The Step-By-Step Guide to Using Data Enrichment in Lending

Explore data enrichment with this hands-on guide. Learn onboarding best practices, avoid common pitfalls, and see real use cases.

Credit risk teams face a tough challenge: approve more borrowers while keeping losses under control. Traditional bureau data alone can’t meet that need.

Data enrichment turns everyday signals like emails, phones, IPs, and subscriptions into actionable insights.

In this article, we share practical steps, real-life use cases, and lessons from RiskSeal’s experience to help lenders put enrichment into practice.

Where data enrichment examples fit in the credit workflow

Data enrichment is a crucial component of the modern credit decision journey. It can be

mapped into several key stages:

- application

- onboarding

- scoring

- monitoring

Data enrichment provides the most value at the scoring and monitoring stages. There, it is enhancing the depth and accuracy of risk assessments.

B2B data enrichment also plays a vital role in the initial stages by flagging potential fraud.

Based on our experience at RiskSeal, we've found that enriching data at two distinct stages provides significant benefits for our clients.

Stage 1: Pre-KYC

We begin by enriching data at the pre-KYC (Know Your Customer) or initial assessment stage. Here, our primary goal is to quickly filter out applicants with the most red flags.

Here, we analyze a wide range of alternative data points, such as digital footprint and behavioral data. That’s how RiskSeal identifies high-risk individuals before they even enter the formal application process.

This allows us to filter out up to 70% of risky applicants, saving valuable time and resources.

Stage 2: Actual credit scoring

The second stage where we apply data enrichment is during scoring, after the client has been onboarded and has an account.

When a client requests a loan, the credit organization needs to assess their creditworthiness in real time. Our enriched data is integrated here to provide a more comprehensive risk profile.

We supplement traditional credit bureau information with signals like:

- digital footprint

- ongoing subscriptions

- device usage patterns

- gambling activity

- location stability

These insights reveal whether a borrower maintains consistent payments, relies on risky behaviors, or shows long-term financial stability.

This second layer of data enrichment for smarter lending ensures a more accurate and nuanced credit decision. It leads to better outcomes for both the lender and the client.

Practical steps to onboard data enrichment services

Here's a step-by-step guide for risk management teams to onboard data enrichment for improving credit risk decisioning.

Step 1. Identify data gaps and objectives

First, your team needs to figure out what data is missing from your current credit assessment process. Ask yourself, what information would help you better understand an applicant's creditworthiness?

Once you've identified these gaps, set clear objectives. You may want to reduce default rates, increase approval rates for thin-file applicants, or improve the accuracy of your risk models.

Step 2. Research and select data enrichment companies

The market has many providers offering various types of data. You'll need to research and select providers that offer the data you need to fill the gaps identified in the first step.

Look for providers specializing in alternative data for credit risk decisions. Evaluate them based on the data quality, security, and cost of their service.

Ensure they comply with all relevant regulations, such as General Data Protection Regulation (GDPR).

Step 3. Integrate data and build predictive models

Integrating new data requires technical work.

You'll need to set up APIs (Application Programming Interfaces) to seamlessly pull data from the providers into your existing credit risk models.

This is often done in a testing environment first to avoid disrupting live operations.

After integration, your data science team will need to build or retrain predictive models using the enriched data. This involves:

- Feature engineering: Creating new variables from the enriched data.

- Model training: Using ML algorithms to find patterns and predict credit risk based on the new, enriched dataset.

- Backtesting: Testing the new models on historical data to see how they would have performed.

Alternatively, working with a trusted provider of B2B data enrichment services can simplify the process.

A specialized digital credit scoring company like RiskSeal can manage everything from proof-of-concept to data interpretation.

Our API-based architecture allows fast, reliable integration without burdening internal teams.

Step 4. Deploy and monitor

Once the new models have been thoroughly tested and validated, you can deploy them in your live credit risk decisioning system.

This should be a gradual process. Start with a small subset of applications to ensure everything works as expected.

Continuous monitoring is crucial. You'll need to track the performance of the new models over time, looking for signs of model drift or data degradation.

Regularly review the model's performance metrics, such as AUC (Area Under the Curve) and Gini coefficient, to ensure they are still providing an accurate assessment of risk.

This iterative process ensures that your data enrichment strategy remains effective and compliant.

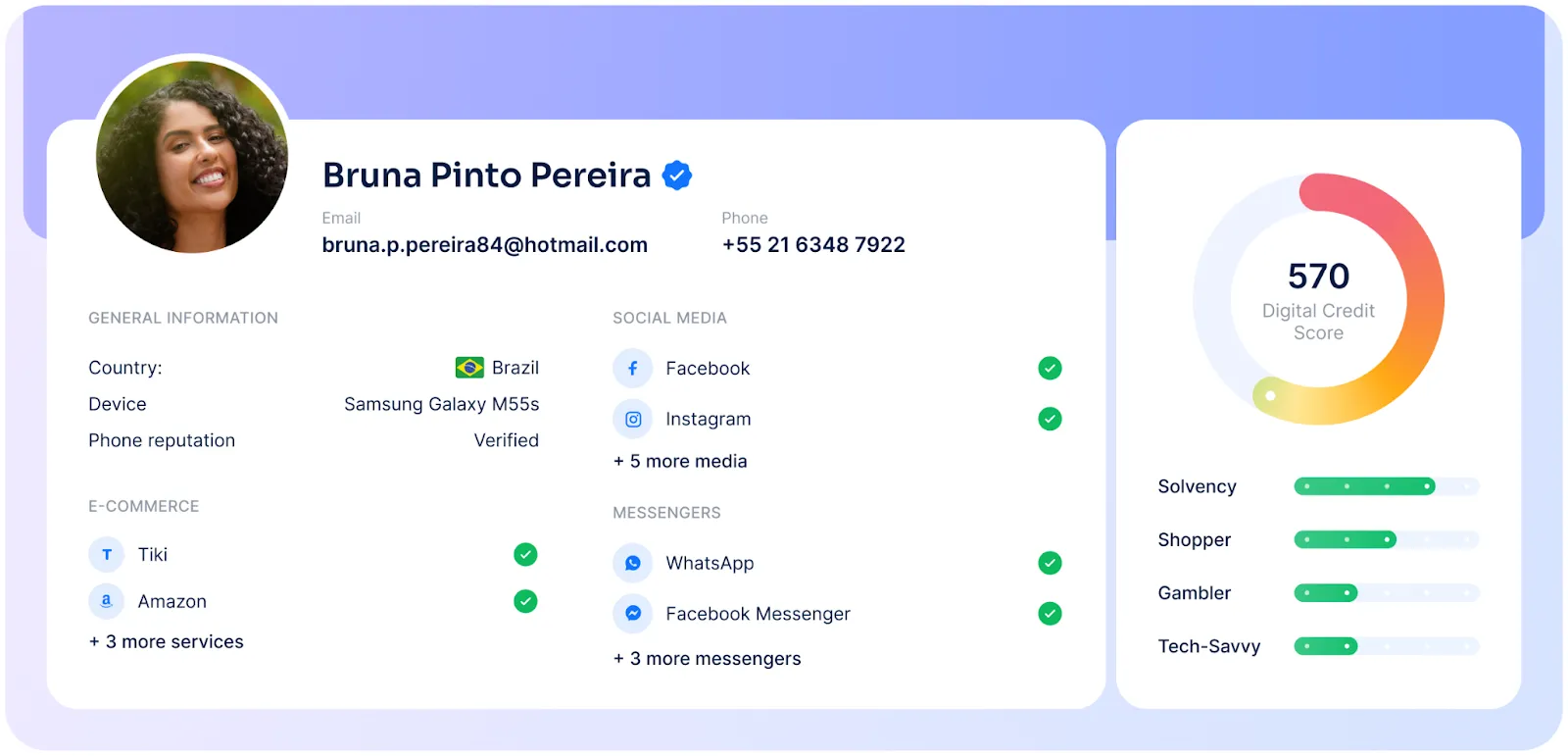

How to choose customer data enrichment sources

When lenders talk about “alternative data,” it means signals beyond credit bureau files.

These come from digital life, online behavior, and personal identifiers. The right mix of data sources helps credit risk teams see a borrower’s true profile.

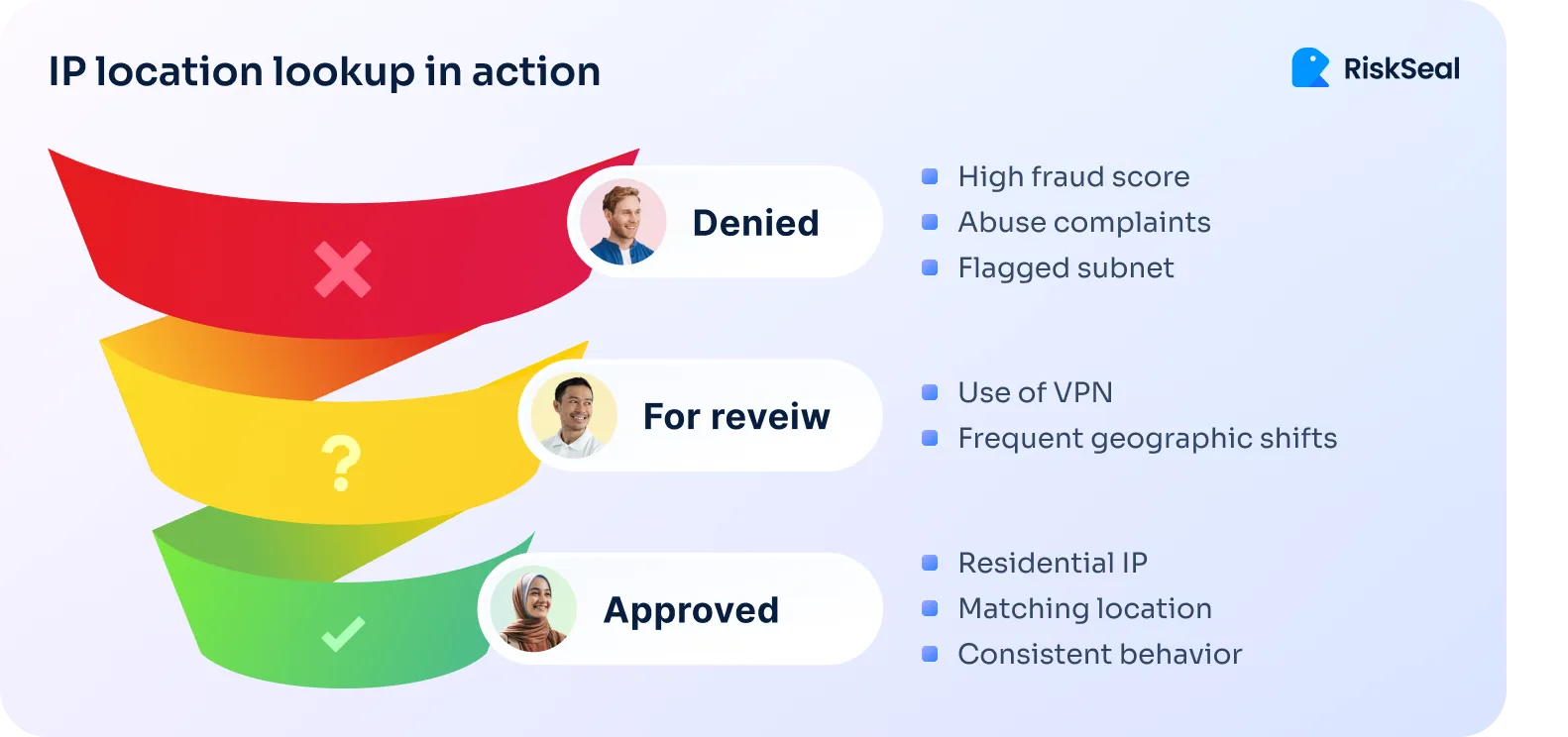

Identifiers as anchors

Identifiers are the basic details a borrower lists on their application. Like email, phone number, IP address, or device information.

An email address can show where a borrower is registered online, from social media to e-commerce. A phone number may reveal whether it is active, disposable, or linked to spam lists.

The IP address adds context. It can show if the user connects from a stable location, a residential network, or a data center. IP lookup also uncovers proxy or VPN use, which may signal higher risk.

Device metadata tells a usage story. A borrower who always uses the same smartphone or switches between one phone and a laptop looks trustworthy. Especially compared to someone cycling through multiple devices.

Behavioral insights

Behavior is one of the strongest predictors of repayment.

Subscriptions are a good example. A stable Netflix Premium or Spotify subscription may point to consistent disposable income.

In contrast, gambling subscriptions can be an early warning sign of financial stress.

Other useful insights include:

- Payment regularity: How reliably bills are settled.

- Online shopping habits: Frequent small purchases vs. erratic large ones.

- Subscription continuity: Keeping the same paid accounts over months or years.

These patterns reveal discipline, solvency, and lifestyle, often better than a static credit report.

Contextual signals

Context matters as much as behavior. Professional history helps lenders understand income potential and stability.

Geolocation stability shows whether someone lives and works in one area or constantly changes addresses.

A strong digital presence also adds trust. Social media accounts created years ago, with steady posting, reduce the risk of synthetic identities.

A complete and consistent online footprint is harder to fake.

Checklist: 5 data points to start with

For lenders new to alternative data, here are five high-value signals worth checking first:

Starting with these five creates a strong base for understanding borrowers beyond bureau data.

.svg)

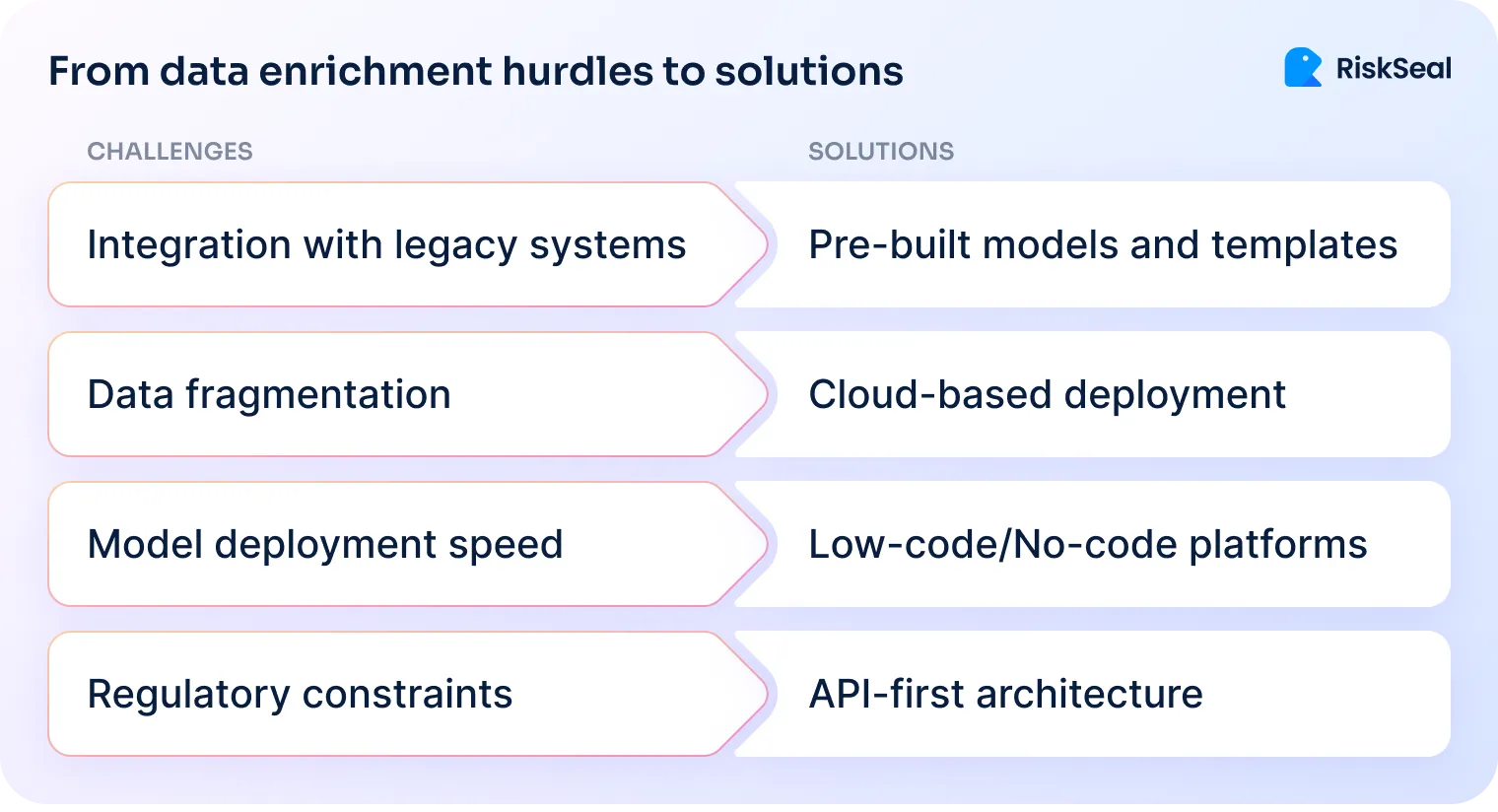

Common pitfalls in data enrichment and how to avoid them

Let’s look at the common mistakes that can derail even the most advanced strategies. And best practices for enriching scoring models while avoiding these mistakes.

Pitfall 1: Treating enrichment as a one-time project

Enrichment is not a “set it and forget it” exercise. Data sources, fraud tactics, and borrower behavior change constantly. Static models quickly lose value.

What to do: The best way to avoid this trap is to recalibrate models frequently.

Enrichment updates should be synchronized with the model lifecycle and feature revisions. That way, the data stays fresh and aligned with real borrower behavior.

Pitfall 2: Overloading models with too much data

Adding every possible data source can create noise instead of insight. Lenders risk building models that are complex, slow, and hard to explain.

What to do: A safer approach is to start small. Pilot tests on a limited set of data points help validate each source’s contribution before scaling.

At RiskSeal, we support this process by offering free proof-of-concept tests, so lenders can see the real impact of enrichment before committing.

Pitfall 3: Ignoring compliance and transparency

Black-box models make lenders vulnerable to regulatory pushback. If decisions can’t be explained, trust and compliance suffer.

What to do: The solution is to use white-box AI that keeps decision logic transparent and outcomes explainable.

At RiskSeal, we make every step of the decision path open and easy to interpret. This way, we’re helping lenders stay fully compliant while maintaining customer trust.

Pitfall 4: Skipping integration planning

Some lenders try to bolt enrichment onto existing systems all at once, leading to delays and inefficiencies.

What to do: The more effective route is modular integration. An API-first setup allows lenders to roll out enrichment step by step.

It focuses first on the areas with the biggest impact before expanding to the rest of the workflow.

Practical benefits of data enrichment tools for risk teams

Data enrichment brings real, measurable improvements to lending operations. It drives growth, improves efficiency, and strengthens protection against fraud.

Portfolio growth without higher risks

Enriched signals help lenders more safely approve thin-file borrowers. Globally, about 1.4 billion adults are unbanked and lack formal credit history. This makes alternative data essential for extending access to fair credit.

Use case

A mid-sized lender integrated RiskSeal’s enrichment into its scoring models.

By adding behavioral and contextual signals, it doubled approvals among borderline applicants while keeping default rates flat.

The portfolio grew faster, but risk exposure stayed the same.

Fraud red flagging at speed

Fraudulent applications often share telltale signs: temporary emails, suspicious IP addresses, mismatched devices.

Enrichment tools make it possible to catch these anomalies in seconds. Before the loan request even reaches underwriting.

Use case

A digital-first neobank introduced early fraud detection using enriched identifiers.

Within six months, it cut default rates by up to 25%. Simply by screening out bad actors at the start of the workflow.

Operational efficiency

KYC checks are expensive and resource-heavy.

By enriching data at the pre-KYC stage, lenders can filter out high-risk applicants before triggering full compliance processes. This helps saving both cost and time.

Use case

A microfinance organization integrated RiskSeal enrichment to pre-screen applications.

Up to 70% of risky profiles were filtered out before KYC. This saved significant compliance costs and freed staff time for quality applicants.

Customer experience edge

Borrowers expect fast, digital-first service. Data enrichment platforms make instant approvals possible by delivering actionable results within seconds.

This speed doesn’t just reduce friction. It becomes a competitive advantage.

Use case

An online lender reduced its credit decisioning time from hours to less than 30 minutes by using enrichment signals in API-based scoring.

RiskSeal delivers alternative data in under 5 seconds per borrower, giving risk teams the inputs they need instantly. This speed allowed the lender to streamline onboarding and turn faster approvals into a competitive advantage.

Data enrichment at RiskSeal

At RiskSeal, we help credit providers enrich their risk models with alternative data in a frictionless, scalable way.

Our API integrates seamlessly with your CRM, so onboarding is fast and staff training is minimal.

We also offer a proof of concept (PoC), where lenders can test enrichment on real-life credit risk outcomes.

The results are compared with and without enrichment across thousands of applications. This clearly shows the impact before you commit.

After go-live, RiskSeal becomes a long-term partner, not just a tool. Your risk team gains:

- Regular performance reviews and score optimization

- Access to new enrichment sources and features

- Strategic guidance and continuous technical support

Use cases include credit decisioning, risk assessment, identity verification, debt collection, and fraud detection.

Key takeaways on what is data enrichment

Use data enrichment as a practical tool to strengthen credit risk models and workflows.

- Pilot enrichment on a limited dataset, validate impact, then scale across the portfolio.

- Use API-first modular rollouts to plug enrichment into scoring without disrupting existing systems.

- Keep models explainable for compliance, and recalibrate often as borrower behavior and fraud tactics evolve.

Data enrichment works best when applied step by step, with clear goals and measurable results.

Want to see how this looks in practice? Book a demo with RiskSeal and test enrichment on your own portfolio.

See more

Discover global lending trends that can shape credit scoring strategy for successful financial inclusion.

.webp)

Understand the crucial aspects fintech providers need to focus on to ensure successful and relevant PoCs.

Alright, you've changed your scorecards by using alternative data. How can you check if they work well? What metrics you should measure? Check out the article.