Learn how modern customer risk assessment leverages AI and alternative data to fight fraud, boost compliance, and speed up smart approvals.

Automation, machine learning, and alternative data drive the rapid growth of digital lending and transform how lenders assess risk.

While speed and convenience attract more borrowers, they also increase the risk of fraud, regulatory breaches, and financial loss.

Since we live in a fast-paced environment, we should not overlook credit risk assessment. As a core part of modern lending, it helps financial institutions understand who they're lending to and the potential risk each borrower poses.

In this article, we will explain why customer risk assessment matters in digital lending and how it helps prevent fraud and meet compliance standards. We will also cover the latest tools improving the process and share best practices to build trust, strengthen security, and support long-term growth.

Digital lending has transformed borrowing, making it simpler and more accessible.

To meet demand, lenders are using automation and alternative data to quickly process applications.

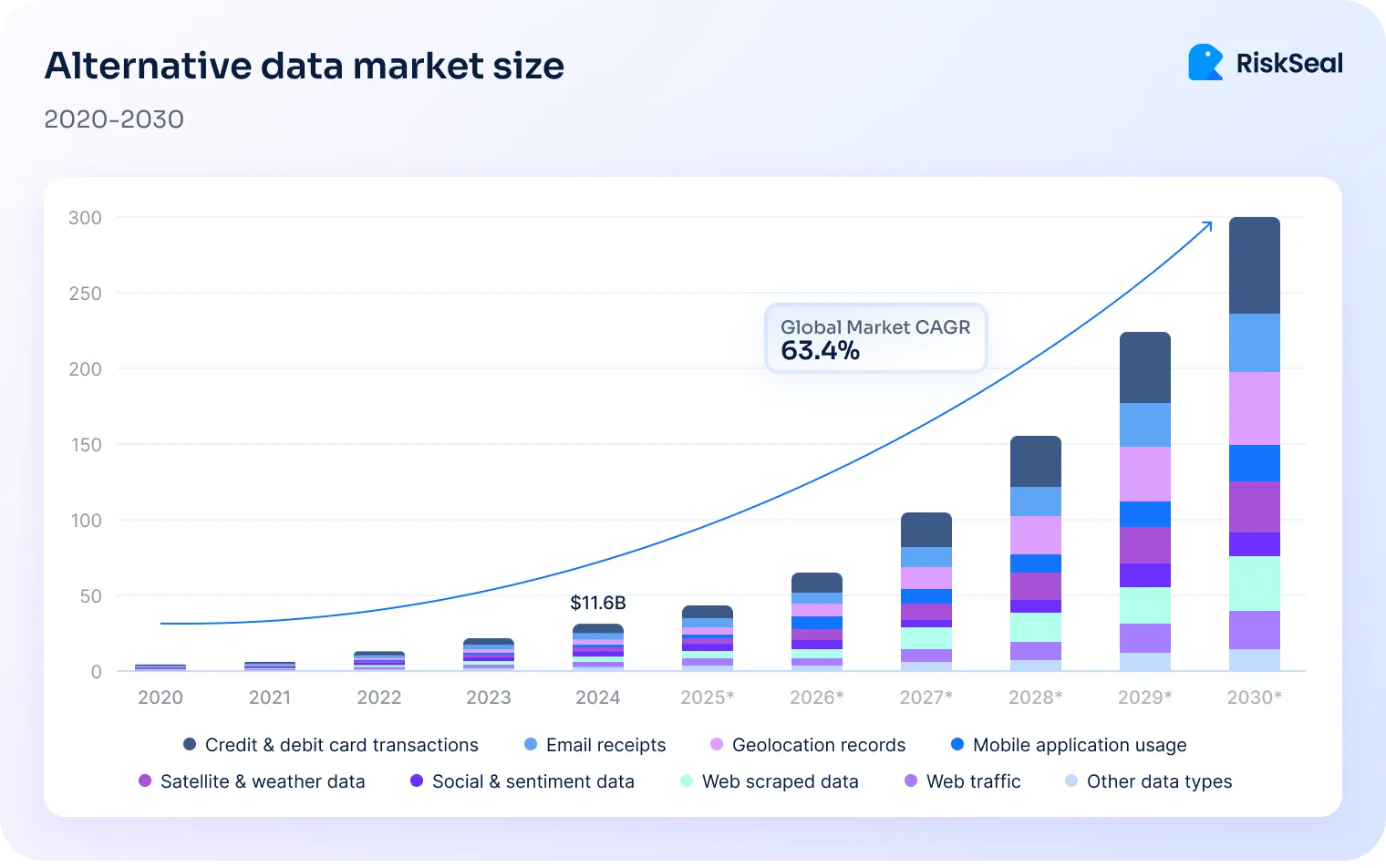

The rapid growth of the global alternative data market, from $11.65 billion in 2024 to a projected $135.72 billion in 2030, highlights its rising importance.

However, this increased speed introduces risks like fraud and compliance issues. That’s why customer risk assessment is essential to keep digital lending safe and reliable.

Customer risk assessment helps lenders evaluate a borrower’s financial behavior and risk level.

It identifies those likely to default, commit fraud, or trigger compliance issues.

By reviewing identity data, spending patterns, and transaction behavior, lenders can catch red flags early.

Be it identity theft, mismatched documents, or unusual locations, this process supports fraud prevention, regulatory compliance, and smoother, safer lending operations.

In digital lending, the risk landscape shifts dramatically due to automation and speed.

Applications are often processed in real time. This gives fraudsters narrower detection windows and increases pressure on systems to spot risks instantly.

Since traditional methods can’t keep up with this pace, digital lenders turn to machine learning models that assess alternative data and behavior patterns on the fly.

A strong customer risk assessment model makes accurate, compliant, and safe lending decisions.

Each component, from verifying identity to monitoring behavior, helps build a complete picture of borrower risk in real-time.

Lenders use a mix of traditional credit data and alternative data to evaluate borrower risk.

Here is a closer look at the key components of a customer risk management model:

Effective customer risk management is both a competitive advantage and a regulatory requirement.

With the right tools, digital lenders can reduce loan losses, improve decision accuracy, and scale confidently while protecting revenue and reputation.

Modern customer risk management blends compliance with competitive strategy.

By using advanced tools like AI, alternative data, and real-time monitoring, digital lenders gain deeper insights into borrower behavior and financial health.

These technologies sharpen decision-making by giving lenders deeper visibility into borrower risk. They also support faster growth by minimizing exposure to fraud and regulatory lapses.

AI and machine learning models scan borrower behavior at scale and identify subtle patterns and anomalies that signal risk.

These systems group customers by repayment habits and predict future defaults more accurately than traditional scoring.

As fraud tactics and borrower behaviors evolve, lenders must regularly retrain these models with fresh data.

With NASDAQ projecting that 70% of banks and financial institutions will increase AI and machine learning investments over the next two years, the importance of keeping these systems sharp and adaptive is only growing.

Alternative data, such as utility payments, rental history, mobile usage, and e-commerce behavior, gives lenders deeper insight into borrowers with limited or no credit history.

This approach increases credit access without compromising the accuracy of risk scoring.

Lenders in emerging markets can use mobile phone bill payment records to successfully assess and serve thin-file customers.

Accounts receivable software gives digital lenders real-time insight into how borrowers manage repayments after receiving a loan.

Unlike traditional credit checks, it monitors invoice activity, payment delays, and cash flow patterns, which are key indicators of financial stability.

When integrated into risk assessment models, accounts receivable software helps flag early signs of distress, such as late or missed payments.

This dynamic data keeps risk scores current and aligned with borrowers’ actual behavior. By using alternative data from accounts receivable software, lenders can make better credit decisions and act early to reduce potential losses.

Customer risk assessment protects digital lending by detecting fraud early and ensuring AML compliance.

At the same time, AI, alternative data, and accounts receivable software support instant identity verification and continuous risk monitoring.

These tools streamline onboarding and flag threats instantly.

Build trust, ensure compliance, and drive sustainable growth by proactively adopting risk assessment practices that strengthen resilience in the current digital lending ecosystem.

Discover how enhanced credit scoring models with alternative data drive financial growth and boost inclusivity.

.webp)

Discover how social media profiling enhances credit risk management by analyzing digital footprints.

Master the credit risk metrics that actually protect your portfolio. Learn how top fintechs track, interpret, and act on risk signals in 2026.

.svg)