Top-10 Alternative Credit Scoring Platforms

Discover the top alternative credit scoring platforms that leverage alternative data for credit assessments.

.webp)

We analyzed 6.1 million loan applications

The results show how digital credit scores correlate with default risk.

The traditional approach to assessing the creditworthiness of borrowers is no longer meeting the expectations of financial institutions.

According to Experian, 60 percent of them say they have to reject a significant proportion of loan applications due to insufficient data.

To solve the problem, lenders should turn to alternative data for credit scoring.

This article showcases some of the best credit knowledge tools from fintech startups. These help credit providers gain a clearer customer view and identify better opportunities.

Best alternative credit scoring startups: selection criteria

Here are the ten best digital credit scoring solutions that can improve the efficiency of credit assessment.

When selecting the best fintech tools for understanding credit, we focused on platforms that:

- Are specifically designed for the credit industry

- Integrate alternative data sources

- Offer a ready-to-use credit score

Through an in-depth analysis of the software market, we compiled a list of the top alternative credit scoring companies:

- RiskSeal

- Trusting Social

- CreditVidya

- Mobile Lending

- PayCrunch

- Creamfinance

- HomeCrowd

- Pulse API

- Mujeres WOW

- Juvo

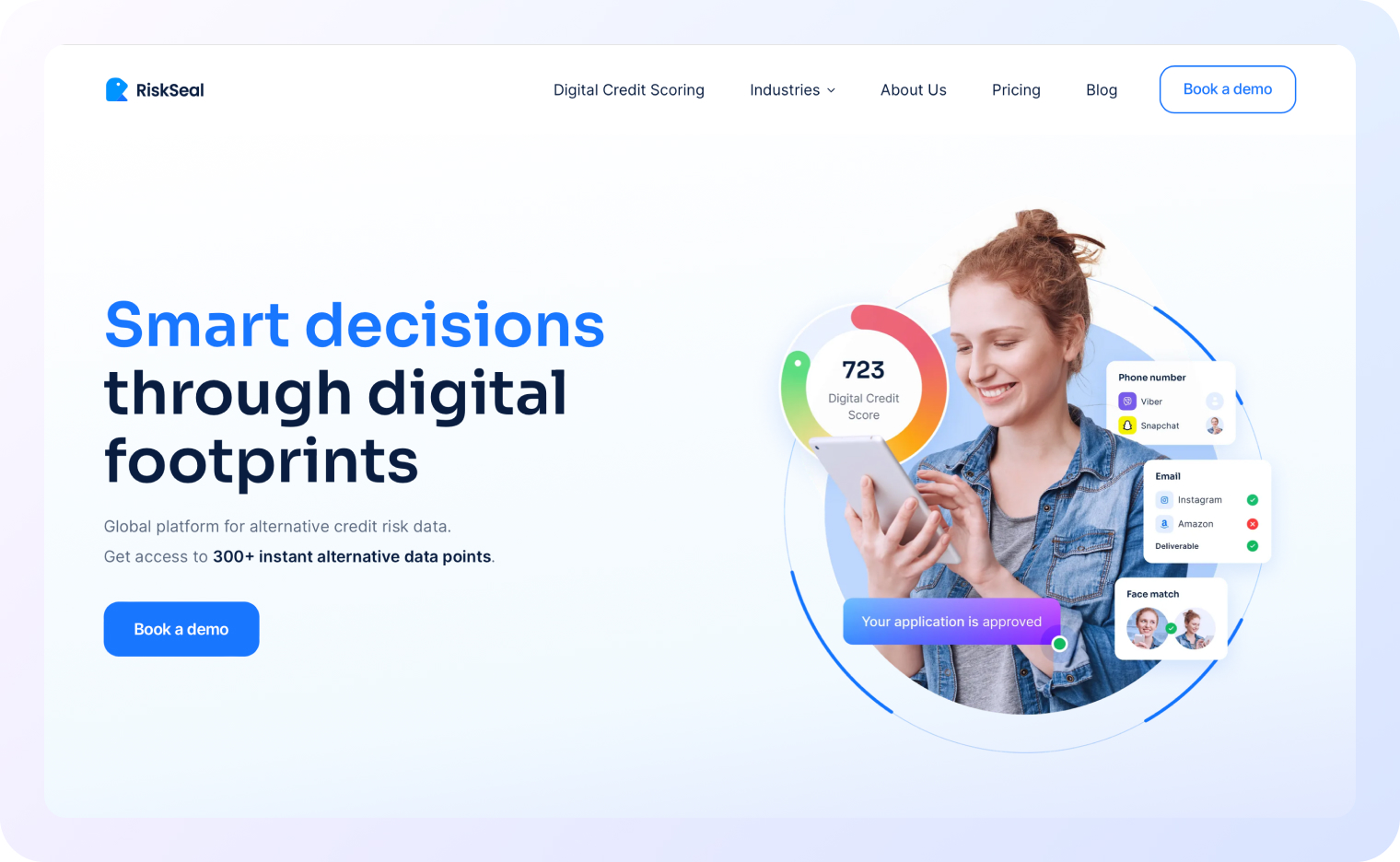

#1. RiskSeal – alternative credit scoring platform

RiskSeal helps financial institutions improve credit decisions with alternative data for lenders that traditional bureaus aren’t meant to capture.

Data sources: RiskSeal focuses on unique digital footprint signals, including:

- email and phone intelligence

- online registrations

- social media presence

- app activity

- premium subscriptions

- IP and location insights

- local platform data across multiple markets

These signals add fresh, non-overlapping context to a borrower profile.

Scoring approach: The platform enriches existing credit models with 400+ of predictive data points per applicant.

Instead of replacing a lender’s scorecard, RiskSeal adds an extra data layer that helps risk teams improve segmentation, detect fraud, and assess thin-file or first-time borrowers more accurately.

Primary use case: RiskSeal is well-suited for banks, online lenders, BNPL providers, fintechs, and consumer credit companies working in markets where bureau coverage is weak or incomplete.

It helps lenders reduce defaults, increase approval rates, improve Gini, and support better collections and recovery.

Key differentiator: RiskSeal’s main advantage is access to region-specific digital signals that other vendors often do not provide.

It can be integrated quickly, works with existing decision engines, and delivers strong model uplift at a competitive cost.

Founded: 2022

Country: USA and Poland

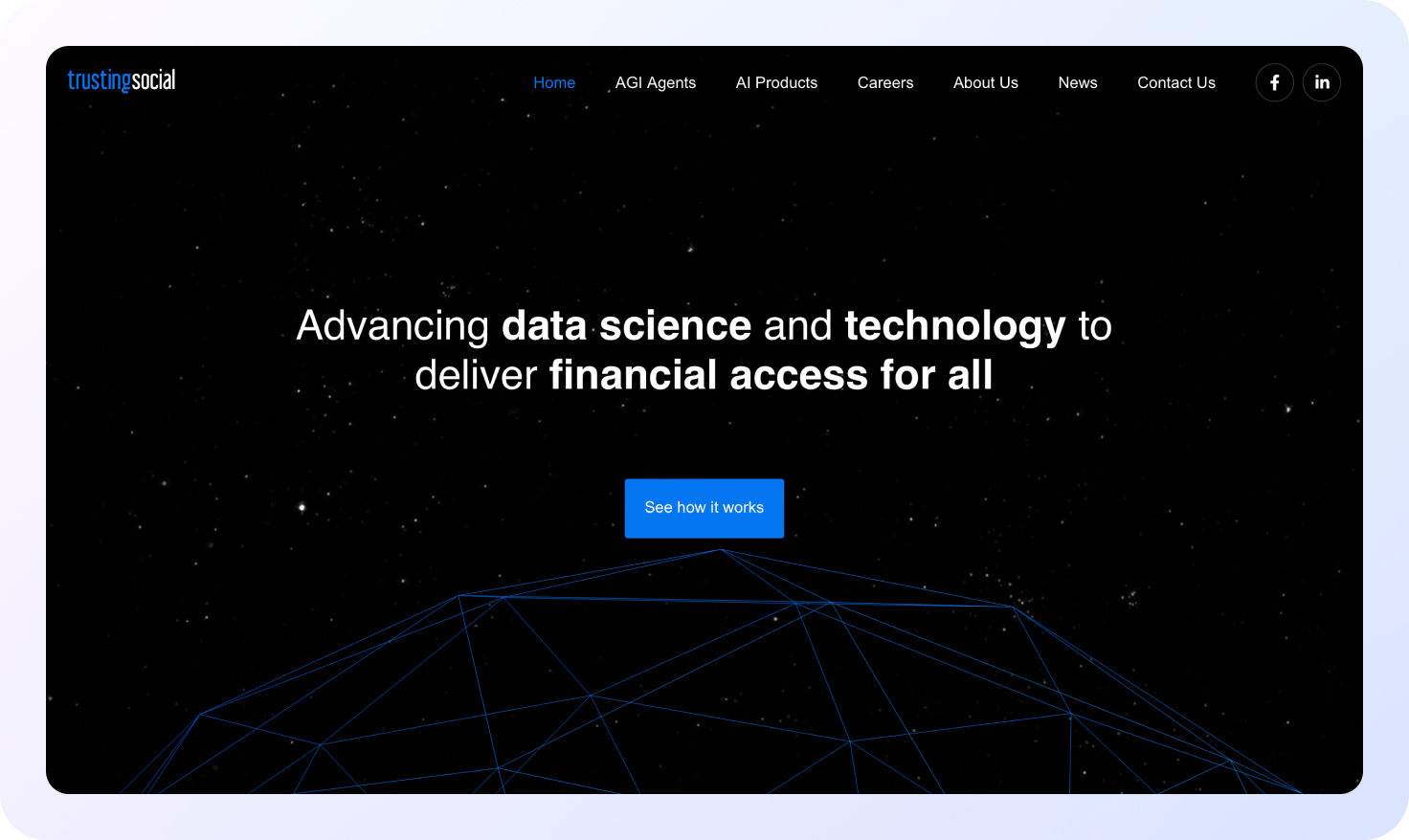

#2. Trusting Social – alternative data credit scoring tool

Trusting Social is an AI-based platform built for alternative data credit scoring.

Data sources: The platform draws on telecom data as its primary source. This includes mobile usage patterns, top-up behavior, and network activity.

It also pulls in behavioral data signals that telecom operators collect from their subscriber base, as well as public social media activity.

Scoring approach: Trusting Social uses Machine Learning and Big Data processing to turn raw telecom signals into credit scores. The algorithms identify patterns in how people use their phones and translate them into risk indicators.

This approach allows the platform to assess millions of unbanked users who have a mobile subscription but no banking relationship.

Primary use case: The solution is best suited for consumer lending in emerging markets, particularly in Southeast Asia.

Key differentiator: Trusting Social's edge is its deep integration with mobile network operators. Rather than scraping public data, it works directly with telcos to access rich, first-party behavioral data at scale.

Founded: 2013

Country: USA

#3. CreditVidya – solution for credit scoring and risk assessment

CreditVidya is a digital credit scoring solution focused on improving financial inclusion.

Data sources: The platform uses a broad mix of alternative data. This includes mobile device metadata, app usage data, SMS transaction records, and location signals.

CreditVidya also analyzes psychometric data and patterns from smartphone usage to build borrower profiles.

Scoring approach: CreditVidya processes these non-traditional inputs through machine learning models to produce a credit score. It looks for behavioral consistency, financial activity patterns, and lifestyle signals that correlate with creditworthiness.

The platform is designed to provide a score even to applicants with no bureau history to rely on.

Primary use case: CreditVidya is built for consumer and MSME lending in India. It serves lenders who need to evaluate first-time borrowers, gig economy workers, or small business owners who fall outside the traditional banking system.

Key differentiator: Its focus on the Indian market and deep use of smartphone-derived data makes it highly relevant for one of the world's largest underbanked populations.

Founded: 2013

Country: India

.svg)

.webp)

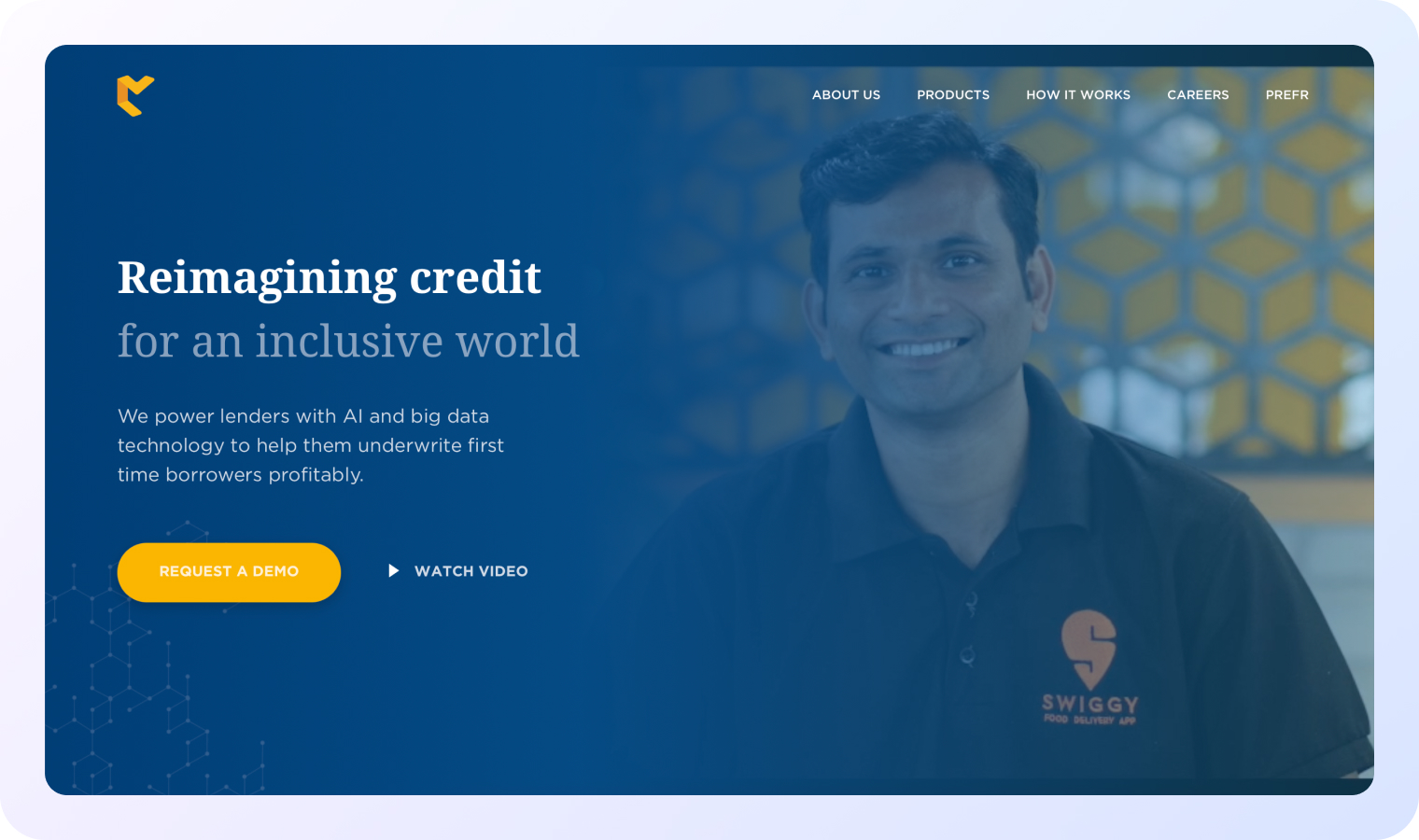

#4. Mobile Lending – alternative credit scoring startup

Mobile Lending is a fintech company specializing in credit assessment for emerging markets.

Data sources: The platform relies on mobile device usage patterns and transaction history as its main data inputs. It captures how often a device is used, what types of transactions are made, airtime purchase frequency, and mobile money activity.

Scoring approach: Mobile Lending's models analyze these behavioral signals to produce a creditworthiness score.

The platform looks at consistency and regularity in mobile financial behavior to predict repayment likelihood. It can generate scores quickly, making it practical for high-volume consumer lending environments.

Primary use case: It is best suited for short-term consumer loans and microfinance in emerging markets, particularly in Africa. The solution helps lenders reach borrowers who rely on mobile money rather than bank accounts.

Key differentiator: Mobile Lending takes a mobile-first approach to credit scoring. Unlike platforms that use mobile data as one signal among many, it is built entirely around mobile behavior as the core scoring input.

Founded: 2018

Country: Netherlands

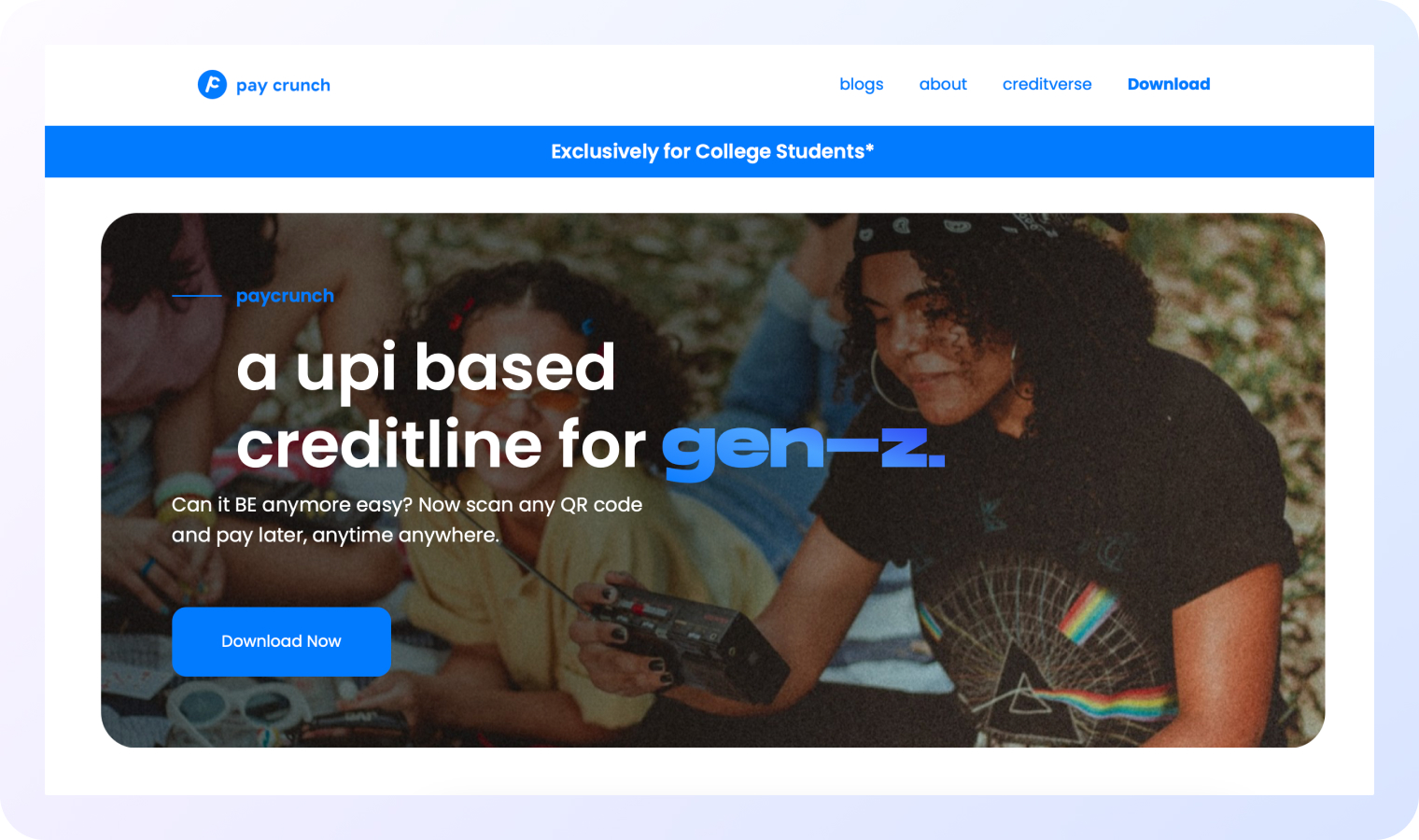

#5. Paycrunch – alternative credit scoring system

PayCrunch is an alternative data provider that delivers a complete credit scoring system, not just raw inputs.

Data sources: The platform uses behavioral data and transaction history. It looks at spending patterns, payment regularity, purchase categories, and how users interact with financial products over time.

Scoring approach: PayCrunch builds borrower profiles from patterns of behavior rather than point-in-time financial snapshots. It evaluates how consistent a user's financial habits are and how those habits evolve.

The system is designed to detect creditworthiness signals that traditional bureau data often misses in younger consumers.

Primary use case: PayCrunch focuses specifically on Gen Z consumers. It is well-suited for lenders offering credit cards, personal loans, and BNPL products to younger borrowers who have little to no credit history.

Key differentiator: Its Gen Z specialization is what sets PayCrunch apart. The platform is designed from the ground up for a demographic that conventional scoring models consistently underserve.

Founded: 2020

Country: India

#6. Creamfinance – alternative credit scoring company

Creamfinance is a fintech company that provides both credit scoring and a range of personal lending services.

Data sources: The platform uses a data-driven approach that combines traditional credit bureau data with alternative sources.

This includes behavioral data, open banking signals, and digital activity patterns pulled from online interactions.

Scoring approach: Creamfinance applies advanced algorithms to blend traditional and alternative data into a single creditworthiness assessment. Its models evaluate risk dynamically, adapting to new data as it comes in.

The platform also manages ongoing risk monitoring, not just point-of-application scoring.

Primary use case: Creamfinance is built for personal lending, particularly short-term and installment loans. It serves both direct lending operations and other credit providers looking to improve underwriting accuracy.

Key differentiator: Creamfinance is unique on this list because it operates as both a lender and a technology provider. This dual role gives it real-world feedback loops that pure technology platforms don't have.

Founded: 2012

Country: Poland

#7. Homecrowd – credit scoring platform for mortgage lending

HomeCrowd is an alternative credit scoring platform built specifically for mortgage lending.

Data sources: The platform uses non-traditional data sources including utility payment history, rental payment records, and social media activity.

These inputs help build a credit picture for borrowers who may not have a mortgage-qualifying credit score through conventional channels.

Scoring approach: HomeCrowd's models analyze payment consistency across utilities and rent, treating these as proxies for financial responsibility. Social signals add an additional layer of context.

The platform translates these inputs into a score that lenders can use to make home lending decisions for borrowers who would otherwise be turned away.

Primary use case: HomeCrowd targets unbanked and underbanked individuals seeking home mortgages. It is designed for markets where large portions of the population rent or pay utilities but have no formal credit history.

Key differentiator: HomeCrowd is the only platform on this list focused exclusively on mortgage lending for underserved populations. That vertical specialization makes it a purpose-built tool rather than a general-purpose scoring system.

Founded: 2019

Country: Malaysia

#8. Pulse API – solution for predicting borrower income

Pulse API takes a targeted approach to credit risk: it focuses on predicting income rather than scoring overall creditworthiness.

Data sources: The platform analyzes employment data including job type, industry, company size, and seniority level. It also incorporates professional network data and career trajectory signals to estimate earning potential.

Scoring approach: Rather than producing a traditional credit score, Pulse API generates an income prediction. It models what a borrower is likely to earn based on their professional profile.

Lenders can then use this as an input alongside other signals to make more accurate affordability decisions.

Primary use case: Pulse API is best suited for lenders that need income verification or estimation as part of their underwriting process.

It works well for personal loans, auto financing, and any product where debt-to-income ratio is a key decision factor.

Key differentiator: Income prediction is Pulse API's sole focus. No other platform on this list takes this approach. It fills a specific gap in the underwriting process rather than trying to replace the full credit scoring workflow.

Founded: 2019

Country: USA

#9. Mujeres Wow – alternative credit scoring platform for women

.jpeg)

Mujeres WOW is an AI-based platform with a clear mission: improving credit access for women.

Data sources: The platform builds credit profiles using non-traditional data specifically relevant to women's financial lives. This includes social data, community participation signals, and peer ratings.

Women on the platform can rate each other based on social role and trustworthiness, creating a community-driven data layer.

Scoring approach: Mujeres WOW combines AI-driven data analysis with peer reputation signals to build a creditworthiness score.

The system weights community trust indicators alongside behavioral and financial data. This makes it effective in contexts where women have limited formal financial histories but strong community ties.

Primary use case: The solution is designed for women in Latin America who are excluded from traditional credit markets. It is particularly relevant for microfinance lenders, credit unions, and social impact investors.

Key differentiator: Mujeres WOW is the only platform on this list built around a community-driven scoring model. The peer rating system is unique and reflects an understanding that social capital is a real and measurable financial asset.

Founded: 2019

Country: Mexico

#10. Juvo – alternative credit scoring tool

Juvo builds credit scores for people who have a mobile phone but no credit history.

Data sources: Juvo's primary data source is mobile usage behavior. It collects signals from how subscribers use their mobile service.

Signals include airtime purchases, data top-ups, call frequency, and usage consistency. This data flows in through direct partnerships with mobile network operators.

Scoring approach: Juvo analyzes these usage patterns over time to build a credit identity for each subscriber.

The platform looks at behavioral regularity and financial discipline as expressed through mobile activity. Scores improve as users engage more consistently, creating a dynamic credit profile that grows with the borrower.

Primary use case: Juvo is best suited for prepaid mobile subscribers in emerging markets who want access to credit for the first time. Its model works well for microloans, airtime credit, and entry-level financial products.

Key differentiator: Juvo's direct partnerships with mobile operators give it access to data that other platforms simply cannot replicate.

It is not analyzing publicly available signals, but working with raw operator data from inside the network.

Founded: 2014

Country: USA

Alternative credit scoring platforms comparison

Choosing the right alternative credit scoring platform depends on your market, your borrowers, and what data you actually have access to.

The ten platforms above cover a wide range of approaches, from digital footprint analysis to income prediction to community-driven scoring. Here is a summary of the key differences.

Each platform targets a different piece of the credit gap.

Some, like RiskSeal and Trusting Social, work broadly across geographies and borrower types. Others, like Mujeres WOW and HomeCrowd, solve a very specific problem for a very specific audience.

The best choice depends on whether you need a comprehensive scoring layer or a focused tool that fills one gap in your underwriting process.

Benefits of adopting alternative credit scoring platforms

Alternative-data scoring platforms are emerging as some of the best fintech solutions for credit score management. They provide major benefits to lenders:

Expanded credit access and inclusion

Low financial inclusion is a critical issue around the world. In the U.S. alone, 19% of the population has no access to credit, being invisible or unscorable:

Pro tip: At RiskSeal, we tackle this challenge by leveraging alternative data sources for credit scoring. Our platform enables analysis on 98% of the global population, offering our clients access to over 300 data points for every applicant.

Enhanced prediction accuracy and risk management

Traditional credit scoring systems rely on historical financial data of the applicant. Due to their insufficiency and irrelevance, it can be difficult for lenders to make an objective credit decision.

Pro tip: Using RiskSeal, our clients significantly improve the predictive power of the scoring model through alternative data. Even without any credit bureau records, the best credit decision software can achieve an AUC of 83%.

Cost savings through automation and digital assessments

According to research, KYC verification of one customer can cost a financial organization from $1,500 to $3,000.

Pro tip: RiskSeal's alternative credit scoring saves from unnecessary costs. Only at the initial stage of borrower verification, our solution cuts off up to 70% of borrowers with clear signs of fraud or a high probability of default.

Another advantage of using RiskSeal is the full automation of the credit scoring process. With us, you will noticeably improve your customers' user experience. After all, we provide an answer on a credit application within 5 seconds.

We analyzed 6.1 million loan applications

The results show how digital credit scores correlate with default risk.

FAQ

What is an alternative credit scoring platform?

Alternative credit scoring platform is a digital solution for assessing a borrower's creditworthiness based on alternative data. Unlike traditional credit scoring systems, they are not limited to credit scores but rely on a wider range of information. They are often based on advanced technologies such as machine learning and artificial intelligence.

How does RiskSeal improve credit scoring with alternative data?

RiskSeal enriches its clients' scoring models with a large set of alternative data. The platform obtains this data by analyzing the digital footprint of potential borrowers left on 200+ local and global online resources.

What are the main benefits of adopting an alternative credit scoring platform?

The main benefits of adopting an alternative credit scoring platform include expanded credit access, enhanced prediction accuracy, and cost savings. These platforms can also improve the user experience by automating credit scoring and speeding up application decisions.

What are the best platforms for alternative credit scoring?

There is no single “best” platform for every lender.

The right choice depends on your organization’s needs. Including the markets you operate in, the level of risk you’re comfortable with, and the budget and resources available.

Some lenders prioritize depth of alternative data, while others focus more on ease of integration or specific use cases like fraud detection or thin-file scoring.

At RiskSeal, we design our scoring system to meet strict requirements for accuracy, transparency, and coverage. That way, we support a wide range of credit providers, especially those operating in emerging markets.

What is the best credit score API for fintech applications?

The best credit score API depends on several technical factors:

- the quality and freshness of data it provides

- how quickly it can process and return results

- the reliability of the underlying scoring logic

- how easy it is to integrate into an existing tech stack

Strong documentation and responsive support also matter, since interpreting alternative data and model outputs requires more than just an API call.

RiskSeal focuses on all of these areas, from data quality and real-time performance to developer-friendly integration. That’s how we help fintechs build accurate, scalable credit workflows.

See more

The press release about RiskSeal and CLIX partnership to support consumer credit marketplaces with alternative data intelligence and deeper borrower insights.

Discover the top-10 APIs bringing predictive power to credit scoring through alternative data.

Discover why Research.com ranks RiskSeal’s digital scoring platform among the top accounts receivable solutions for lenders.