Credit Scoring in Neobanks: Features, Challenges, Solutions

Dive into why traditional credit scoring fails neobanks and explore smarter, data-driven solutions for assessing credit risk.

.webp)

The financial services landscape is changing at an astonishing speed. Just yesterday, opening an account or applying for a loan required a visit to a physical bank branch.

Today, the situation has changed. Traditional banking organizations are being gradually replaced by a new format of institutions – digital neobank.

What are they? What are the features of their operations and what challenges do they face in the lending process? Read about this and more in our article.

Why traditional credit scoring fails neobanks

Let's first break down - what is a neobank?

It is a financial institution that provides its services (including lending) exclusively online.

This means that its clients do not have the option to visit the physical offices of the company. They simply do not exist.

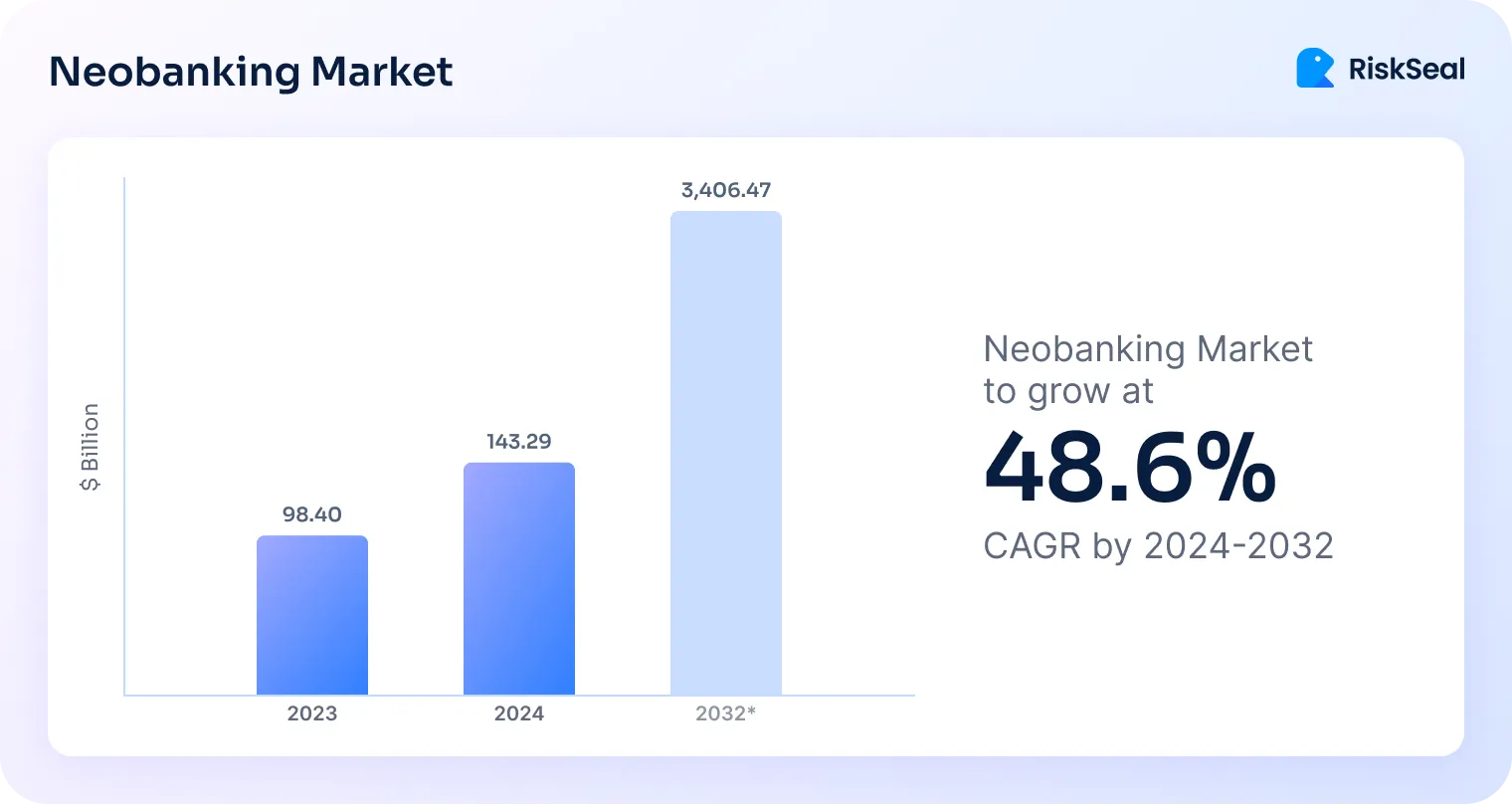

The popularity of such organizations is rapidly growing.

If in 2024, the global neobanks market was valued at $143 billion, by 2032, it is expected to grow to $3,406 billion.

To meet the needs of a constantly growing target audience while maintaining the quality of their credit portfolio, neobanks cannot rely solely on the capabilities of traditional credit scoring.

Here are the main reasons why:

1. Limited data from credit bureaus. Credit decisioning based on historical financial data about the applicant is imperfect.

This approach is slow, unclear, and unsuitable for thin-file users. These applicants either have no credit history or their history is limited.

2. Insufficient flexibility. Traditional credit scoring cannot adapt to market changes and new fraudulent schemes.

For example, traditional banks do not issue loans to individuals without official employment. Today, more and more people work for themselves as freelancers.

According to statistics, this form of employment is typical for more than 46% of workers:

At the same time, research results show that 44% of freelancers earn more than officially employed individuals.

Neobanks lose a significant portion of financially capable clients in their face.

The same applies to fraudsters.

They are constantly looking for new ways to deceive, and traditional scoring systems are not fully capable of detecting them.

3. Limited application processing capabilities. With traditional credit scoring, the review of a credit application can take several hours or even days.

Traditional scoring models struggle with large amounts of data. As a result, fewer clients are served, which limits the lender’s profits.

The unique credit scoring needs of neobanks

The implementation of digital credit scoring allows neobanks to meet their priorities when assessing the creditworthiness of potential borrowers.

The main needs include:

Risk assessment at scale

Neobanks need to assess thousands of users daily.

At the same time, they cannot afford to make decisions over hours – the result must be provided with minimal delay.

Maintaining default levels

While serving a large number of clients, neobanks must not forget about the quality of their credit portfolio.

This means they need a scoring system capable of processing more applications without increasing the risk of delays and defaults.

Effective fraud prevention

Accurate identity verification of applicants is another key need for neobanks.

They need to filter out synthetic identities and fraud rings in seconds.

Compliance with regulations and standards

Neobanks are strictly monitored by regulatory authorities.

They must meet KYC/AML, GDPR, and region-specific legal requirements.

Alternative data types useful for neobanks

Good results are shown by the use of alternative data credit risk solutions for neobanks. They allow the creation of a complete financial profile for applicants, including those with thin files.

Which types are the most informative?

Email data

An email address contains many useful insights for a lender.

For example, you can check when an email account was created. If it’s very new, it could be a sign of fraud - scammers often use temporary or fake email addresses.

It is also advisable to analyze email deliverability (email activity) and domain information (reputation, type – paid/free, etc.).

It’s important to check whether the email is listed in blacklists or other databases of high-risk subscribers.

Phone data

Analyzing the applicant’s phone number can also be useful for neobanks.

It helps identify red flags such as the use of burner phones, virtual SIM cards, or disposable numbers. These are common communication methods used by fraudsters.

It’s also possible to check if the operator code matches the residential address information from the application and determine whether the subscriber is listed in various blacklists.

Note: With the help of a data enrichment solution, it’s possible to verify whether accounts are registered to the phone number and email on various platforms.

If no accounts are found, the applicant should be assigned a high-risk level since this is uncommon in today’s digital world.

Location insights

The fact that all regions differ in their economic status cannot be ignored.

Unemployment, crime rates, income levels, etc., differ from country to country and even city to city.

The standard of living of the population directly impacts their ability to repay loans.

As a result, default rates can vary even within one country, for example, between rural areas and major cities.

Paid subscription data

Another type of alternative data that neobanks should consider is whether applicants have any paid subscriptions.

This fact alone speaks in favor of the borrower.

After all, a person who spends money on paid services is likely not suffering from a lack of finances.

It’s important to consider another aspect here: the regularity of payments. Any late payments could raise doubts about the applicant’s reliability.

E-commerce data

Credit scoring using digital footprints allows the analysis of how the borrower manages their finances online.

What products do they buy most frequently? What is their average monthly spending? How often do they make returns?

From this data, conclusions can be drawn about the person’s consumer habits.

This information can also suggest certain personality traits that may indicate a tendency to default. For example, impulsivity is reflected in nighttime purchases.

Social media activity

Social networks are some of the most informative sources of alternative data for credit risk assessment in neobanks.

They can provide information about the applicant’s geolocation, interests, education, and career (on platforms like LinkedIn).

It’s also possible to analyze the applicant's followers. After all, a person’s social circle can indirectly indicate their financial status.

.svg)

Machine learning models for neobanks

Machine learning-based assessment can adapt to changing market trends, which is crucial for neobanks.

For example, it responds to spikes in fraud, market downturns, and more.

In digital credit organizations, the following ML-based techniques are used:

Face recognition

Modern scoring systems (such as RiskSeal) can match applicant photos found on various online platforms.

If it is discovered that the photos show different people, the applicant will be assigned a high-risk level.

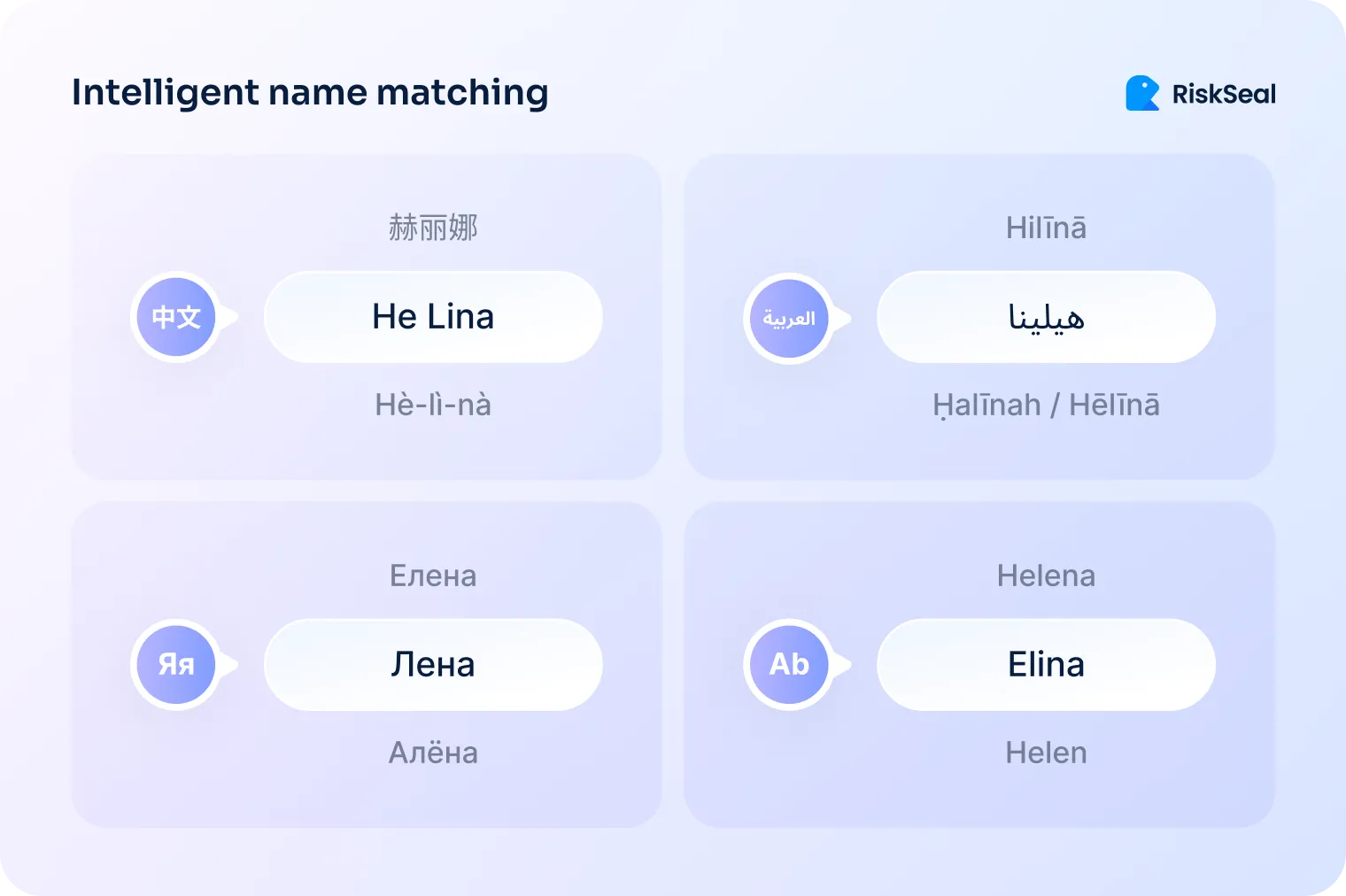

Name matching

The same comparison can be made for usernames. If different names are listed in multiple accounts, this will also raise suspicion of fraud.

The scoring system needs to account for different linguistic variations of the same name.

For example, RiskSeal recognizes the names Heléna (Hungarian), Elena (Spanish), and Hełine (Armenian) as the same name. This reduces the number of false positives.

Anomaly detection. ML algorithms help track patterns in user behavior and identify deviations from typical patterns.

For example, if someone usually spends a certain amount on online shopping each month, but suddenly makes several unusually expensive purchases, it could be a sign that their account has been taken over by fraudsters.

How can RiskSeal help neobanks?

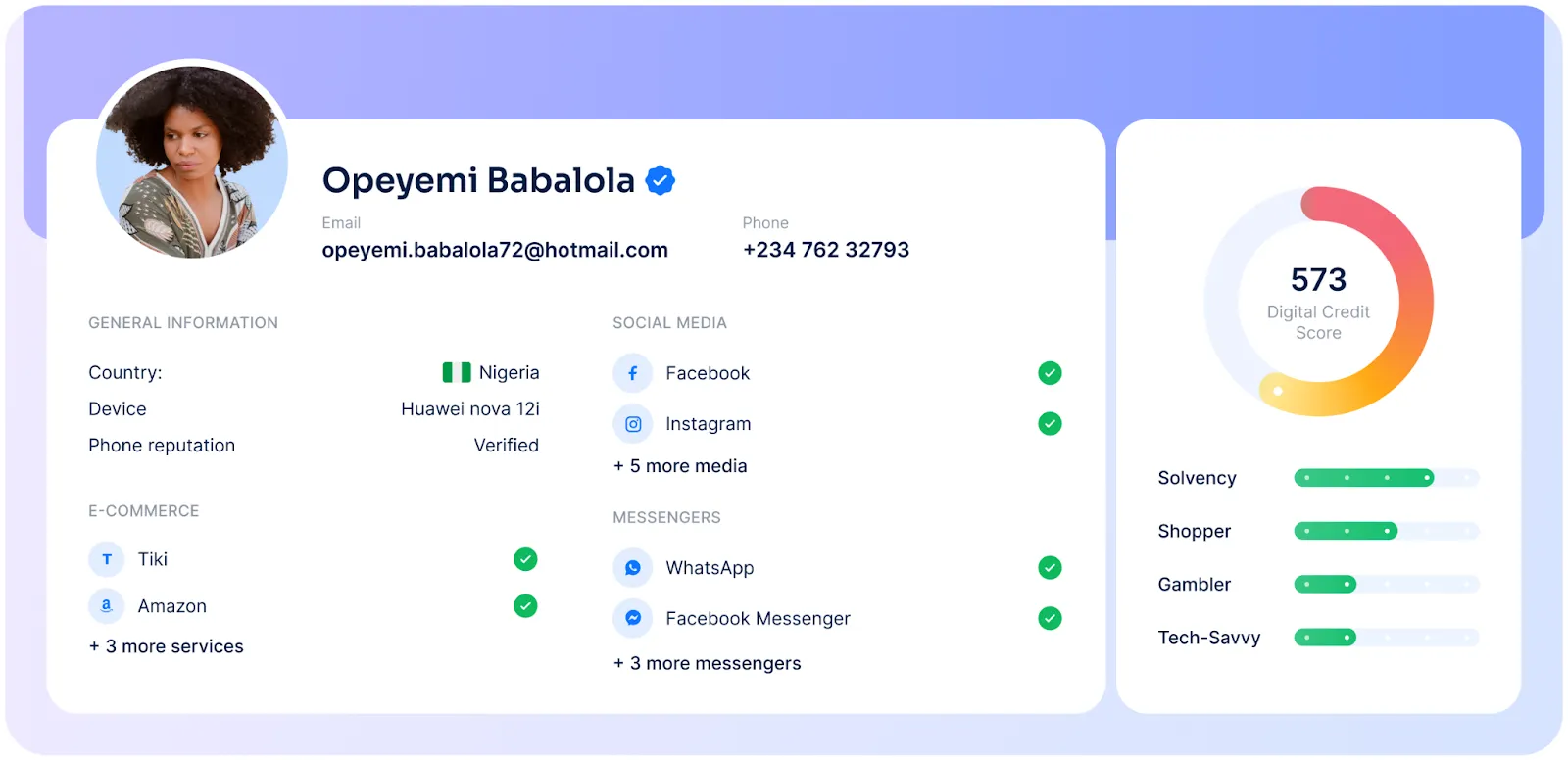

Risk Seal offers neobanks a reliable Digital Credit Scoring system. With its help, you can obtain 400+ alternative data points for each applicant.

Our neobank clients get:

- Real-time checks that take seconds

- Reduced user drop-offs

- Improved conversion rates without compromising risk

- Up to 70% reduction in KYC costs through early fraud detection

- Expanded target audience by increasing financial inclusion

This makes RiskSeal an all-in-one platform for credit risk onboarding, helping neobanks accelerate approvals while minimizing fraud.

Contact our manager to learn all details.

FAQ

What unique credit risk challenges do neobanks face?

Neobanks face the need to review thousands of credit applications daily and make fast decisions on them – all without compromising default rates.

Traditional credit scoring cannot meet such demands. Therefore, neobanks should consider using alternative data.

What types of alternative data are useful for credit scoring in neobanks?

Neobanks can use alternative data such as email and phone records, location data, information about paid subscriptions and online shopping, and social media activity.

With this information, a neobank can create a comprehensive financial profile for the applicant.

How do machine learning models enhance credit risk accuracy?

ML models allow for a range of checks to identify potential borrowers.

This includes face recognition – comparing applicant images across different platforms, name matching – identifying mismatches in user names, and anomaly detection – spotting suspicious behavioral patterns.

How does RiskSeal Digital Credit Scoring system support neobanks?

The RiskSeal scoring system provides neobanks with over 400 data points for each potential borrower. We research global and local digital platforms to analyze users' digital footprints.

As a result, neobanks can extend credit to thin-file users, effectively prevent fraud, improve their customers' user experience, and reduce default rates.

See more

Explore how credit stress testing and real-time alternative data empower lenders to spot early warning signs and protect portfolios during the Christmas season.

.webp)

Learn how data enrichment enhances credit risk models by filling gaps, spotting fraud early, and supporting inclusive lending.

Learn how modern customer risk assessment leverages AI and alternative data to fight fraud, boost compliance, and speed up smart approvals.