How Smarter Risk Assessment Helps Lenders Pull Ahead of Competitors

Discover how forward-thinking customer risk assessment can turn risk into revenue with alternative data, AI, and continuous monitoring.

The Credit Risk Assessment market is valued at $9.52 billion in 2025 and is expected to reach $23.97 billion by 2032.

In this race, outdated processes don’t just slow lenders down. They put them at risk.

Risk assessment has shifted from a regulatory checkbox to a driver of market advantage.

In this article, we’ll explore how lenders can turn customer risk assessment into a powerful engine for growth.

The 2026 guide to LATAM digital footprints for credit scoring

Why customer risk assessment was a cost center

The traditional approach to risk assessment was purely defensive. Lenders focused on checking boxes for rules like KYC.

Risk assessment wasn’t optional. It was mandatory for two reasons:

1. Compliance. Regulations after the 2008 crisis made AML customer risk assessment and KYC non-negotiable. If you fail to comply, you face fines or even loss of license.

2. Loss prevention. Lending required filtering out obvious defaults and fraud. Without it, the business couldn’t survive.

But the process was costly.

Teams of underwriters and analysts spent hours collecting documents, re-entering data, and manually checking applications.

Technology costs added up, too: credit bureau fees, outdated systems, third-party databases.

The result? Slow approvals, frustrated customers, and business stagnation.

It consumed resources but produced no direct revenue. Much like handling customer complaints, risk assessment was necessary, but it was never a driver of growth.

How customer risk assessment tools drive growth

Market leaders are now flipping this old view on its head. A smart, modern CRA process creates a clear competitive advantage.

This new approach allows lenders to make better, faster, and more inclusive decisions. They use it to:

- Deliver rapid approvals. Modern CRA provides customers with near-instant lending decisions. This improves the user experience and boosts conversion rates.

- Unlock new customer segments. Lenders can now safely serve individuals with little or no traditional credit history, who were previously ignored.

- Reduce financial losses. A more accurate picture of risk directly lowers default rates. This protects the bottom line and improves overall profitability.

Customer risk assessment is no longer just about avoiding fines. It is a strategic tool for acquiring the right customers and driving sustainable growth.

When done right, your risk process actively finds creditworthy applicants. It builds loyalty through a seamless experience and directly increases your profits.

Looking ahead, this shift is closely tied to broader credit scoring trends to watch in 2026. It is believed that smarter use of data and automation will shape how lenders compete.

.svg)

.webp)

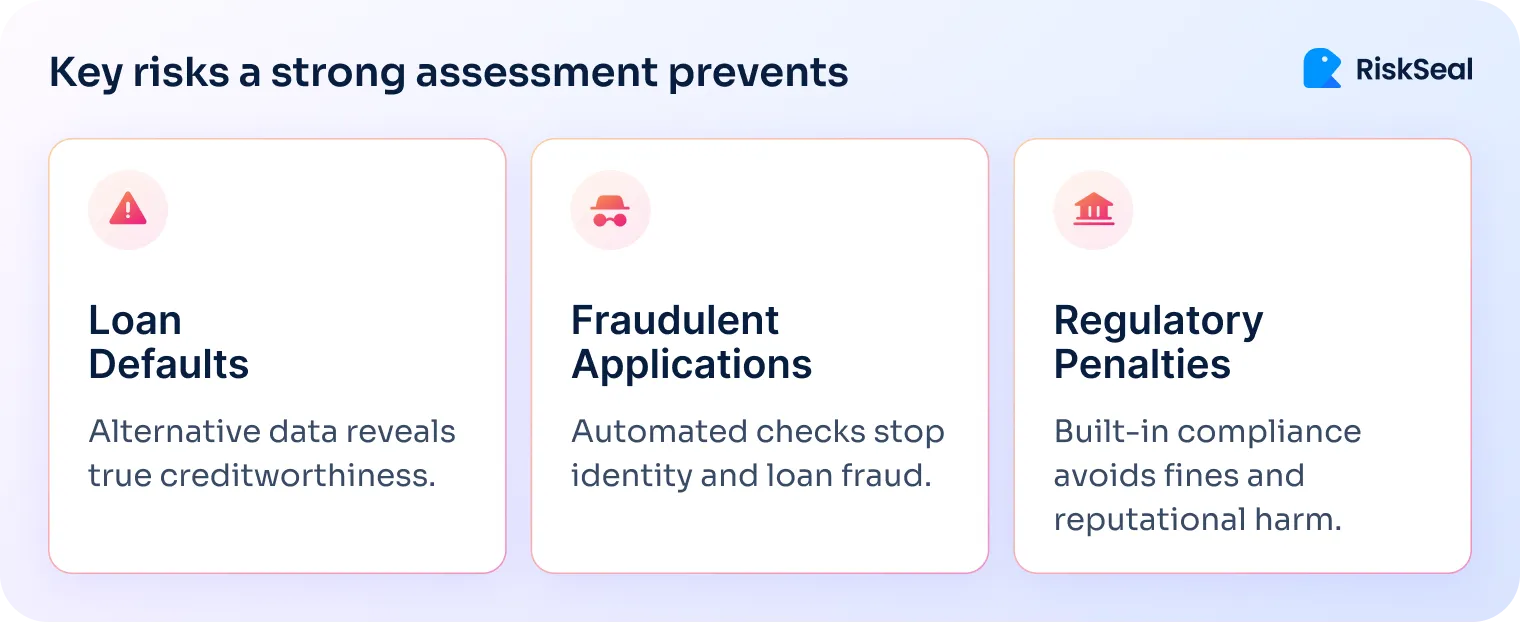

What strong risk assessment protects against

A strong AML customer risk assessment methodology is your primary defense in digital lending.

It protects your business from financial loss and regulatory penalties by addressing each risk head-on.

Reducing default rates with better data

The biggest question in lending is simple: will the borrower pay back?

The problem is that traditional credit scores don't always give a clear answer. They are often a lagging indicator of financial health and don't exist for many creditworthy individuals.

The solution is to look beyond the score. Lenders now use alternative data to build a complete, real-time picture of an applicant's creditworthiness.

This includes information like digital footprint, real-life financial habits, and employment data. Such an approach leads to fairer, more accurate decisions and reduces defaults.

Preventing fraud in digital lending

Digital channels are a prime target for fraudsters. Credit providers contend daily with synthetic identities, loan stacking, and identity theft in lending.

And the cost is far from minor. Most financial organizations report hundreds of thousands to millions in direct fraud losses each year:

Modern CRA stops fraud at the front door.

It uses automated tools for identity verification, including document checks and liveness detection.

It also analyzes behavior through device intelligence and velocity checks to spot suspicious patterns. This blocks fraudulent applications instantly, saving you time and capital.

Meeting KYC requirements automatically

Failing to meet regulatory requirements can be devastating.

Non-compliance with AML customer risk assessment and KYC rules has consequences. Including massive fines and severe reputational damage.

The right risk assessment process automates compliance. It integrates screening against global sanctions lists and databases of Politically Exposed Persons (PEPs).

This screening happens instantly during onboarding. It then continues with ongoing monitoring to ensure you remain compliant.

How alternative data improves credit risk decisions

Alternative data is the x-factor in modern lending.

It provides a deeper view of an applicant that traditional credit bureaus alone simply cannot offer.

Expand into underserved markets with confidence

Traditional scoring models often reject creditworthy applicants.

In the U.S. alone, this leaves 26 million "thin-file" or "credit-invisible" consumers without access to fair credit.

These are often young people, immigrants, or small business owners who are financially responsible but lack a formal credit history.

This is where alternative data shines.

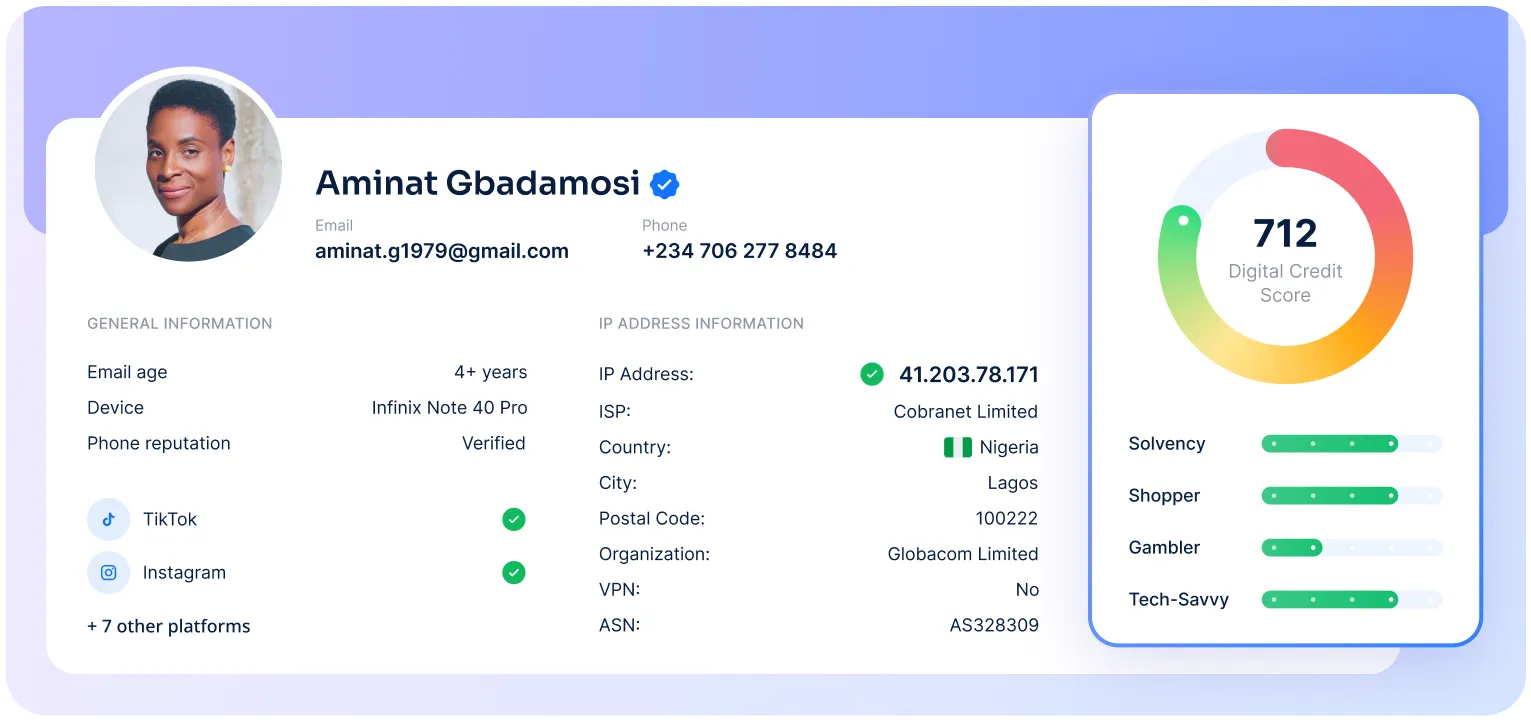

At RiskSeal, we help clients analyze a wide range of data signals to build a complete picture of an applicant. These signals include:

- Digital footprint. Information from an email address or phone number can reveal a user's history and stability online.

- Behavioral analytics. Regular payments demonstrate stable disposable income and an ability to manage recurring bills.

- Device and location consistency. Stable logins from the same device and expected locations show reliability, unlike unusual geographies or shared devices.

Using this information allows credit providers to safely approve more customers. They can confidently expand into new markets that outdated competitors are too scared to touch.

Deliver instant credit decisions your customers expect

In digital lending, speed is everything. Customers expect immediate decisions. A slow, clunky application process will send them straight to a competitor.

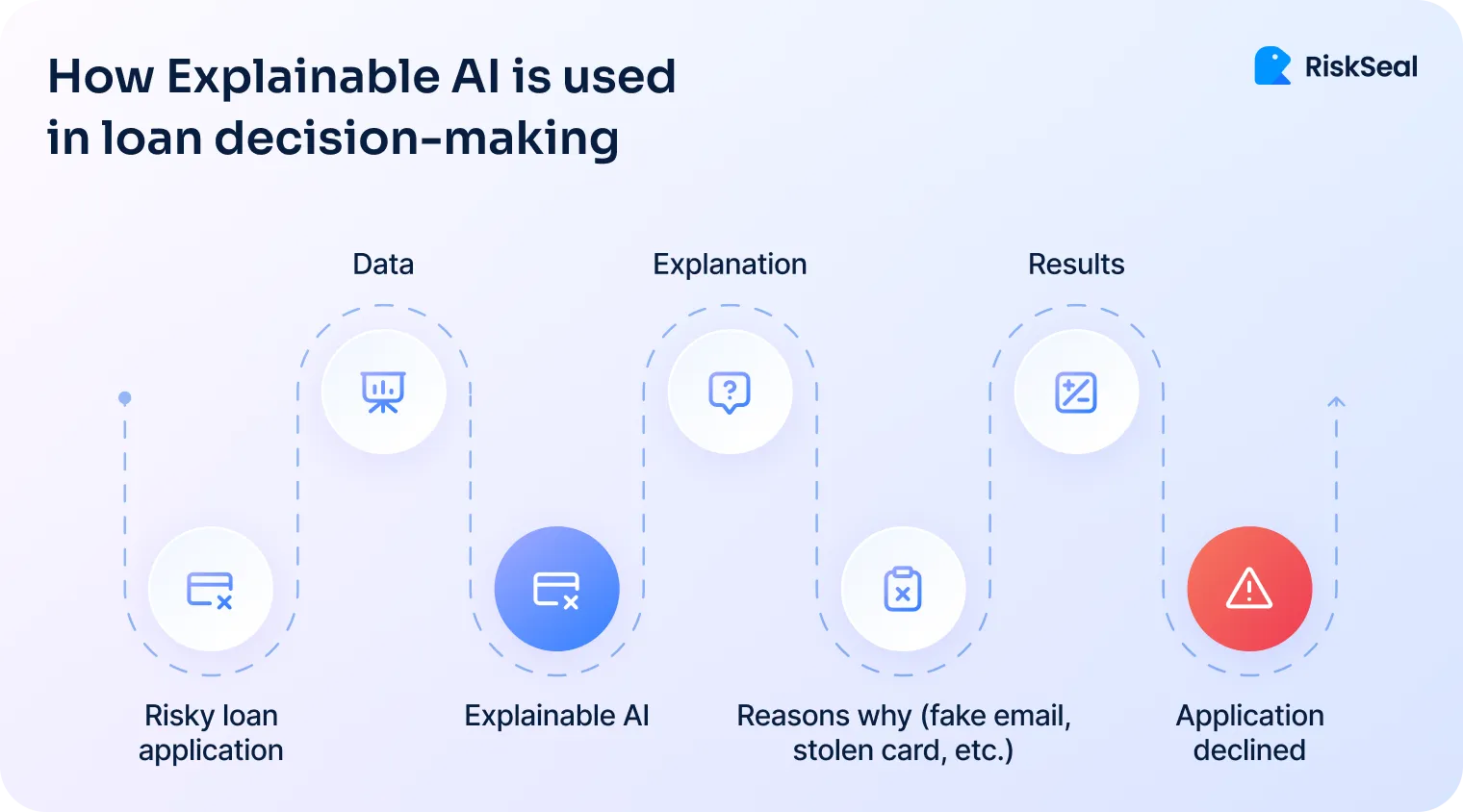

This is a problem that AI and machine learning solve directly.

AI models process thousands of alternative data points in milliseconds. They turn complex information into a single, reliable risk score.

This allows you to provide instant, automated loan decisions. A seamless, low-friction experience leads to higher conversion rates and happier, more loyal customers.

Give risk teams real-time visibility into borrower profile

Risk doesn't end after a loan is disbursed. A customer's financial situation can change.

Traditional risk management relies on static reviews. This means a lender is often the last to know when a customer is in trouble.

Modern CRA platforms offer dynamic, continuous monitoring. They analyze a borrower's financial behavior and public records in real time.

For example, the system can flag a sudden change in spending habits or a new public court record.

This alert allows you to intervene proactively with personalized support before a default happens. You move from reactive collections to proactive risk management.

Customer risk assessment example: a neobank’s growth challenge

A fast-growing neobank was targeting young professionals, a segment often lacking deep credit histories. The lender’s growth targets conflicted with an outdated risk assessment process.

The challenge

The neobank's risk department was becoming a bottleneck.

The team was overwhelmed by time-consuming application reviews. They slowed approvals and created friction.

The core problem was a choice between moving fast (and accepting higher fraud/default rates) or being safe (and rejecting too many good "thin-file" customers).

The numbers highlighted the operational strain:

The solution

To resolve this, the Chief Risk Officer integrated a next-generation CRA platform for neobanks.

The new system used AI to process 400+ alternative data points in real-time, allowing the team to instantly analyze:

- Digital footprints to flag suspicious device or location anomalies.

- Subscription payments to prove financial responsibility outside of traditional credit.

- Behavioral signals to spot early indicators of financial stress.

The results

Within six months, the new platform delivered a massive shift in core lending metrics. The risk department was no longer a bottleneck. But a strategic partner in the neobank's growth.

The takeaway

By adopting a modern, alternative data-powered CRA, the risk department transformed from a cost center into a profit accelerator.

The bank grew its loan portfolio by 30% in the next quarter without compromising asset quality.

A customer and vendor risk assessment software shouldn't just stop bad loans. It should identify and enable good ones.

RiskSeal’s approach to customer risk assessment

RiskSeal is a digital credit scoring platform built for the challenges of modern lending.

We provide the tools you need to make faster, fairer, and more profitable decisions. And see the true risk profile of every applicant.

Our approach centers on three key features designed to work together seamlessly:

Instant digital credit scoring

We provide a ready-to-act alternative score for every borrower.

Our AI-powered analysis dives deep into alternative data sources to generate this score in under five seconds. Without sacrificing accuracy.

Digital footprint analysis

We help you understand who is truly behind the application.

By analyzing a user's digital footprint, we verify their identity and assess their stability. That way, we’re effectively stopping fraud before it impacts your bottom line.

Powerful data enrichment

Our platform doesn't compete with traditional credit bureau data. It enriches it.

We add layers of unique insight from alternative data. This gives lenders a comprehensive applicant that a simple credit score could never provide.

Lenders who use RiskSeal achieve a:

- 70% reduction in KYC and customer verification costs.

- 2x increase in their customer approval rate.

- 25% decrease in their default rate.

Beyond the numbers, our work is driven by a core mission: to expand financial access for all.

By analyzing digital footprints, we uncover insights traditional credit data misses, extending coverage to underserved populations.

This allows lenders to serve the millions of "credit-invisible" individuals and businesses safely and profitably.

Final thoughts

The days of treating customer risk assessment as a defensive cost are over. That old mindset blocks growth and overlooks profitable markets.

Forward-thinking lenders now view their risk strategy as an investment. They use alternative data to safely serve new customers and deliver the instant decisions the market demands.

To win, you need more than basic checks. Partnering with an advanced alternative risk platform provides the speed and precision required to manage modern digital risk.

Want a customer risk assessment template tailored to your needs? Let’s show you in a demo.

Inside the LATAM alternative credit data report

See more

Discover four practical ways to strengthen consumer credit risk in 2026 with real-time underwriting, alternative data, smarter collections, and compliance-ready AI.

Explore the booming BNPL market and uncover how RiskSeal helps providers tackle rising fraud, defaults, and risk assessment challenges.

.webp)

Discover how social media profiling enhances credit risk management by analyzing digital footprints.