How to Accurately Score Gen Z Borrowers

Discover why traditional credit models miss Gen Z borrowers and how alternative data helps lenders score them accurately.

Gen Z is entering the credit market at scale, but the system still struggles to assess them. Their financial behavior looks responsible, yet often remains invisible to traditional models.

This creates a growing gap between how risk is measured and how money is actually managed today leaving lenders with a visibility problem.

In this article, I break down what actually drives Gen Z's financial behavior and how digital footprint analysis can help lenders make better decisions without relaxing risk standards.

Gen Z’s financial mindset compared to other generations

Gen Z approaches money with a strong sense of purpose.

They often choose where to work and spend based on values, not just income. Financial decisions reflect long-term priorities, not short-term gains.

They also prioritize stability more than previous generations. Many grew up watching economic uncertainty firsthand.

As a result, people born between 1997 and 2008 focus on saving, liquidity, and avoiding unnecessary financial exposure.

Of course, no generation fits into a perfect box. But these patterns come from what our team sees every day when working with fintechs and BNPL providers serving younger borrowers.

For Gen Z, money is a tool for flexibility. It enables freedom, not status. This mindset shapes how they interact with credit and financial institutions.

How Gen Z borrows: Non-traditional by design

Gen Z tends to avoid traditional credit products. Credit cards and long-term loans often feel rigid and expensive. Instead, they prefer structures that are predictable and easier to control.

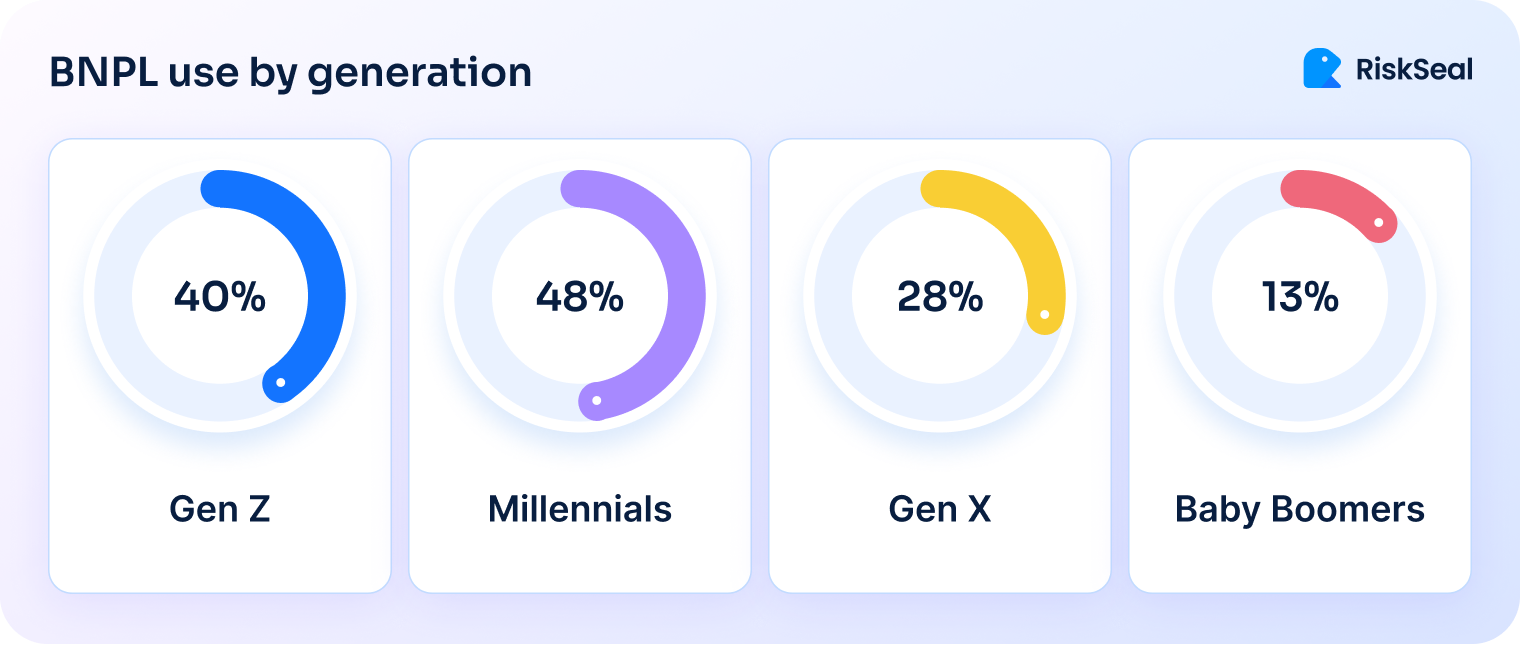

Buy Now, Pay Later has become a natural fit. Just in 2025, 44% of younger borrowers used buy-now-pay-later services. This is close to 30 million people in the U.S.

It offers short-term commitments and clear repayment terms. This aligns better with how they plan and manage expenses.

Here’s how BNPL usage differs across generations, according to Empower data:

They also evaluate borrowing through a return-on-investment lens. Whether it is education or financing a purchase, the question is simple: does this make financial sense over time?

Student loans highlight how financial pressure has changed across generations. Fewer Gen Z borrowers take on this debt compared to Millennials.

In 2023, 34% of Gen Z aged 22-24 had student loans, while 49% of Millennials did at the same age in 2013.

At the same time, the cost burden has increased. Gen Z borrowers aged 20-25 held an average balance of $20,900.

After adjusting for inflation, this is about 13% higher than what Millennials carried at that age.

This early exposure shapes borrowing behavior. Many Gen Z borrowers approach credit with more caution. They prefer smaller, more predictable commitments that feel easier to manage.

Gen Z expectations in a digital-first financial world

Gen Z interacts with money through digital-first environments. Mobile apps are the default, not an added feature. Every step, from application to repayment, is expected to happen seamlessly on a phone.

Financial learning also happens differently. Platforms like TikTok and YouTube shape how this generation understands credit and budgeting.

This leads to faster adoption of new tools, but also more diverse financial behavior patterns.

Income structures add another layer. Many combine freelance work, side hustles, and full-time roles. Cash flow can vary month to month, but this does not automatically signal higher risk.

Against this backdrop, expectations from lenders are evolving.

Speed and instant access

Speed is no longer a differentiator. It is expected at every stage.

Borrowers want loan decisions in minutes, not days. Once approved, funds should arrive instantly. Any delay feels outdated in a real-time digital environment.

Clear and transparent communication

Transparency plays a central role in trust.

Borrowers expect simple pricing and no hidden fees. They prefer clear, direct language over complex financial terms.

Real-time visibility into balances and repayments is also becoming standard.

According to The Financial Brand, 48% of Gen Z borrowers struggle to remember their payment due dates.

At the same time, 51% say reminders with embedded payment options would help them stay on track.

Flexible repayment structures

Fixed repayment schedules do not always match modern income patterns.

Many borrowers expect to adjust payments when income fluctuates. Options like pausing or rescheduling payments provide a sense of control.

This is especially important for those with non-linear earnings.

Recognition of real financial behavior

A single score often feels too limited.

Borrowers expect lenders to consider a broader financial picture. This includes cash flow, alternative data, and non-traditional income sources.

They want systems that reflect how they actually manage money.

Alignment with values and experience

The relationship with financial institutions is becoming more selective.

Many borrowers care about how lenders operate, not just what they offer. At the same time, they expect a balance between automation and human support when needed.

The structural limits of traditional credit bureaus

Credit bureaus remain the backbone of modern lending. However, their design reflects a different economic reality – one where financial behavior followed more predictable patterns.

As new borrower profiles emerge, especially among younger segments, gaps in visibility become more apparent:

- History-first logic. Traditional models rely heavily on past borrowing activity. If a borrower has not used credit products, there is little to assess.

This creates a visibility gap for financially responsible individuals who simply avoided traditional debt.

- Product-bound signals. Creditworthiness is tied to specific financial instruments like credit cards or installment loans.

Payments outside these products often remain invisible, even when they reflect consistent financial discipline.

- Income rigidity. Stable, employer-based income remains a core assumption.

Variable income streams, even when sufficient and recurring, are harder to interpret within existing models.

- Negative reporting bias. Many systems capture missed payments more reliably than positive behavior.

For example, telecom or utility payments often appear only after delinquency, not during consistent on-time performance.

- Static snapshot approach. Scores typically reflect a fixed point in time.

They may not fully capture improving financial behavior or recent changes in stability, especially for newer borrowers.

- High sensitivity to limited data. When profiles contain only a few records, each data point carries more weight.

A single error or anomaly can significantly affect outcomes.

These limitations do not point to a failure of the system. They reflect its original purpose and constraints.

The opportunity lies in complementing traditional data with broader signals that improve visibility without compromising risk standards.

How alternative credit scoring helps fintechs assess Gen Z borrowers

Alternative credit scoring does not replace traditional models. It extends them with real-world signals that improve visibility where standard data is limited.

This helps lenders assess Gen Z borrowers with more context, not more risk.

According to Artem Lalaiants, a digital credit scoring expert, modern scoring models rely on behavioral and digital signals that reflect how people actually manage money today.

- Digital footprint signals. Email age, phone stability, and online account history help confirm identity and consistency. These signals are especially useful when formal credit history is limited.

- Everyday payment behavior. Rent, utilities, and subscriptions show real financial discipline. Consistent payments for services like Netflix or mobile plans indicate planning and solvency.

- Cash flow visibility. Transaction data shows how income and expenses interact over time. This helps lenders understand affordability, even with variable or gig-based income.

- Modern credit usage. BNPL activity adds context to short-term borrowing behavior. When used responsibly, it signals structured and predictable repayment habits.

- Behavioral patterns. Spending habits, recurring payments, and income frequency reveal financial stability. These patterns often highlight early signs of stress before defaults occur.

- Device and identity signals. Device type, geolocation consistency, and session behavior help confirm authenticity. This adds an extra layer of confidence during onboarding and decisioning.

At the same time, using alternative data based on digital footprint requires balance. Lenders need clear logic, explainable models, and strong data governance.

When done right, these signals improve approval rates while maintaining risk standards and compliance.

How RiskSeal supports this shift

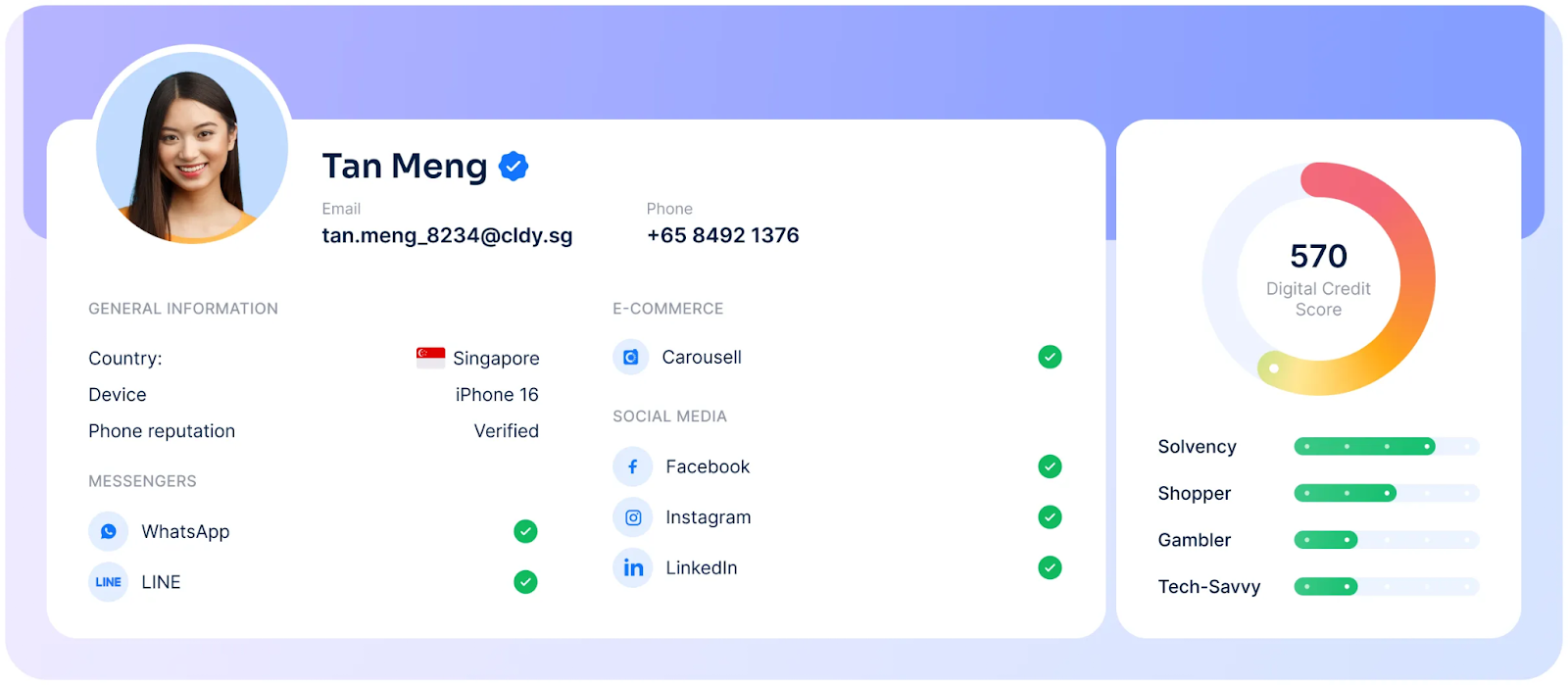

RiskSeal helps lenders see what traditional bureaus do not capture. It adds a layer of alternative credit data that uncover real borrower behavior beyond bureau records.

The platform focuses on high-coverage local data sources across multiple markets.

These signals do not overlap with bureau data. Instead, they add new, non-correlated inputs that improve model performance and segmentation.

RiskSeal’s digital footprint data goes deeper than standard enrichment. It includes signals like:

- email age

- phone number longevity

- account activity

- subscription patterns

These indicators, alongside with other 400+ data points per applicant, help distinguish real, active users from low-intent or synthetic profiles.

The platform works especially well for thin-file and first-time borrowers. It helps lenders separate low-risk applicants from unknown ones without relaxing risk policies.

All data is fully compliant and aligned with regulatory requirements. This gives risk and compliance teams confidence when using alternative data in production.

For lenders, the outcome is measurable. Stronger Gini and AUC, higher approval rates, and lower default risk.

Not by replacing existing models, but by strengthening them with data they did not have before.

Wrapping up

Gen Z is not difficult to assess. They are simply different from what legacy models expect.

As financial behavior evolves, risk assessment must evolve with it. Expanding the data lens allows lenders to see more, not assume more.

Those who adapt will not only improve decisioning, but also reach a generation that is ready to engage on its own terms.

See more

.webp)

Learn to identify high-value borrowers early: pretransaction signals predict lifetime value and reduce default risk.

.webp)

Discover how expanding financial inclusion and lending to overlooked borrowers can drive profits and transform lives around the world.

Learn key behavioral data types, real-world use cases, and benefits for lenders.