How Alternative Credit Scoring Is Driving Financial Inclusion in Emerging Markets

Discover how expanding financial inclusion and lending to overlooked borrowers can drive profits and transform lives around the world.

.webp)

Many creditworthy individuals around the world remain underserved, unable to access loans from banks. The reason is that they have no credit history, which traditional credit scoring relies on.

To avoid losing a significant share of profit, lenders need to identify reliable borrowers among thin files and open up the possibility of lending to them.

Read on to learn how to optimize credit risk assessment. By identifying overlooked borrowers, lenders can grow portfolios and drive profitability.

What is financial inclusion, and why does it matter?

Financial inclusion means providing the unbanked population access to essential financial services, including lending.

Expanding access to financial services brings huge benefits, both to individuals and businesses.

As a result, people, regardless of their region of residence, can fully participate in the financial system.

Lenders, in turn, can significantly expand their target audience by reaching creditworthy borrowers who do not meet the requirements of financial organizations with traditional risk scoring.

.svg)

.webp)

How lending access transforms lives in developing countries

Financial inclusion is not just about people having access to bank accounts or loans.

It is a powerful tool for economic development and social equality.

To illustrate the importance of global access to lending, let us turn to official statistics:

Barriers to education for youth in developing countries

According to UNESCO, 20% of young people in developing countries do not have access to education. The main reasons cited are extreme poverty and living in rural areas.

This is quite logical. Low incomes do not allow them to pay for their studies. Limited access to physical bank branches prevents them from obtaining student loans.

Poverty in developing countries limits even basic needs

World Bank statistics show that in 2024, 692 million people were living below the poverty line, on $2.15 a day.

Most of these people live in developing countries, particularly in the Asia-Pacific region and Africa.

In other words, they do not even have the means to meet their basic needs. Talking about purchasing household appliances, electronics, and so on is completely out of the question.

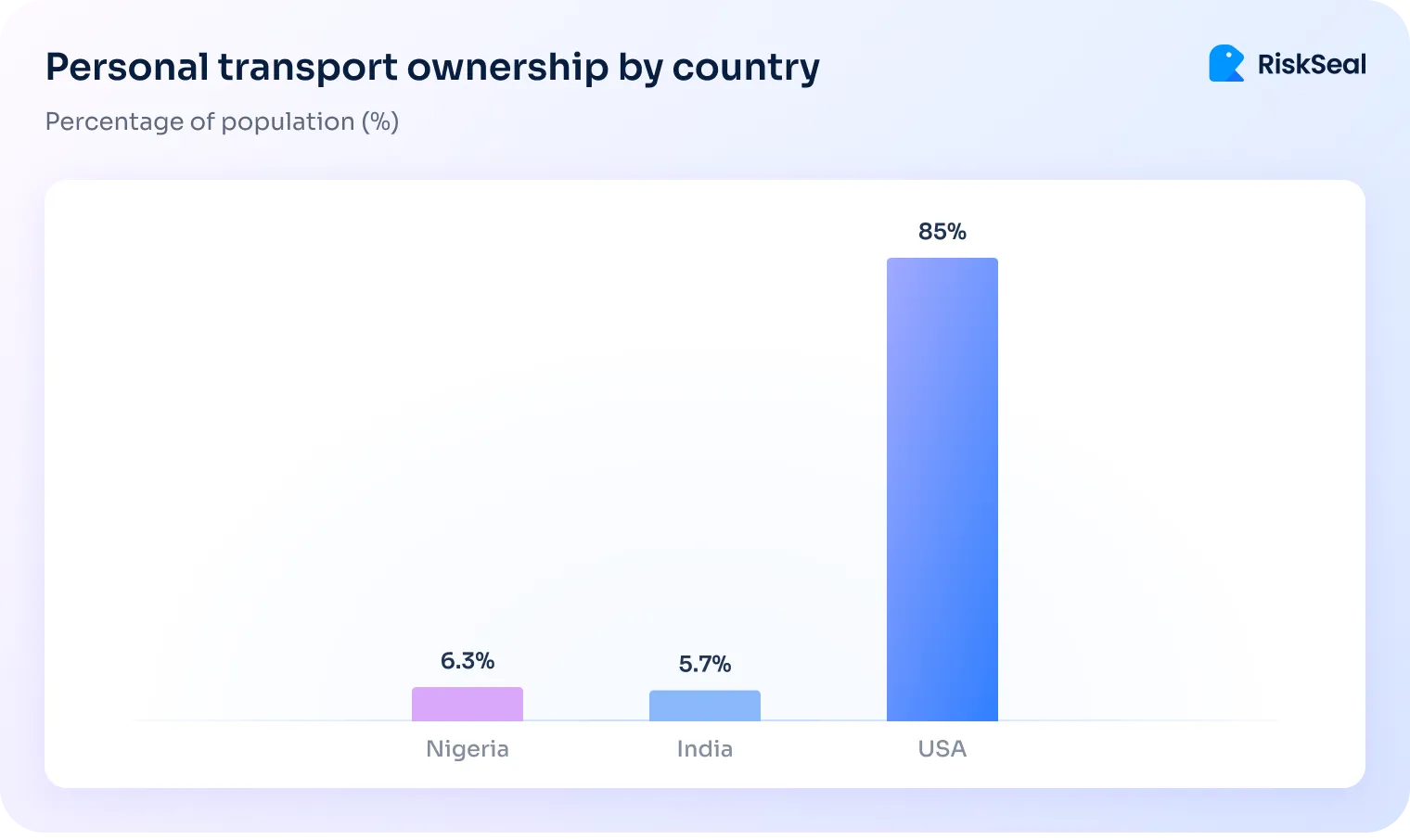

Car ownership is rare in developing countries

The results of recent studies show that very few people in developing countries can afford a car.

For example, in Nigeria, only 63 out of 1,000 people (6.3%) own personal transport. In India, 57 out of 1,000 (5.7%).

By comparison, in the United States, 85% of the population owns a car, and in many European countries, the number of cars exceeds the number of residents.

Financial inclusion trends in emerging markets

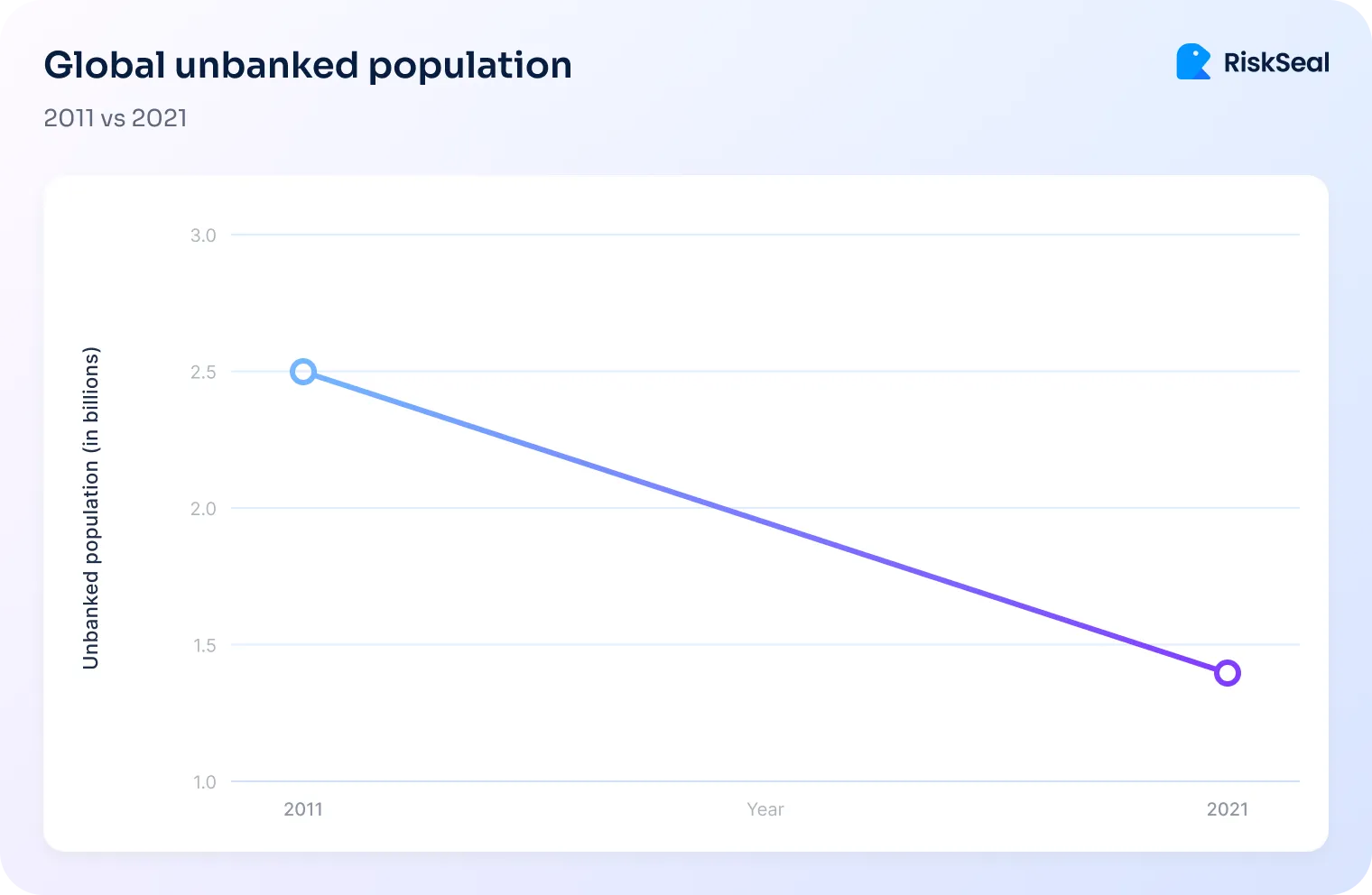

Financial inclusion in developing countries is showing positive dynamics.

According to the World Bank, over the past 10 years, the number of unbanked individuals worldwide has decreased by 1.1 billion:

Let us look at the key financial inclusion trends observed in developing countries.

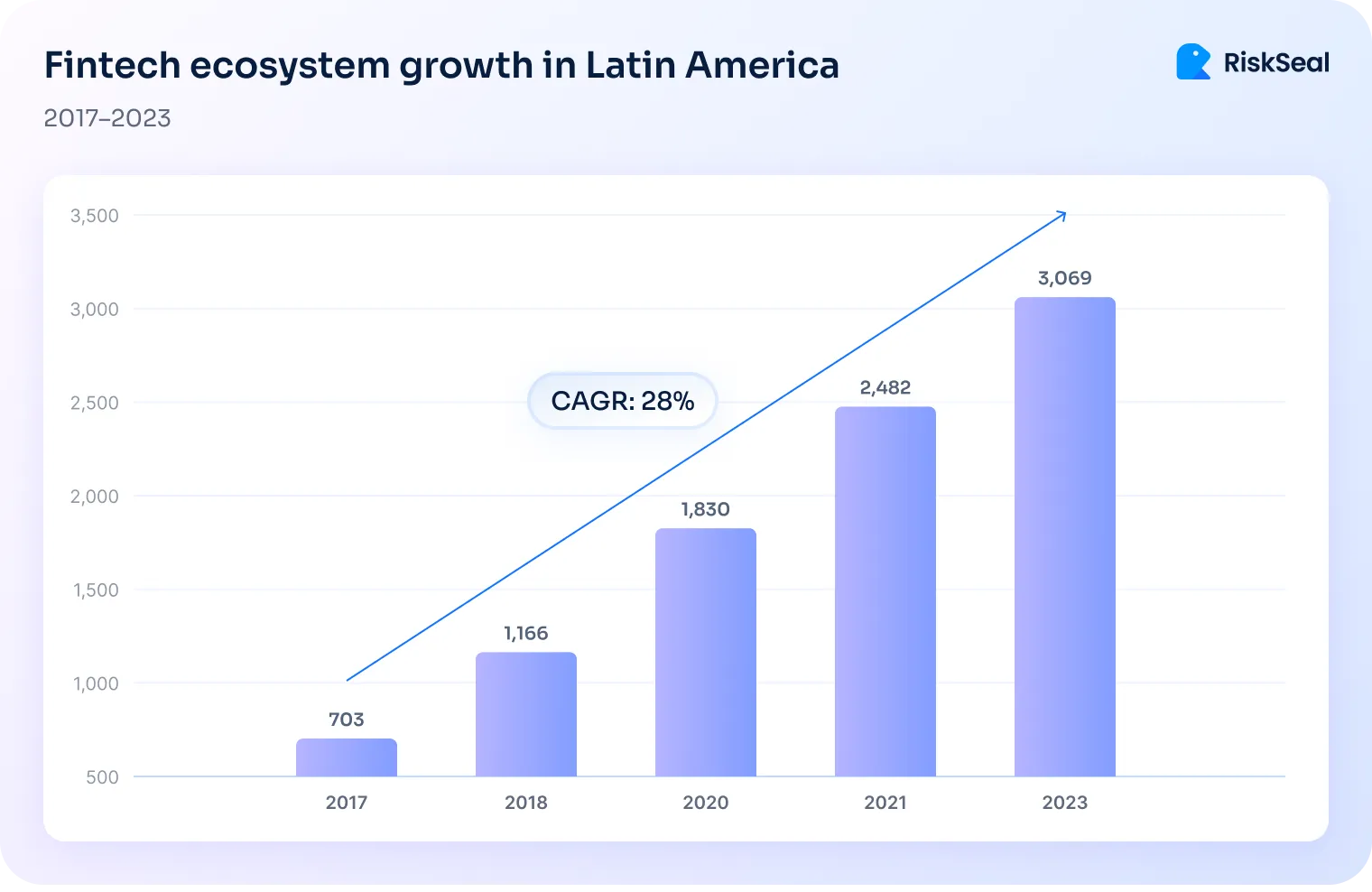

LATAM financial inclusion

LATAM is experiencing a true fintech revolution.

According to official data, over the past six years, the industry in the region has grown by 340%:

Indeed, many countries in this region are seeing the emergence of companies offering digital banking services to populations that previously had no access to the financial system. Among them are Nubank in Brazil and Ualá in Argentina.

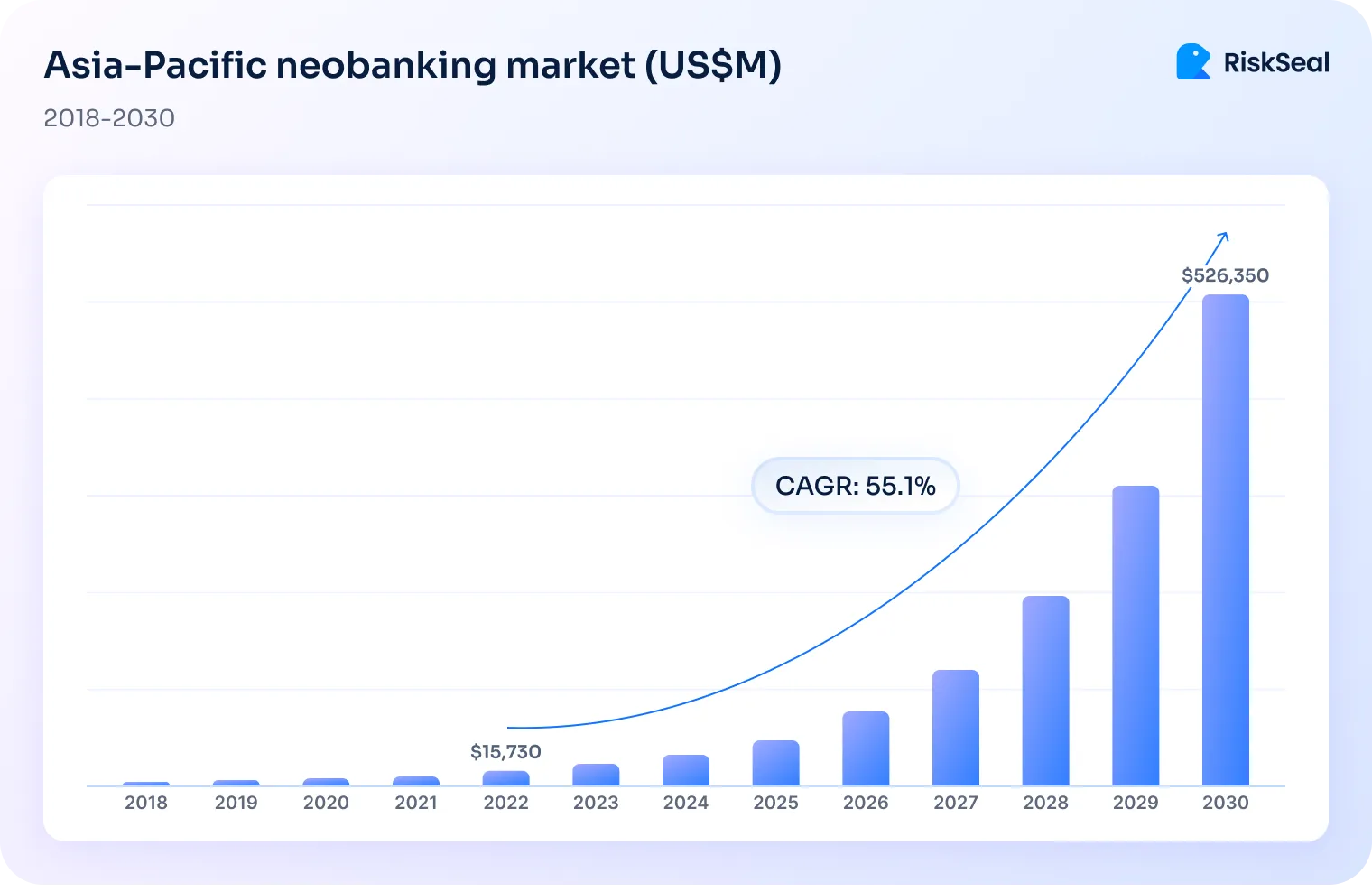

APAC financial inclusion

In the APAC region, financial inclusion is expanding rapidly, driven by the growth of microcredit and the emergence of neobanks.

While in 2022 the neobanking market in this region was valued at $16 billion, by 2030 it is projected to grow to $526 billion:

The same trend is observed in the microcredit market. It is expected to show a CAGR of 13.1% over the next three years, reaching $7 billion by 2028.

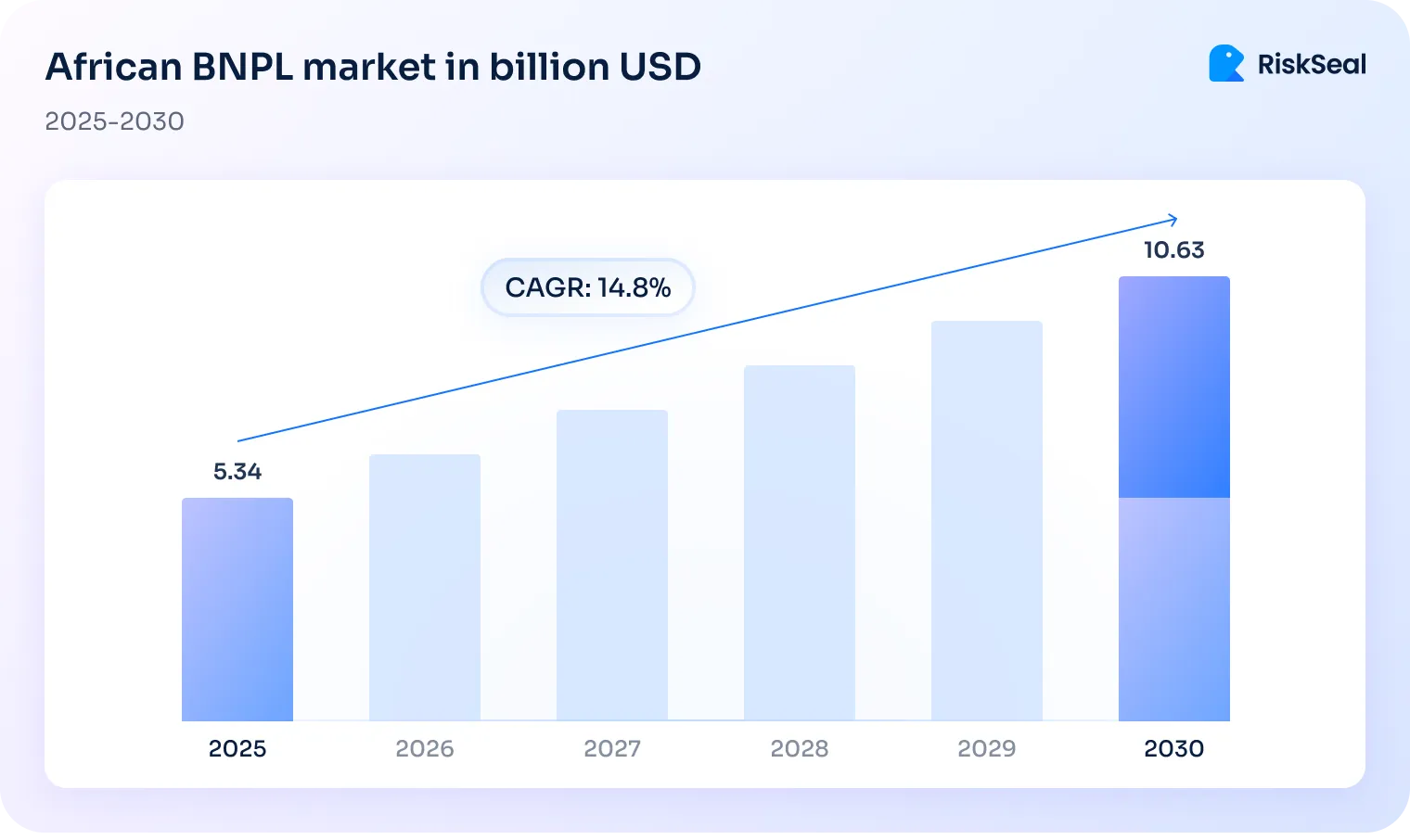

Financial inclusion in Africa

The financial sector in Africa is going through big changes, with alternative lending becoming more and more popular.

In particular, BNPL services, P2P lending, payday lending, etc., are in high demand among users.

As for the P2P lending market in this region, it is projected to show a CAGR of 10.2% in the coming years. By 2031, its volume will reach $4.5 billion.

The BNPL services market is developing even faster. While it is currently valued at $5.3 billion, by 2030 it is projected to almost double:

Barriers to financial inclusion

Despite generally positive dynamics, including in developing countries, financial inclusion still faces several obstacles.

Lack of access to traditional financial services

Many potential borrowers are unable to get a loan from traditional banks due to the lack of a credit history.

Fintech lenders also cannot serve thin files by relying only on traditional data.

However, there is a solution - turning to alternative credit scoring, which becomes possible with a progressive data enrichment solution.

Fraud risk in emerging markets

Another top priority for lenders is fraud prevention in emerging markets. It has become one of the biggest challenges for credit scoring fintech companies expanding in high-growth regions.

Criminals take advantage of financial institutions’ desire to expand the accessibility of their services, increasing the number of attempts to make fraudulent deals.

According to recent data, the number of fraud cases in Africa rose by 393% in 2024, and in Latin America, by 255%.

Common fraud schemes include synthetic identity fraud and document forgery.

Low financial literacy of the population

This leads to people in developing countries easily falling victim to criminals.

In particular, they suffer from data leaks and theft of personal information through phishing attacks.

This contributes to an increase in credit risk, since all illegally obtained data can be used to apply for fraudulent loans.

Case study: increasing financial inclusion in Mexico

RiskSeal has a successful track record of cooperation with the Mexican fintech company AvaFin.

The lender came to us because they saw a big opportunity to offer credit to people without access to traditional banking. But without an alternative way to assess creditworthiness, they couldn’t take full advantage of that opportunity.

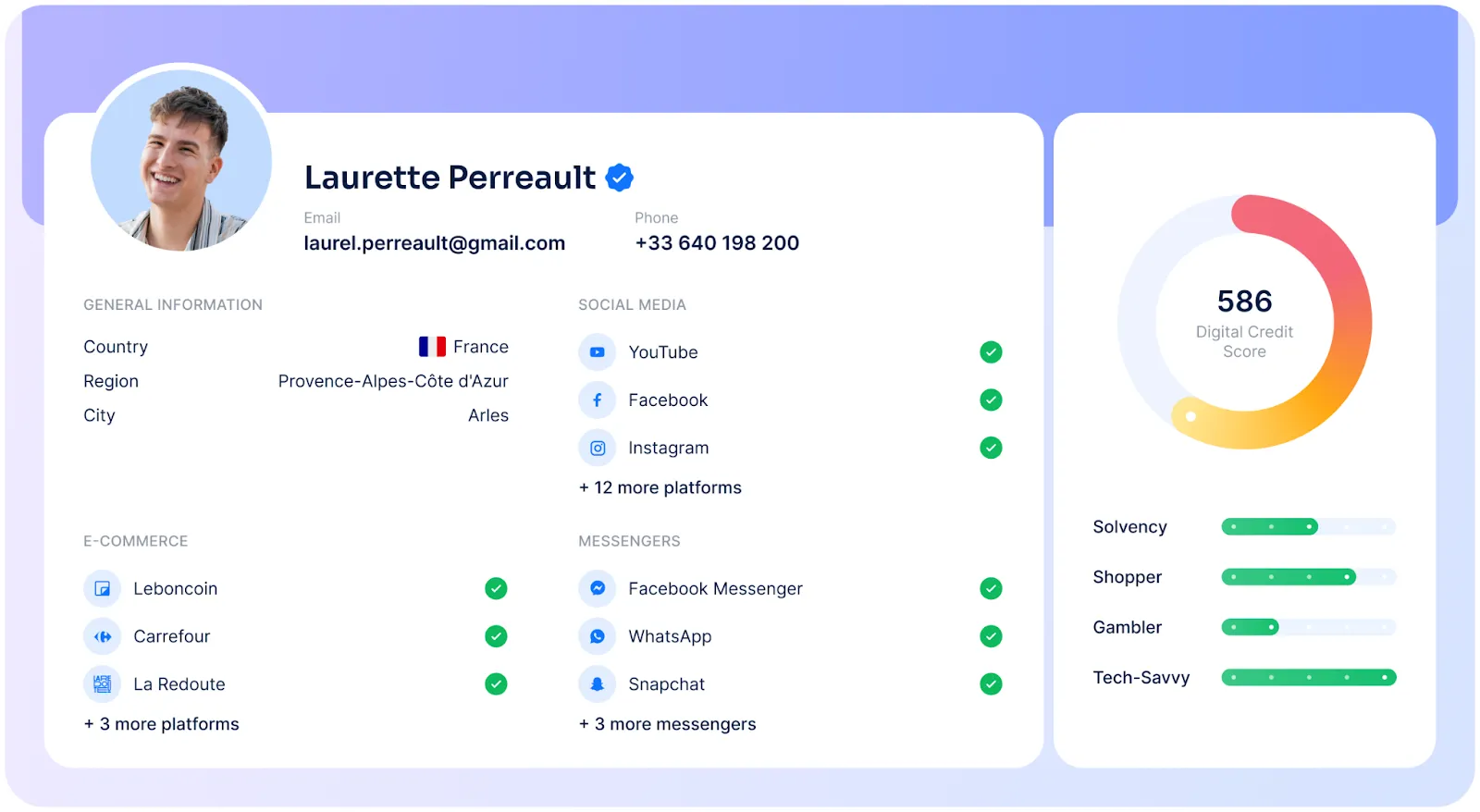

As a result of using RiskSeal Digital Credit Scoring platform, AvaFin gained access to the following data:

- Information from social networks (social media profiling) and other online resources.

- Email data (estimated creation date, mailbox activity, blacklisting, data breach incidents, etc.)

- Phone number data (use of disposable numbers and virtual SIM cards, number activity, fraud incidents, spam messaging, etc.)

- Information obtained from applicant identity verification (name matching, face recognition, and geolocation verification).

Based on the results of our cooperation, the client noted the high effectiveness of credit risk assessment and the significant predictive power of the RiskSeal scoring model.

With RiskSeal’s data, AvaFin was able to issue more loans. This became possible due to the assessment of the solvency of applicants who are “invisible” to traditional banks.

How RiskSeal promotes financial inclusion

RiskSeal is a digital scoring platform that provides access to creditworthy borrowers through alternative data for banks and fintech companies.

How can RiskSeal help a lender increase the number of approved applications?

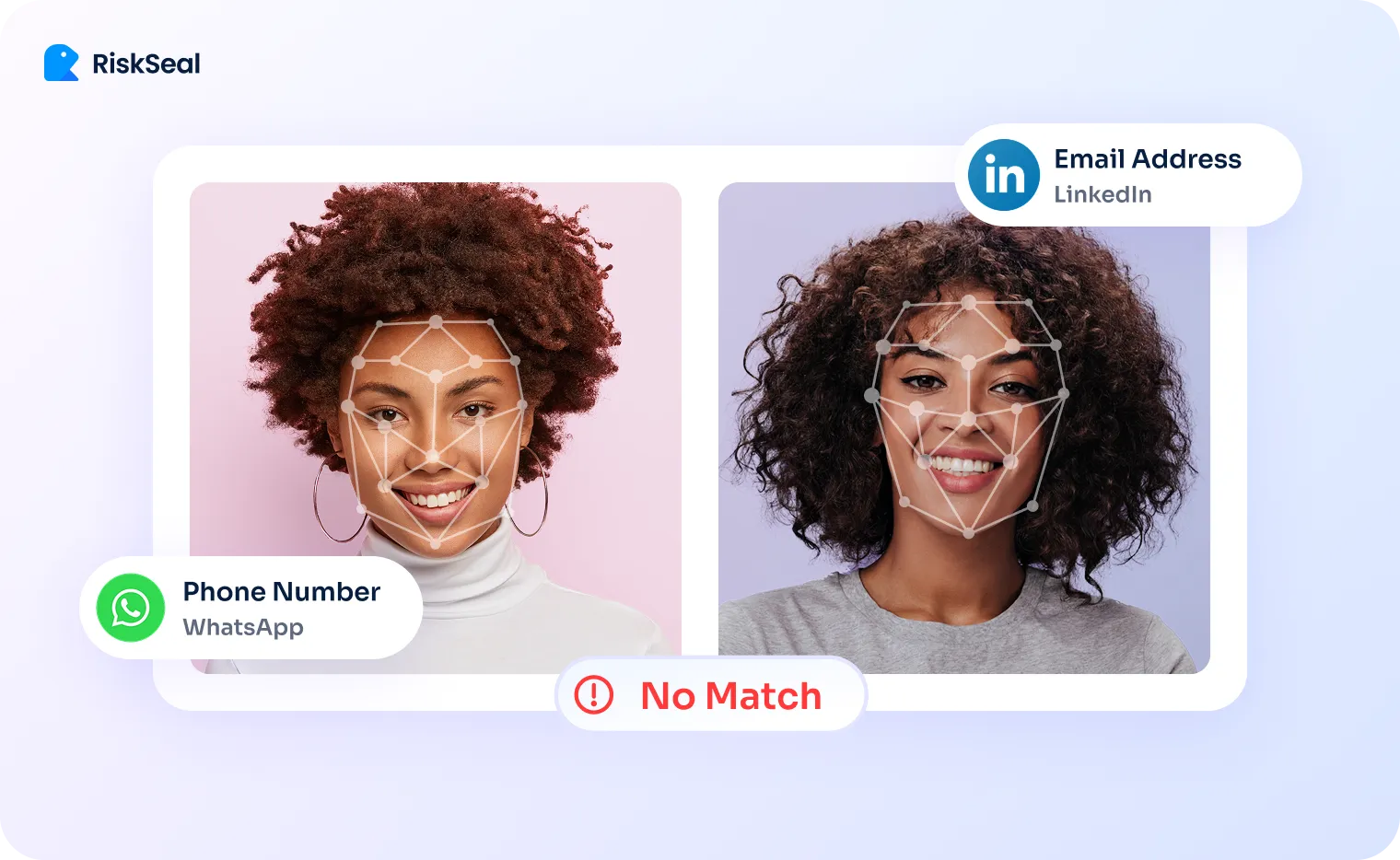

Digital identity verification. With the help of innovative technologies, we achieve reducing onboarding friction while ensuring security.

These technologies include face recognition and name matching. The former compares borrower photos from various online accounts, while the latter matches user names across public sources.

Any discrepancies detected in the process of digital credit scoring should be a reason for the lender to suspect fraud.

Alternative data for credit risk scoring. RiskSeal is a reliable alternative data provider specializing in analyzing the digital footprint of potential borrowers.

We return over 400 data points about applicants, allowing our clients to create a comprehensive financial profile of an individual.

Examples of non-traditional data you'll receive include email lookup, phone number lookup, location data, and even using social media for credit scoring to assess an applicant’s reliability.

Continuous fraud monitoring. Our platform applies AI in credit risk management. Reliable algorithms can analyze user behavior and detect unusual patterns, allowing lenders to strengthen fraud detection while speeding up approvals.

To do this, RiskSeal applies specialized methods, for example, geolocation checks and behavioral analysis. The former involves comparing the address stated by the applicant with geolocation data.

The latter helps identify suspicious borrower behavior, such as a sudden change in spending habits, logging in from an uncharacteristic device, and more.

Final thoughts

Turning to alternative data providers like RiskSeal is one of the key trends in credit scoring.

These platforms help lenders give out more loans and increase their profits. They also make financial services available to people without bank accounts.

To keep lending services safe and compliant, fintech companies, regulators, and alternative data providers need to work closely together.

Want to learn how RiskSeal helps financial institutions balance inclusion and security? Contact us for a demo.

See more

Explore how to spot high-risk borrowers. Discover key red flags, alternative credit scoring, and risk mitigation strategies.

Discover why traditional credit models miss Gen Z borrowers and how alternative data helps lenders score them accurately.

.webp)

The development features of the lending sector in India and the role that alternative credit scoring plays in it.