Back to Glossary

Credit Scoring

Discover what credit scoring is and how alternative data helps lenders assess risk more accurately.

Discover what credit scoring is and how alternative data helps lenders assess risk more accurately.

Every lending institution works with credit scoring daily.

This process is at the core of evaluating a borrower’s profile and deciding whether to approve a loan, set terms, or reject an application.

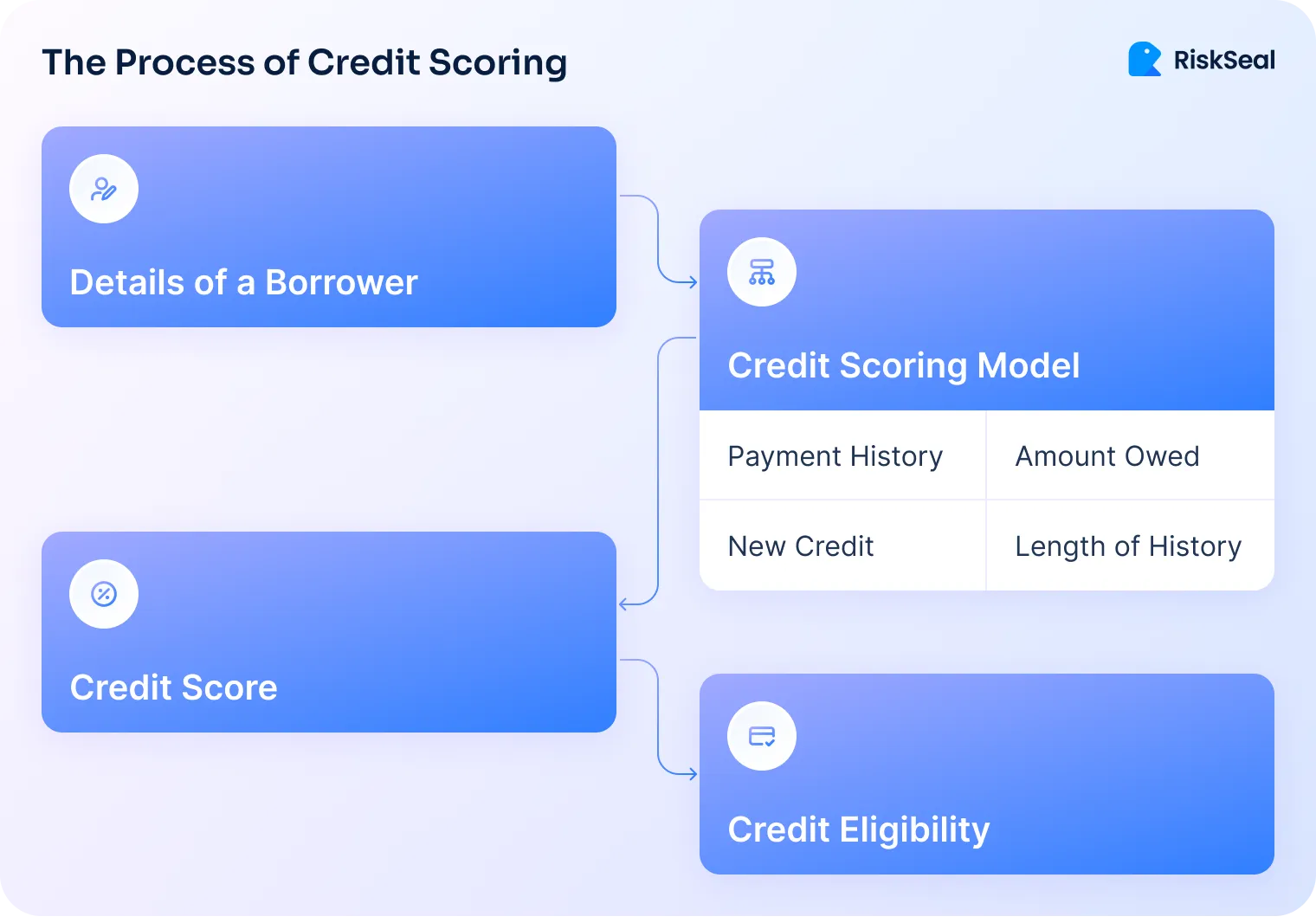

Credit scoring is a statistical analysis used by lenders to evaluate the risk of lending money to a borrower.

It estimates how likely a person or business is to repay debt on time.

These scores guide decisions such as:

Credit scoring plays a key role in modern lending infrastructure.

Credit scoring in neobanks and other financial institutions helps risk teams manage credit risk more efficiently. It also scales decision-making across large applicant volumes.

Core functions of credit scoring include:

Well-designed credit scoring reduces default-related losses and drives more profitable lending decisions.

Credit score is a number that shows how likely a borrower is to repay a loan. It combines different signals into a single risk score. That score also helps lenders make fast, consistent credit decisions.

Each data point is assigned a weight based on its risk impact. To understand credit score meaning, know that it calculates scores using rules, statistics, or machine learning.

Higher scores usually mean lower risk. Lenders set thresholds to approve, decline, or review applications.

Common scoring signals include:

While these models provide structured and repeatable outcomes, they still leave important gaps.

Especially when evaluating borrowers with limited credit histories or non-traditional financial behavior.

Alternative credit scoring is the use of non-traditional data to evaluate a borrower's creditworthiness. It’s useful when traditional credit history is missing or limited.

Alternative data helps fill risk gaps. It provides real-time insights into a person’s digital identity, behavior, and financial habits. These signals allow lenders to evaluate borrowers who might otherwise be invisible to traditional scoring models.

The table below shows examples of signals used by top alternative credit scoring platforms and what they reveal to lenders:

Advanced systems also use AI and biometric signals. These include facial recognition and device-based identity matching. They help detect fraud, verify identity, and improve scoring accuracy early in the onboarding process.

Credit scoring is essential to managing risk. But when it comes to traditional vs. alternative credit scoring, the difference matters.

Traditional models work well but often miss key signals. Especially for thin-file or credit-invisible applicants. Modern systems fill these gaps by using alternative data, AI, and biometric checks.

Want to strengthen your scoring process? Reach out to the RiskSeal team to see how enriched data can help.