How to Navigate Seasonal Credit Risk Before the Holiday Rush

Explore how credit stress testing and real-time alternative data empower lenders to spot early warning signs and protect portfolios during the Christmas season.

Every December, credit portfolios expand. And so does risk.

In 2024, U.S. consumers spent nearly $994 billion during the holiday season. About 36% of Americans took on new holiday-related debt.

The holiday rush is a stress test for every credit risk model.

To stay ahead, lenders need smarter data and the agility to separate short-term spending spikes from real structural risk.

Key holiday lending risks before Christmas

The weeks before Christmas consistently bring a mix of opportunity and risk. Lending volumes surges and borrower behavior shifts in unpredictable ways.

Seasonal surge in borrowing and credit utilization

During the holidays, borrowing jumps 20-30% as people spend more on gifts, travel, and celebrations.

This surge can mask deeper risks. Many borrowers already carry debts from previous holidays. New borrowing stacks on top of old obligations.

Credit risk managers must tell the difference between short-term cash needs and early warning signs of financial trouble.

Post-holiday spike in defaults and portfolio deterioration

The real stress test begins after the holidays. In January and February, late payments often rise as borrowers deal with higher bills and lower savings.

Unsecured lending segments, like credit cards, BNPL, and microloans, often show the first cracks.

Even a small rise in missed payments can quickly affect portfolio quality and early-year profitability.

Relaxed underwriting during peak season

Seasonal demand pressures lenders to capture more business. It’s easy to loosen approval criteria or raise credit limits to boost short-term revenue.

But these short-term gains often turn into long-term losses when repayment capacity weakens.

BNPL platforms are particularly exposed. Holiday usage can increase by 14-20%, often accompanied by relaxed underwriting standards.

Because BNPL debts are often missing or delayed in credit reports, lenders may misjudge a borrower’s real debt load. Especially if no modern BNPL software is used for scoring.

How can risk teams prevent costly surprises in the new year? By balancing growth with strict risk controls and full visibility into their data.

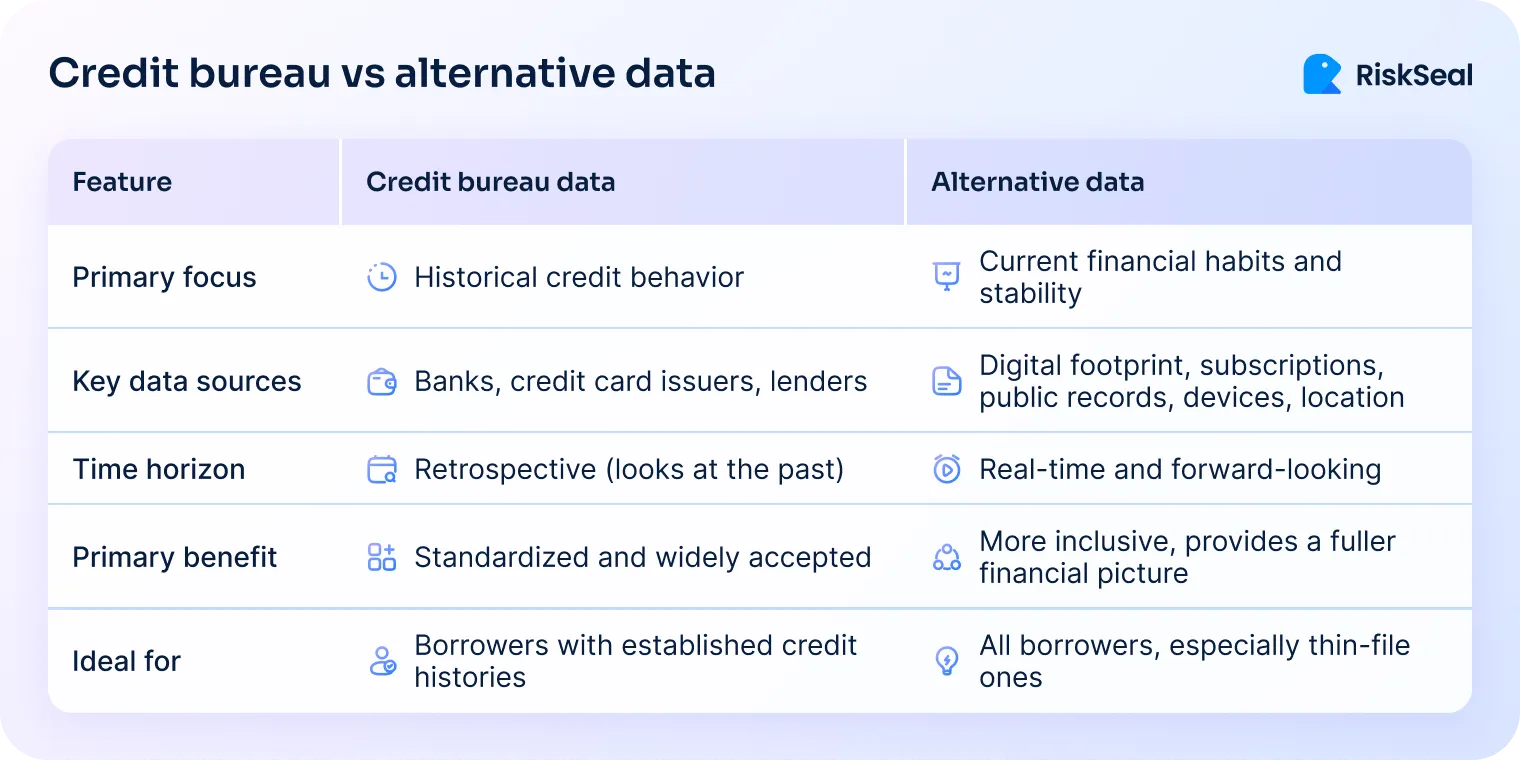

How the US consumer borrowing surge in December exposes gaps in traditional data

Christmas shopping moves at a pace that traditional credit data can’t match. Relying solely on bureau data leaves lenders reacting to problems rather than preventing them.

1. Timing gaps and data latency during peak holiday spending

Holiday credit cycles move faster than bureau updates.

Applications, approvals, and repayments can surge within days. And traditional data reflects these changes weeks later.

By the time delinquencies show up in January reports, early intervention windows are already gone.

2. Limited insight into short-term borrower behavior

Bureau data captures what borrowers owe, not how they use credit.

It overlooks short-term shifts that often signal overextension. This includes impulse buying or “treat yourself” spending.

Without behavioral context, models can’t separate short-term liquidity stress from real default risk.

3. Hidden exposure across BNPL, store credit, and microloans

Holiday financing through BNPL, store credit, or microloans grows sharply but isn’t always visible in bureau files right away.

Some borrowers juggle multiple products from different lenders. Others borrow for the first time raising the question of how to score people with no credit history.

These gaps create blind spots in understanding a borrower’s true credit exposure.

4. Rising fraud and identity risk during the holiday rush

High transaction volumes and rushed approvals open doors to synthetic IDs and first-party fraud.

Traditional credit files focus on repayment history. Not digital red flags like mismatched IPs, disposable emails, or device switching patterns.

5. Limited adaptability in high-demand periods

The end-of-year sales season pressures lenders to expand approvals and increase credit limits.

Traditional models provide a solid long-term view of borrower reliability. But they lack the agility to adjust exposure dynamically during these intense spending periods.

To close that gap, many lenders are turning to alternative data. It’s a real-time insight source that helps teams make better decisions during high-stress cycles.

How alternative data enhances credit stress testing during the holiday surge

Traditional credit data is still the foundation of sound lending. But during the holidays, its lag and limited behavioral scope make it difficult to react fast.

Borrowers’ financial and digital behaviors can shift in days – not months – and risk managers need data that can keep up.

Alternative data adds that missing agility. It brings real-time, context-rich insight into borrower behavior as their risk profiles evolve.

Used alongside bureau data, it gives lenders a clearer, faster view of changing creditworthiness.

It helps lenders:

1. Spot early warning signs before delinquencies appear, allowing proactive outreach or limit adjustments.

2. Understand short-term borrower intent — detecting liquidity stress versus planned spending spikes.

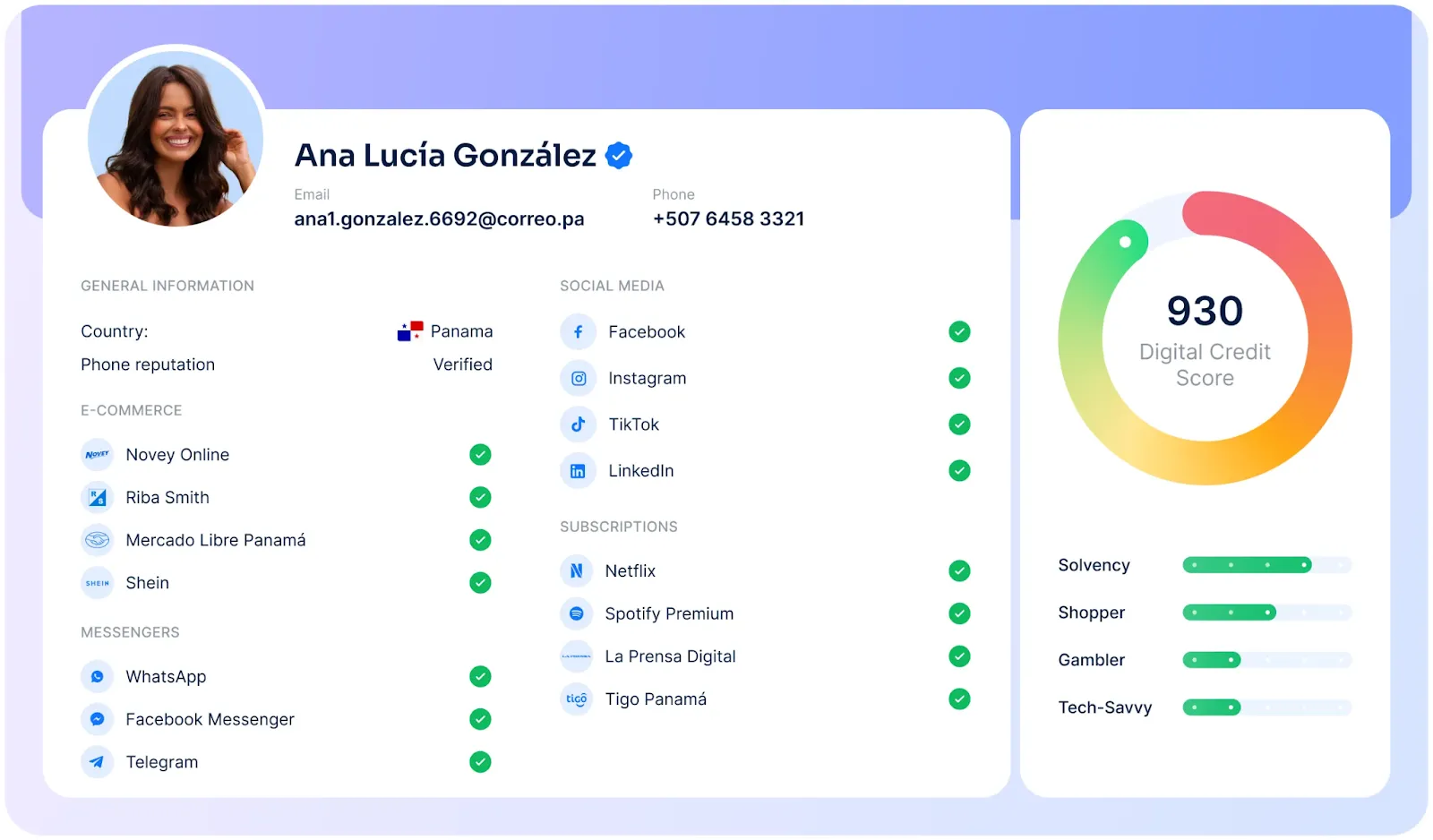

3. Identify inconsistencies or anomalies in digital footprints, such as mismatched contact data or location shifts.

4. Support more confident decisions when volumes surge and credit activity becomes harder to interpret.

For example, RiskSeal clients use real-time digital and behavioral signals to flag risk changes within hours, not weeks.

This helps them maintain approval speed while preventing exposure creep. Even at peak lending volume.

Alternative data doesn’t replace traditional credit insights; it enhances them.

During the November-December rush, this approach helps lenders spot the difference between normal spending and deeper risk. And act before problems snowball.

.svg)

Alternative data signals that matter most during the holiday season

During the holidays, borrowers open new accounts, make large purchases, and apply for credit across multiple platforms. All within days.

To stay ahead, risk teams need signals that reflect this real-time behavior and expose early signs of instability or fraud.

Below are the most valuable data indicators that top alternative data providers track when lending activity peaks.

1. Email activity and registrations

Holiday shoppers flood e-commerce sites. They create new accounts and might use multiple emails for promotions and discounts.

A sudden surge in new registrations linked to unverified domains may indicate synthetic profiles. Or even be a sign of fraud attempts.

For legitimate users, consistent, long-standing email identities often correlate with stable financial behavior.

2. Phone number intelligence

Phone data is one of the strongest identity anchors during high-volume lending periods.

Checking number consistency across applications helps spot recycled or shared numbers. These are often used in fraudulent schemes.

Numbers tied to multiple, unrelated profiles or recent SIM activations warrant attention.

Stable phone usage over time often points to a real, consistent identity. Verified carrier data can also signal stronger repayment reliability.

3. IP and device signals

IP addresses and device fingerprints offer powerful insight into behavioral authenticity.

During the rush for fast credit approvals, fraud risk rises. Anomalies like location mismatches, device changes, or shared IPs often appear first.

A customer applying from multiple countries within hours may indicate synthetic identity use. Same with switching devices mid-application.

Tracking device consistency across sessions helps risk teams block suspicious activity before approval.

4. E-commerce data

Online shopping behavior is one of the most revealing seasonal indicators.

Frequent purchases across diverse merchants usually reflect healthy consumer engagement. But excessive transaction intensity may signal overspending or identity misuse.

Merchant variety, purchase frequency, and amounts bought show how someone spends. This helps differentiate between normal holiday behavior or financial overextension.

5. Spending and subscription behavior

Recurring payments show financial discipline. Streaming subscriptions, phone plans, or digital services often remain steady. Even during heavy seasonal spending.

Consumers with consistent paid subscriptions are less likely to default after the holidays.

Tracking regular payments helps tell short-term cash flow issues apart from serious repayment risk.

6. Digital footprint stability

When multiple identifiers – email, phone, IP, device – align consistently, they form a stable digital identity.

This coherence signals authenticity and usually correlates with stronger repayment performance.

In contrast, fragmented or inconsistent digital footprints often point to higher fraud risk. And even volatile financial behavior.

By combining alternative data sources, online loan application software can spot patterns early.

This helps risk teams separate borrowers with short-term cash issues from those with deeper financial risk.

This early clarity enables decisions before portfolio quality slips. This may include adjusting credit limits, conducting proactive outreach, or offering tailored repayment options.

How RiskSeal helps lenders stay ahead of holiday lending risk

RiskSeal is a digital credit scoring platform built specifically for the credit industry.

The platform helps credit risk teams strengthen decisioning, prevent fraud, and maintain growth. Even during the most volatile lending periods of the year.

What RiskSeal checks

RiskSeal analyzes core identity and behavioral components behind every credit application. It performs deep checks across:

- Emails, assessing authenticity, age, and behavioral history.

- Phone numbers, verifying consistency, carrier reputation, and connection to known profiles.

- IP addresses, identifying location mismatches, shared networks, and proxy usage.

- Digital identity patterns, detecting synthetic or mismatched identifiers that may signal fraud.

- Behavioral trends such as eCommerce activity, spending consistency, and subscription stability.

These checks form a detailed digital fingerprint that goes beyond surface-level KYC and static bureau data.

How RiskSeal turns data into clear decisions

With RiskSeal, lenders gain a clear understanding of who is risky and who will repay. The platform enables:

- Proactive portfolio monitoring. Continuous alternative signal tracking that detects risk clusters weeks before bureau updates.

- Fraud detection at scale. Intelligent checks across email, phone, and IP that flag anomalies during seasonal application surges.

- Augmented decisioning. A digital footprint analysis system that distinguishes between genuine spenders under temporary pressure and truly scammish profiles.

RiskSeal helps credit providers find the perfect balance between growth and control.

With real-time alternative insights, they can approve more good customers and prevent costly defaults before they happen.

Final thoughts on stress testing credit risk models before Christmas

The holiday season doesn’t have to be a time of elevated anxiety for credit risk teams.

With the right data and proactive models, it’s totally possible to start lending confidently while protecting portfolio health.

Alternative data empowers lenders to act early, see risk as it forms, and turn uncertainty into informed decision-making.

Want to explore how richer digital signals can enhance your risk assessment during high-volume periods? Book a demo to see how we support lenders through every season.

See more

Explore how digital footprint analysis improves credit scoring models, boosting default prediction accuracy and approval rates in emerging markets.

Discover how alternative credit scoring differs from traditional and aids in identifying reliable clients without credit histories.

.webp)

Dive into why traditional credit scoring fails neobanks and explore smarter, data-driven solutions for assessing credit risk.