How to Build Risk-Adjusted Customer Acquisition in Lending

Learn how to grow approvals with risk-adjusted acquisition, better funnel checks, and borrower quality metrics.

According to First Page Sage’s 2026 CAC benchmarks, financial services companies spend an average of $784 to acquire a customer. This is higher than most other industries.

When CAC is that high, every application carries more weight. A declined applicant still costs money. An approved borrower needs to repay profitably. And any shortcut that improves conversion today can create losses later.

Of course, lenders need to grow originations. But the fastest path is not always the healthiest one. I have seen teams optimize for more applications today, only to let portfolio risk surface months later.

This article lays out a practical framework for expanding the funnel without quietly weakening the book behind it.

The CAC trap: When more conversions create more risk

The typical growth playbook looks like this: test channels, lower friction, improve conversion, scale what works. That logic is sound, until it isn't.

The problem is that not all acquired borrowers perform equally. A channel with a 40% conversion rate might generate twice the defaults of a channel converting at 20%.

Without a risk layer woven into your acquisition strategy, you're optimizing for a metric that has no direct relationship to profitability.

I have seen this pattern repeatedly while working with lenders across EMEA and Southeast Asia. These are not easy markets to generalize. But many share the same acquisition challenge:

- fast digital growth

- thin-file borrowers

- uneven bureau coverage

- sharp differences in channel quality

The teams that struggle most are usually the ones where marketing and risk operate in silos.

Marketing chases volume. Risk cleans up the mess later. By the time DPD30 data surfaces, you've already funded hundreds of bad loans.

The fix is a risk-adjusted acquisition framework. One where risk signals feed back into channel decisions before money goes out the door.

Build risk checks into every stage of the funnel

The goal is not to slow acquisition down. It is to make every stage of the funnel more selective, more measurable, and more connected to repayment outcomes.

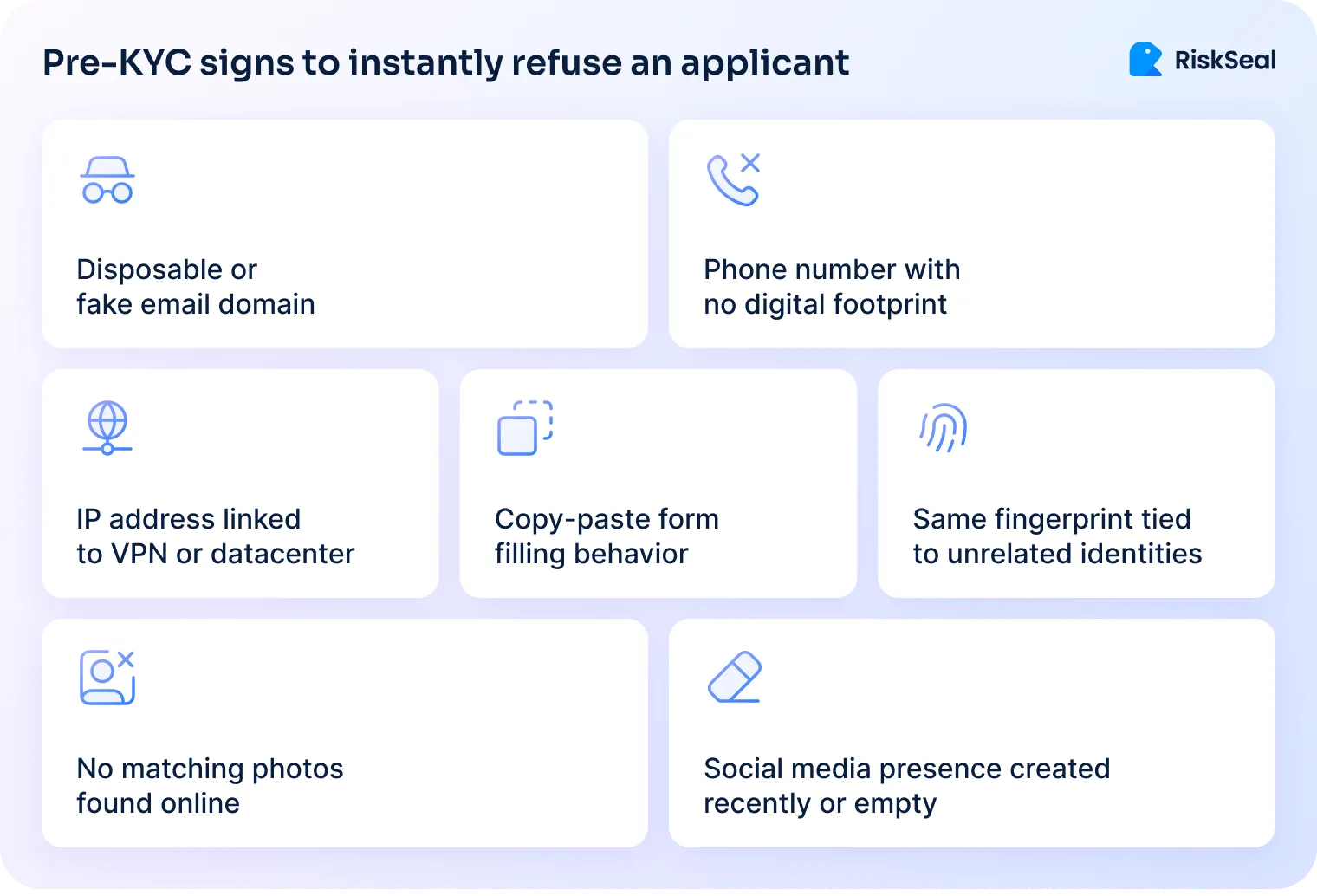

Step 1: Pre-screen early to catch weak applications before full decisioning

Don't wait for a full credit application to start evaluating risk. Lightweight pre-screening signals include:

- email age and validity

- device reputation

- IP and geolocation consistency

- social media presence

All these reviewed in context can flag high-risk applicants before they even hit your decision engine.

This isn't about rejecting people early, but routing them correctly. A thin-file applicant with a strong digital footprint is a very different risk profile from one with no verifiable online presence at all.

Pre-screening also reduces the cost of full credit checks on applicants who would never pass anyway.

Step 2: Verify sooner by adding alternative signals before approval

Once an applicant enters the funnel, enrich their profile with alternative data before making a decision. Digital footprint signals – email domain age, platform account history, behavioral consistency – add meaningful lift to traditional scoring, especially for thin-file borrowers.

I witnessed this directly when working with lenders in emerging markets: bureau coverage is often sparse, but digital signals are abundant.

A borrower who has maintained the same email address for eight years and has verified profiles on multiple platforms is telling you something a credit bureau cannot.

Step 3: Decide faster by keeping speed and accuracy in the same pipeline

Speed matters for borrower customer acquisition, but speed without accuracy is expensive.

Real-time decisioning requires that your data sources, scoring model, and decision rules are integrated into a single pipeline. Not a manual review queue.

The goal is sub-60-second decisions for clean applications, with clear escalation paths for edge cases.

But fast decisions can also create adverse selection. Borrowers who need immediate cash, or who have already been rejected elsewhere, are often drawn to the lowest-friction application paths. It means speed needs guardrails.

Account for this bias directly in your framework. Monitor approval quality by channel, device type, time-to-submit, and repeat application behavior. A fast funnel should still know when to slow down, request more verification, or route an applicant into manual review.

Decisioning latency is a conversion killer. But inconsistent decisioning is a portfolio risk and a compliance risk, especially when similar applicants receive different treatment.

Step 4: Close the loop and feed repayment outcomes back into marketing

This is the step many teams skip, or treat as a static autopsy. Your risk outcomes need to feed back into your acquisition strategy. Regularly, not quarterly.

Which traffic sources produce the worst DPD30 rates? Which lead aggregators send thin-file clusters? Which campaigns attract borrowers who take the loan and immediately go delinquent?

That data should be in the hands of your marketing team as soon as possible, not after the next portfolio review.

But a truly risk-adjusted loop doesn't just look backward at channel performance. It also reacts forward to macroeconomic signals.

A lender’s risk appetite is not fixed. When inflation squeezes disposable income or the cost of capital spikes, your margin for error shrinks.

The feedback loop must act as a dynamic dial. In a stable economy, you might tolerate a higher DPD30 from a high-volume channel to chase growth.

When macro indicators flash red, the risk team needs to automatically tighten the filters feeding back into your marketing engines. This prevents marketing from optimizing for a risk threshold that became obsolete the moment market conditions shifted.

By tying acquisition directly to both repayment outcomes and current economic realities, you ensure marketing isn't driving using yesterday's map.

Beyond CAC: The metrics that show borrower quality

Too many acquisition dashboards stop at conversion rate and CAC. Those are necessary but not sufficient. Here's a more complete view:

Tracking DPD30 by acquisition channel is particularly powerful. It tells you not just how much borrowers cost to acquire, but how well they perform. This is basically the only number that ultimately determines whether your CAC was justified.

What actually works once the model goes live

The framework only matters if it survives contact with real data, real vendors, and real regulatory scrutiny.

Backtesting on real borrower history before launch

Before integrating any new data source like alternative credit signals from digital footprint providers run a retrospective test on a meaningful historical sample. Small samples are unreliable here.

A 500-application test can look statistically promising and still fail to represent your actual borrower population. I'd recommend a minimum of 10,000-20,000 applications with at least 6 months of performance data before drawing conclusions about predictive lift.

Feature health monitoring and vendor risk

Once you've integrated a data source, don't assume it stays stable. Vendors change their data pipelines. Coverage degrades. A signal that was predictive 18 months ago might now be noisy or biased.

Build feature health monitoring into your model ops workflow. Track:

- Coverage rate (what % of applications return a value)

- Distribution drift (is the signal shifting over time)

- Predictive stability (does the signal still correlate with performance)

Vendor dependence is a real operational risk. Where possible, avoid building models that rely on a single alternative data source with no fallback.

Staying compliant in the EU context

If you operate in the EU, your acquisition and decisioning process sits squarely within GDPR and the AI Act's emerging requirements for automated decision-making.

This means explainability isn't optional. It's a regulatory expectation.

Compliance cannot sit outside the acquisition workflow. It has to be built into the data layer, the decisioning logic, and the explanations a lender can give afterward.

That is one reason we designed RiskSeal’s API with these safeguards as defaults. Explainable AI is part of the output, not an afterthought.

Data protection is supported by ISO 27001 certification. Compliance coverage includes the EU’s GDPR, Mexico’s LFPDPPP, and other applicable local laws and regulations.

For lenders, this matters because regulatory readiness should not depend on manual cleanup after a model goes live. Every signal used in decisioning should be traceable. Every outcome should be explainable.

And every integration should make it easier, not harder, to prove that growth is happening responsibly.

Smarter customer acquisition in banking for healthier loan books

Growing originations and maintaining portfolio quality are not opposing goals, but they require deliberate design.

The lenders I've seen do this well treat customer acquisition in banking as a risk function from the very first touchpoint, not just a marketing exercise.

Build the feedback loop, track the right metrics, test rigorously before you scale, and keep compliance in your architecture from day one. That's how you grow a loan book you're actually proud of.

See more

Alright, you've changed your scorecards by using alternative data. How can you check if they work well? What metrics you should measure? Check out the article.

The press release about RiskSeal and RNDpoint partnership to provide digital lending organizations with detailed digital profiles of borrowers.

Uncover how data leakage distorts credit models and why alternative data carries a different risk profile.