Explore how credit scoring models use AI, alternative data, and digital signals to improve risk assessment, fraud detection, and borrower coverage.

Credit scoring is the logic behind every lending decision. It helps banks and lenders decide who to approve, how much credit to offer, and how to manage risk after approval.

For decades, this logic relied mainly on bureau data and repayment history. That approach still matters. But it leaves gaps when borrowers have thin files, fast-changing financial behavior, or limited formal credit records.

AI and alternative data are helping lenders close those gaps.

A credit scoring model is a statistical or algorithmic system that estimates credit risk. It predicts whether an applicant is likely to repay a loan or default, and produces a numerical score or risk category. A higher score usually means lower expected risk.

Lenders use this estimate during underwriting to support decisions around approval, rejection, credit limit, pricing, or manual review. Models also help standardize decision-making across large applicant volumes.

A strong model does not replace human risk expertise. It gives underwriters a structured risk signal to use alongside policy rules, affordability checks, fraud checks, and compliance requirements.

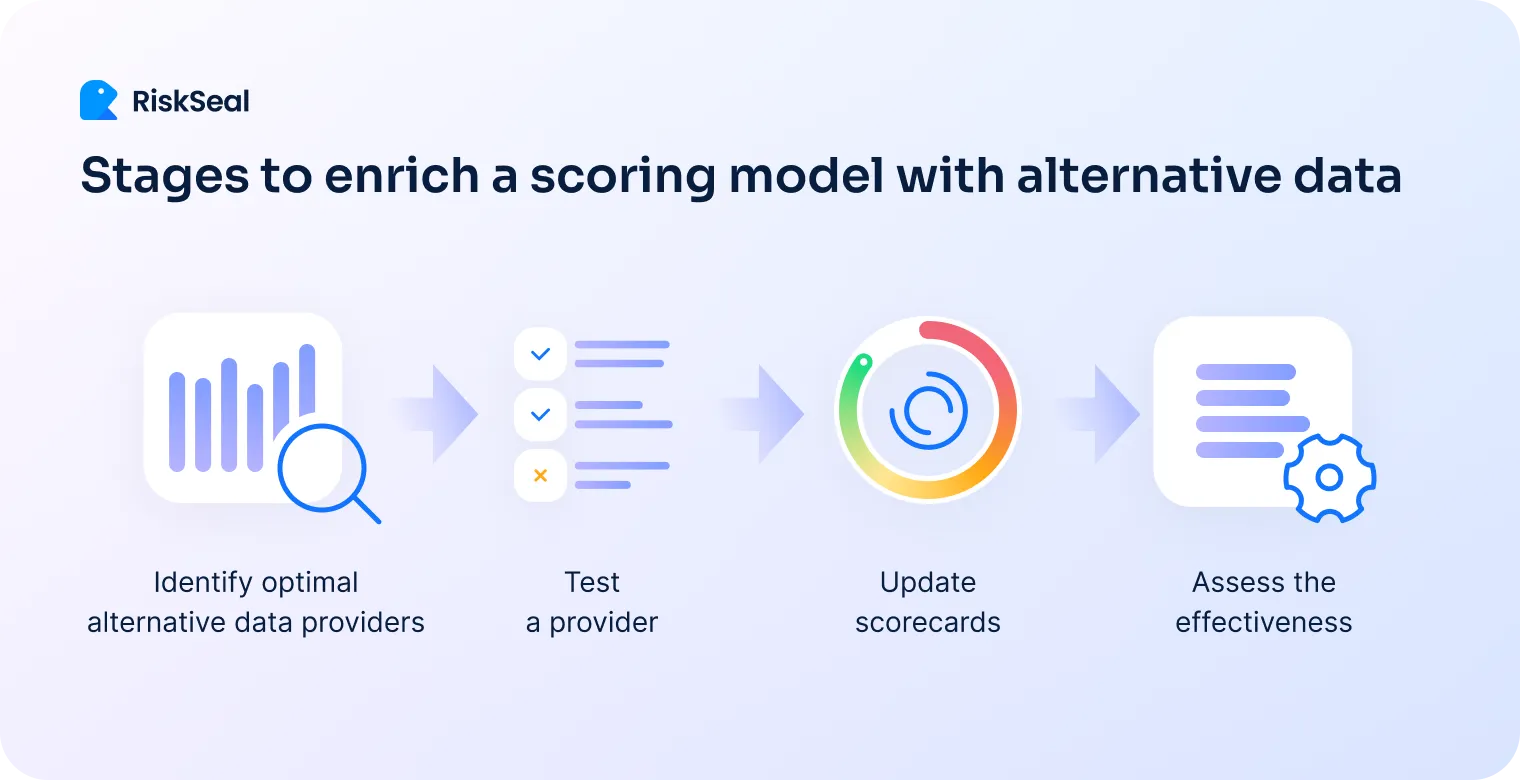

An enhanced credit risk model uses a broader data set than a traditional model.

It combines financial data with alternative data, behavioral signals, and digital footprint insights to build a more complete borrower profile.

Key signals include:

Enhanced models are especially useful when bureau data is limited, helping risk teams assess applicants who lack formal credit history.

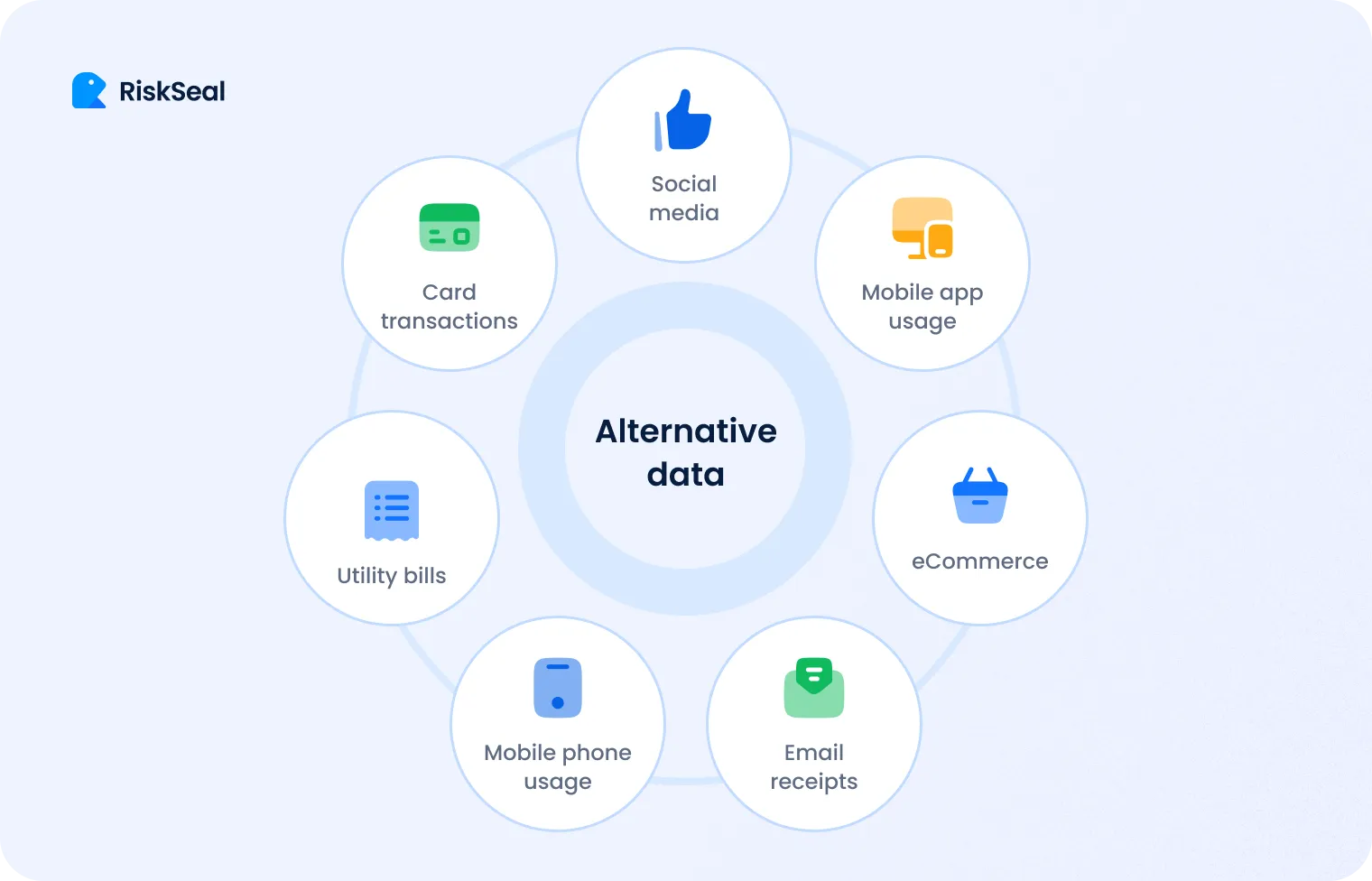

Alternative data includes non-traditional information that helps lenders understand credit risk beyond bureau files and repayment history.

It draws on real-world digital signals to show whether an applicant's identity is established, consistent, and active.

Sources include:

A long-standing email, active phone number, consistent social presence, and normal network activity can support a stronger borrower profile.

A newly created email, suspicious IP location, or inconsistent digital trail may point to higher risk.

Some providers also include device fingerprinting and adverse media screening depending on the use case and regulatory environment.

AI and machine learning help lenders work with larger and more complex data sets, identifying relationships between risk signals that simpler scorecards may not capture.

In enhanced credit decisioning, these technologies combine traditional repayment data with alternative digital signals to make risk assessment more dynamic.

AI-driven models can also be retrained with fresh data to respond to new borrower behavior, fraud patterns, and market conditions.

That said, models must be tested, validated, monitored, and explained before use in live credit decisions.

Turn digital footprint data into smarter credit models

Banks traditionally use a mix of external scores, internal models, and scorecards across different parts of the credit decision process.

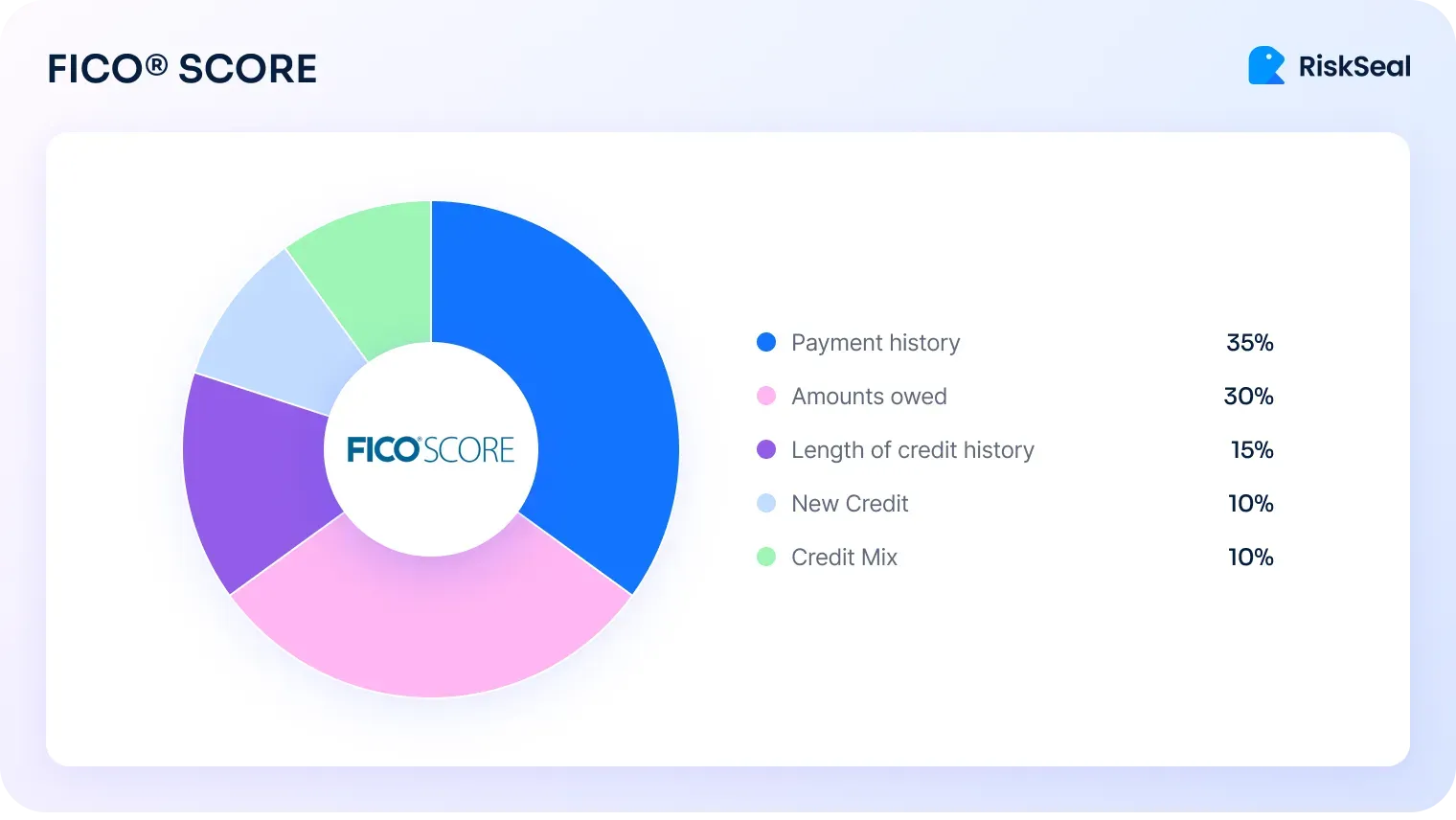

FICO is one of the most widely known systems. It uses credit report data – payment history, amounts owed, credit history length, new credit, and credit mix – to assess repayment risk.

Banks typically combine it with internal policies, affordability checks, and fraud screening.

VantageScore is another consumer lending model, developed by the three major U.S. credit bureaus. It uses factors such as payment history, credit utilization, balances, and available credit.

Some versions support broader borrower coverage, helping assess applicants with limited credit history.

Internal bank scoring systems use the bank's own historical customer and transactional data.

These models match risk assessment to the bank's specific products and risk appetite, and support portfolio monitoring, capital planning, and pricing.

Application scorecards assess new credit requests at origination, using application data, bureau data, income, employment, affordability, and fraud indicators.

Behavioral scorecards apply to existing customers, using account behavior, repayment history, utilization, and recent risk changes.

Banks use them to manage credit limits, renewals, collections strategy, and early warning monitoring.

Banks evaluate borrowers through several layers of risk checks: credit history, income stability, repayment behavior, debt burden, affordability, collateral, and fraud risk.

The exact signals depend on product and market – consumer lending, SME lending, mortgages, credit cards, BNPL, and microfinance each require different inputs.

Traditional data works well for borrowers with rich credit files, but it can miss applicants with thin files or fast-changing financial behavior.

This creates a difficult trade-off: rejecting these borrowers limits growth, while approving them without sufficient data increases default and fraud risk.

Enhanced and AI-driven scoring addresses this gap. It provides more signals while keeping credit decisions structured, auditable, and suitable for regulated environments.

Credit scoring models can be classified by methodology, credit lifecycle, and data source.

Subjective expert models rely on the experience of credit officers, often using the 5 Cs of credit: character, capacity, capital, collateral, and conditions.

Useful when data is scarce or human review is required.

Statistical parametric models use mathematical formulas to link borrower data with default risk. Logistic regression is a common standard, valued for transparency and interpretability.

Discriminant analysis separates applicants into risk groups by assigning weights to variables.

Machine learning models capture complex patterns that linear models may miss. Decision trees create rule-based structures. Neural networks model deeper relationships in large data sets.

Ensemble methods such as stacking and boosting can improve predictive accuracy when properly validated.

Traditional models are strongest when a borrower has reliable credit history.

Enhanced models add current context – digital footprints, telecom data, email and phone signals, IP and device data. This matters most when formal repayment history is incomplete.

Enhanced models don't rely on a single signal. They look at combinations of signals and how those signals interact, which is where ML and AI credit scoring can improve predictive power.

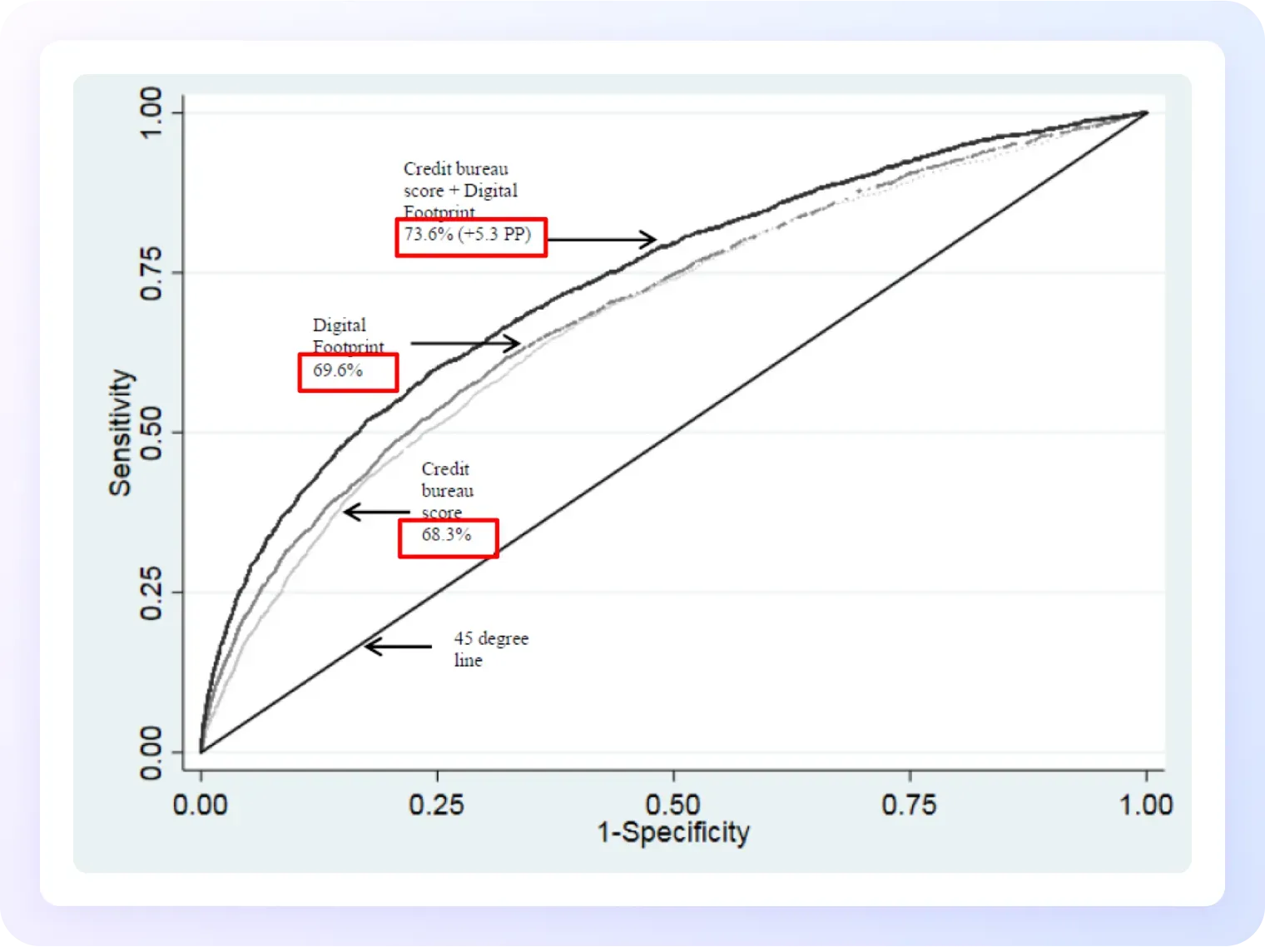

In one benchmark, bureau-only scoring had an AUC of 0.68. Alternative data alone reached 0.70, while a combined model reached 0.73.

Even a modest AUC lift matters in real lending. It can mean more approved good borrowers, fewer false declines, and earlier identification of higher-risk applications.

Model updates should follow a clear process in regulated lending: retrain, test, validate, approve, and monitor before deploying in live decisions.

A credit scorecard assigns points to risk factors, with the total score categorizing the applicant by risk level.

Scorecards translate borrower characteristics into a decision-ready signal and can reduce manual review time while supporting consistency at scale.

Application scorecards combine application data, bureau data, affordability inputs, fraud checks, and sometimes alternative data. All to determine whether the borrower fits the lender's policy and risk appetite.

Behavioral scorecards use repayment patterns, utilization, and recent account changes to monitor risk after initial approval.

Scorecards support risk segmentation into bands such as low, medium, high, and manual review enabling consistent pricing, credit limits, approval rules, and collection strategy.

They are often embedded in automated underwriting engines alongside policy rules, fraud logic, and compliance checks, keeping decisions fast, consistent, and auditable.

Here’s how traditional bureau-based models compare to alternative ones in real-life credit approval environments:

A modern credit scoring platform should help lenders collect data, run risk models, return scores, automate decisions, and monitor performance inside the lending workflow. Not just produce a score in isolation.

Scoring platforms connect data sources, execute scoring logic, return risk outputs, and support real-time decisioning.

They should allow risk teams to test, monitor, and adjust decision logic through API integrations with loan origination systems, CRM, and decision engines.

Automated underwriting uses scores, policy rules, affordability checks, and fraud signals to process applications with less manual work.

Clear low-risk cases move through faster; high-risk cases are declined or flagged before reaching an underwriter, letting underwriters focus on complexity.

Fraud prevention is strengthened by alternative data. Email, phone, IP, device, and behavioral signals can expose identity mismatches before funds are issued or goods released.

Risk automation connects scoring, policy rules, fraud checks, credit limits, and approval conditions. It reduces repetitive work and improves decision traceability.

Credit scoring models must be accurate and explainable. Risk teams need to understand why a model produced a score, both for internal governance and for adverse action processes.

Models should be documented with clear records of data sources, variable logic, validation results, and monitoring procedures. They should be tested for bias, proxy variables, and unintended discrimination.

Regulatory requirements add further structure. The Basel Committee highlights the need for credit risk policies, internal controls, and validation for models used in risk ratings.

IFRS 9 requires forward-looking credit risk assessment for impairment under an expected credit loss framework.

Auditability, covering data inputs, model outputs, decision reasons, and overrides, should be built into the scoring process from the start.

Credit scoring models are evolving beyond traditional bureau data. AI and alternative data improve predictive accuracy, especially for thin-file borrowers and digital lending channels, and help detect fraud earlier.

The strongest models combine traditional data, alternative data, solid validation, and clear governance. That way, they support better approvals, stronger portfolio control, and more inclusive lending.

For banks, fintech companies, neobanks, BNPL providers, and microfinance institutions, automated scoring solutions are increasingly a standard part of how faster, more reliable credit decisions get made.

What are credit scoring models?

Systems that estimate borrower risk and help lenders predict the probability of default.

What credit scoring models do banks use?

FICO, VantageScore, internal scoring systems, application scorecards, and behavioral scorecards. Typically combined with policy rules, affordability checks, and fraud screening.

What is the difference between traditional and alternative credit scoring models?

Traditional models rely on bureau and repayment data. Alternative models add signals such as digital footprint, telecom, email, phone, IP, and behavioral data. Traditional models are strongest for established borrowers; alternative models add context for thin-file or digital-first applicants.

How does AI improve credit scoring models?

It handles larger and more complex data sets, detects patterns traditional models may miss, and supports faster automated decisions. Yet still requires validation, monitoring, explainability, and governance.

What data is used in alternative credit scoring?

Email, phone, IP, device signals, telecom data, payment data, and digital behavior. The exact mix depends on the lender, market, product, and compliance requirements.

Why are alternative credit scoring models important for fintech companies?

Fintech companies often serve digital-first and thin-file customers. Alternative scoring helps them assess more applicants, reduce fraud, and make faster decisions.