Credit Risk as a Competitive Advantage: Turning Risk Decisions Into Growth

Rethink credit risk to capture growth opportunities traditional scoring leaves behind.

Competitive pressure in lending has never been fiercer. Every lender is racing to approve faster while staying safe.

Yet most are stuck doing credit risk the same way.

The question isn't whether you can avoid losses. It's whether your credit decision platform can capture opportunities your competitors miss.

Why traditional credit risk management no longer differentiates lenders

The credit risk market has become structurally commoditized.

Most lenders base decisions on the same bureau data and the same core scores. That data is necessary, but it no longer creates advantages. It defines the baseline.

When many institutions rely on identical inputs, outcomes converge. Approval rates look similar. Decline reasons repeat. Risk distribution across portfolios starts to resemble the market average.

This is a consequence of shared infrastructure.

Traditional credit data was designed for stability, not differentiation. It changes slowly and reflects past behavior by design. That makes it reliable, compliant, and widely accepted, but also uniform.

The borrower pool itself has also shifted.

According to credit bureau reports, roughly one in four U.S. consumers has a credit score above 800. That group consistently receives the best pricing and easiest approvals.

The remaining 75% fall below that threshold, even though many are financially stable and actively borrowing.

Age plays a visible role here. Older consumers tend to have higher scores, often averaging around 760.

Gen Z borrowers, by contrast, commonly sit closer to the high-600s. This gap reflects credit history length, not repayment intent.

As a result, traditional models systematically favor maturity over momentum. They capture long-term repayment patterns well, but they struggle to reflect recent behavioral shifts.

For risk teams, this creates a familiar constraint. Growth has to happen inside narrow boundaries defined by data that everyone else also uses.

Expanding approval rates without changing the risk profile becomes difficult. So does reaching younger or thin-file segments without increasing exposure.

Traditional credit data still anchors decisions. It just no longer sets leaders apart.

.svg)

.webp)

The hidden cost of conservative credit and risk management

Conservative risk controls reduce losses. They also introduce less visible costs.

Every additional rule in fraud prevention or onboarding improves security at the margin. At the same time, it reduces throughput. The tradeoff is not moral, but economical.

False declines are one of the clearest examples.

When a legitimate borrower is rejected, the immediate loss is a single transaction. The larger impact appears later – in lower conversion rates, higher acquisition costs, and slower portfolio growth.

Digital-first borrowers rarely retry after a rejection. They continue their search elsewhere, often within minutes. From a business perspective, this makes each false decline a lost acquisition, not a delayed one.

Onboarding friction compounds this effect. Longer verification flows and manual checks increase certainty, but they also increase abandonment.

Research shows that 68% of consumers have abandoned digital banking applications mid-onboarding because the process felt too long or too complex.

This creates a measurable efficiency problem. Marketing and acquisition spend still brings users into the funnel. Risk controls determine how many convert into funded accounts.

As friction increases, cost per booked loan rises, even if lead volume stays constant. The longer-term impact is harder to track, but more expensive.

Borrowers who exit early do not generate repeated loans or referrals. Lifetime value assumptions compress, even when default rates remain stable.

From the outside, the portfolio looks well controlled. From a growth perspective, capital is often underutilized.

This is why many risk teams reassess conservatism as portfolios scale.

The question shifts from whether a credit scoring platform reduces risk to whether it maximizes return on deployed capital, not just minimizes losses.

How alternative data improves credit risk analysis beyond bureau scores

When traditional credit data no longer differentiates outcomes, lenders look for additional signals.

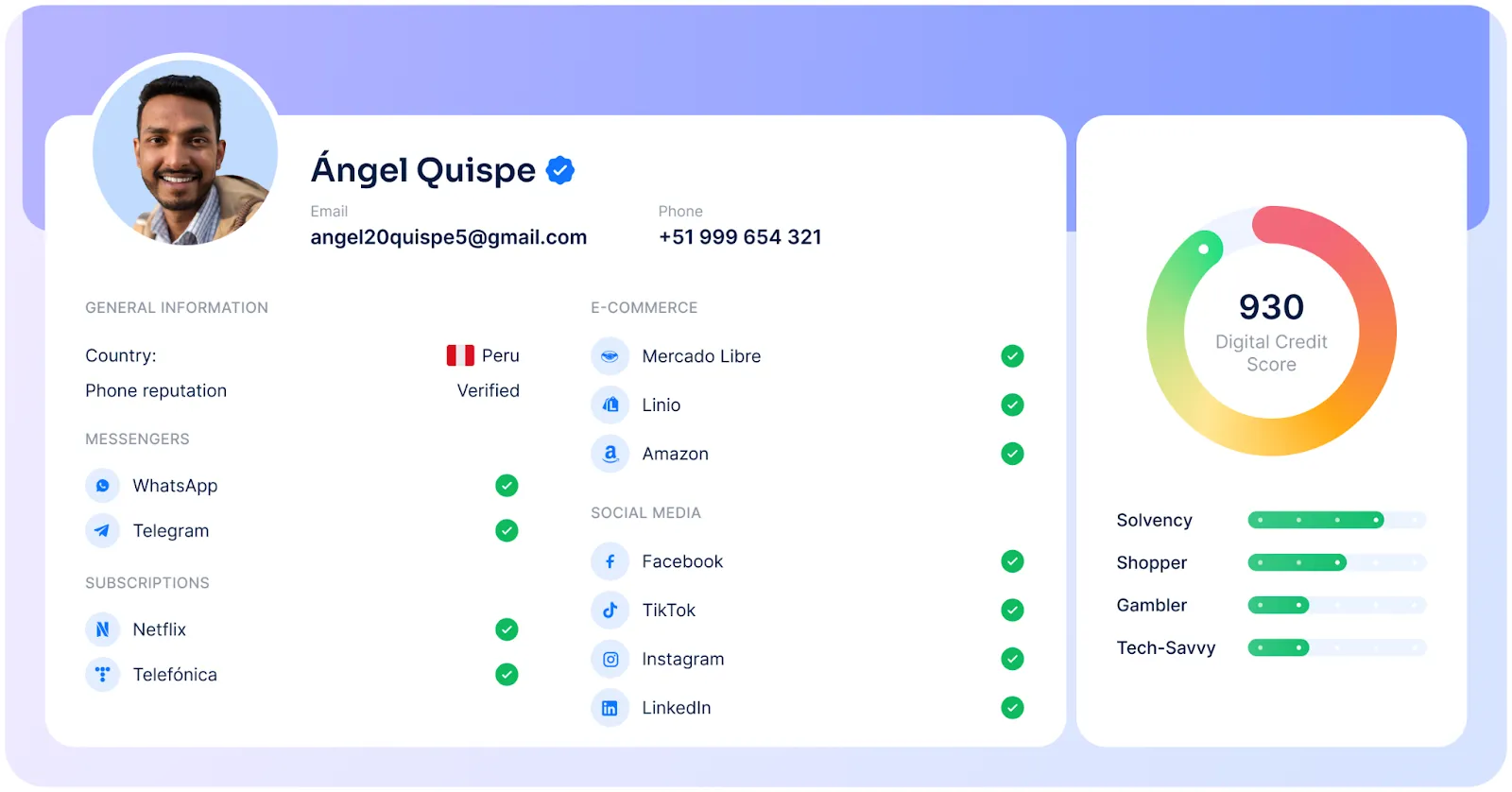

Alternative data extends risk analysis beyond repayment history. It adds context around intent, stability, and current digital behavior – factors that standard bureau files are not designed to capture.

These signals are not abstract. They are observable and predictive.

For example, email characteristics often reflect long-term digital presence. An account that has existed for ten years suggests continuity and investment in identity. A recently created address points to a very different risk profile.

At RiskSeal, this analysis goes beyond email age or domain alone. We map registrations and activity linked to an email address across platforms.

An email connected primarily to short-lived lending or gambling services behaves differently from one tied to Hulu, Spotify, GitHub, and region-dominant apps like Rappi in Colombia.

Phone number validation adds another layer. It helps distinguish established users from synthetic or rapidly recycled identities. IP and location patterns can surface anomalies early without introducing extra steps for the borrower.

Subscription presence and eCommerce activity further indicate participation in the digital economy. These behaviors reflect financial engagement that may not yet appear in a credit file.

Taken together, alternative signals allow lenders to assess risk with more nuance and timeliness.

These signals are explainable, auditable, and designed to complement bureau data rather than replace it. This allows risk teams to expand visibility without stepping outside established regulatory frameworks.

Because these inputs update continuously, they support earlier detection of risk changes. This allows teams to act on emerging patterns rather than waiting for bureau data to catch up.

In practice, this is how alternative data providers for credit decisions enrich traditional scoring by expanding visibility without removing discipline.

The business impact of modern credit risk management techniques

When risk assessment improves, everything accelerates. Better data doesn't just prevent losses. It unlocks growth opportunities that transform your entire business model.

Higher conversion through real-time risk decisions

Fewer false declines mean you validate identity and intent in seconds. Good applicants get a smooth experience. Bad actors get stopped fast. This is where you win customers.

In RiskSeal’s internal datasets, expanding real-time behavioral context has, in some cases, led to approval rate increases of up to two times without compromising risk criteria.

The math is straightforward. Every percentage point improvement in approval rates for creditworthy customers translates directly to revenue growth.

Better customer outcomes through faster decisions with lower friction

Lower onboarding friction increases completion. Fewer manual reviews and document loops mean more applicants reach a decision.

Speed only matters if it applies broadly. Modern decisioning systems can generate a digital credit score in under five seconds while covering most applicants.

In Mexico, for example, RiskSeal’s alternative data makes roughly 83% of the population credit-visible, compared to about 49% visible to credit bureaus.

That combination – speed plus coverage – creates practical separation that is hard to replicate.

Stronger credit portfolios through modern credit risk modeling

Stronger portfolios come from better risk visibility, not higher risk tolerance.

When models use more current and granular signals, risk classification improves at decision time. In practice, our data shows default rate reductions of up to 25%, driven by accuracy gains rather than stricter approvals.

Lower defaults improve unit economics and make growth more predictable at scale.

If approached correctly, AI credit risk assessment can turn risk into a strategic partner instead of the department that says no. This will help the whole business move faster.

How different lenders shape credit risk requirements

Different lending models face different constraints. But they share the same problem: traditional data doesn't update fast enough.

BNPL providers operate at the point of impulse. When a customer is ready to buy, even small delays or false declines can end the transaction. Approval decisions need to happen in seconds, not minutes, or the sale is lost.

Neobanks compete on experience. When your brand promise is seamless digital banking, you can't ask customers to mail in documents. The account opening experience is the product.

Microfinance lenders serve underbanked and thin-file populations. Bureau scores can't assess someone who's never had a credit card.

These lenders need alternative signals or they can't serve their market at all. Their entire business model depends on evaluating risk through non-traditional means.

Each model has different risk appetites and margin structures. But all benefit from richer signals and faster decisioning.

Speed without accuracy is reckless. Accuracy without speed loses customers. You need both.

How RiskSeal turns risk assessment into your competitive edge

RiskSeal strengthens credit decisioning where traditional data stops working. The competitive advantage comes from how risk teams see more applicants, more clearly, and earlier in the decision flow.

Alternative data where bureau signals thin out

When credit files are limited or slow to update, alternative data adds predictive context.

It captures intent, stability, and digital behavior that do not appear in bureau reports, especially for thin-file and emerging segments.

High coverage with local, region-specific signals

Coverage is a core differentiator. RiskSeal provides high-coverage alternative data built on region-specific digital behavior.

This allows lenders to assess a much larger share of applicants using signals that global bureaus and generic vendors do not capture.

The result is broader visibility without relying on proxy assumptions or blanket rules.

Secure and compliant by design

RiskSeal’s data sourcing is transparent and GDPR-aligned, supported by clear documentation, strict security controls, and ISO 27001 certification.

This makes adoption viable in regulated environments, including the EU, without introducing compliance risk.

Measurable impact on portfolio performance

When integrated into existing risk models, these signals improve segmentation even in portfolios that already appear “fully optimized.”

In practice, lenders observe:

- lower default rates

- higher approval rates for creditworthy applicants

- and measurable uplift in model performance metrics like Gini.

These improvements occur without expanding risk tolerance, driven instead by better classification at decision time.

A data enrichment layer in the risk stack

Architecturally, RiskSeal acts as a data enrichment layer. It complements bureau data and internal models by adding signals that are difficult to replicate without deep regional investment.

This layer strengthens decisions upstream, improves portfolio outcomes downstream, and becomes a durable source of competitive separation.

Smarter credit risk decisions win market share

Credit risk done right isn't just about avoiding losses.

It's about capturing opportunities your competitors miss and building trust that keeps customers coming back. And it's about turning defense into offense.

The lenders winning market share today aren't the ones playing it safest. They're the ones making smarter decisions faster.

FAQ

Which fintechs have the most accurate credit risk assessment models?

The fintechs with the most accurate credit risk models are defined by how they build decisions, not by brand.

They combine traditional credit data with alternative signals, such as real-time digital behavior, to improve risk visibility beyond what bureau data alone can provide.

This approach is particularly effective in segments where bureau coverage is limited or slow to update, including younger borrowers, informal workers, and customers new to formal credit.

In practice, model accuracy improves when decisions reflect current borrower behavior rather than additional rules applied to the same static data.

How to manage credit risk?

To manage credit risk, start by establishing clear visibility into approvals, pricing, and early performance signals.

Use a mix of data sources to assess applicants and track portfolio behavior continuously, so policies can be adjusted based on observed outcomes rather than static assumptions.

Effective credit risk management also links decisioning to business objectives.

Risk parameters, product design, and growth targets are evaluated together. This allows teams to expand responsibly while keeping losses predictable.

Why is credit risk management important?

Credit risk management directly determines a lender’s ability to scale. Poor risk control leads to losses, but overly conservative risk management limits approvals, damages conversion, and slows growth.

Strong credit risk management protects margins, improves capital efficiency, and builds resilience during market shifts. It also enables lenders to serve broader segments, including thin-file customers and informal workers, without increasing default rates.

In competitive markets, credit risk management is no longer just about loss prevention. It’s a strategic lever for growth and differentiation.

What are the best practices for managing credit risk?

The best practices for managing credit risk include:

- Using diverse data sources. Combine bureau data with additional signals to reduce blind spots and improve visibility across borrower segments.

- Relying on real-time signals. Base decisions on current behavior rather than delayed or infrequently updated snapshots.

- Validating models continuously. Monitor portfolio outcomes and refine models based on actual performance, not static assumptions.

- Tracking false declines alongside defaults. Measure missed creditworthy borrowers as a cost, not just losses from bad approvals.

- Aligning risk with business goals. Embed risk thinking across product, growth, and operations so decisions support both portfolio health and customer experience.

Applied consistently, these practices improve risk visibility and decision quality across the credit lifecycle.

What are the most effective credit risk management strategies?

The most effective credit risk management strategies focus on segmentation, speed, and adaptability.

Rather than relying on one-size-fits-all rules, high-performing lenders build flexible decisioning frameworks that evolve with borrower behavior and market conditions.

Key strategies include:

- Borrower segmentation. Group borrowers based on behavior, context, and risk drivers, then apply differentiated decisioning instead of blanket policies.

- Alternative data integration. Use alternative data providers to improve visibility where bureau data is thin, outdated, or non-differentiating.

- Real-time risk assessment. Act on current signals during onboarding and across the lifecycle to catch emerging risk early and approve good customers faster.

- Continuous model optimization. Monitor performance and recalibrate models based on outcomes, not assumptions, as behavior and markets change.

- Portfolio-level feedback loops. Use collections and repayment data to refine upstream risk decisions and reduce long-term losses.

Over time, these strategies lead to stronger portfolios, better collections performance, and lower operational costs without slowing growth.

How do banks manage credit risk?

Banks typically manage credit risk through layered controls:

- bureau-based scoring

- policy rules

- manual reviews

- portfolio monitoring

This structure prioritizes stability and regulatory compliance, but often moves slowly.

To improve performance, many banks are now complementing traditional processes with alternative data and automated decisioning. This helps them compete with fintechs on speed and inclusion while maintaining governance standards.

The banks that adapt fastest are those that modernize risk decisioning without compromising control, using better data to make more precise decisions at scale.

See more

Compare RiskSeal and SEON digital scoring systems and choose the best option for your business goals.

.webp)

Discover the top alternative credit scoring platforms that leverage alternative data for credit assessments.

.webp)

Discover 25 leading alternative data providers helping lenders improve credit decisions, detect fraud, and serve borrowers beyond traditional scoring.