10 Best APIs for Predictive Credit Scoring in Lending Platforms – 2026 Edition

Discover the top-10 APIs bringing predictive power to credit scoring through alternative data.

We analyzed 6.1 million loan applications

The results show how digital credit scores correlate with default risk.

Traditional credit scoring leaves 1.7 billion adults worldwide without access to formal financial services.

Fintechs are turning to predictive APIs that analyze alternative data to assess creditworthiness more accurately. These tools help approve previously unbankable customers while maintaining low default rates.

In this post, we'll review 10 credit scoring APIs that bring predictive power to your lending platform.

Best APIs for predictive credit scoring in lending: our picks

Here are the APIs we're analyzing in this guide:

- RiskSeal

- Mastercard Alternative Credit Scoring API

- Equifax API Products

- Zest AI

- Trusting Social

- Credolab

- Juvo

- Argyle

- Heron Data

- CreditVidya

How we selected these alternative data APIs

We evaluated each platform based on specific criteria that matter most to credit risk managers:

- Credit industry fit. The API is designed specifically for credit decisioning, rather than generic data enrichment or identity checks.

- Predictive power. Evidence of measurable uplift in approval rates for underserved and unbanked users, alongside improved default rates.

- Data sources and features. Breadth and quality of inputs, including alternative data points (email, phone, IP, social signals) provided.

- Integration and usability. API-first design with real-time processing and smooth embedding into loan origination systems.

- Compliance and security. Strong adherence to privacy regulations and built-in fraud detection.

- Pricing and scalability. Clear pricing models like pay-as-you-go or per-transaction, plus free trials where available.

Now, let’s review each alternative credit data API in more detail, focusing on how they compare and what to consider when selecting the right solution.

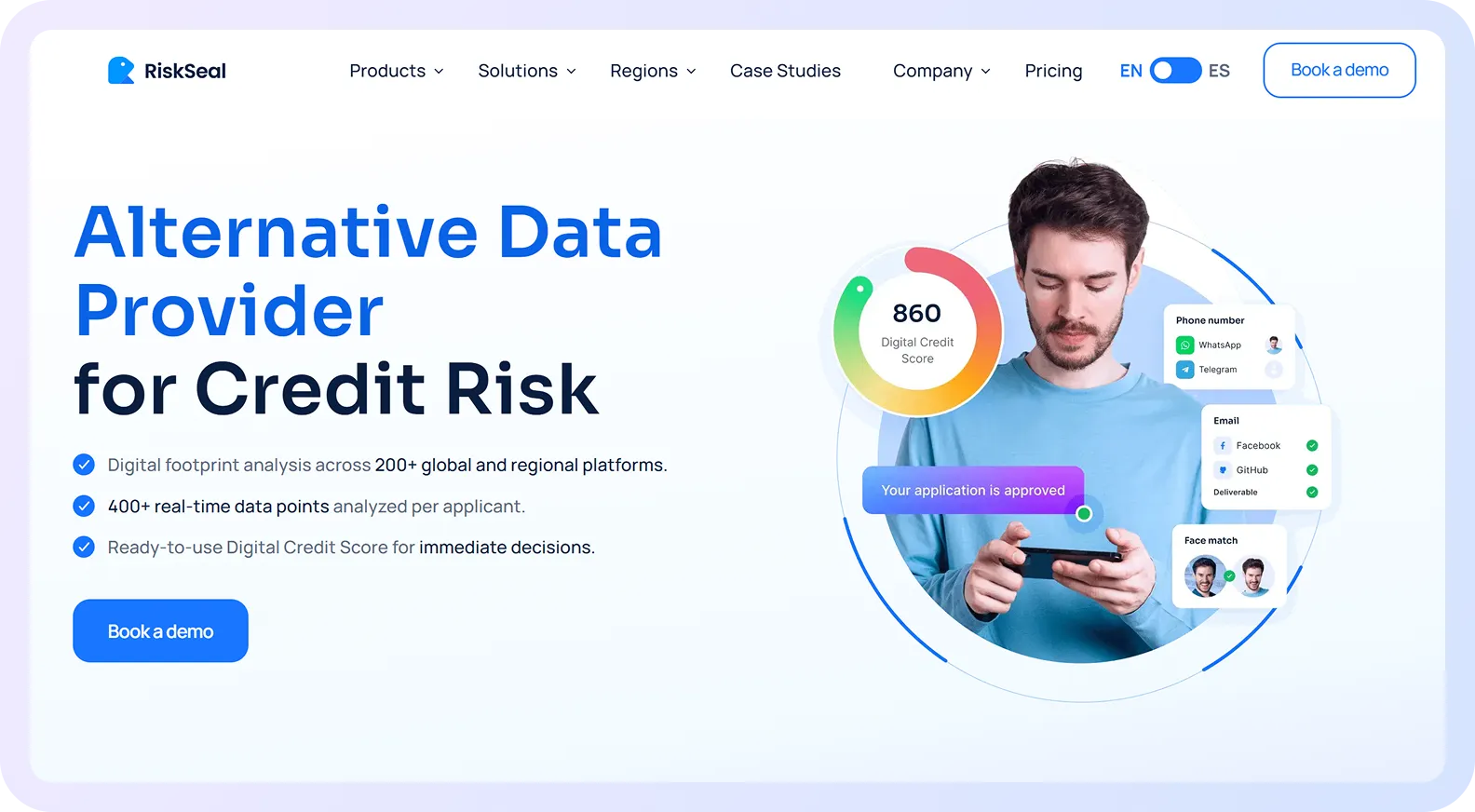

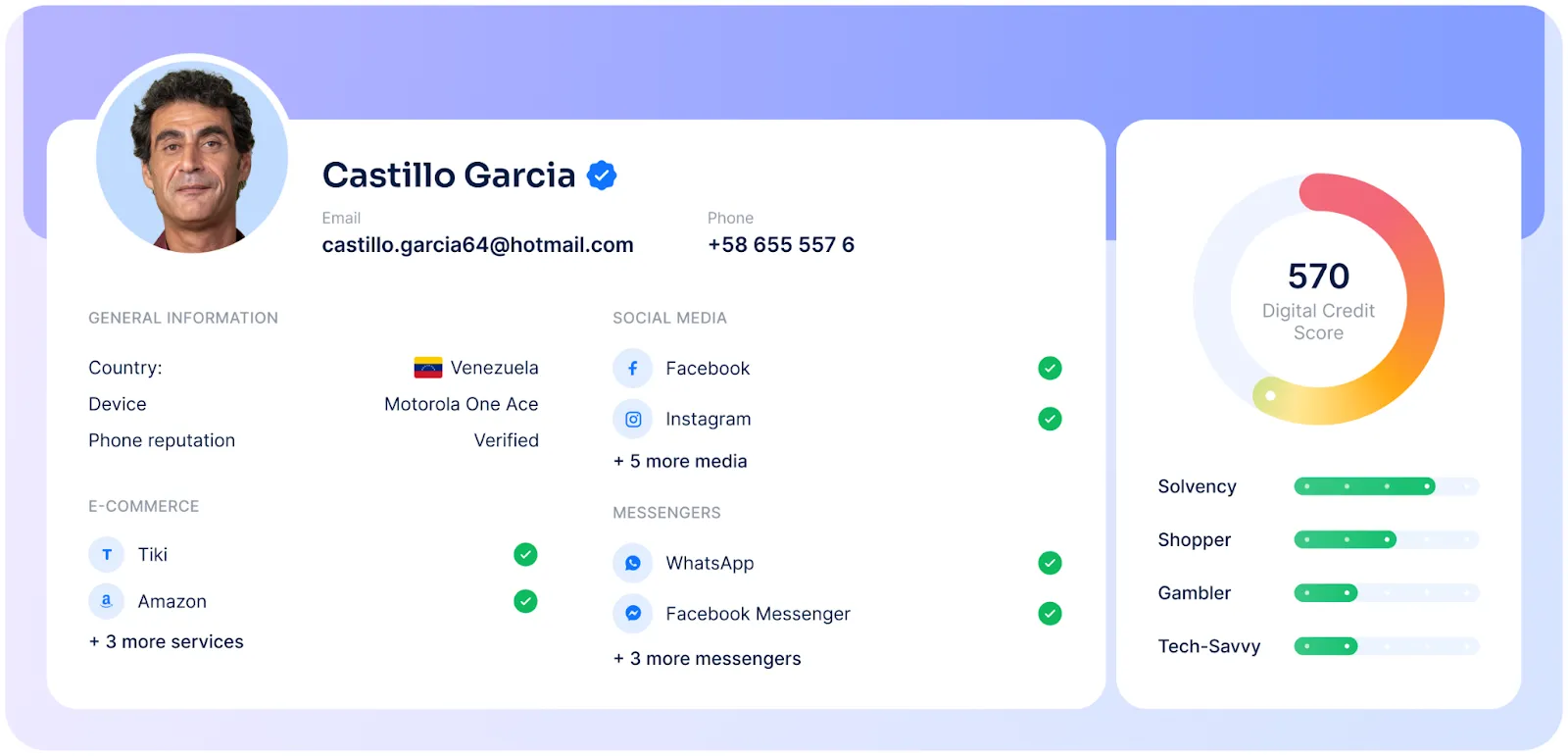

1. RiskSeal Digital Credit Scoring API

Overview

RiskSeal analyzes digital footprints across both global and local platforms to enrich credit risk models with real-time alternative data.

The API is designed to complement existing bureau-based scoring, adding predictive power where traditional data becomes thin or delayed.

RiskSeal processes hundreds of digital signals collected from 200+ platforms worldwide, including region-specific services that other vendors do not cover.

This local depth is critical for accurate risk segmentation across diverse markets. RiskSeal’s key data categories include:

- Email and phone signals. Age, usage consistency, domain, cross-platform presence, and hundreds of other indicators of long-term digital activity.

- Social platform presence. Depth and consistency of activity across global networks like Facebook and Instagram, as well as local platforms such as KakaoTalk in South Korea.

- E-commerce activity. Engagement patterns across global marketplaces like Amazon and region-specific platforms such as Allegro in Poland.

- Paid subscriptions. Engagement and stability signals, such as Netflix subscription alongside region-specific platforms like Shahid VIP Streaming in Saudi Arabia.

- Web and tech accounts. Identity consistency through usage of services like Google or LinkedIn, as well as locally dominant platforms like Computrabajo in Peru.

- IP and location signals. Behavioral patterns that help detect anomalies without adding friction for legitimate users.

RiskSeal generates a Digital Credit Score (0-999) within seconds. This score is not a replacement for bureau data, but an additional input into existing models to improve decisioning accuracy.

Lenders use RiskSeal alongside bureau scores to achieve measurable uplift in Gini and AUC, including in mature markets with strong credit coverage.

Clients report improved approval rates, lower defaults, and better risk segmentation, particularly for thin-file borrowers and underserved segments.

Integration typically takes one business day and does not require changes to existing decision engines or workflows.

RiskSeal is ISO 27001 certified and fully GDPR-aligned, with transparent documentation suitable for regulated markets, especially in the EU.

Identity-related checks such as name consistency are available as supporting signals, but RiskSeal’s core value lies in credit risk enrichment.

Pricing

RiskSeal uses a pay-as-you-go pricing model starting at $499/month, with no setup fees. Custom pricing is available for high-volume lenders and enterprise use cases.

A free proof of concept allows teams to test performance uplift on representative portfolio segments before committing.

.svg)

.webp)

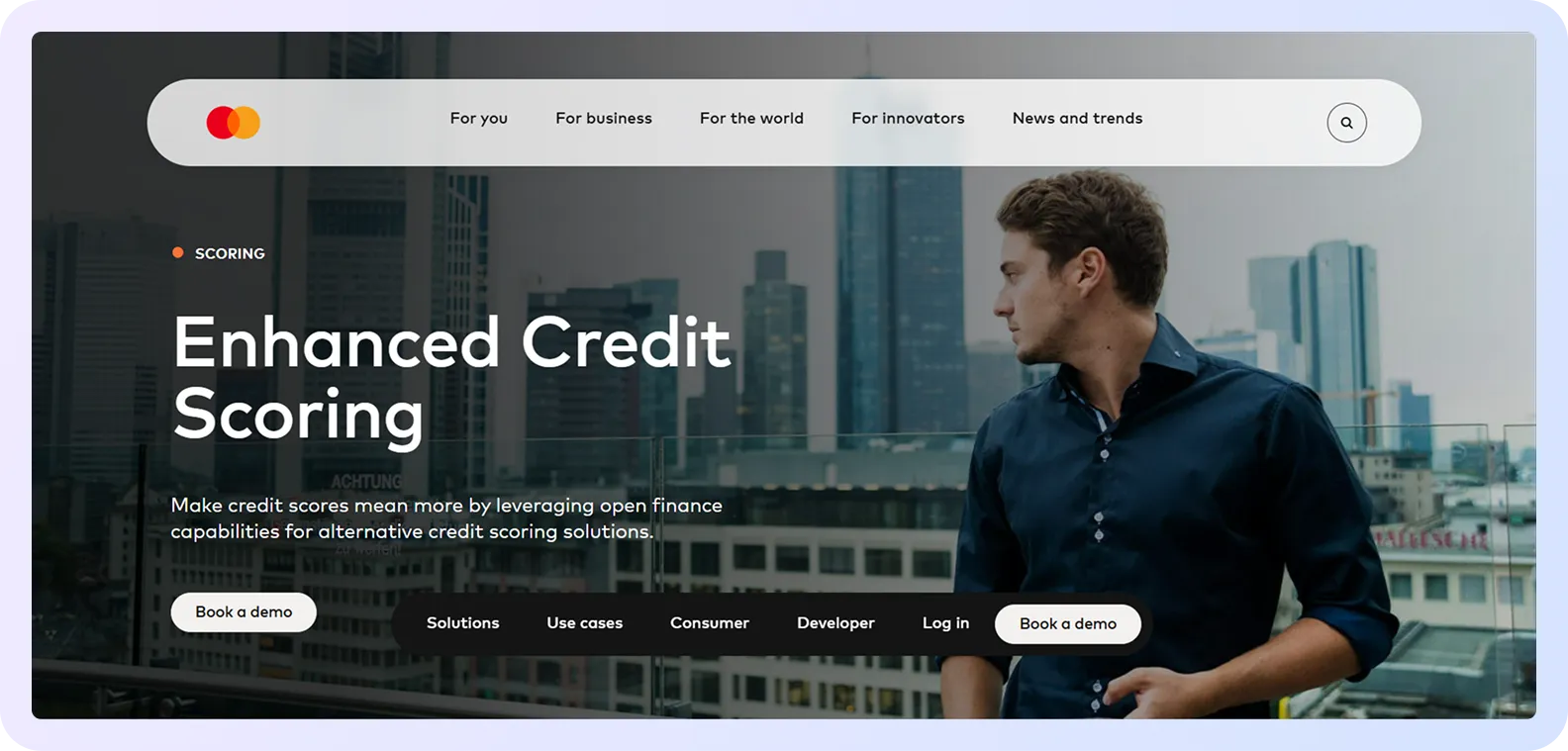

2. Mastercard Alternative Credit Scoring API

Overview

Mastercard's Alternative Credit Scoring API is part of its Consumer Credit Analytics suite. It uses transaction data from Mastercard's network to assess borrowers with limited credit histories.

The API analyzes debit and credit card transactions across industries, geographies, and channels. Through its partnership with Credolab, it processes over 1 million behavioral features from device metadata and biometrics.

The system is built for thin-file consumers. It delivers near real-time credit scores and delinquency predictions to complement traditional bureau data.

Single API call returns instant credit scores and fraud risk indicators. The platform includes device fingerprinting, geolocation checks, and velocity monitoring.

All data collection requires explicit consumer consent. Fraud detection draws from a database of over six billion devices.

Pricing

Pay-per-use model charges per API call.

Sandbox access provided through the developer portal for testing.

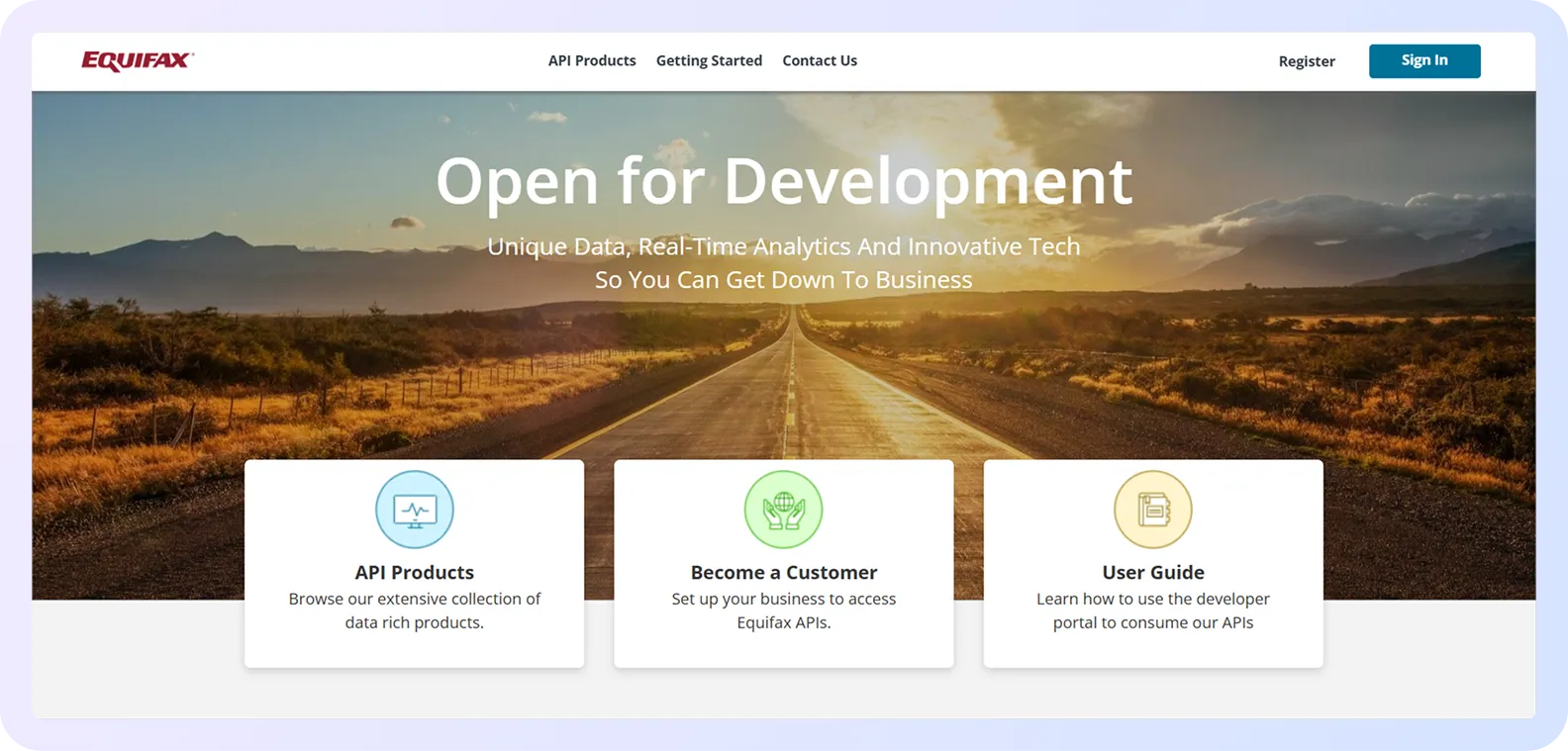

3. Equifax API Products

Overview

Equifax offers a suite of APIs that deliver VantageScore and FICO scores, credit reports, and monitoring tools. The platform draws from Equifax's credit bureau database to support underwriting and risk management.

The suite combines traditional credit file data – payment history, liabilities, public records – with alternative data assets. It's designed for credit providers who need multi-bureau insights and real-time information.

Single API call retrieves credit scores, reports, and real-time alerts for credit changes. Multi-bureau queries available for broader risk assessment.

The platform includes income verification and compliance checks like OFAC alerts. Developer tools provided for testing and customization.

All data access requires consumer consent. Security follows Equifax's standards for protecting sensitive information.

Pricing

Per-report pricing ranges from $2.90 to $3.99 through resellers. Tiered models include monthly minimums or annual commitments for API access.

4. Zest AI API

Overview

Zest AI provides ML-powered underwriting software for lenders who want to automate credit decisions. The platform helps financial institutions assess risk more accurately while expanding access to underserved borrowers.

The system uses custom ML models trained on traditional credit data and alternative signals. It's built for credit unions, banks, and online lenders looking to improve approval rates without increasing losses.

Credit institutions report a 25% average lift in approvals and auto-decisioning rates of 70-83%. The platform reduces defaults through better risk forecasting.

API-first design enables real-time processing and seamless embedding into loan origination systems. Dedicated Customer Success team supports implementation.

The platform includes bias mitigation tools and model risk management guidelines. Applicant reports deliver transparency into credit decisions.

Pricing

Custom pricing based on tailored models and usage. Scalable for fintechs of all sizes through cloud-based deployment.

5. Trusting Social API

Overview

Trusting Social specializes in AI credit scoring for underbanked populations in emerging Asian markets. The platform analyzes alternative data from telco and social network sources to assess new-to-credit borrowers.

The system processes over 120 billion records weekly from anonymized telecom data and phone number patterns. It's built for lenders who need instant creditworthiness evaluations in markets with limited bureau coverage.

Credit providers report 48-63% reductions in credit losses across product categories. The platform claims 10x higher disbursal rates for creditworthy individuals and serves over a million borrowers monthly.

Real-time API delivers Credit Scores and Fraud Scores at the application stage. The platform includes facial recognition and ID cross-validation for identity verification.

Bespoke model customization allows loan companies to tailor risk assessment to their portfolios. Data collection requires explicit customer consent and uses anonymized or aggregated information.

Pricing

Custom pricing not publicly disclosed. Scalable for high-volume lending operations across multiple markets.

6. Credolab API

Overview

Credolab uses smartphone and web metadata to generate alternative credit scores for unbanked and thin-file consumers. The platform analyzes behavioral biometrics and device data without requiring traditional credit history.

The system processes over one million behavioral features to create risk scores. It's designed for banks and fintechs that need to assess credit invisibles in emerging markets.

Lenders report up to 32% increases in approval rates and 21.9% reductions in cost of risk. The platform reduces first payment defaults through better delinquency forecasting.

The platform generates fraud scores, risk assessments, and income predictions without PII or financial history. Real-time alerts flag potential fraud during application processing.

Privacy-consented data collection uses anonymized metadata. The platform supports flexible validation across the customer lifecycle.

Pricing

CredoLite starts at $299/month for 100k uploads annually. CredoOne starts at $624/month. Custom CredoScore pricing available. Free demos offered.

7. Juvo API

Overview

Juvo offers Financial Identity as a Service by analyzing mobile user behavior data. The platform creates financial identities for creditworthy individuals who lack traditional credit histories in emerging markets.

The system uses transaction data from mobile operators to generate proprietary credit scores. It's built for microfinance institutions and banks operating in Latin America, the Caribbean, and Brazil.

Juvo targets financially excluded populations through partnerships with mobile operators. The platform enables access to microlending and other financial services for underbanked segments.

Identity scoring algorithms assess creditworthiness based on mobile transaction patterns. The platform includes microlending capabilities and segmentation tools for lending decisions.

Real-time scoring supports quick underwriting at the point of application. The platform focuses on ethical data use for financial inclusion.

Pricing

Custom pricing based on partnerships and usage. Not publicly disclosed.

8. Argyle API

Overview

Argyle specializes in income and employment verification through consumer-permissioned payroll and bank connections. The platform provides fintechs with direct-source data to assess borrower stability and creditworthiness.

The system covers 90% of the U.S. workforce with real-time access to income, employment, and asset information. It's designed for personal lending, mortgages, and tenant screening applications.

Argyle handles 8 million API calls daily with 99.9% uptime. The platform enables faster loan approvals through automated verifications and comprehensive earnings history.

API-first design integrates seamlessly into loan origination and point-of-sale systems. Real-time data streaming supports fraud detection and paycheck-linked lending.

The platform includes earned wage access capabilities and automated employment verifications. Consumer consent required for all payroll and bank connections.

Pricing

Pay-per-use or subscription models with no upfront costs. Up to 80% cost savings compared to traditional verification methods. Free trial available.

9. Heron Data API

Overview

Heron Data uses AI to analyze bank transactions and financial documents for automated credit decisioning. The platform transforms raw banking data into actionable insights for small business lending and underwriting.

The system enriches transaction data with risk scores, merchant identification, NAICS codes, and financial metrics. It's built for credit organizations and funders who need to process high volumes of business loan applications.

Lenders report 80% reductions in processing costs and save up to 320 hours weekly. The platform supports faster credit decisions through automated document extraction and categorization.

API and SDK enable real-time integration with CRM systems and lending workflows. The platform includes KPI dashboards for business intelligence and risk assessment.

Automated categorization extracts financial metrics from PDFs and transaction data. Integration with DataMerch provides payment history insights for better risk forecasting.

Pricing

Custom quotation-based pricing per document processed. Volume-based scaling available with no upfront costs mentioned.

10. CreditVidya API

Overview

CreditVidya, now part of CRED after its 2022 acquisition, provides alternative credit scoring for first-time borrowers in India. The platform uses AI and big data to assess underserved segments through mobile and digital behavior analysis.

The system processes over 10,000 data points from unconventional sources to generate credit scores. It's designed for banks and fintechs operating in India's lending market.

Loan providers report 15% higher loan approval rates and 33% lower delinquencies at the same risk level. The platform focuses on financial inclusion for new-to-credit users.

SaaS lending-as-a-service platform integrates into existing underwriting workflows. Automated credit scoring covers individuals and small businesses.

The system includes document verification and fraud detection capabilities. Predictive scores generated from mobile behavior and digital footprints.

Pricing

Custom pricing based on usage. Details not publicly available following CRED acquisition. Platform designed for high-volume scalability.

Finding the right credit scoring API for your needs

Choosing the best APIs for integrating predictive credit scoring into lending platforms starts with clear goals.

Define your target market, borrower segments, and data requirements before evaluating solutions.

Use this quick comparison to identify which digital footprint software matches your lending focus:

Different APIs excel in different areas.

Some focus on emerging markets while others specialize in income verification or transaction analysis.

Your choice should align with your specific lending use case.

How to choose the best APIs for predictive credit scoring in lending platforms

We've already discussed the importance of aligning API choice with your organization's goals. But operational и risk factors should influence your decision too.

Data interpretation approach

Avoid providers that prioritize raw data volume over quality. Collecting as much data as possible doesn't guarantee higher accuracy.

Look for providers who focus on meaningful data points rather than volume. The best alternative data providers use sophisticated algorithms to extract predictive signals from quality data sources.

Compliance with regulations

The API owner must adhere to local and global laws and regulations. This includes things like GDPR in the EU or LFPDPPP in Mexico, among others.

Non-compliance puts your lending operations at risk. Verify that your chosen provider follows all relevant privacy and data protection requirements in your target markets.

Free proof of concept

The software provider should prove their predictive power on real-life applications.

This means comparing the results generated during a test or pilot project with your own historical portfolio data, including observed defaults.

This validation might take time. But companies confident in their API won't hesitate to provide proof of concept on your actual loan portfolio.

Certifications for data protection

Digital footprint analysis and credit scoring require high responsibility for data safety. Choose companies that are proven experts.

ISO 27001 certificate holders demonstrate commitment to information security management. This certification shows the provider takes data protection seriously.

Ease of integration and tech support

Modern user-friendly solutions allow simple, fast, and straight-forward integration. Settling for less only wastes time that could otherwise be spent growing the business.

Complex integration processes signal outdated technology or poor documentation. Look for APIs with clear guides, sandbox environments, and responsive technical support teams.

Making predictive analytics in lending work for your business

The right predictive credit scoring API transforms your risk assessment capabilities.

Start by testing multiple solutions with proof-of-concept projects on your actual portfolio. Watch how each handles your specific borrower segments and data availability challenges.

The platform that delivers measurable Gini improvements while maintaining fast integration timelines deserves your investment.

Remember that the cheapest option rarely provides the best long-term value when portfolio performance is at stake.

We analyzed 6.1 million loan applications

The results show how digital credit scores correlate with default risk.

FAQ

What is a predictive credit scoring API?

A predictive credit scoring API is a software interface that generates credit scores and risk assessments in real-time through automated data analysis.

These APIs use machine learning and AI algorithms to predict loan repayment likelihood.

They process alternative data sources, such as digital footprints, device behavior, and telecom patterns, alongside traditional credit bureau information.

Lenders integrate these APIs directly into their loan origination systems to automate underwriting decisions and approve more creditworthy borrowers.

What types of alternative data are most commonly used in predictive credit scoring?

Common alternative data sources include:

- digital footprints from email and phone usage

- profile pictures and usernames

- behavioral biometrics

- telecom transaction patterns

- social media presence

- e-commerce platforms presence

- subscription service payments

These data points help assess borrowers who lack traditional credit histories.

How long does it take to integrate a predictive credit scoring API into a lending platform?

Modern APIs typically integrate in 1-5 days depending on your technical infrastructure.

Best-in-class providers offer REST APIs with comprehensive documentation and sandbox environments for testing.

Some solutions require custom setup that may extend to several weeks. Always ask for integration timelines during demos.

Are predictive credit scoring APIs compliant with regulatory, privacy, and fair lending requirements?

Reputable APIs like RiskSeal comply with regulations like GDPR in Europe and LFPDPPP in Mexico.

They collect only publicly available information, like presence on social media or e-commerce platforms, but never private data such as messages or products purchased.

Look for providers with ISO 27001 certification and bias mitigation tools. Always verify compliance with your specific market requirements before committing.

How much does a predictive credit scoring API typically cost?

Pricing models vary widely.

Pay-per-use options charge per API call, typically $2.90-$3.99 for bureau data. Subscription models start around $299-$624 monthly for limited volumes.

Enterprise solutions use custom pricing based on call volume and features. Most providers offer free trials or proof-of-concept periods to test performance.

How do I choose the best predictive credit scoring API for my lending platform?

Match the API to your target borrower segments and geographic markets. Request proof-of-concept tests on your actual portfolio to validate predictive power.

Evaluate integration complexity, data sources, compliance certifications, and pricing transparency.

Schedule demos with three to five providers and compare GINI uplift results before making your final decision.

See more

.webp)

Understand the crucial aspects fintech providers need to focus on to ensure successful and relevant PoCs.

.webp)

Discover 25 leading alternative data providers helping lenders improve credit decisions, detect fraud, and serve borrowers beyond traditional scoring.

Discover global lending trends that can shape credit scoring strategy for successful financial inclusion.