Financial Fraud Prevention Using Digital Footprint Analysis

Identify the growing threat of financial fraud, explore its impact, and discover how digital footprint analysis helps prevent fraudulent activities.

Financial fraud is a serious problem for modern credit organizations. Traditional credit scoring models cannot fully protect lenders from criminals who try to apply for a loan with the original purpose of not repaying it.

Lenders are increasingly turning to assessing potential borrowers by analyzing their digital footprints.

At RiskSeal, we work closely with financial institutions to provide them with effective fraud prevention solutions. In this article, we’ll explain the different types of fraud in the fintech industry and how it can be prevented with the help of digital footprint analysis.

The growing problem of financial fraud

Financial fraud is an illegal act done to gain money or benefits. It covers areas like insurance, taxes, and investments. Our focus will be on credit fraud.

The fact that the problem of financial fraud is relevant for credit organizations is evidenced by disappointing statistics.

Financial organizations' losses due to fraud are impressive. According to Alloy, only 3% of respondents have not experienced a financial scam. The rest have lost significant sums in the past year.

Global companies are increasingly focusing on financial fraud prevention and detection (FDP). This is direct evidence of the seriousness of the problem.

According to Markets and Markets analysis, the global FDP market is estimated to be worth $28.8 billion in 2024, while it is forecast to grow to $63.2 billion by 2029.

This trend can be seen in the chart below.

These data show that the problem is significant and needs to be addressed. You can read more about financial fraud prevention methods in our material.

Key types of financial fraud

Credit fraud can take many forms, targeting individuals, businesses, or financial institutions.

Loan fraud

This type of financial fraud occurs when someone deliberately provides false information to get credit they don't qualify for.

Such actions include providing incomplete, false, or misleading information to a lender to manipulate the loan application approval process.

To illustrate the extent of the issue, let's look at mortgage fraud statistics.

According to current data, in 2023, home loan companies saw an increase of more than 34% in monthly fraud attempts. Half of these were successful, meaning the loan was granted to criminals.

Identity theft

There are several types of such fraud:

Account takeover. Fraudsters gain access to the victim's credit account through identity theft. This allows them to make unauthorized transactions.

Application fraud. Criminals use stolen identities to open new credit accounts. In this case, the real account holder is responsible for applying for credit.

Identity theft has reached unprecedented levels in recent years. According to Surf Shark, on average, each email account is hacked three times during its lifetime.

Statista analysts claim that in 2023 alone, nearly 40.5 million consumers will suffer account takeover by fraudsters.

Loan stacking

This type of fraud involves the simultaneous application for a loan to several financial organizations.

The applicant does not disclose this information to the lenders. This does not allow an objective assessment of the borrower's real credit risk.

Lending organizations need to know the debt-to-income ratio (DTI). If this ratio is higher than 36%, the lender may consider the borrower to be financially overstretched. This can be a reason to refuse to lend or to apply higher interest rates.

Credit card fraud

Fraudsters often clone or duplicate credit cards. They do this by using stolen data, often obtained through skimming devices or data breaches.

Statistics show that 60% of credit card holders in the United States have experienced a fraud attack. Most of them have been attacked more than once.

Synthetic identity fraud

Its essence lies in the fact that criminals create a false identity that combines real and fictitious data.

For example, attackers may steal someone else’s Social Security number or phone number while using a non-existent applicant’s name.

This identity is subsequently used to apply for a loan, making it crucial for lenders to monitor synthetic fraud red flags at the application stage.

In the USA, the number of loans issued to synthetic identities has been steadily increasing year after year. Two years ago, the value of such transactions stood at $1.8 billion, but by 2023, this figure had risen by nearly $1 billion.

Phishing and social engineering

Fraudsters force people to give up personal or financial information through deception. To this end, they use fake emails, websites, or phone calls.

This information is then used to commit credit fraud, such as entering into new loan agreements or making unauthorized account transactions.

According to ExpressVPN, social media fraud was the biggest financial loss in 2023. Whereas phone calls and fake emails rank only 3rd and 4th respectively.

Friendly fraud (first-party fraud)

A legitimate cardholder pays for a purchase and then disputes the charge by falsely claiming that the transaction was unauthorized. This is often done to avoid paying for goods or services.

The statistics on friendly fraud are shocking. In 2023, 38% of merchants will experience a fraudulent chargeback, causing $84.9 billion in losses.

These numbers are predicted to increase every year.

Account testing fraud

Its essence is that fraudsters test a stolen card or account by making small transactions. Successful transactions prove that the card or account is active and not listed as stolen. This allows criminals to move on to larger purchases.

According to financial analysts, account testing fraud is one of the most popular types of e-commerce fraud, with losses from which could reach a record $38.5 billion in 2027.

Bust-out fraud

A form of long-term fraud where the perpetrator opens multiple credit accounts builds a positive credit history and then maxes out the accounts with no intention of repaying the debt. This often results in significant financial loss for lenders.

According to Alloy, this is the most common type of financial fraud that also maximizes losses.

Merchant fraud

Fraudsters set up fake merchant accounts to process transactions using stolen credit card information.

After fraudulent transactions are processed, they disappear with the funds, leaving the victims and credit card companies to deal with the losses.

Skimming

Skimming involves reading credit card data using a special device. It can be installed in ATMs, petrol stations, or even in hacked point-of-sale terminals.

The scale of the problem is truly enormous. According to FICO, the number of cards whose data was stolen in 2023 is 77% higher than in 2022. The numbers are 120,000 and 70,000, respectively.

Credit repair scams

Fraudulent companies offer to “repair” bad credit by disputing legitimate negative information or using illegal methods to improve credit scores.

These scams can make a victim's situation worse, putting them in an even more difficult financial position.

Fraudulent documentation

This involves submitting fake documents, such as identification, bank statements, tax returns, or pay stubs, to support a loan application.

These forged documents create a false impression of the borrower's financial stability.

Such documents are difficult to identify without specialized checks, as fraudsters are meticulous in their forgery.

Statistically, they usually change most of the information in the document.

You can learn more about fraud schemes in P2P lending in one of our previous articles.

Why use digital footprints to prevent fraud

Digital footprints are an effective tool for financial fraud prevention. It allows you to create a detailed and, most importantly, real picture of your identity.

After all, it is easy to forge documents, but a digital history of several years is almost impossible.

Learn more about how digital footprint analysis helps combat credit fraud in our article.

.svg)

.webp)

Privacy and ethics in digital footprint analysis for fraud protection

As digital footprint analysis becomes key to fighting fraud, privacy and ethics matter more than ever.

Responsible data use builds trust, ensures compliance, and strengthens identity fraud prevention software that protects both lenders and borrowers.

The difference between digital footprints and personal data

A digital footprint is the public trail people leave online. It includes social profiles, posts, and other visible activity.

Personal data, on the other hand, means sensitive information – bank details, ID numbers, or medical records.

E.g., RiskSeal only works with publicly available or consensually shared data. We never collect private or confidential information.

This helps lenders get reliable insights without crossing ethical lines.

Our data protection processes are certified under ISO 27001. It’s one of the most trusted standards for information security. We keep privacy at the core of fraud prevention.

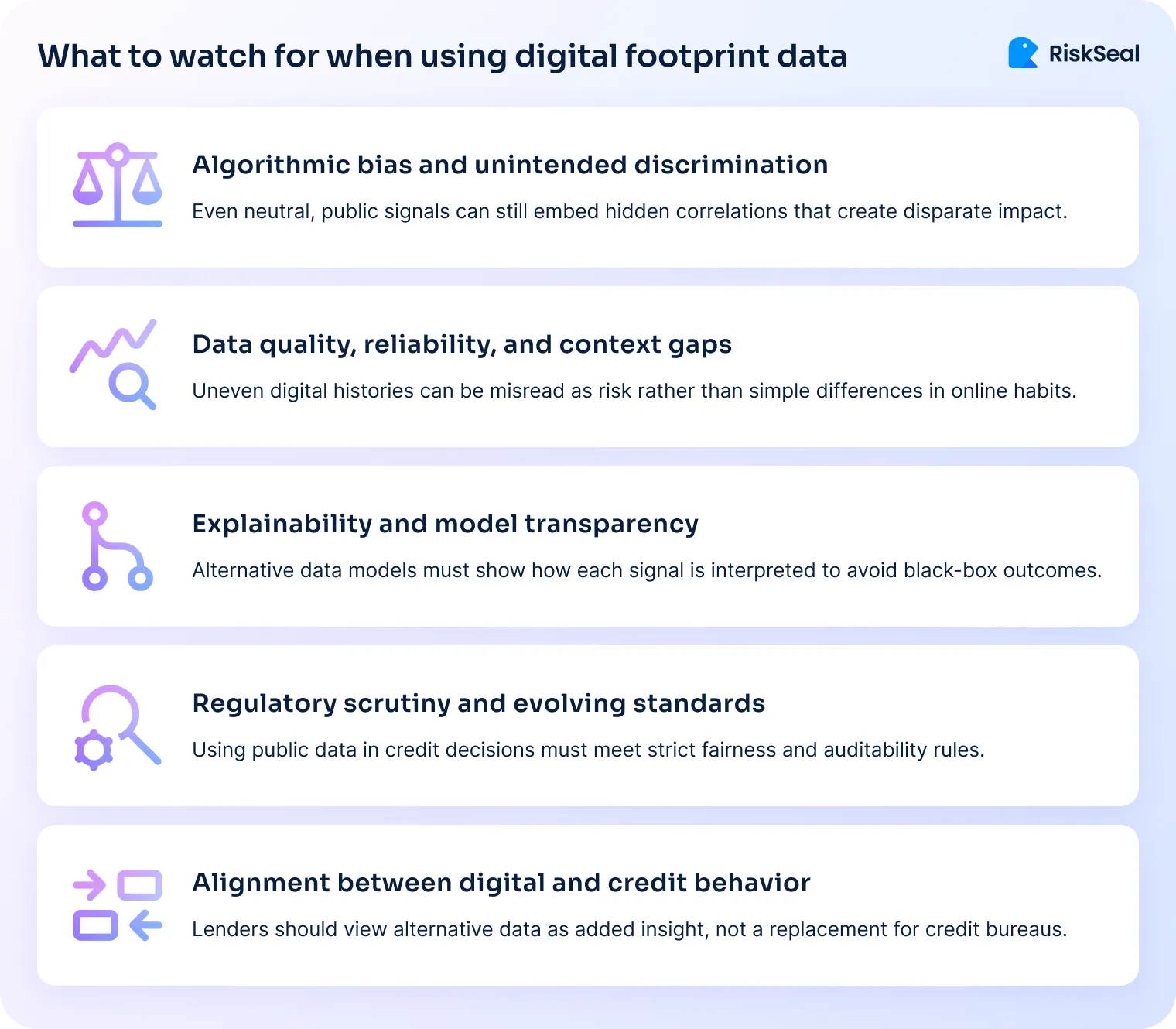

The ethical boundaries of digital footprint analysis

Digital footprints are public, but that doesn’t mean everything is fair game. Ethical data use stops at the line between insight and intrusion.

Fraud detection should rely on open, verifiable data. Not invasive monitoring.

There’s also a fairness challenge. Alternative data can expand access to credit. But if unchecked, it can also repeat social or demographic bias.

To prevent that, lenders should run regular bias and fairness tests. Metrics like disparate impact ratios or false positive rates reveal hidden imbalances.

Transparency matters too. Explainable AI tools show how digital signals shape credit decisions.

When lenders combine bias detection, transparent models, fair data sourcing, and human oversight, they protect both people and performance.

Ethical practices don’t slow fraud prevention. They strengthen trust.

Compliance with privacy regulations

Modern privacy laws protect individuals while allowing responsible data use.

Frameworks like GDPR, LGPD, and Mexico’s LFPDPPP demand clear consent, transparency, and the right to access or erase personal data.

When data crosses borders, companies must follow international transfer rules such as the EU’s Standard Contractual Clauses or Brazil’s LGPD provisions.

These ensure equal protection wherever the data travels.

Compliance isn’t just a checkbox. It’s a sign of respect for customers and regulators.

Ethical data use builds stronger partnerships and long-term credibility. In fraud prevention, trust is the most valuable signal of all.

Case study: how digital footprint analysis stopped a fraud attempt

A fast-growing BNPL company in Colombia reached a critical scaling stage. With new customers coming fast, so did fraud attempts. Traditional tools weren’t keeping up.

What was the issue?

The lender experienced a wave of synthetic identity applications. Fraudsters were creating convincing, composite profiles that easily passed traditional credit checks.

On the surface, these applicants looked legitimate. Documents matched. Credit files seemed complete. Yet many of these new accounts defaulted within weeks.

Losses started to mount, and manual reviews were slowing the onboarding process. The team needed faster fraud detection without blocking genuine customers.

What RiskSeal did

RiskSeal’s digital footprint analysis was deployed directly into the BNPL platform. The system checked each applicant’s online presence and connections in real time:

- Mismatched social profiles used the same photo but different names.

- Email and phone lookups revealed links to unrelated identities.

- IP traces pointed to proxy networks far from the stated location.

Red flags appeared instantly. These signals uncovered a coordinated fraud ring that standard verification couldn’t catch.

Within days, the lender fine-tuned its risk filters and automated the fraud review process.

The result

The impact was immediate:

- False positive rate dropped by 18%

- Customer drop-off during onboarding decreased by 10%

- Average fraud detection time fell from five minutes to under five seconds

The BNPL company now flags fraudulent applications before they reach underwriting.

Digital footprint analysis transformed fraud detection from a manual checkpoint into a real-time shield for growth.

Fraud prevention services by RiskSeal

RiskSeal's digital scoring system uses many advanced methods to screen potential borrowers, including phone verification through a reverse phone number search engine.

Digital footprint analysis

We research 200+ online resources, identifying:

- Registered accounts on various platforms.

- Publicly available social media data.

- Behavioral indicators.

In the digital footprint analysis process, we apply techniques such as:

1. Email lookup solution. Comprehensive analysis of social media profiles and cross-referencing blacklists for potential threats.

2. Phone number lookup. Identification of linked social media accounts and detection of disposable cell phone numbers to ensure accurate user verification.

3. IP address lookup. We trace the true origin of online connections, detecting proxy or TOR usage to improve security and prevent fraud.

Identity verification

RiskSeal allows you to identify with a high degree of probability when an applicant is not who they say they are. This is possible with advanced digital identity verification methods.

Face recognition. This is a technology that allows comparing several photos of a potential borrower and determining whether they depict the same person. Its action is based on analyzing facial features to find matches or differences.

Location insights. This is a way to determine the real location of the borrower. It allows for comparing the detected data with the data specified in the application and assigning a high-risk level to the borrower in case of discrepancies.

Name matching. This is a method of identity verification, which consists of establishing the equivalence of applicant's names used in different sources. We take into account the linguistic peculiarities of name spelling so we return the most accurate results to our clients.

Database of past credit checks

We have a database of email addresses and phone numbers that we have already checked.

We inform our clients that we have already analyzed a particular user's data and provide information such as:

- Number of credit applications

- Date of first application

- Date of last application

With the help of this database, the RiskSeal credit scoring platform effectively solves the problem of loan stacking fraud.

FAQ

How financial companies are using digital footprint data to prevent fraud?

Financial institutions analyze the digital footprints of potential borrowers to identify their identity, verify their location, and determine their behavioral characteristics. Digital footprint analysis allows the recognition of different types of fraud, including loan stacking, synthetic identity fraud, and others.

How to prevent financial fraud?

For financial fraud prevention, it is important to combine traditional credit scoring methods with digital footprint analysis. This approach provides a comprehensive profile of a potential borrower, not just limited to their historical financial data.

What are the most common types of credit fraud?

The most common types of credit fraud include loan fraud, identity theft, loan stacking, credit card fraud, synthetic identity fraud, and bust-out fraud. Criminals also often use false documents to obtain credit fraudulently.

How does RiskSeal utilize digital footprint analysis to combat credit fraud?

RiskSeal utilizes digital footprint analysis to verify the data provided by the borrower and identify their identity. We utilize advanced technologies such as email and phone number lookup, IP address lookup, face recognition, location insights, and name matching.

See more

Explore the role of face match technology in the lending industry and examine its effectiveness in credit risk management.

.webp)

Explore how fraudsters exploit disposable phone numbers for loan scams and how phone lookup helps lenders prevent financial fraud.

Learn how lenders can use face match, name match, and location match analyses to build inclusive financial systems.