Explore key trends in alternative credit scoring that empower fintechs to assess unbanked populations.

.webp)

We analyzed 6.1 million loan applications

The results show how digital credit scores correlate with default risk.

Credit scoring is evolving and changing fast.

Traditional models miss around 1.4 billion unbanked people worldwide, according to the World Bank. That’s a huge gap for lenders.

To help close it, fintechs are turning to alternative data and digital credit scoring models. Here are 7 alternative credit scoring trends that will shape the risk assessment practices in 2026.

To stay ahead in the market, lenders must stay updated on the latest alternative credit scoring trends.

Here are the main ones:

1. Increased adoption of artificial intelligence (AI)

2. Increased integration of alternative data

3. Focus on promoting financial inclusion

4. Modifications in regulations and compliance requirements

5. Decentralized scoring using blockchain

6. Partnerships between fintech, traditional financial institutions, and tech companies

7. Use of psychometric data in scoring

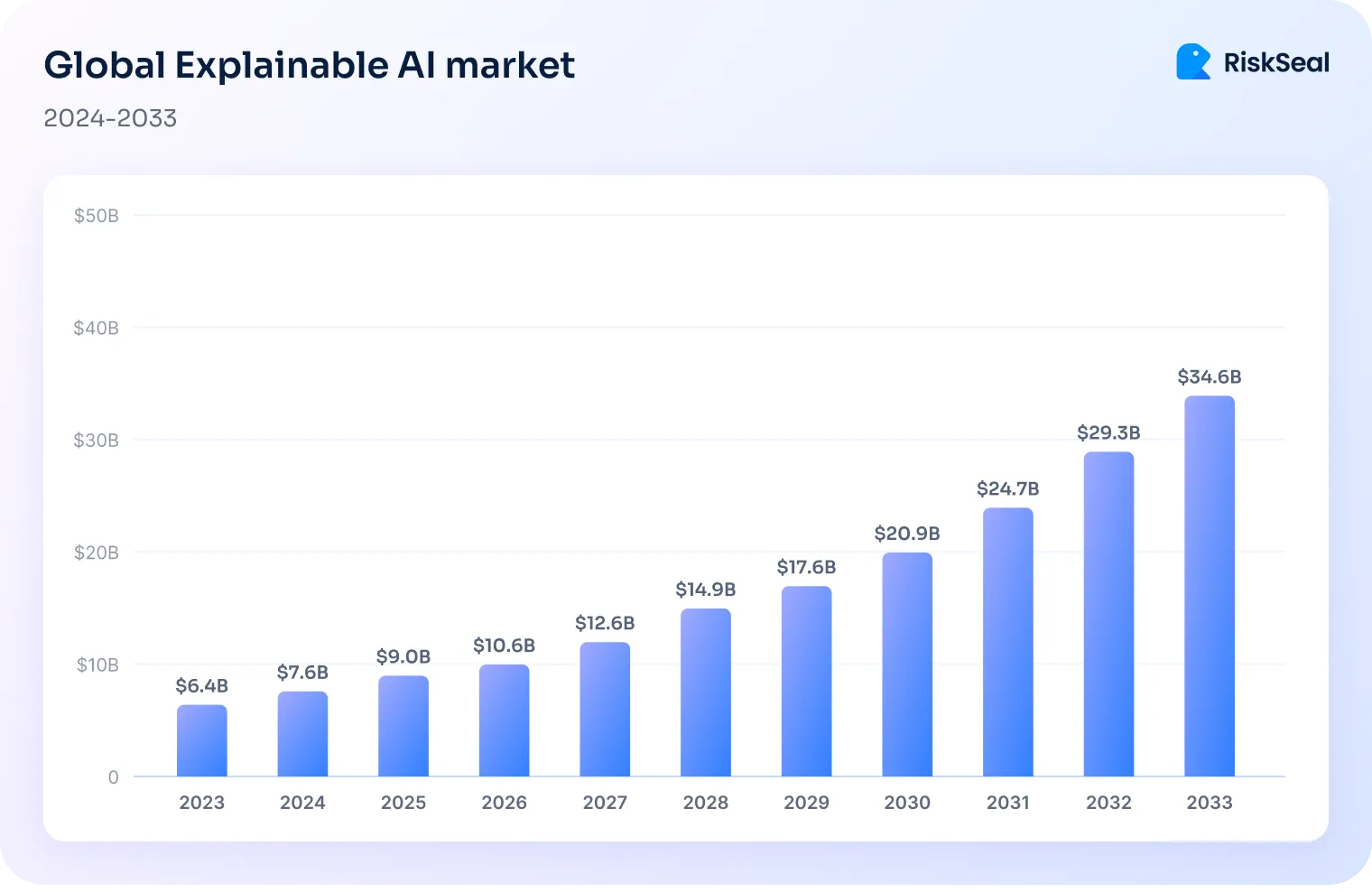

The global AI market in fintech was estimated at $10.3 billion in 2024. Experts expect it to reach $40.2 billion by 2030.

We believe fintech companies are expected to see the following AI-driven changes in the next 6-18 months.

Right now, rules limit how lenders can use AI and machine learning.

Many AI models function like a “black box”. They don’t clearly reveal how decisions are made, even as regulations increasingly demand transparency.

To meet these standards, lenders are turning to explainable AI, also known as “white box” models. They offer greater visibility into how risk decisions are made.

Stuart Tarmy, Global Director of Financial Services Industry Solutions at Aerospike, believes financial institutions need to explain the reasoning behind AI-based decisions to customers. He views such transparency as both a regulatory necessity and a competitive advantage.

Similarly, Stratyfy highlights the urgency of model interpretability in lending. They recommend striving for “a level of transparency suitable for high-stakes use cases that truly impact people’s lives, such as determining who gets a loan or a job.”

With the EU AI Act’s explainability rules taking effect by August 2026, explainable models are set to become standard next year.

Risk for lenders: AI decisions may be non-transparent, potentially unfair, and hard to justify to regulators.

How to manage:

This method uses smart algorithms to predict how likely someone is to repay a loan. It looks at alternative data using tools like regression and neural networks.

A 2025 study found that multilayer neural networks and logistic regression were top performers in classifying loan repayment risk. Especially as neural nets captured complex borrower patterns.

V7 Labs also notes that AI models now analyze thousands of variables and learn from past outcomes. This makes them more accurate than traditional scoring methods.

With these advancements, tools like regression and neural networks are expected to become standard in credit risk evaluation by 2026.

Risk for lenders: Models trained on biased or unbalanced data may result in discriminatory outcomes and affect fair lending laws.

How to manage:

AI can process large amounts of data instantly. Machine learning models find patterns and spot unusual borrower behavior. The use of AI in credit risk management allows lenders to make fast, automated lending decisions. It also improves fraud detection and real-time borrower assessment.

In the next 6-12 months, more digital lenders are expected to adopt real-time AI tools to scale quickly and cut costs.

A 2025 analysis by TurnKey Lender predicts that real-time lending powered by AI and automation will become standard by the end of the year, enabling loan approvals in minutes. GenAI tools are already helping lenders automate full workflows and boost decision accuracy.

Similarly, a March 2025 ITFA report highlights that AI enables lenders to react instantly to changes in borrower behavior and market conditions. This makes dynamic risk assessment a core feature of modern lending platforms.

Risk for lenders: Undetected anomalies, model drift, or fraud attempts may go unchallenged in a fully automated pipeline.

How to manage:

Fintech companies are starting to rely more on non-traditional data to judge if someone can repay a loan.

A study by the National Bureau of Economic Research found that digital footprint signals can predict loan defaults as accurately as traditional credit scores. Using both together improves accuracy even further.

Governments are also expanding legal frameworks to support this shift.

In India, starting April 2026, the Income Tax Department will have the authority to review individuals’ digital activity. This will include social media and online financial accounts to detect fraud and tax evasion.

By 2026, the lack of credit bureau data will no longer be a barrier to access. Borrowers will increasingly be assessed on their digital footprint, enriched with alternative credit data that reflects real behavior.

Here are examples of alternative data that can be used for this:

All these alternative points form digital footprints of potential borrowers. Many credit organizations working with RiskSeal say this data will play a key role in credit scoring by 2026.

Risk for lenders: Alternative data may be inconsistent, unverified, or raise privacy concerns. If misused or poorly interpreted, it can lead to inaccurate credit decisions or privacy violations.

How to manage:

Limited financial inclusion is a serious problem. It is especially acute in developing countries.

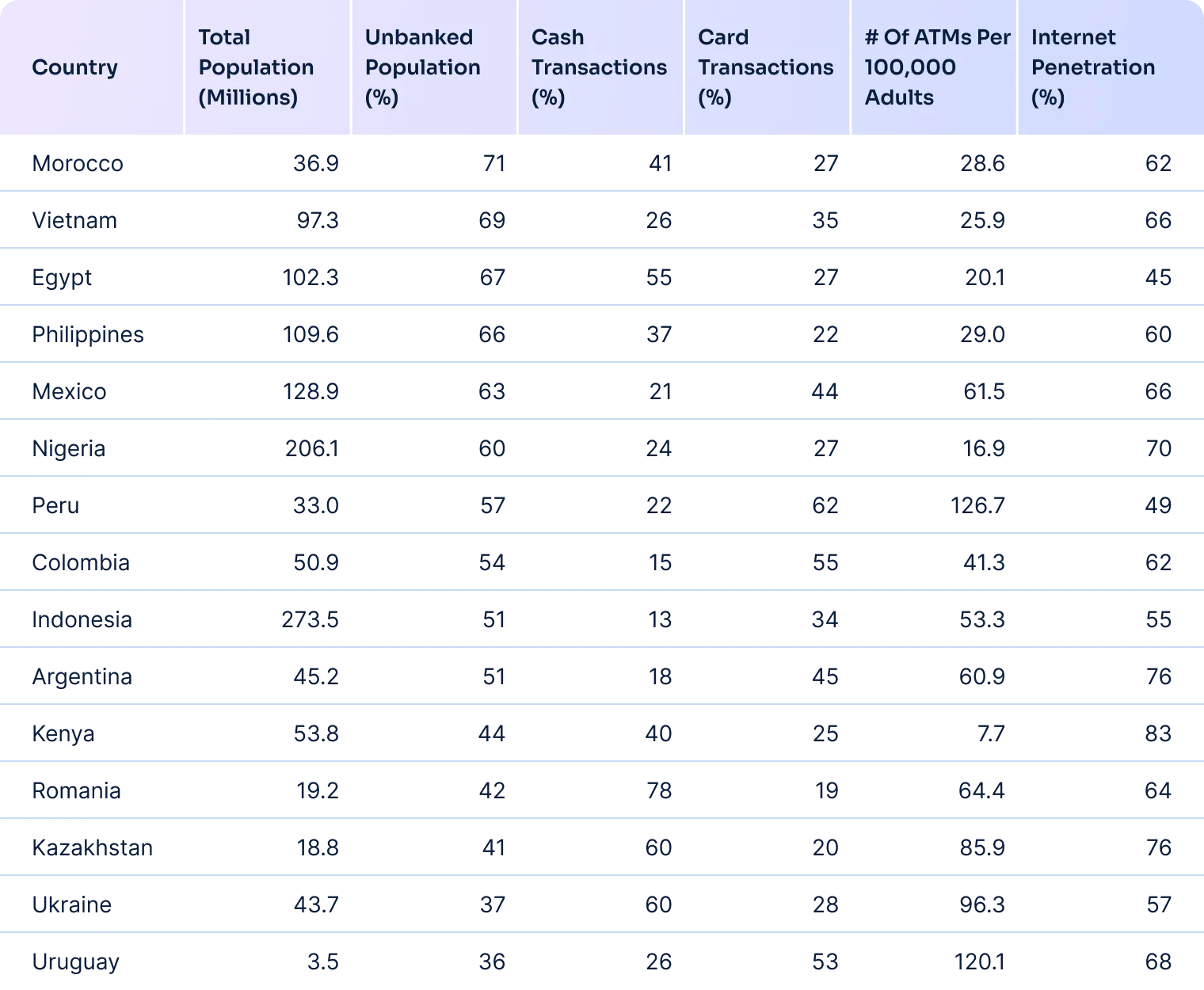

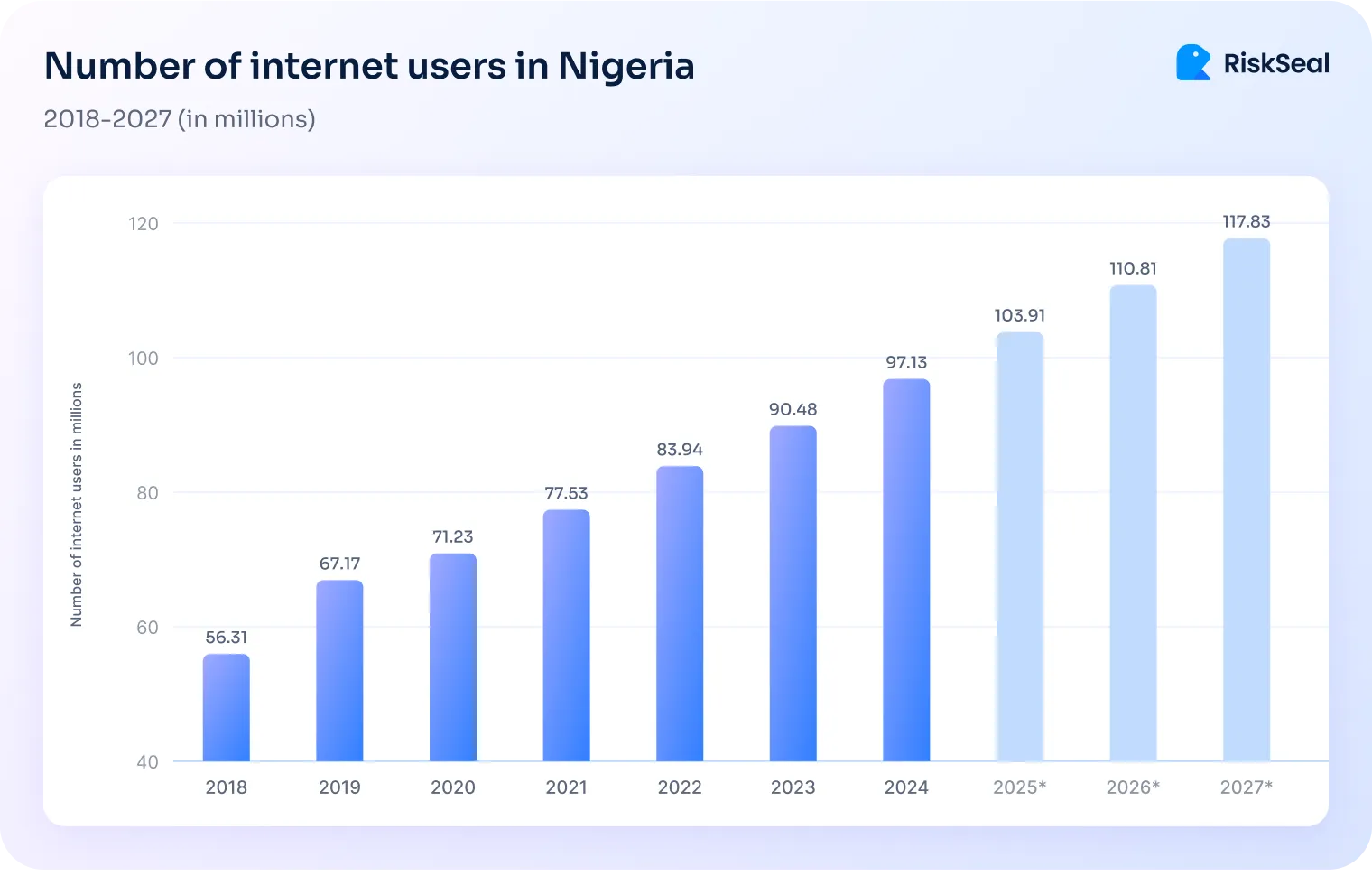

In Nigeria, only 40 percent of people have recourse to banking services. In Mexico, the situation is even more striking. Only 37% of the working-age population there hold bank accounts.

Alternative credit scores allow lenders to find a way out and increase financial inclusion. Unlike traditional banking services, the internet is far more accessible to people.

For example, let's look at the internet penetration in Nigeria and Mexico.

According to Statista, almost 75% of Mexicans are active online, and their number will continue to increase:

In Nigeria, the figure is slightly lower at around 45%. However, it is still higher than the percentage of residents covered by banking services.

A study by Harvard Business School showed that alternative data in lending models reduced rejection by 70% for borrowers typically excluded by traditional scoring. Especially for those with thin or no credit history but low default risk.

With alternative data enabling more inclusive credit assessments, we believe many fintechs will increasingly adopt these tools in 2026.

This shift will help them better serve underserved and first-time borrowers.

Risk for lenders: Expanding credit access may increase approval of high-risk or unqualified applicants.

How to manage:

Regulations on creditworthiness are changing as technology grows. This is because more personal data is being used in lending.

To protect users, lenders must follow key laws:

What’s changing in creditworthiness rules in 2026

By 2026, new rules in the EU and the US will change how lenders assess creditworthiness. The EU’s CCD2 and AI Act will push for fairer and more transparent credit scoring.

In the US, the CFPB’s open banking rule will make it easier to use more types of data to evaluate borrowers.

Risk for lenders: Conflicting local and global rules may create legal risks or force lenders to shut down certain scoring models.

How to manage:

Decentralized scoring enables the use of blockchain technology to create a reliable credit score.

Here are some of the benefits and challenges of this approach:

According to the research, blockchain is already moving from proof-of-concept to practical use. Including areas like supply chain finance, cross-border payments, and asset securitization.

In regions where 1.3 billion adults remain unbanked, blockchain and mobile wallets offer a pathway to financial inclusion.

These decentralized tools expand access to capital and enable participation in digital finance. Especially through microloans and crowdfunding.

That’s why RiskSeal expects more early-stage fintechs to begin testing blockchain-based credit scoring by 2026. Particularly in mobile-first markets with limited credit infrastructure.

Risk for lenders: Blockchain-based scoring may use unverified or incomplete data. Borrowers could hide negative information. It also raises privacy concerns due to public data visibility.

How to manage:

Synergy between fintechs, banks, and software development companies is already revolutionizing credit scoring. Each has a crucial part to play in this process.

When they work together, fintechs bring new ideas, banks bring experience, and IT companies provide tech support.

According to the Insight Report by the Cambridge Centre for Alternative Finance, 84% of fintechs are already partnering with traditional financial institutions. The findings are based on data from 240 fintech firms operating across 109 countries.

These partnerships often take the form of API integrations, collaborations with tech providers, and funding agreements. The main drivers are access to infrastructure (48%), product and service innovation (34%), and improved credibility and trust (34%).

That’s why we believe over the next 6–12 months, these partnerships will deepen. They will accelerate digital onboarding, expand product offerings, and help reach more underserved markets.

Risk for lenders: Misaligned goals or poor coordination between partners can slow progress. It can also cause credit scoring results to be inconsistent.

How to manage:

Alternative credit models are starting to include behavioral and cognitive traits. Especially in regions where formal credit history is limited or nonexistent.

Here’s how psychometric checks are used in credit risk management:

Lenders use psychometric data to assess reliability, emotional stability, and financial discipline.

By comparing test results to large datasets, they can identify behavioral patterns that are hard to fake. This helps evaluate applicants with no credit history while reducing fraud risk.

A 2025 global study found strong results from psychometric testing in lending. At Juhudi Kilimo, a Kenyan lender, it increased credit acceptance rates by 5%. It also improved predictions of repayment compared to financial data alone.

We at RiskSeal think more and more fintechs will start adopting psychometric analysis by 2026. In our view, even fintechs in data-rich markets may still struggle with precision in borrower assessment. Psychometric scoring could offer a valuable layer of insight.

Risk for lenders: Scoring based on behavior may raise ethical concerns. It can also create unintended bias if not carefully designed and validated.

How to manage:

At RiskSeal, we bring the future of credit assessment to life, combining AI and alternative data. We enable data-driven lending practices to support lenders across emerging markets.

Artificial intelligence is at the core of RiskSeal’s platform. It helps lenders go beyond traditional credit scores. We apply AI to uncover hidden risks and identify trustworthy applicants.

Here’s how we use AI:

As a result, RiskSeal helps lenders detect up to 70% of fraud at the application stage, reducing defaults and lowering KYC costs.

RiskSeal uses a wide range of real-time, digital signals. This is especially valuable in markets where traditional data is unavailable.

We analyze:

These 400+ data points help lenders understand who the applicant really is beyond a traditional score, enabling precise digital credit scoring and fairer lending decisions.

In regions like Honduras, Nigeria, and Mexico, millions remain unbanked, but are active online. RiskSeal bridges this gap by making their digital footprint count.

Our technology helps lenders reach:

This approach makes credit more inclusive while still managing risk responsibly.

RiskSeal is designed with regulatory compliance in mind. We ensure that innovation never comes at the cost of data privacy or fairness.

RiskSeal isn’t just following trends. We’re helping shape them, with a platform that’s fast, secure, fair, and built for emerging markets.

Alternative credit scoring is becoming a standard. By adopting new technologies and data sources, fintechs can reach more people and manage risk more effectively.

Knowing these 7 trends will help lenders adapt in a highly competitive credit industry.

We analyzed 6.1 million loan applications

The results show how digital credit scores correlate with default risk.

What is alternative credit scoring?

Alternative credit scoring is an approach to estimating the creditworthiness of potential borrowers based on the use of non-traditional data sources.

Among them are a history of online payments, social network activity, mobile phone usage, etc.

What are the key trends of alternative credit scoring?

Six key trends stand out in alternative credit scoring.

First, the use of AI is growing, improving how credit is assessed. Second, blockchain technology is being used to increase security and transparency. Third, more companies are using alternative data like utility bills and social media to evaluate credit.

There’s also a strong focus on financial inclusion, aiming to provide credit to underserved populations. Ensuring compliance with regulations is crucial, and finally, partnerships between fintechs, banks, and tech companies are becoming more common to drive innovation.

How is RiskSeal driving innovation in alternative credit scoring?

RiskSeal is an AI-based Digital Credit Scoring system that uses digital footprint analysis to evaluate borrowers.

Our company leverages advanced technology and the vast potential of alternative data to enhance financial inclusion, reduce risk, and increase loan approvals.

Explore how alternative credit scoring reduces CAC by improving risk segmentation, fraud filtering, and approval quality.

Discover global lending trends that can shape credit scoring strategy for successful financial inclusion.

Discover four practical ways to strengthen consumer credit risk in 2026 with real-time underwriting, alternative data, smarter collections, and compliance-ready AI.

.svg)

.webp)