How Data Enrichment Helps Lenders Approve More with Less Risk

Learn how data enrichment enhances credit risk models by filling gaps, spotting fraud early, and supporting inclusive lending.

.webp)

You have an applicant’s email address, a phone number, and less than a second to decide: approve, reject, or send to manual review.

That’s the pressure credit risk managers face daily.

And it’s no surprise that more lenders are investing in better tools.

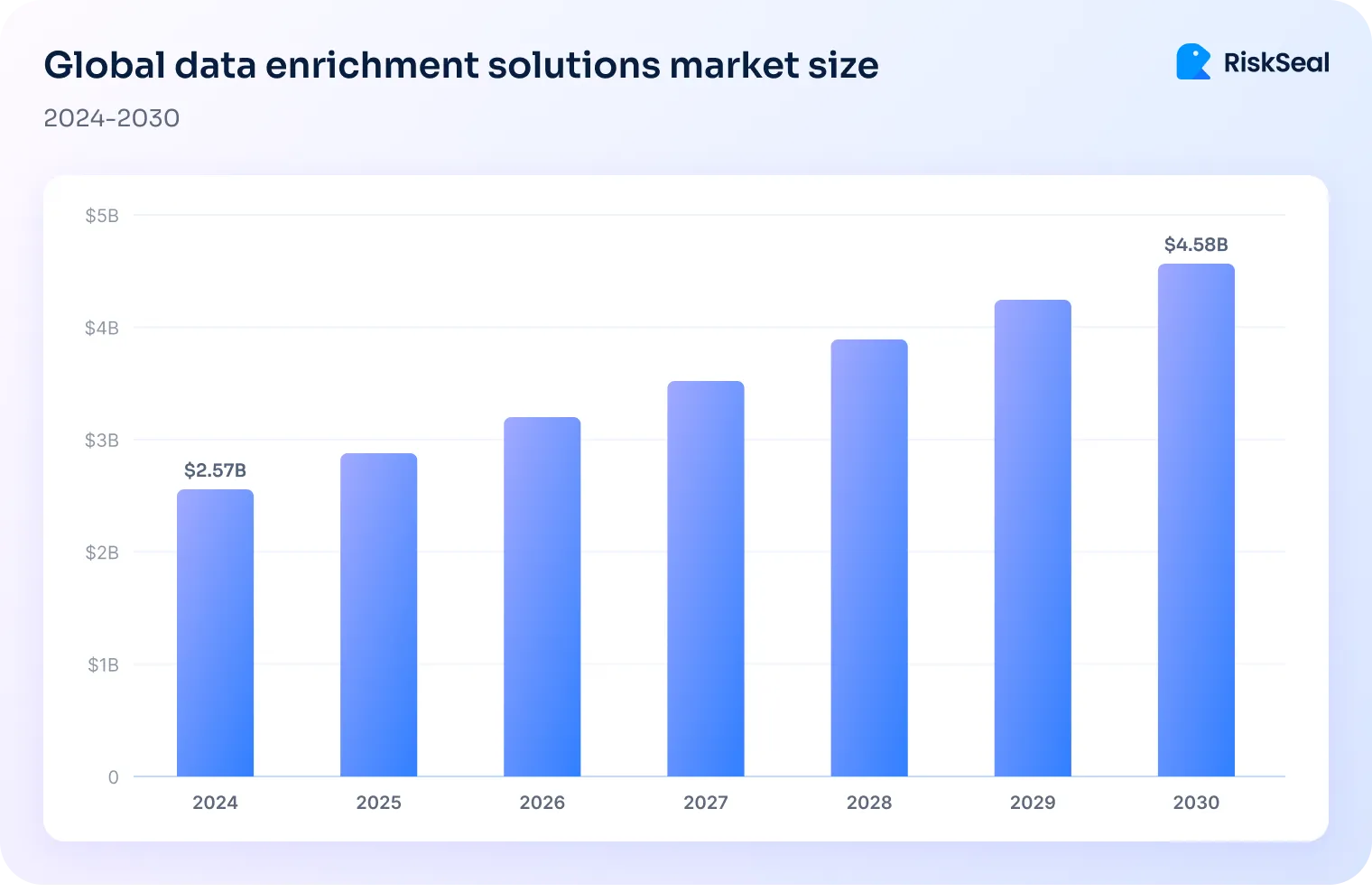

The value of the global data enrichment solutions market was at $2.57 billion in 2024. It is expected to reach $4.58 billion in revenue by 2030, growing at a 10.1% CAGR.

Explore a silent process that fills in the gaps and helps lenders say “yes” or “no” faster and more confidently – data enrichment.

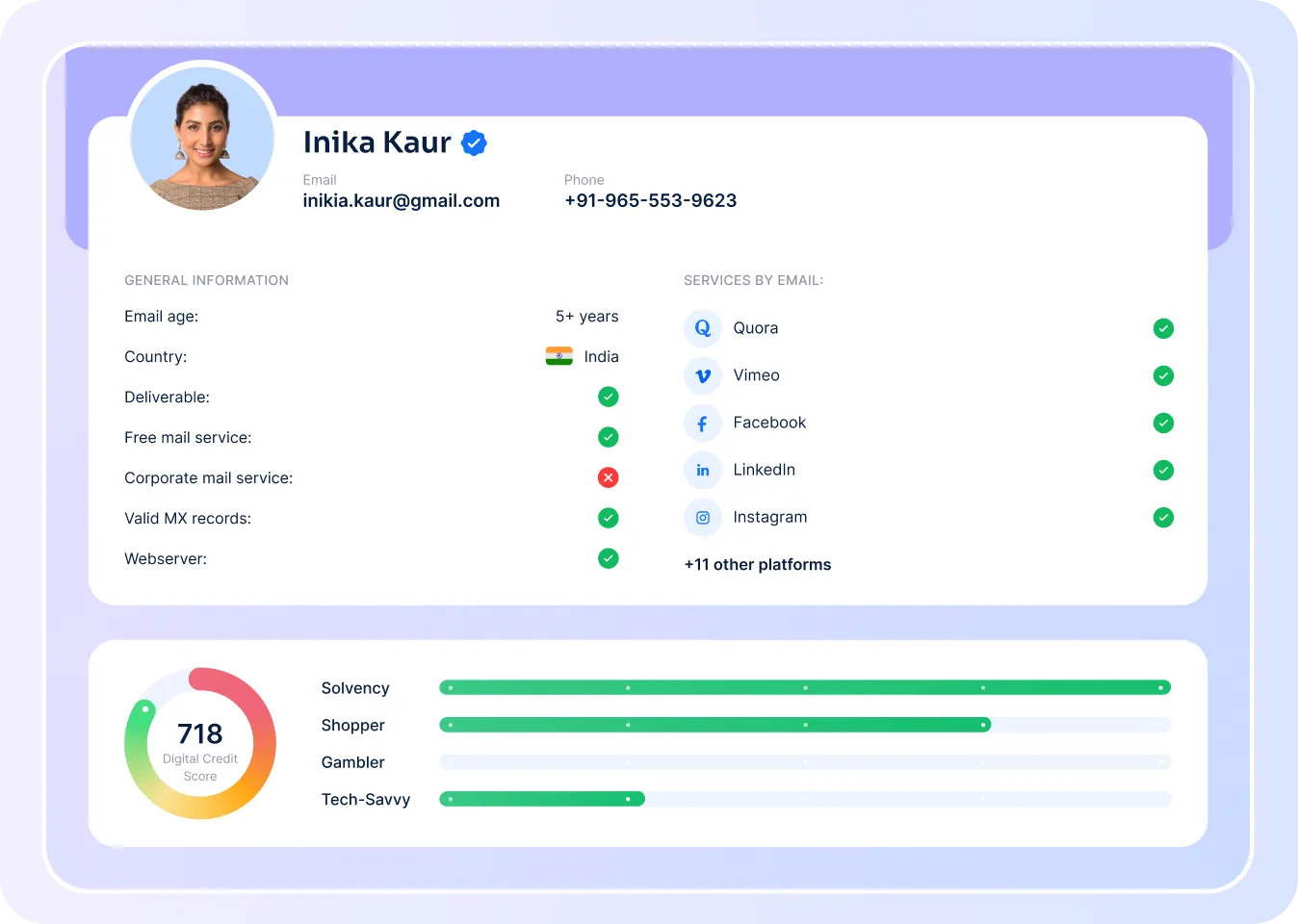

What is data enrichment through a credit lens?

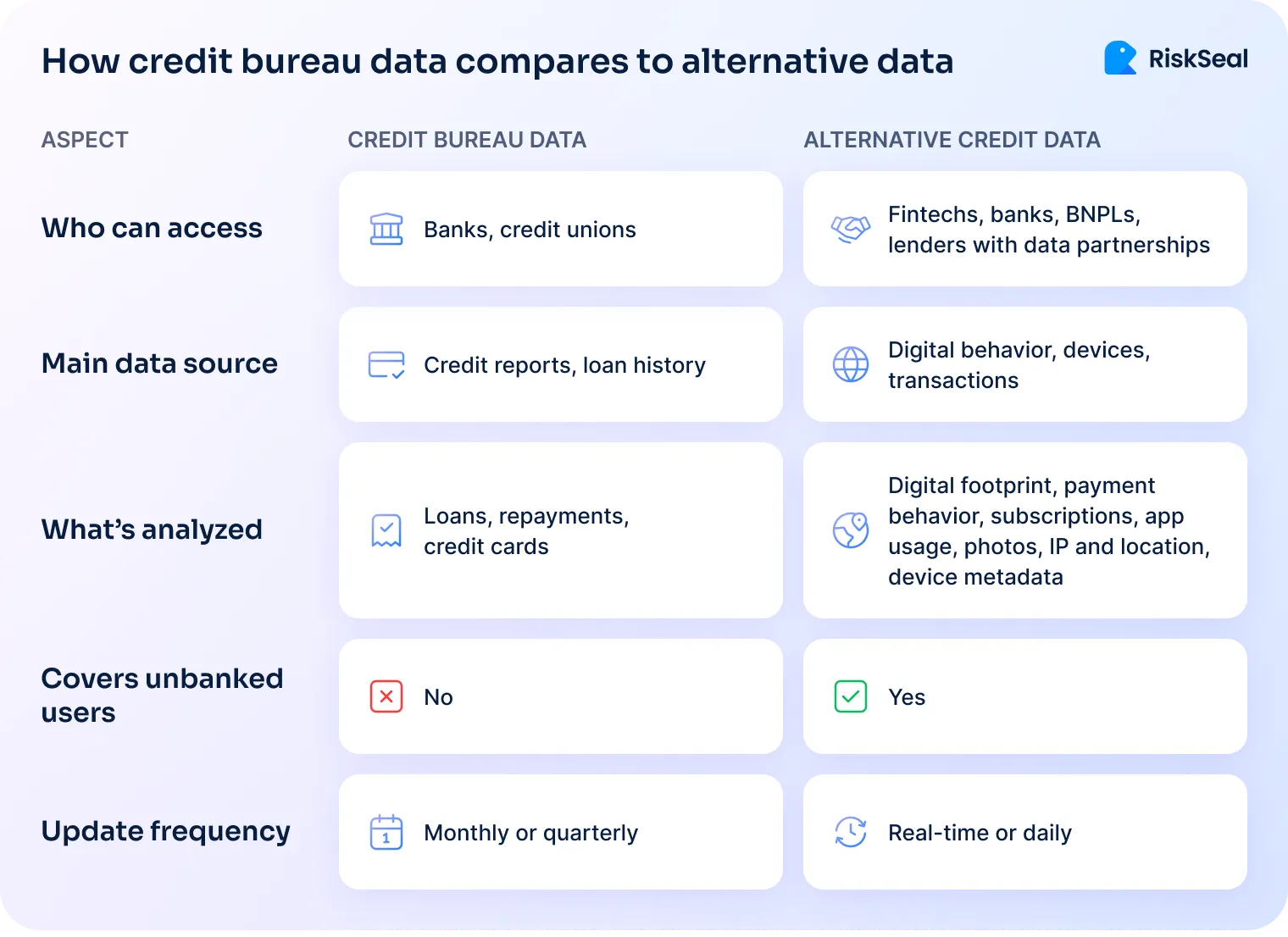

Data enrichment in credit means adding alternative information to traditional credit data.

There are many different types of alternative data in lending, such as digital behavior, utility payments, transaction histories, and social profiles.

By showing the full picture, data enrichment helps lenders serve people who are invisible to traditional models. Also, this extra layer of insight allows them to spot more hidden risks.

4 ways B2B data enrichment solutions power credit risk models

Partnering with alternative data providers is key to a more transparent view of every applicant.

Here are just a few ways this kind of data strengthens risk models.

1. Filling the gaps

When traditional checks fall short for no-file or thin-file applicants, enriched digital signals step in.

They reveal patterns of stability and intent that help lenders see a clearer credit picture.

2. Spotting red flags early

Data enrichment flags suspicious combinations, such as a brand-new email, a proxy IP, or a disposable phone number.

These often point to synthetic fraud. This early warning gives lenders a chance to filter out risky applications.

3. Speeding up approvals

Applicants who show strong digital trust signals can move through the process faster.

Enrichment helps lenders separate these low-risk profiles so they can reduce manual reviews.

4. Refining the score

Extra data deepens your scoring models and paints a fuller picture of each applicant.

It allows lenders to expand their services to reach unbanked and underbanked segments.

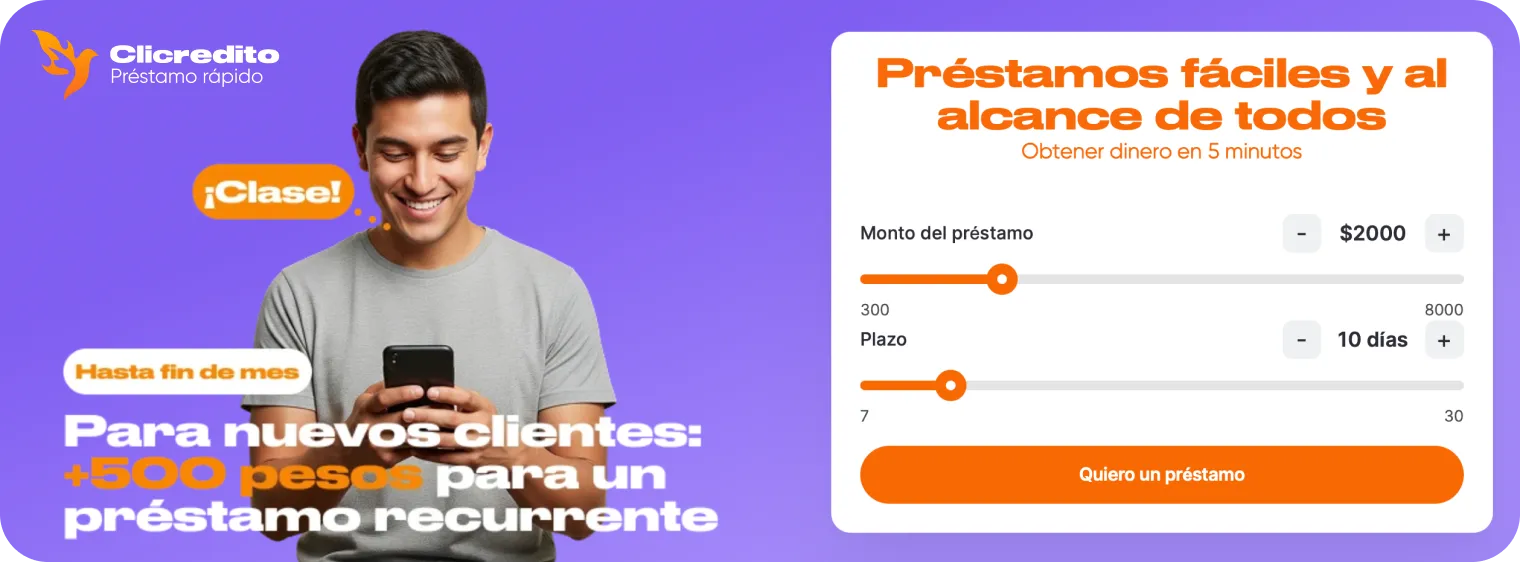

Case study. Clicredito MX scores “invisibles” with data enrichment

Can a data enrichment solution fuel a lender's growth?

Yes, and Clicredito MX proved it by leveraging alternative data to scale up its approvals.

What happened?

Clicredito MX is a Mexican fintech company built to give consumers rapid access to capital. They offer a fully digital application and can disburse funds within minutes.

Due to this speed and convenience, the number of applicants grew rapidly.

What went wrong?

With many applicants new to credit, Clicredito MX found it hard to assess them using traditional data alone.

Thin files and lack of credit histories kept approvals low, putting a ceiling on growth.

How the challenge was tackled

That’s when they partnered with RiskSeal to look beyond credit reports.

RiskSeal pulled in alternative financial stability signals from digital footprints analysis.

That way, Clicredito MX became able to evaluate applicants’ real financial discipline.

The result

By adding RiskSeal’s alternative data to traditional scoring, Clicredito MX made much better credit decisions.

They approved more applicants with little or no credit history and caught fraud faster.

All without taking on extra risk.

The takeaway

Data enrichment helped Clicredito MX grow by making invisible customers scorable.

By using new insights into applicant behavior, they approved more loans, lowered defaults, and became a more trusted lender.

Alternative data sources to enrich your credit model

Here are some of the most valuable and proven data sources for enriching your credit models.

RiskSeal uses over 400 data points behind the scenes. But here we’re sharing signals giving the most actionable insights, the ones we never run a check without.

1. Email and phone lookup data

An email address is part of every internet user’s life. Looking closely at it can reveal a lot about who your borrower really is.

Example: Imagine an applicant with a five-year-old email, linked to active social profiles. They look far more trustworthy than one using a brand-new throwaway address.

2. Social media and messenger presence

Data available through digital footprint reveals valuable clues about an applicant’s real-world habits and identity.

Example: An applicant with a long-time Facebook profile looks much more credible than someone with new or empty online profiles.

For Mexican applicants, accounts on services like Didi Taxi are a must as well.

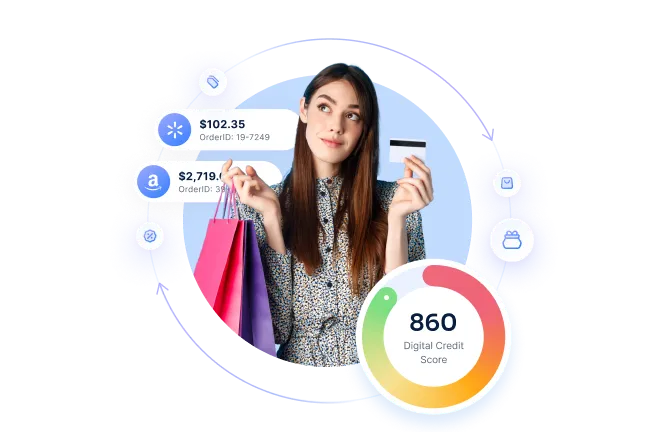

3. E-commerce activity

Shopping behavior can reveal a lot about a borrower.

Activity across popular marketplaces and local online stores gives risk managers a clearer sense of their stability and trustworthiness.

Example: A long-standing Amazon account with consistent purchases indicates payment discipline.

For an Indonesian borrower, regular shopping on Tokopedia also reinforces this.

4. Subscriptions

Today, it’s hard to imagine someone without at least one streaming subscription like Netflix or Spotify.

Paid service engagement offers a lens into a borrower’s disposable income and financial discipline.

Example: An applicant who has kept up their paid subscriptions for several years is showing strong financial habits.

This suggests they’re more likely to repay a loan, something RiskSeal’s clients often observe in practice.

5. Web registrations

Logins, registrations, and activity on everyday platforms offer strong clues about a borrower’s habits.

Beyond global names, regional services also add valuable context. RiskSeal clients often find the most telling insights there.

Gambling sites are especially noteworthy. In some locations, they’re a serious red flag. Elsewhere, lenders may see this as a grey area and don’t necessarily exclude applicants just for having an account.

Example: A software engineer applied for a loan. His digital footprint was tied to long-active GitHub and Stack Overflow accounts with years of contributions.

This consistency reassured the risk team that they were dealing with a real person, not a freshly created synthetic profile.

6. Location and device signals

Location and device clues give lenders a clearer view of where and how applicants connect.

By looking at IP data, GPS information, and device details together, risk teams can catch red flags that often slip through standard checks.

Example: An applicant listed a Dutch address and phone number, claiming to live in the Netherlands.

But their IP traced back to Somalia, and the device ran old Android firmware. This raised immediate red flags during screening.

7. Name matching and face recognition

Name matching and face checks help credit providers verify who applicants really are.

By comparing names across emails and social profiles, and then checking avatars, they can spot inconsistencies that traditional data often misses.

Example: A man applied for a loan as Carlos Hernández, using the email carlos1hernandez.official@gmail.com.

But checks revealed his Facebook profile used the name Ali Junaid, and his Telegram username was @junaid_crypto_2022.

His LinkedIn wasn’t linked to the email, and his avatars included an actor’s face and the Bitconnect logo. These inconsistencies raised strong synthetic identity signals.

.svg)

The future of data enrichment solutions in credit scoring

Data enrichment goes far beyond today’s credit decisions. It is also shaping what’s coming next in credit decision-making.

1. From alternative to essential

What we once called “alternative data” is now at the core of modern risk assessment.

Borrower profiles draw on transaction habits and online behavior, not just traditional credit reports.

This shift helps lenders double approval rates and run applicant checks in under 5 seconds.

Neobanks already use AI to:

- Adjust credit limits as spending patterns change.

- Spot fraud or default risks as they happen.

- Support borrowers with irregular incomes.

Privacy still needs attention, so regulators are moving in this direction too. Policies like the EU’s GDPR show that digital footprints can help promote financial inclusion.

BNPL platforms use bank transaction data, like unreported loans, to fill gaps left by traditional reports. The two new FICO models now incorporate BNPL data for the first time, bringing these loans directly into mainstream credit scoring.

Together, these examples make one thing clear: dynamic, data-rich credit decisions are becoming the new normal.

2. AI-native scoring will rely on real-time signals

Credit scoring is shifting to live data that updates as life happens. Static reports are being replaced by real-time signals like device security and spending habits. This helps lenders lower default rates and improve approval accuracy.

Neobanks like Revolut and Chime already check device security (OS updates, VPN use, jailbreak status) as part of their risk screening. A study showed a 30% drop in application fraud after these real-time device signals were prioritized.

And it doesn’t stop there. Lenders now look at:

- IP and geolocation mismatches.

- Suspicious mouse movements and browsing behavior.

- Real-time income shocks and cash flow changes.

This kind of data makes it easier to catch risks early and adjust decisions as circumstances change. FICO® Score 10 T already factors in trends over time, and BNPL providers like Affirm use spending alerts to spot problems faster.

Of course, this comes with new challenges:

- Fairness rules need careful attention.

- Real-time systems require more robust, costly tech.

Still, the direction is clear. Brazil’s open banking rules encourage live data sharing. Companies like Mastercard already adjust authorization based on real-time behavior.

In the foreseeable future, AI-native scoring will be standard practice. It will align credit decisions better with real-world behavior.

3. Enrichment will power inclusive credit by design

Enrichment helps lenders see people who would normally stay invisible.

By using alternative data, it opens doors for gig workers, immigrants, young borrowers, and informal earners.

This shift is already happening:

- Real-time scores built on ride-hailing, e-commerce, and gaming data.

- Dynamic signals like gig earnings, remittances, and informal income.

- Live credit checks powered by delivery driver earnings or online sales.

This matters because it helps lenders evaluate underserved groups more fairly. Governments and NGOs see this too.

In India, the RBI’s Guidelines on Digital Lending encourage using alternative data, like utility bills or digital payments. It helps bridge the credit gap for the 190 million unbanked.

In Mexico, fintech law supports similar goals by allowing companies to use AI-driven models and alternative data.

These efforts show how policies around the world are making financial services more inclusive.

4. Explainability and ethics will shape the space

As AI models grow more complex and more influential, lenders need to focus on making them clear, fair, and trustworthy.

Decision-making can’t stay a black box, especially when people’s finances are at stake.

This shift is driven by several key forces:

- Regulatory pressure, like the EU’s AI Act and CFPB guidance in the U.S. requiring lenders to explain automated decisions.

- Ethical expectations, where biased algorithms ruin trust and reputations. A recent example is the Apple Card controversy case.

- Provenance and auditability, ensuring every data point and outcome can be tracked and defended if challenged.

That’s why lenders are already turning to:

- Fairness tools like IBM’s AI Fairness 360 and Google’s What-If Tool.

- Auditable AI platforms like DataRobot and H2O.ai, which log decisions for future review.

- Enhanced documentation, so they can show exactly how utility bills or gig income shaped a score.

As new rules, public attention, and better technology come together, clear and fair AI is becoming the standard.

Lenders who follow these practices will earn more trust, and those who don’t may be left behind.

Data enrichment at RiskSeal

Data enrichment is what sets RiskSeal apart. It turns scattered data into clear, actionable insights for every applicant.

Here’s what RiskSeal’s enrichment functionality does:

- Data. Combines traditional credit data with alternative signals.

- Sources. Pulls information from 200+ trusted online platforms.

- Coverage. Includes both regional and global platforms.

- Signals. Flags suspicious details like disposable emails or risky IPs.

- Updates. Provides real-time information to support instant decisions.

And all of this happens in less than 5 seconds per applicant.

Final words

Data enrichment reveals a lot that traditional checks often miss. It turns incomplete profiles into real, human stories, so lenders can make decisions with more confidence.

Ready to see how many more applications your organization can approve safely? Book a demo with the RiskSeal team today.

See more

Discover how forward-thinking customer risk assessment can turn risk into revenue with alternative data, AI, and continuous monitoring.

Master the credit risk metrics that actually protect your portfolio. Learn how top fintechs track, interpret, and act on risk signals in 2026.

Explore the booming BNPL market and uncover how RiskSeal helps providers tackle rising fraud, defaults, and risk assessment challenges.