Top Risks BNPL Companies Must Tackle to Stay Competitive in 2026

Discover the top risks BNPL providers must tackle, from fraud to thin files, to stay competitive and compliant in 2026.

BNPL is growing fast, but so are the risks.

Most BNPL loans go to borrowers with weaker credit. Deep-subprime borrowers account for 45% of originations. Subprime borrowers make up another 16%.

Approval rates remain high. 78% of applications from subprime or deep-subprime consumers approved.

This makes risk management a key priority for BNPL providers. In this article, we take an in-depth look at the challenges and emerging risks they face every day.

Customer risks in the BNPL business model

BNPL’s success is built on speed, simplicity, and frictionless user experience. But those same strengths introduce new credit risk vulnerabilities.

Affordability vs. impulsivity

Breaking payments into small installments can make it hard to tell if a customer is borrowing responsibly or taking on too much.

Many BNPL users rely on the service to access credit quickly. Especially during stressful life events. In fact, 76% of those who missed a BNPL payment had experienced one or more major life events in the past year.

Impulse purchases are also common during seasonal sales. This is when ads and marketing promotions encourage quick spending.

BNPL providers must manage risk while keeping onboarding and approval processes fast. Even at a huge sales-driven scale.

Thin-file borrowers

BNPL attracts many credit-invisible consumers. Some of these consumers may be financially responsible, but for most, their credit behavior is unknown. These include:

- Renters with no mortgage record

- Savers who avoid credit cards

- Freelancers without salaried income

Excluding such applicants can lead to missed growth opportunities. But approving them blindly creates elevated risk.

Credit providers must therefore enrich bureau scores with alternative digital signals in BNPL to solve the credit invisibility issue.

Repayment behavior complexity

Some BNPL defaults aren’t caused by financial hardship but by behavioral deprioritization.

Because BNPL is perceived as low-stakes, certain customers treat repayments as optional. This makes it difficult to distinguish genuine distress from opportunistic default.

Payment stacking and hidden leverage

A growing challenge is BNPL stacking. This happens when consumers take out loans across multiple BNPL providers at once.

Nearly 60% of young users (18-28) have between two and five BNPL plans simultaneously. Often without fully realizing their cumulative obligations.

Traditional credit bureaus don’t yet fully capture BNPL exposures, leaving lenders blind to aggregate risk.

Providers are increasingly sharing data with each other to spot hidden debt quickly.

Income volatility

BNPL adoption is especially high among people whose income streams fluctuate significantly.

Their risk profiles are dynamic month to month. This requires continuous monitoring rather than static underwriting at loan origination.

In today’s economy, many people juggle multiple gigs, side hustles, and alternative income sources. Credit bureaus often cannot track this.

Without leveraging behavioral data in lending to closely monitor a person’s financial behavior and spending habits, risk can go unnoticed.

Behavioral bias and spending psychology

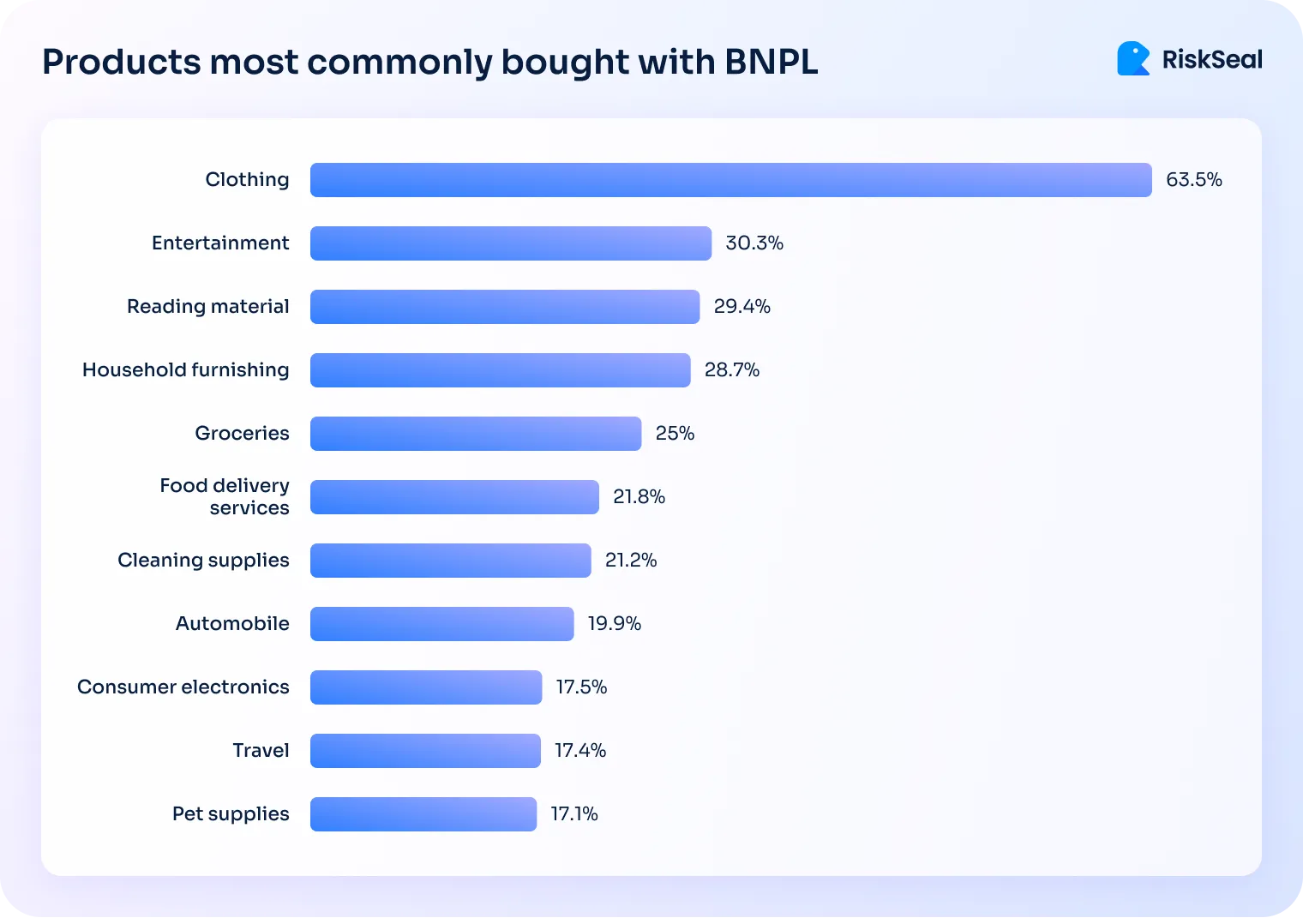

By lowering the “pain of paying,” BNPL encourages larger and more frequent purchases.

This can inflate exposure at the portfolio level. Particularly in categories like fashion, beauty, and electronics.

These are expected to generate a 72.5% share of BNPL usage in 2025 due to high repeat demand.

.svg)

.webp)

BNPL fraud risks

BNPL’s instant-approval model makes it an attractive target for fraud. Effective BNPL fraud prevention is becoming critical as fraud tactics evolve.

Dynamic fraud, static defenses

Traditional fraud defenses don’t work in a high-velocity BNPL environment.

Static KYC checks and manual reviews are valuable techniques, but they aren’t real-time. Fraudsters exploit every millisecond of latency between onboarding and loan approval.

As BNPL adoption grows, attackers increasingly use automation and AI-driven bots. They also conduct large-scale testing to bypass outdated security layers.

Without continuous, real-time monitoring, platforms face higher approval of fraudulent transactions. This leads to mounting operational losses.

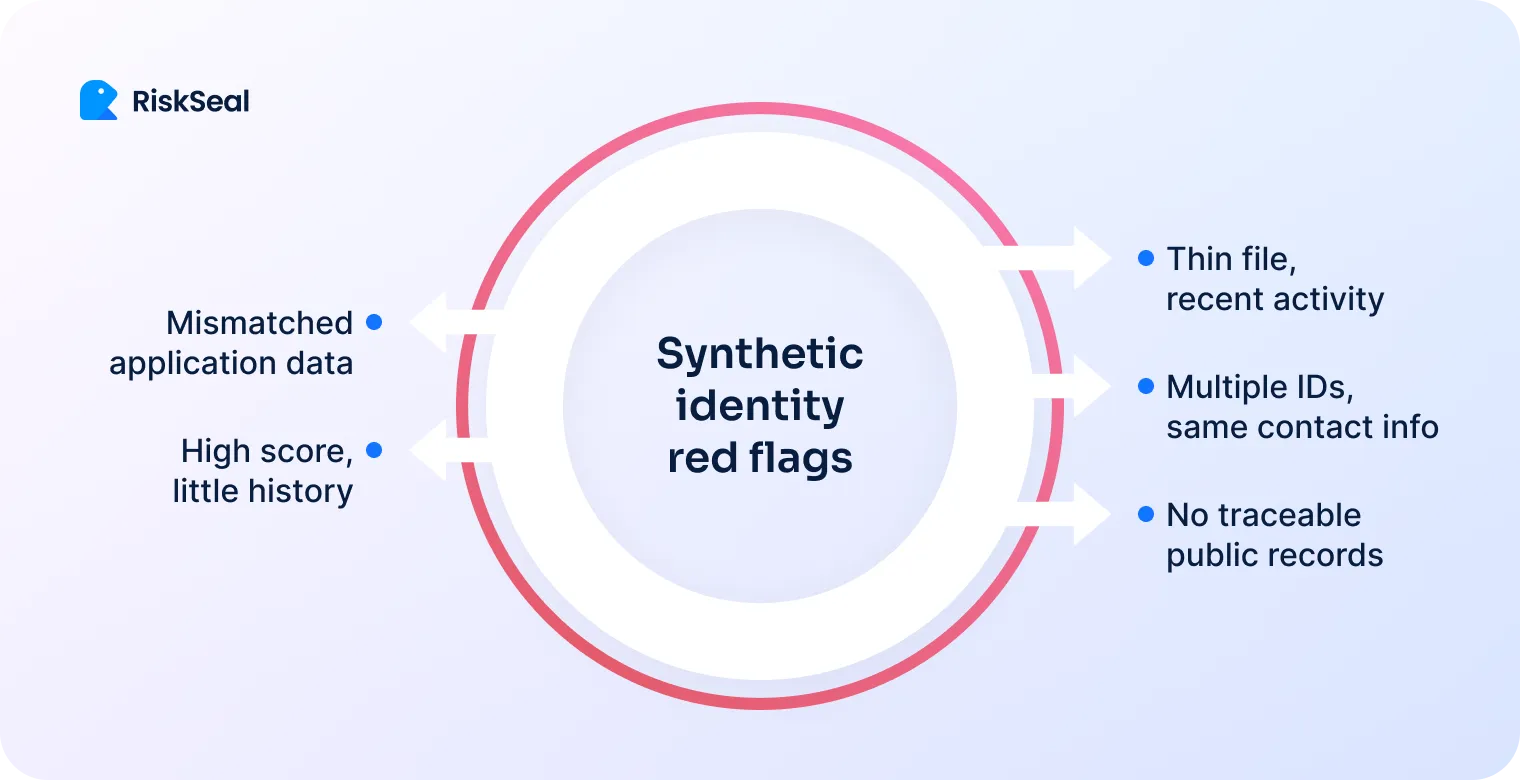

Synthetic identities and account takeovers

BNPL platforms face rising exposure to synthetic identity fraud, where real and fake data are combined to create “legitimate” profiles that pass onboarding.

Similarly, account takeover attacks leverage phishing and credential stuffing to hijack customer accounts and make unauthorized purchases.

In recent years, Fraud-as-a-Service (FaaS) networks have made BNPL platforms even bigger targets.

FaaS involves organized groups selling ready-made fraud tools, stolen identities, and automation scripts, making large-scale attacks faster and easier.

The “Never pays” phenomenon

An increasing share of BNPL losses comes from users who never intend to repay. They complete multiple purchases before abandoning accounts entirely.

The short loan cycles make detection challenging. Providers often absorb losses before patterns emerge.

This behavior is especially common among new or thin-file customers. Detection typically requires cross-platform monitoring to identify repeat offenders.

First-party and collusion fraud

Fraud can also come from applicants themselves or from collusion with merchants.

In first-party fraud, applicants misrepresent income, employment, or identity, taking advantage of lightweight onboarding.

Collusion fraud occurs when merchants and “customers” coordinate fake transactions, inflating sales while cashing out BNPL funds.

Friendly fraud happens when genuine customers dispute valid charges. They are forcing providers to refund payments while the merchant retains the revenue.

Market and regulatory risks shaping BNPL trends

BNPL’s meteoric growth has triggered heightened regulatory scrutiny across major markets. Providers now face a patchwork of evolving compliance obligations.

Fragmented global landscape

BNPL regulation is developing unevenly across major markets. The UK, U.S., and EU are taking different approaches to affordability checks, consumer protection, and provider oversight.

Growing pressure on transparency

Credit bureaus are gradually integrating BNPL data, but inconsistent provider reporting risks regulatory intervention.

Investors are also scrutinizing BNPL portfolios for charge-off rates, delinquency trends, and consumer protection policies.

Macroeconomic sensitivity

BNPL portfolios are highly exposed to economic downturns. Younger, thin-file customers are more vulnerable to job losses and inflation shocks.

This makes stress testing and forward-looking risk modeling critical.

Operational risks and smarter BNPL risk management

Even when customer and fraud risks are managed effectively, operational execution can make or break BNPL sustainability.

Inefficient collections

With small-ticket loans, traditional recovery tactics (legal action, third-party collectors) are often costlier than the outstanding balance.

Providers increasingly experiment with AI-driven repayment nudges and embedded collection workflows.

Data fragmentation

BNPL portfolios suffer from incomplete borrower profiles and limited repayment history. Without unified data pipelines, providers struggle to:

- Track borrower exposure across merchants

- Anticipate delinquency early

- Optimize credit limits dynamically

Retail concentration risks

Many BNPL providers rely heavily on a few high-risk sectors. These include electronics, fast fashion, and travel, creating portfolio vulnerability.

Seasonal shopping spikes and aggressive promotions can sharply increase defaults. High return volumes in these categories add further financial strain.

Expanding into more industries helps balance risk and keeps cash flow steady. Monitoring sector trends closely allows providers to react before issues escalate.

Reputation management

Negative narratives, like “BNPL debt traps,” spread fast. This erodes customer trust and attracts investor skepticism.

Providers must integrate risk governance and brand protection strategies into their operating models.

Simply approving fewer loans to make lending “safer” isn’t a solution. Overly strict approvals frustrate potential borrowers, reduce adoption, and can even harm the brand.

Instead, providers need smart risk management that balances protection with a smooth, customer-friendly experience.

RiskSeal’s digital credit scoring system built for BNPL

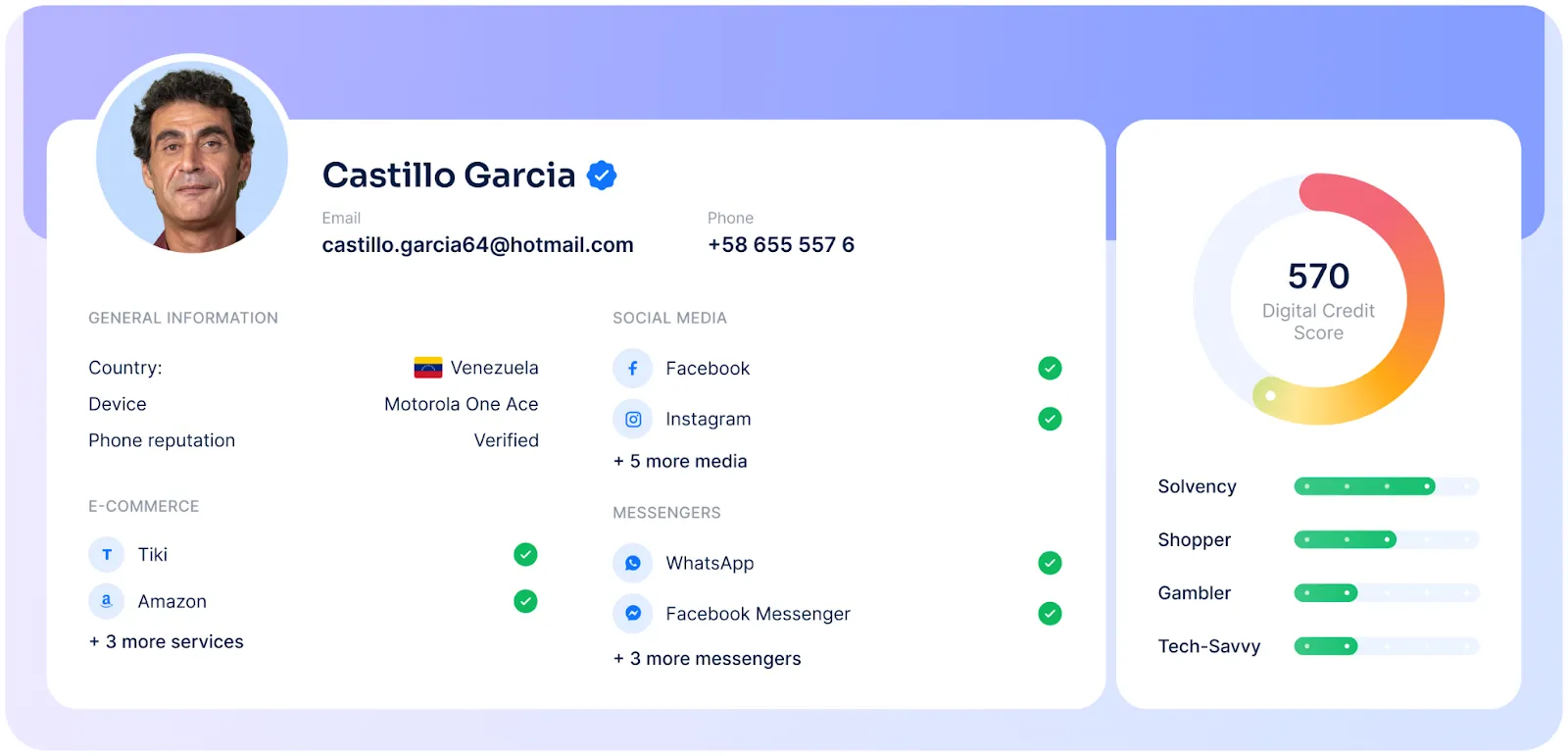

RiskSeal helps BNPL providers make fast, accurate lending decisions, even with minimal borrower data.

The platform uncovers over 400 digital signals per applicant, solving the thin-file challenge and enabling informed approvals when credit bureau data is missing.

This allows providers to expand credit access without increasing risk.

RiskSeal also reduces defaults and “never-pays” by combining digital footprint analysis with behavioral patterns.

The platform delivers a real-time BNPL credit score in as little as five seconds. This gives risk teams actionable insights while keeping the checkout smooth for customers.

Providers using RiskSeal see higher approval rates, lower defaults, and a better customer experience, all at the same time.

Closing insights into the BNPL credit score assessment

BNPL’s future depends on balancing frictionless customer experiences with disciplined risk management. Providers that thrive will be those that:

- Use real-time, behavioral, and alternative data to enhance underwriting.

- Shift fraud defenses from reactive to predictive.

- Embed compliance intelligence into their risk frameworks.

- Build portfolio resilience through diversification, better collections, and data-driven insights.

To see how RiskSeal can help your BNPL business manage risk while expanding credit access, book a demo today.

See more

Explore how digital footprint analysis improves credit scoring models, boosting default prediction accuracy and approval rates in emerging markets.

Master the credit risk metrics that actually protect your portfolio. Learn how top fintechs track, interpret, and act on risk signals in 2026.

.webp)

Discover how social media profiling enhances credit risk management by analyzing digital footprints.