Explore how fraudsters exploit disposable phone numbers for loan scams and how phone lookup helps lenders prevent financial fraud.

.webp)

Why might someone need a disposable mobile number (DPN)?

Among legitimate purposes are protecting personal privacy, running short-term business projects, traveling, and other situations where using a primary number is undesirable or impossible.

Aside from that, disposable numbers are often used by fraudsters to carry out their criminal schemes, including in the financial sector.

Lenders must pay maximum attention when verifying borrowers with such contact details.

The modern telecommunications market offers users various types of disposable cell numbers.

These numbers are valid for a limited period, typically from a few hours to a few days.

They are ideal for one-time interactions, such as SMS verification, including for loan applications.

These are inexpensive gadgets for temporary use that users can easily throw away - “burn.”

Burner phone numbers usually have no contract with a mobile operator, offer limited features, and come with prepaid minutes.

This is another go-to option for financial fraudsters. After securing a fraudulent loan, they can simply discard the phone along with the SIM card.

These numbers operate through cloud services and are not tied to a specific device or SIM card.

This operating principle makes it difficult to identify the user, which can be effectively exploited by fraudsters.

Virtual SIM cards, so-called eSIMs, are also gaining popularity. From 2022 to 2032, this market is projected to grow from $8 billion to $20 billion:

VoIP telephony uses the internet for calls and SMS instead of traditional phone networks.

Acquiring such a number does not require strict identity verification, making them popular among fraudsters for illegal activities.

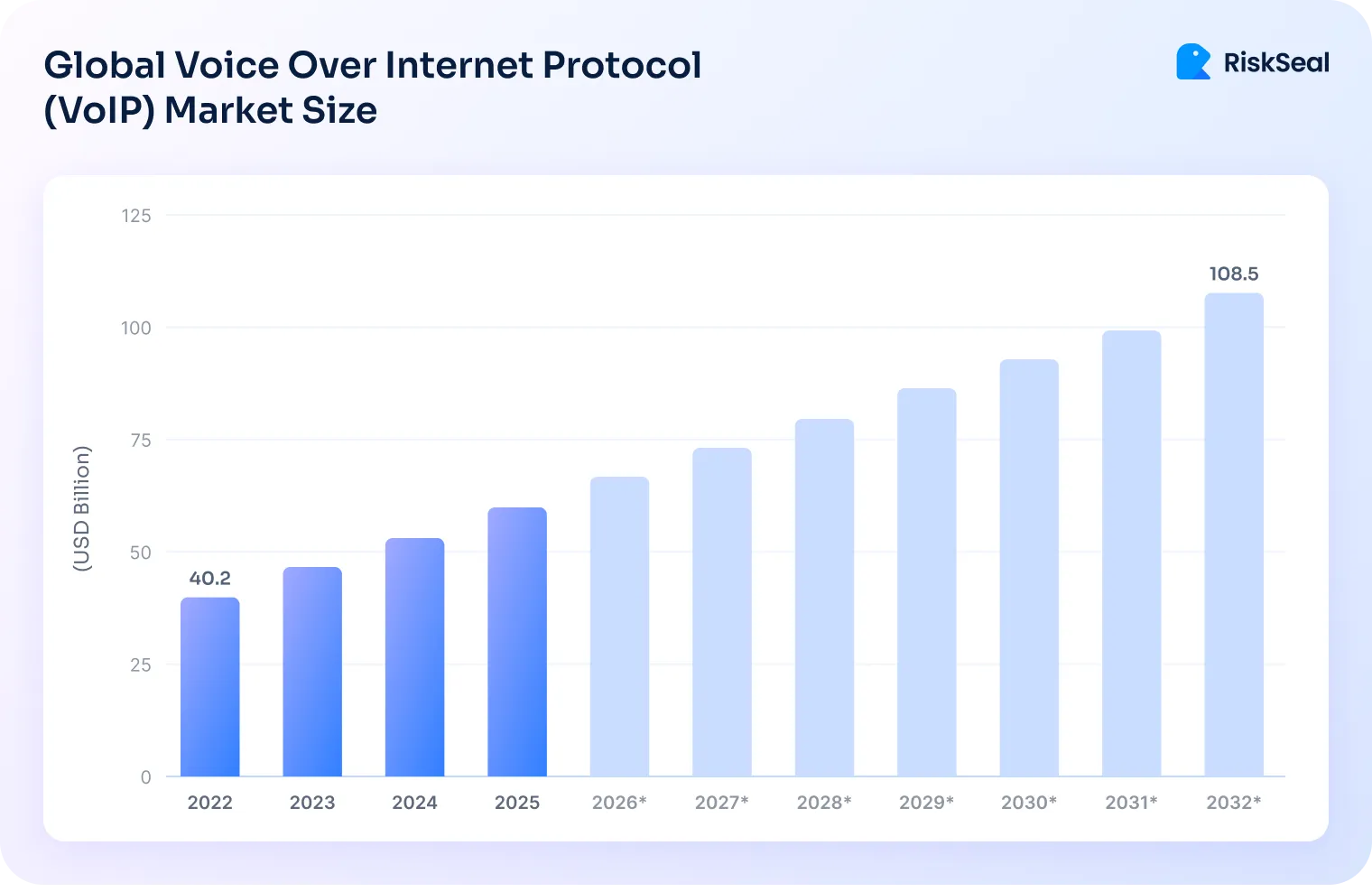

The VoIP Market was valued at $40 billion in 2022. Experts predict that by 2032, this figure will grow to $108 billion:

These are disposable numbers that forward calls and messages to a primary number while keeping it hidden.

This is one way to mask identity, allowing criminals to remain anonymous during financial fraud.

These are publicly available virtual numbers that allow receiving SMS messages.

They are often used for SMS verification or registration on various platforms.

While they can be used for legitimate purposes, like protection from spam and data leaks, fraudsters often use online SMS numbers to hide their real number.

These are phone numbers with prepaid credit, used without signing a contract with a mobile provider.

Such numbers can be purchased without identity verification, which fraudsters take advantage of.

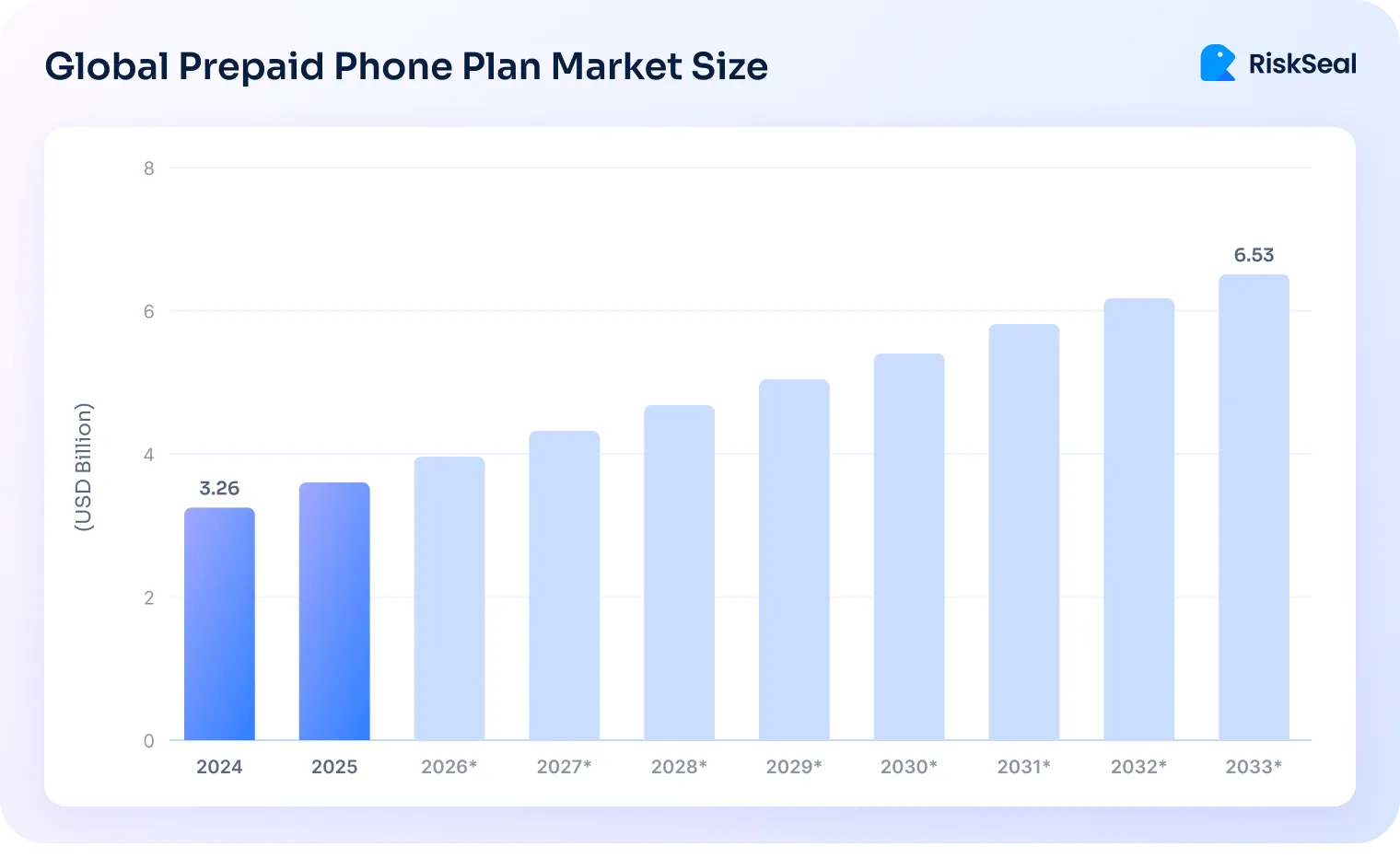

The Global Prepaid Phone Plan Market is also growing. In 2024, it was valued at $3 billion. By 2033, the market is expected to double, to $6 billion:

Users are increasingly choosing prepaid SIM cards over signing contracts with mobile operators.

The feature of such numbers is that they are used without being linked to a specific person.

They can be temporary or virtual, but the main point is that you will never know who they belong to.

Their registration does not require identity verification. This, once again, allows fraudsters to commit illegal actions with impunity.

As the name suggests, such numbers are used only once, for example, for a single call or SMS. After that, they are automatically deleted.

This is an excellent option for financial fraudsters.

They can use such a number to contact a credit organization, after which it will be impossible to reach them again.

This type of number is specifically designed to receive verification codes when registering on various services.

They are publicly available and do not require logging in to be used.

In short, exactly what criminals need to register on digital lending platforms.

Fraudsters are increasingly exploiting DPN services for criminal activities.

This fact is well illustrated by the study “Your Code is 0000: An Analysis of the Disposable Phone Numbers Ecosystem.”

In it, based on an example of a well-known fintech application that offers microloans, the following was established: the service sent confirmation messages for fund disbursement to at least 131 different disposable mobile numbers.

Potentially, each of the recipients could have been a fraudster who illegally obtained a loan.

Financial fraudsters are becoming more and more inventive every day.

We’ll highlight the most common types of loan fraud, which alternative data providers like RiskSeal can help prevent using credit scoring powered by phone number lookup.

Disposable phone numbers are often used to create synthetic identities. These are non-existent individuals who are assigned a mix of real and fabricated data.

Such combined profiles can later be used for various criminal purposes, including applying for loans.

This type of fraud is very common.

According to Experian, in 2023, 34% of companies whose executives participated in the survey experienced identity theft.

A similar situation is seen with synthetic fraud: 32% of respondents reported such attacks.

Synthetic fraud example: A fraudster purchases a disposable cell number and links it to a synthetic identity. Then they apply for several loans, after which they disappear.

The lender is stuck with bad transactions that will never be repaid.

Fraudsters may provide disposable numbers as contact information in a loan application. This prevents the lender from verifying the applicant’s identity, employment, and other data important for assessing creditworthiness.

Example of a loan application fraud: A criminal applies for a payday loan. In the application, they provide a disposable number and false employment information.

Without access to the borrower’s real phone number, the lender cannot verify the accuracy of the information.

As a result, they may approve the loan based on fabricated data.

Fraudsters may use disposable mobile numbers to bypass multifactor authentication.

This allows them to take over legitimate users’ loan accounts.

What happens next? After gaining control over the account, they can redirect loan payments or change account details to seize the funds.

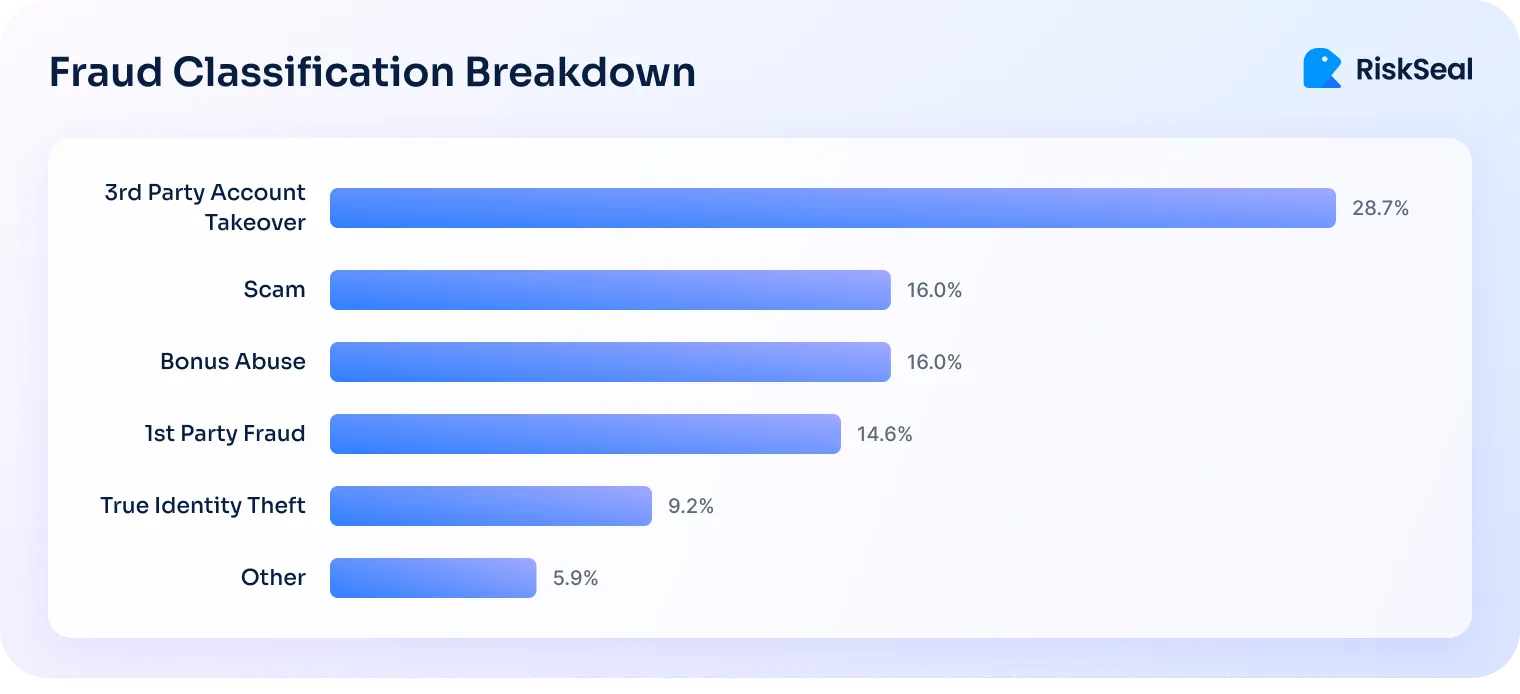

Account takeover fraud is also very widespread globally. According to statistics, this scheme accounts for nearly one-third of all fraudulent attacks:

Example of an account takeover fraud: A fraudster contacts the support service of a digital lending platform and requests to change the phone number.

By replacing the number provided by the real client with a temporary one, they gain access to the account.

After that, they can perform any manipulations with the funds.

This type of fraud happens when someone applies for several loans at once without telling the lenders about other applications.

Using a disposable phone number makes it easier for fraudsters to carry out this scheme.

After all, lenders cannot detect parallel applications and end up approving loans that are knowingly bound to default.

Example of a loan stacking fraud: A borrower uses a one-time number to submit several payday loan applications within a short period.

They receive the requested payouts because lenders are unable to track their activity.

To identify disposable cell numbers, lenders turn to alternative data providers who specialize in digital footprint analysis. One such provider is the credit scoring system RiskSeal.

With their help, lenders gain a wide range of capabilities:

1. Data enrichment. Knowing the applicant’s phone number, the lender can access the following data: information from social media profiles, email metadata, and results from IP address analysis.

All of this information can be used to enrich the scoring model, increase the accuracy of credit assessment, and detect fraud.

2. Behavioral analysis. Digital footprint analysis makes it possible to identify suspicious behavioral patterns related to phone number usage.

For example, it may be suspicious if multiple accounts are linked to a single number.

Fraud may also be suspected if there is a large volume of calls in a short period or if patterns of international calls are detected.

3. Reverse lookup and cross-referencing. Reverse phone number lookup API connects risk teams to trusted databases for verifying the legitimacy of phone numbers and detect disposable or fraudulent ones.

Lenders can also identify disposable number providers by cross-referencing databases.

4. Machine learning and AI applications. AI-based scoring platforms use predictive models to flag potential disposable numbers.

Good results are shown by using historical data to train models to detect fraud patterns.

In the practice of the alternative data provider RiskSeal, there is a successful case of phone lookup integration into the credit scoring model of the financial company Clicredito MX.

The company approached RiskSeal to broaden its customer base by offering credit to Mexico’s unbanked population.

However, evaluating the creditworthiness of these individuals posed a significant challenge due to limited traditional financial data. Recognizing this gap, our client saw an opportunity to leverage alternative data sources, such as digital footprints.

Alongside other checks, the company actively verified the phone numbers of potential borrowers.

These checks allowed Clicredito MX to enrich its scoring models with the following data:

The lender successfully combined the obtained data with information from credit bureaus and achieved the following results:

The use of a disposable mobile number can be a potential indicator of fraud. Criminals may use it to hide their real contact information and prevent identification.

A phone verify lookup allows lenders to instantly confirm whether a number is disposable or risky, helping detect fraud attempts during loan applications.

With its help, lenders can improve the quality of their credit portfolio by reducing default rates and the number of fraudulently issued loans.

Explore the role of face match technology in the lending industry and examine its effectiveness in credit risk management.

.webp)

Discover proactive tactics to detect fraud early with alternative data sources and real-time behavioral insights.

Explore the most prevalent fraud schemes in P2P lending and the crucial role of digital footprint analysis.

.svg)

.webp)