How to Boost Predictive Power Using Digital Footprints

Learn how digital footprints can enhance credit scoring by utilizing data from social media profiles and website registrations to assess borrower solvency.

.webp)

The global digitalization of modern society makes it possible to obtain information about almost every person by analyzing their online activity.

Data from social network profiles, registrations on various websites, statistics on the use of Internet services – all of this is broadly available data that can be useful to lenders in the process of assessing the solvency of a potential borrower.

Based on the results of the National Bureau of Economic Research (NBER) study, we have tried to understand the role of digital footprint analysis in credit scoring.

The concept of digital footprint

Digital footprint is the trail of information that a person leaves behind when using various Internet resources and digital devices.

This source of information opens up huge opportunities for credit organizations, as more than 5.4 billion people are active online worldwide, and this figure is constantly growing.

.jpeg)

Examples and value of digital footprint data

Digital footprints allow forming an idea of a person's financial status.

For example, the use of an iOS device, the presence of a mailbox on paid email hosts, subscription to premium services, etc. speaks in favor of a high economic status.

By analyzing the digital footprint, the lender can get information about the borrower's financial habits and purchasing behavior. Registrations on gambling platforms, regularity of payments for paid subscriptions, etc. will tell about this.

Digital footprints can reveal specific personal qualities of a loan applicant. For example, impulsive buying behavior and a tendency to default are evidenced by online purchases made at night.

Thus, digital footprints represent a wealth of valuable data for effective credit scoring.

Given RiskSeal's expertise in digital footprint analysis, we will cover the topic from our own experience.

The role of credit bureau data in credit scoring

Credit bureaus are organizations that collect and store people's credit history. Their main function is to provide credit reports upon request of creditors or credit history owners.

.svg)

.webp)

Information collected by credit bureaus

To fulfill their tasks, credit bureaus collect and store such information about a person:

1. Credit history. This includes data on credit accounts ever opened, types of credit products, the ratio of outstanding debt to the available credit limit, and other financial information.

2. Payment behavior. This is the part of the credit history that contains information about late payments, creditors’ applications to collection agencies or courts, and the timeliness of loan payments.

3. Demographic data. This includes information about a person's age, gender, and place of residence.

Creating a credit bureau score

Based on the information discussed above, credit bureaus create a person’s credit score.

This is a numerical representation of a potential borrower's creditworthiness, which in traditional credit scoring is usually expressed as a number between 300 and 850.

However, this range can vary from organization to organization.

As an example, consider the credit rating assigned to borrowers by Experian, one of the U.S. credit bureaus. Here, a borrower can be assigned a credit score from 0 to 999.

.jpeg)

The credit rating of a potential borrower directly affects the likelihood of a favorable decision on a loan application and the terms of the loan.

For example, those with a “Very poor” rating are likely to be denied a loan.

If the rating is “Poor” or “Fair”, the lender may approve the loan but apply a higher interest rate. Alternatively, the lender may require a guarantor or collateral as an additional guarantee of repayment.

Potential borrowers with a high rating will be granted a loan with the highest probability and on the most favorable terms.

Limitations of traditional credit scoring

The limited data sources used by credit bureaus prevent banks from lending to about 1.4 billion people worldwide. This is the number of able-bodied people who are unbanked and, therefore, lack a credit history and credit score.

To solve this problem, more and more lenders have started to turn to alternative data for credit scoring and, in particular, to digital footprint analysis.

This approach to assessing potential borrowers helps to stimulate financial inclusion.

This is particularly relevant for developing countries, where the percentage of unbanked people is very high.

According to the World Bank report, 135 countries can be classified as emerging markets.

Disadvantages of traditional credit scoring methods

In addition to a lack of financial inclusiveness, credit scoring based on credit bureau data has other disadvantages:

- Static nature. Current credit scores provide a picture of a person's creditworthiness based on historical data. They may not take into account recent changes in an applicant's financial situation. For example, losing or changing jobs, changes in income levels, etc.

- Greater likelihood of bias. Traditional credit scoring models can be biased against applicants based on a variety of factors. These include age, gender, region of residence, etc.

- Limited list of data used. Relying on credit bureau data, lenders may overlook equally important information that affects a borrower's ability to pay and creditworthiness. For example, employment stability or education level.

Digital footprints vs. credit bureau score predictive power

The comparative analysis of the predictive power of digital footprint-based scores and credit bureau scores is based on data from the National Bureau of Economic Research (NBER) study.

The researchers use Area Under the Curve (AUC) metric to compare credit scoring models based on digital footprint credit scores and credit bureau scores.

The following results were obtained:

- The AUC of the model using digital footprint variables is 69.6 %.

- The AUC of the model using only credit bureau scores is 68.3 %.

What does this imply for credit institutions?

Can digital footprint data substitute for credit bureau data?

Based on the data published in the NBER report and our own experience, we can say that digital footprint cannot completely replace traditional credit bureau data.

Rather, it complements them by providing a powerful scoring model to objectively evaluate borrowers.

Below, we present some research findings that support this view.

The correlation between a score based on digital footprint data and a credit bureau rating is only about 10%.

This is illustrated by the graph below. The X-axis shows the percentiles for credit bureau scores, and the Y-axis shows the percentiles for digital footprint-based scores:

.jpeg)

As a consequence, the discriminatory power of a scoring model that uses both data sources is significantly greater than that of a model based on digital footprint or credit bureau data alone.

In other words, a lender using data from both sources can make more informed decisions on loan applications.

Complementary nature of digital footprints

Supporting the fact that digital footprints can improve the accuracy of credit bureau scores is a comparison of the AUC of a composite credit scoring model to individual models.

As reported in the study results, the AUC of the combined model is 73.6%. This is 5.3% higher than the model using only credit bureau scores and 4% higher than the model based on digital footprint credit scores.

.jpeg)

Data from Experian, one of the USA credit bureaus, was used as input data for this comparative analysis.

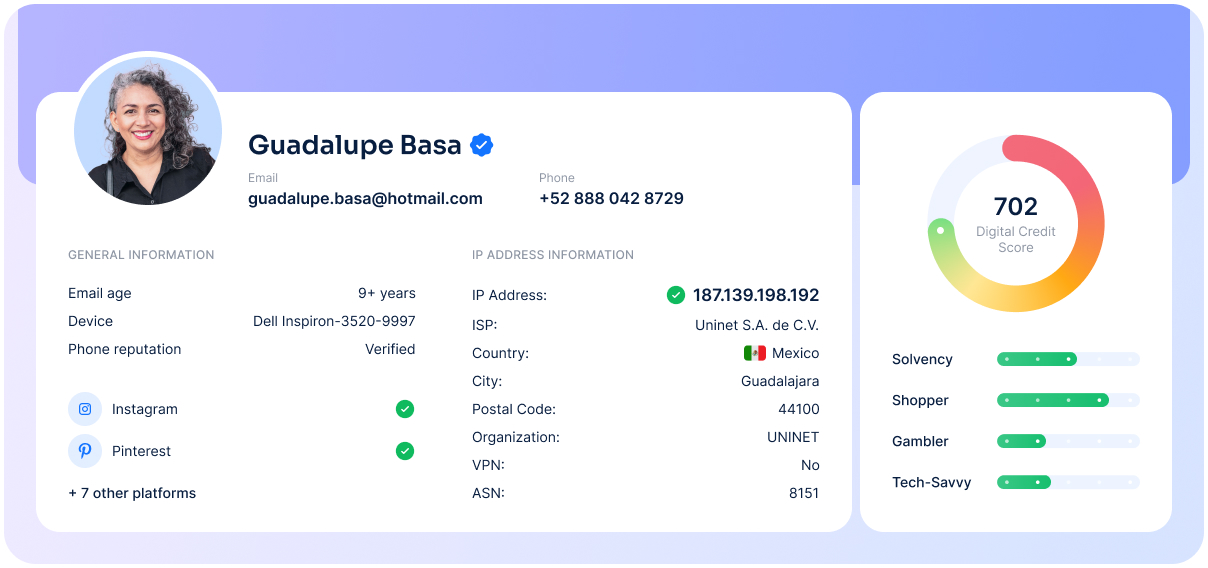

Digital footprint analysis at RiskSeal

Digital footprint analysis is the basis of the RiskSeal digital scoring system.

To assess the creditworthiness of a potential borrower, we analyze the following data:

- email address

- phone number

- IP address

- full name

- location

- borrower's avatars

We assess their digital footprints across 200+ digital platforms and provide the client with 300+ applicant data points, detailed profiles, and digital footprint credit scores.

During the analysis process, we focus on resources such as:

1. Premium services (e.g., Apple, Samsung). The use of premium products is a good indicator and has a positive impact on the digital footprint credit score.

2. Paid subscriptions (Netflix, Spotify, Disney+, streaming services). Regular usage and timely payments indicate the applicant's discipline and ability to pay.

3. Professional social networks (LinkedIn, Computrabajo, etc.). Such platforms provide data on a potential borrower's employment, education, and position.

In addition to providing clients with a wide range of data to objectively evaluate a borrower, RiskSeal's digital footprint analysis helps improve financial accessibility.

Our credit scoring method allows people with no credit history and no traditional credit score to qualify for a loan.

The same NBER study confirms this. According to its results, the discriminatory power of the digital footprint for unbanked people matches the discriminatory power for borrowers with a credit history – 72.2% versus 69.6%.

This means that digital footprint analysis from RiskSeal can help millions of people who don't have access to formal financial services get credit.

FAQ

How is a credit bureau score created?

Credit bureaus collect information about a person that includes credit history, payment behavior and demographic data.

Based on this, people are given a score – usually between 300 and 850, but these numbers can vary from organization to organization.

Each score corresponds to a different credit rating for the potential borrower. It can be “Very bad”, “Bad”, “Fair”, “Good”, or “Excellent”.

What are the potential biases in traditional credit scoring methods?

Traditional credit scoring methods are characterized by several disadvantages, including a certain bias towards applicants based on various factors – for example, age, gender, region of residence, and more.

What is the predictive power of digital footprints compared to credit bureau scores?

The predictive power of digital footprints is slightly higher than that of credit bureau scores.

According to the NBER study, digital footprints have an AUC of 69.6%, while credit bureau scores have an AUC of 68.3%.

How can digital footprints enhance the accuracy of credit bureau scores?

Digital footprints significantly improve the accuracy of credit bureau scores. According to the same study, the AUC for the combined models is 73.6%. This is 5.3% higher than the model using only credit bureau scores and 4% higher than the model based on digital footprint credit scores.

What is the focus of digital footprint analysis at RiskSeal?

RiskSeal focuses on analyzing three types of resources: premium services, paid subscriptions, and professional social networks. The registration of a potential borrower on such platforms allows for the speaking of high economic status and stable employment.

How do digital footprints facilitate unscorable customers' access to credit?

Consumers without a credit history cannot qualify for credit from financial institutions that use traditional credit scoring.

However, using digital footprint analysis allows a lender to obtain an applicant's digital credit score and make an informed credit decision.

See more

Discover four practical ways to strengthen consumer credit risk in 2026 with real-time underwriting, alternative data, smarter collections, and compliance-ready AI.

Discover how enhanced credit scoring models with alternative data drive financial growth and boost inclusivity.

.webp)

Discover how BNPL reshapes lending as split payments boost access and alternative credit scoring helps manage rising credit risk.