Back to Glossary

Alternative Credit Scoring

Discover how alternative credit scoring uses non-traditional data to improve lending decisions and increase financial access.

Discover how alternative credit scoring uses non-traditional data to improve lending decisions and increase financial access.

Traditional credit scoring has long been the foundation of lending decisions.

However, it relies heavily on historical financial data, which leaves a large portion of the global population underserved.

Millions of consumers have little or no formal credit history, making it difficult for lenders to assess their reliability.

Alternative credit scoring uses a broader range of data to evaluate borrowers. It includes digital behavior, transaction patterns, and identity signals.

This approach has gained traction with the rise of fintech and online lending, where speed, accuracy, and fraud prevention are critical.

As a result, lenders can make more informed decisions while expanding access to credit.

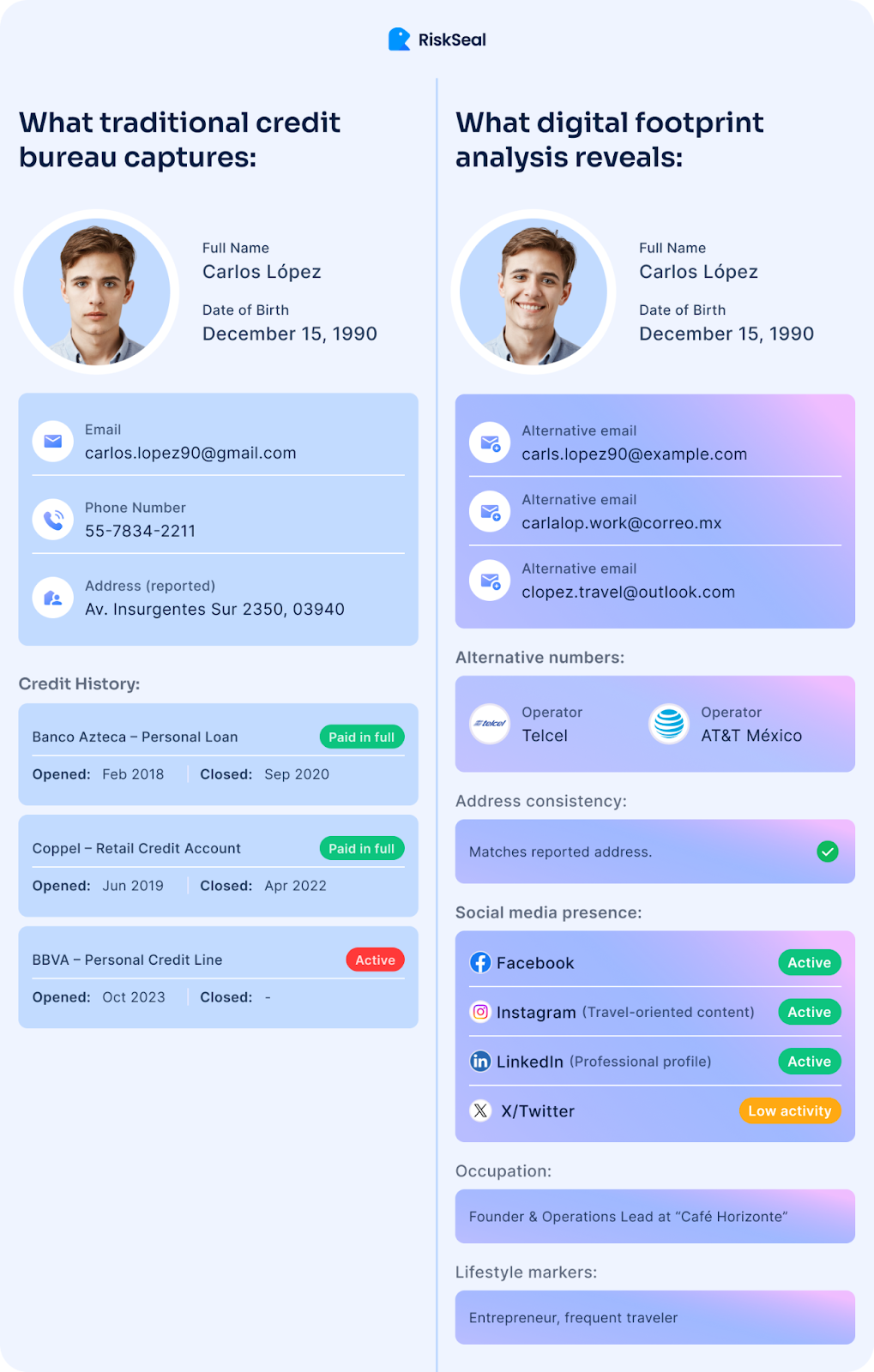

Alternative credit scoring assesses creditworthiness through a person’s digital footprint. It looks at how individuals exist and behave across online services.

Lenders analyze signals such as email history, phone activity, and account presence. They also review app usage, subscription services, and platform registrations.

Some signals include whether an email or phone was linked to suspicious activity, or how consistently a person appears across platforms.

This approach helps risk teams see patterns that are not visible in formal records. It adds context to identity, behavior, and intent.

To illustrate this, take two applicants.

The first has a 10-year-old email address. It is linked to LinkedIn, streaming services, and several social platforms. Profile photos are consistent, and activity looks stable over time.

The second applicant uses an email created yesterday. It appears in multiple loan applications within hours. There is little to no digital history, and the data shows inconsistent signals.

Both applicants may look similar in a basic application form. However, their digital footprints tell very different stories.

This is where alternate credit scoring becomes valuable. It allows lenders to move beyond static inputs and evaluate the reliability of a borrower based on real-world digital behavior.

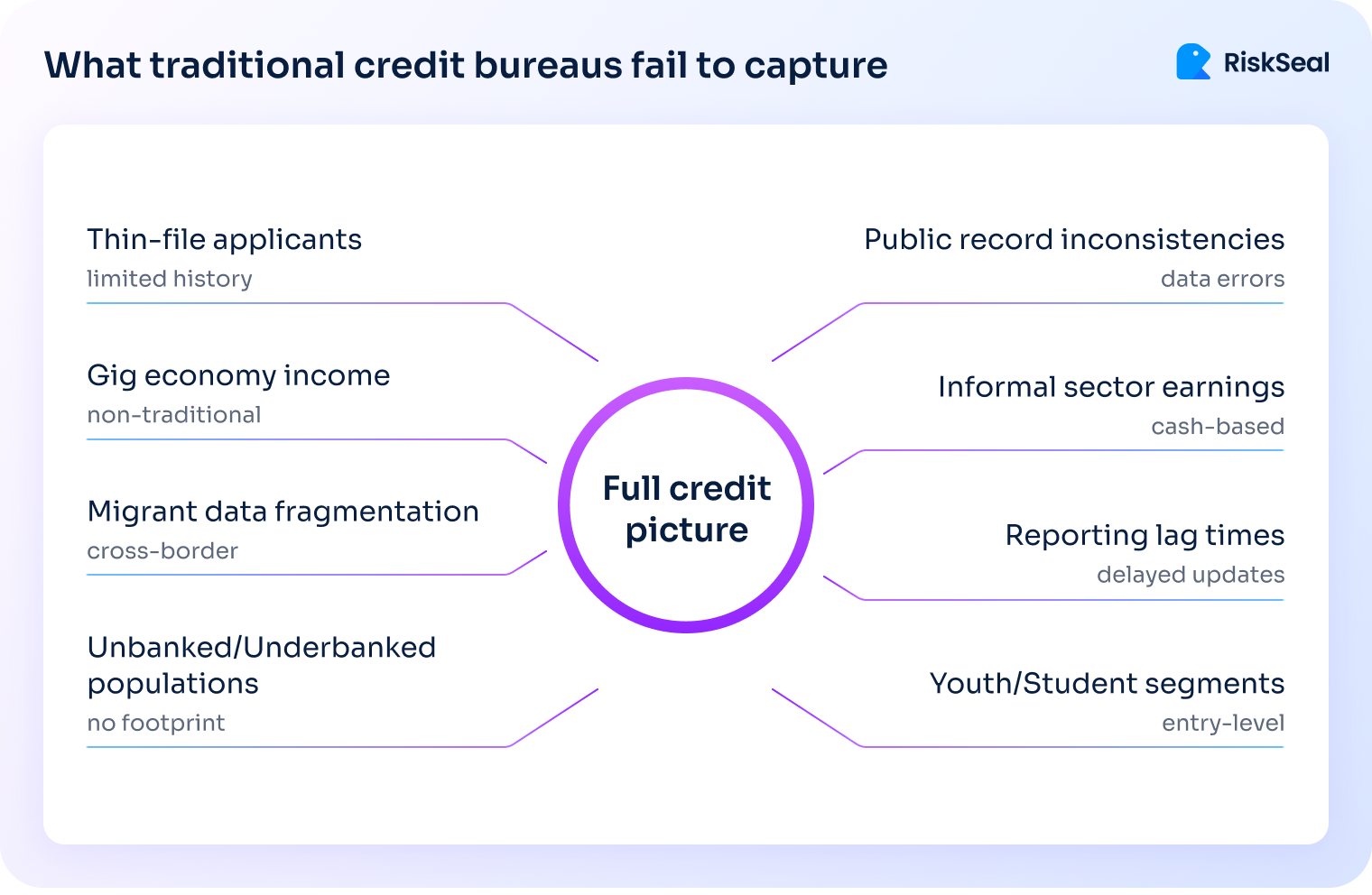

Traditional credit scoring systems are reliable, but they were not designed for today’s digital environment.

First, they depend on existing credit history. This excludes “credit invisible” users, including young adults, freelancers, and people in emerging markets.

Second, the data is often outdated. Credit reports reflect past behavior, but they do not capture a borrower’s current financial situation in real time.

Third, the data sources are limited. Traditional models focus on loans and credit lines, ignoring other financial signals such as subscriptions, digital payments, or online activity.

Because of these limitations, fintech companies adopt alternative approaches. They need faster decisions, broader coverage, and more accurate risk signals.

Alternative data helps them achieve this without compromising risk control.

Lenders use multiple categories of alternative data to build a more complete risk profile:

In some cases, lenders also use device fingerprinting, in-app behavior, and transaction patterns to enrich their analysis.

Each of these data points adds context. Together, they help lenders form a more accurate view of the applicant.

Alternative credit scoring follows a structured process that combines data analysis with risk modeling.

1. Data collection. Lenders gather data from multiple sources, including digital activity, financial behavior, and identity signals.

2. Data verification. The system checks consistency across data points. For example, it compares IP location with the declared address or validates email ownership.

3. Risk modeling. Machine learning models analyze patterns in the data. They identify correlations between behaviors and repayment outcomes.

4. Score calculation. The system assigns an alternative credit score based on the analyzed data. This score helps lenders decide whether to approve, reject, or review the application.

Many platforms also integrate fraud detection at this stage. Suspicious signals are flagged early, reducing the risk of issuing loans to fraudulent applicants.

Alternative credit scoring offers several practical advantages for lenders:

Lenders work with publicly available signals and data that users have already consented to share when registering for services, creating accounts, or using digital products.

This approach helps risk teams balance growth and risk more efficiently.

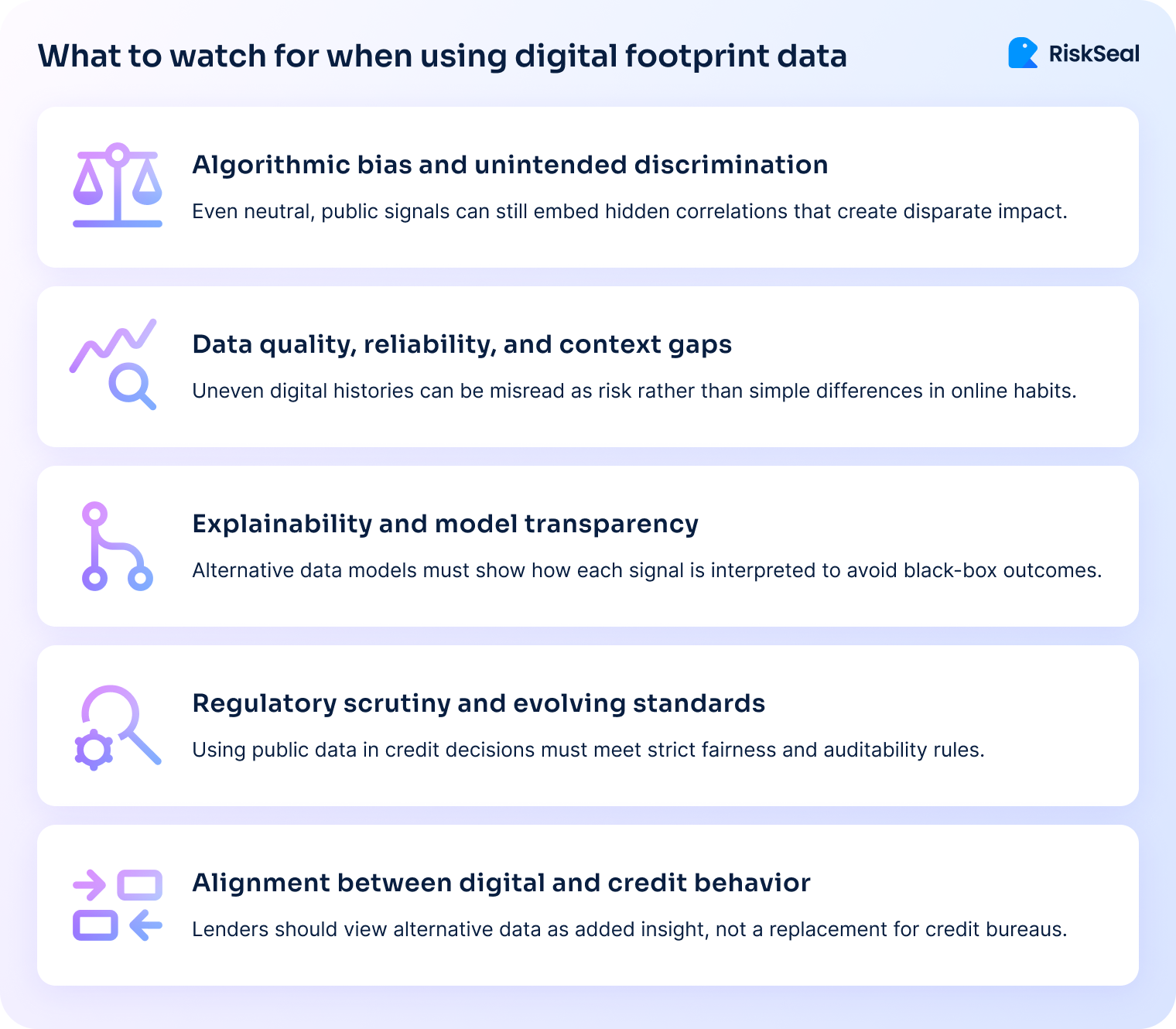

Despite its advantages, alternative credit scoring comes with challenges that lenders must manage carefully.

Using non-traditional data raises questions about user consent and data protection.

To address this, many teams adopt a privacy-by-design approach. They limit sensitive data exposure through anonymization and give users clearer control over what they share.

This helps build trust while staying aligned with regulatory expectations.

Not all alternative data is equally reliable.

To reduce noise, lenders cross-check signals across multiple sources instead of relying on a single input.

For example, they may validate behavioral patterns against transaction data or account history. Some teams also adjust model weights based on data confidence.

Regulations around alternative data vary by region and continue to evolve.

Risk teams often benchmark alternative models against traditional scoring outputs to explain decisions more clearly.

Many also test new approaches in controlled environments before full deployment to avoid compliance gaps.

Machine learning models can be difficult to interpret, especially in regulated environments.

To address this, lenders use explainability tools that highlight which signals influenced a decision. Clear reasoning helps support adverse action requirements and internal reviews.

Addressing these challenges requires a balanced and practical approach. With the right controls in place, alternative credit scoring can remain both effective and compliant.

Alternative credit scoring is widely used across modern financial services:

These use cases highlight the flexibility of alternative risk scoring in digital environments.

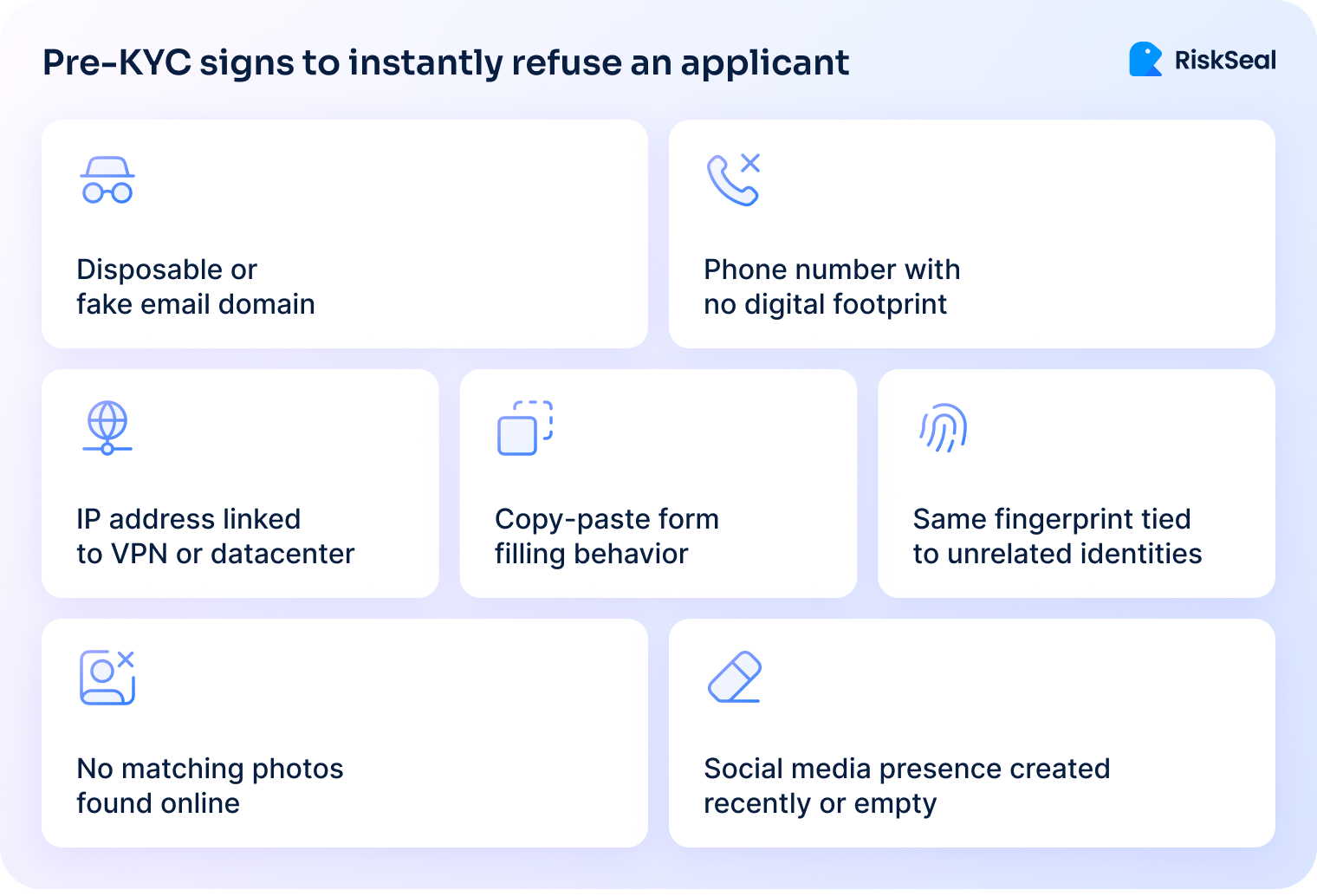

Fraud prevention is a critical part of modern credit risk assessment. Alternative data plays a key role in identifying suspicious activity early.

Digital footprint analysis allows lenders to verify identity signals such as email history, phone data, and online presence. Inconsistencies across these signals often indicate potential fraud.

Behavioral data adds another layer of protection. Unusual interaction patterns or device mismatches can signal automated or fraudulent activity.

Solutions like RiskSeal combine these signals into a unified risk profile. By analyzing identity, behavior, and technical data together, lenders can detect fraud at the application stage.

This reduces losses, lowers KYC costs, and protects both lenders and legitimate borrowers.

Alternative credit scoring is quickly becoming a standard in modern lending. It helps lenders move beyond the limitations of traditional models and adapt to a digital-first world.

By using real-time and diverse data sources, lenders can improve risk assessment, expand access to credit, and strengthen fraud prevention.

At the same time, careful attention to privacy and regulation remains essential.

For credit providers operating in competitive and regulated environments, alternative data offers a practical way to make better decisions while supporting growth.