital footprint consistency: email age, account activity, platform presence. These signal identity stability in ways that matter for fraud and risk assessment.

- Financial behavior beyond banking: how someone manages subscriptions, utilities, and e-commerce accounts reflects financial discipline even without a formal credit trail.

- Identity and contact consistency signals: not surveillance, but coherence markers. A borrower with a stable digital profile, consistent contact details, and a verifiable behavioral footprint is telling you something.

Alternative data doesn't guess at risk. It observes behavior where traditional systems see nothing.

This matters especially for thin-file applicants – which, in Mexico, disproportionately means women.

Why financial inclusion is better underwriting

I want to be direct about this: expanding credit access to women in Mexico is not a charity initiative. It's not about regulatory compliance or ESG optics.

It's about finding borrowers who already demonstrate strong repayment behavior and scoring them accurately enough to serve them.

More approvals don't mean more risk if the scoring is right.

In my experience working with lenders across different markets, the segments that look riskiest through a traditional lens often perform the best once you have the right data to see them clearly.

That reframing matters for how risk teams approach this.

The question isn't "how do we justify approving more women?" It's "why is our model missing a low-risk segment, and what data do we need to fix that?"

How RiskSeal helps lenders score thin-file applicants

At RiskSeal, we don't replace bureau data. We extend it.

Our approach is built around three core questions for any applicant:

- Who are they? – Identity validation through digital footprint signals.

- How do they behave? – Patterns across platforms, transactions, and digital activity that reflect actual financial behavior.

- Is the story consistent? – Cross-referencing signals to detect fraud, identity fabrication, or data misrepresentation.

For thin-file applicants, including the large share of women in Mexico's informal economy, this framework creates a fuller picture.

Alternative credit scoring does not require formal income documentation or an established credit history.

The goal is accurate scoring for borrowers that traditional systems currently can't assess well. That's the infrastructure problem we're solving.

How alternative credit data providers can close the visibility gap

Traditional credit models weren't built for today's workforce.

They certainly weren't built for the economic reality of women in Mexico: informal earners, caregivers, micro-entrepreneurs managing real financial lives without formal paper trails.

Closing the gender credit gap doesn't require new borrowers, lower standards, or a different risk appetite.

It requires better visibility into borrowers who are already there. And that is exactly where working with an alternative credit data provider changes the conversation.

Start measuring what you currently ignore. The lowest-risk opportunities in your pipeline are hiding in your rejection folder.

Inside the LATAM alternative credit data report

See more

.webp)

Explore the urgent need for alternative credit scoring methods in Nigeria, as traditional systems fail to meet the substantial credit demands.

.webp)

Learn to identify high-value borrowers early: pretransaction signals predict lifetime value and reduce default risk.

Explore Mexico’s consumer lending market, from major loan types and fintech trends to key providers, risk challenges, and growth opportunities.