How Not to Blow Your Credit Portfolio This Black Friday

Learn how to prepare your business for Black Friday by using real-time credit risk signals that enrich scoring and protect against rising defaults.

Black Friday unleashes a wave of loan applications – an unmatched growth opportunity for lenders.

But it’s also prime time for fraudsters and impulsive borrowers, creating a high-stakes environment for risk teams.

How can you grow approvals without letting risk grow too? This article breaks down modern data strategies that help you approve more and risk less.

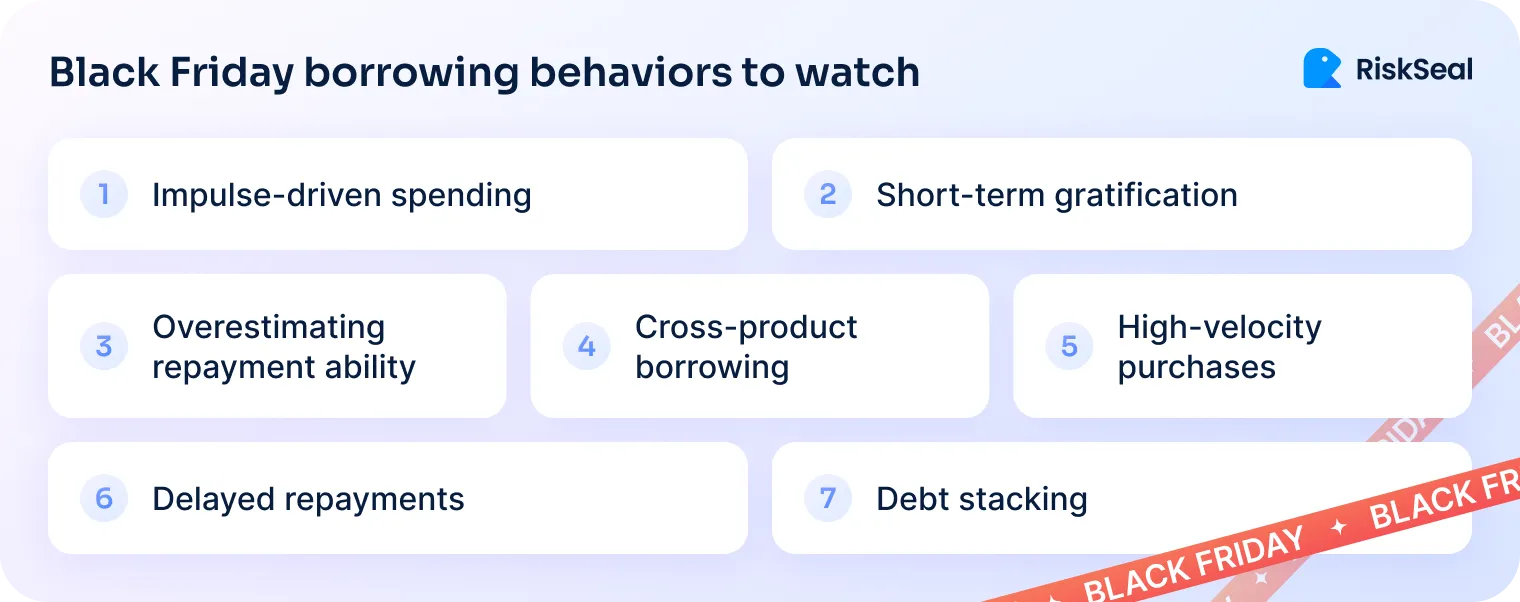

Black Friday borrowing patterns lenders must be ready for

Black Friday isn't just a retail boom. It's also a borrowing boom.

And it carries predictable patterns that impact credit portfolios well into the new year.

Behavioral drivers like short-term gratification fuel this spending. Consumers often underestimate the long-term cost of their purchases.

This leads to significant debt accumulation. The data from recent holiday seasons paints a clear picture of the borrowing patterns around Black Friday:

- Impulse-driven debt. The average Black Friday debt reached $600 per shopper in 2023.

- Repayment struggles. Around 35% of these borrowers failed to pay off their holiday balances within three months.

- Delinquency spikes. This spending directly contributed to an 8% rise in delinquencies seen in Q1 2024.

The surge in BNPL is a clear example of how fast holiday lending moves.

These platforms offer instant approvals, which is why they fueled nearly $10 billion in Black Friday sales in 2023.

This growth creates both opportunity and risk.

On one hand, BNPL expands access to credit at scale. On the other, it makes accurate credit risk scoring for BNPL essential during peak shopping periods.

Black Friday floods the pipeline with applications that need decisions in seconds.

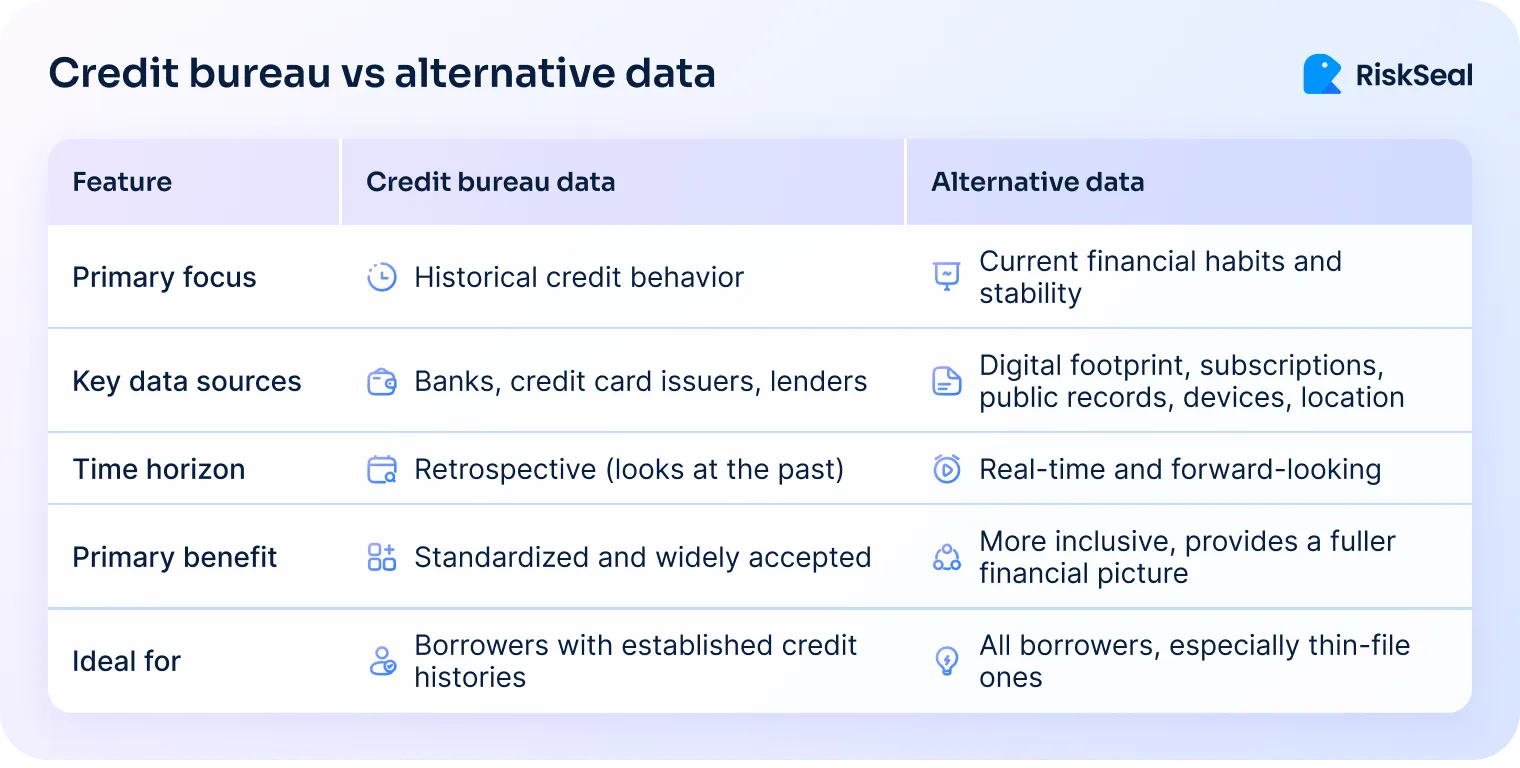

Traditional credit models can’t keep up. Bureau data is slow to update and offers limited insight into new or underserved borrowers

That leaves lenders with a difficult choice. Approve too quickly and risk rising fraud and defaults. Approve too cautiously and lose valuable business to competitors.

5 credit portfolio risks lenders can’t ignore when preparing for Black Friday

The seasonal surge in borrowing introduces five critical risks for lenders.

These risks compound over time and put pressure on portfolio performance as the new year begins.

- Rising loan defaults. Holiday-driven borrowing often leads to higher default rates in the following months.

- Delayed repayments. Prolonged repayment timelines increase exposure to non-performing loans and strain collections.

- Portfolio delinquency spikes. Q1 consistently brings a predictable rise in delinquency rates as holiday balances come due.

- Cross-product overextension. Borrowers often layer debt across different credit providers, raising the likelihood of multi-account defaults.

- Erosion of portfolio health. Taken together, these trends weaken overall credit portfolio performance.

With delinquencies approaching five-year highs in early 2025, lenders face pressure on both profitability and resilience.

The short-term revenue boost from holiday lending can quickly be offset by long-term credit losses and operational strain.

.svg)

How to prepare your business for Black Friday

Traditional bureau data still plays a role in risk assessment. But during fast-moving periods like Black Friday, it’s too slow and incomplete.

Credit reports often take 30-60 days to reflect new obligations or missed payments. This leaves a blind spot when activity spikes.

New arrivals, younger borrowers, or those who avoid traditional credit may be strong candidates, but bureau-only models overlook them.

Relying solely on scores risks unnecessary rejections. Real-time alternative data closes this gap.

Digital signals allow lenders to make faster, more accurate, and more inclusive decisions at scale.

Fight application fraud before the damage is done

Fraudsters often rely on volume. They submit large numbers of fake applications, hoping some will bypass outdated systems.

This clogs pipelines, wastes underwriting resources, and increases the risk of funding fraudulent accounts.

Real-time signals help filter these applications instantly:

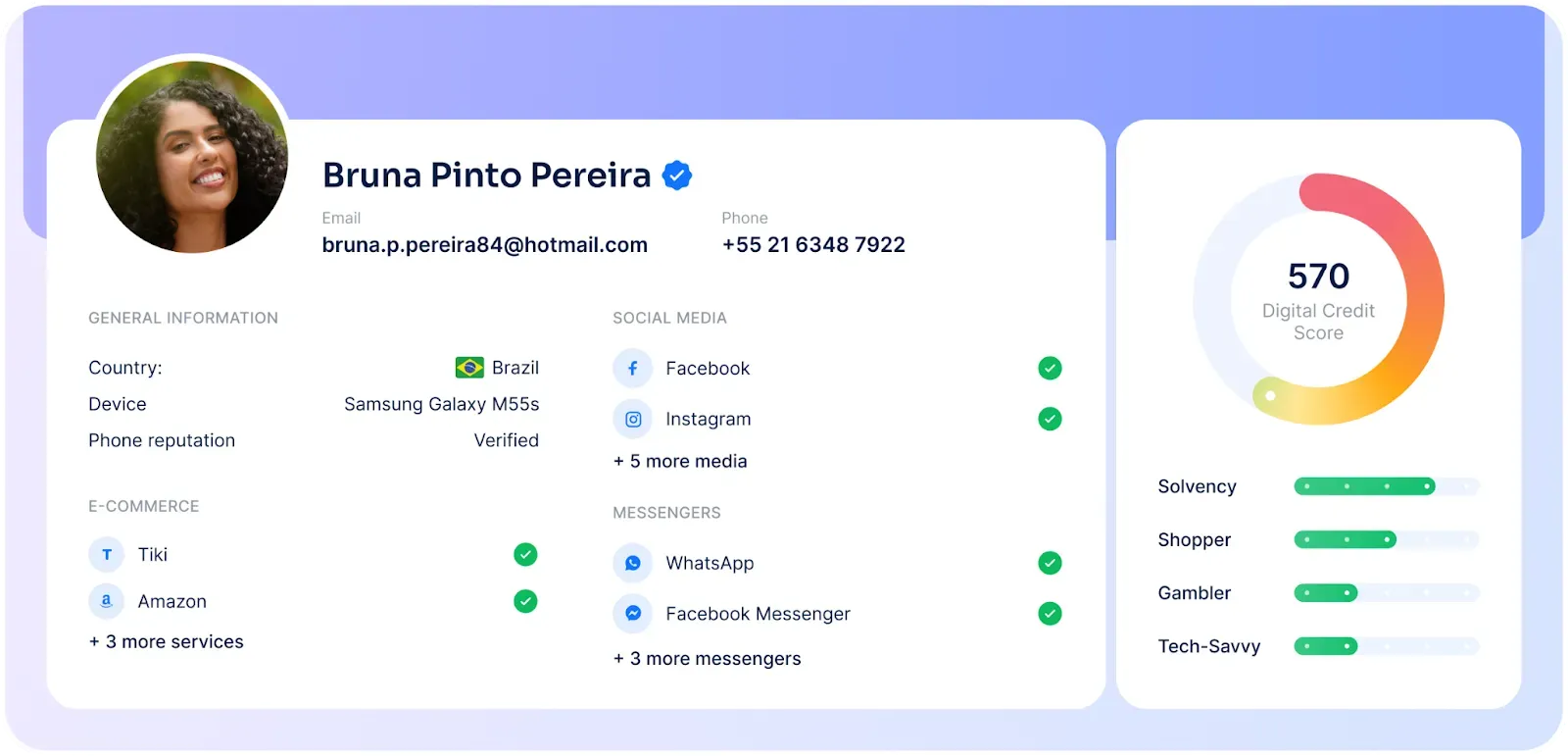

- Email and phone data. Legitimate borrowers tend to use long-standing email addresses and numbers. RiskSeal includes email age as a key trust signal. Newly created emails often point to high-risk borrower signs.

- IP and device alignment. A borrower’s IP should match their stated location. High-risk IPs (proxy, VPN, Tor) or mismatched device settings point to fraud.

- Browser and account behavior. Automated scripts leave traces, like odd copy-paste behavior or virtual machine use. These patterns separate bots from real applicants.

Spot identity theft and synthetic identities early

This form of fraud is more advanced. Not every fraud detection solution for lenders can spot it.

Fraudsters may use stolen personal data (identity theft) or mix real and fake details to create synthetic profiles. These can look convincing, even backed by fabricated documents.

Their weakness is the lack of an authentic, long-term digital history. Real people leave footprints that are difficult to fake:

- Digital footprint cohesion. Genuine applicants show consistent connections between name, phone, email, and online accounts. Among our clients, we consistently see that adding digital footprint to scorecards enhances predictive power.

- Social connections and history. Authentic profiles have natural networks and activity over the years. Synthetics often show newly created accounts with little depth.

- Profile authenticity. Stock or recycled avatars are common in fakes. Real users leave trails through profile pics, consistent posting, and human followers that fraudsters can’t mimic.

Detect loan stacking in real time

Loan stacking is when a borrower applies for credit from several lenders within days.

Bureau data won’t capture this in real time. This leaves lenders blind to overlapping obligations.

Key signals to watch:

- Shared identifiers. Reuse of the same phone number, email, IP, or device ID across multiple applications signals stacking. RiskSeal maintains a cross-client database, so we instantly detect repeated applications across lenders or signs of prior default.

- Cross-lender intelligence. Networks that aggregate application data can flag repeated identifiers across institutions in real time.

- Behavioral clustering. Applications from different “borrowers” tied to the same device or IP may indicate coordinated activity.

Recognize impulsive overspending and unreliable borrowers

Not all high-risk cases are fraud. Some borrowers simply overspend and become unreliable payers.

Credit scores were never built to track behavioral risks. This means lenders need other signals to assess spending and repayment reliability.

Digital signals provide a clearer view:

- Subscription patterns. Frequent sign-ups and cancellations suggest unstable cash flow. RiskSeal data shows a clear correlation between ongoing subscriptions, like Disney+ or Spotify, and higher repayment reliability.

- Low digital maturity. Limited online activity or few digital accounts may correlate with weaker financial management.

- Unstable digital habits. Constantly changing emails, phones, or devices without a clear reason often maps to higher repayment risk.

Catch hidden defaults before they escalate

Collections teams need early warnings before defaults surface in bureau data. By the time a missed payment shows up, it’s already late.

Digital behavior can flag distress earlier:

- Reduced online activity. A sudden drop-off in normal digital behavior suggests disengagement.

- Service cancellations. Canceling multiple subscriptions at once often signals cost-cutting under financial strain.

- Disappearing digital traces. Deactivating profiles, abandoning emails, or unstable device usage makes borrowers harder to reach. It’s a strong sign of looming payment avoidance.

In short, bureau data shows the past. Real-time digital signals reveal the present.

For lenders, combining both is key to managing holiday-driven risk without losing valuable business.

Expert tips for using risk signals in credit scoring this Black Friday

At RiskSeal, we’ve seen firsthand what works – and what doesn’t – when it comes to credit scoring during peak lending seasons.

Below are our top recommendations to help you make smarter, faster decisions using real-time data.

Done right, this approach strengthens risk models and uncovers threats that traditional scoring often misses.

Integrate real-time checks at application

Real-time checks are critical during Black Friday.

Don’t wait for bureau updates that lag weeks behind. Use live email, phone, device, and IP data to flag fraud before underwriting even begins.

Combine this with behavioral and financial signals such as subscription patterns and spending habits.

This layered approach enriches credit risk scoring models rather than replacing traditional scores. This isn’t just theory. It shows up clearly in the data.

The chart below compares three models: one built on traditional bureau data only, one on alternative digital data only, and one that combines both.

Make sure new signals actually add value

Adding alternative data should improve scoring accuracy, not complicate it. That’s why testing at scale is essential.

Thousands of applications need to be run through enriched models before drawing conclusions. Serious providers make this process easier by offering Proof-of-Concept programs.

At RiskSeal, we provide PoC for free, allowing lenders to see how new signals perform on real borrower data before committing to a rollout.

This ensures that every new layer of data adds measurable value to the decisioning process.

Assign weight to risk indicators

Not every signal has the same level of importance. Some are strong predictors of fraud or default, while others may only suggest minor risk.

Credit models should assign weight to these signals instead of treating them all equally. This helps downgrade borderline applicants rather than rejecting them outright.

Careful calibration reduces false declines while keeping portfolio risk under control. Done well, this turns alternative data into a precise tool rather than a blunt filter.

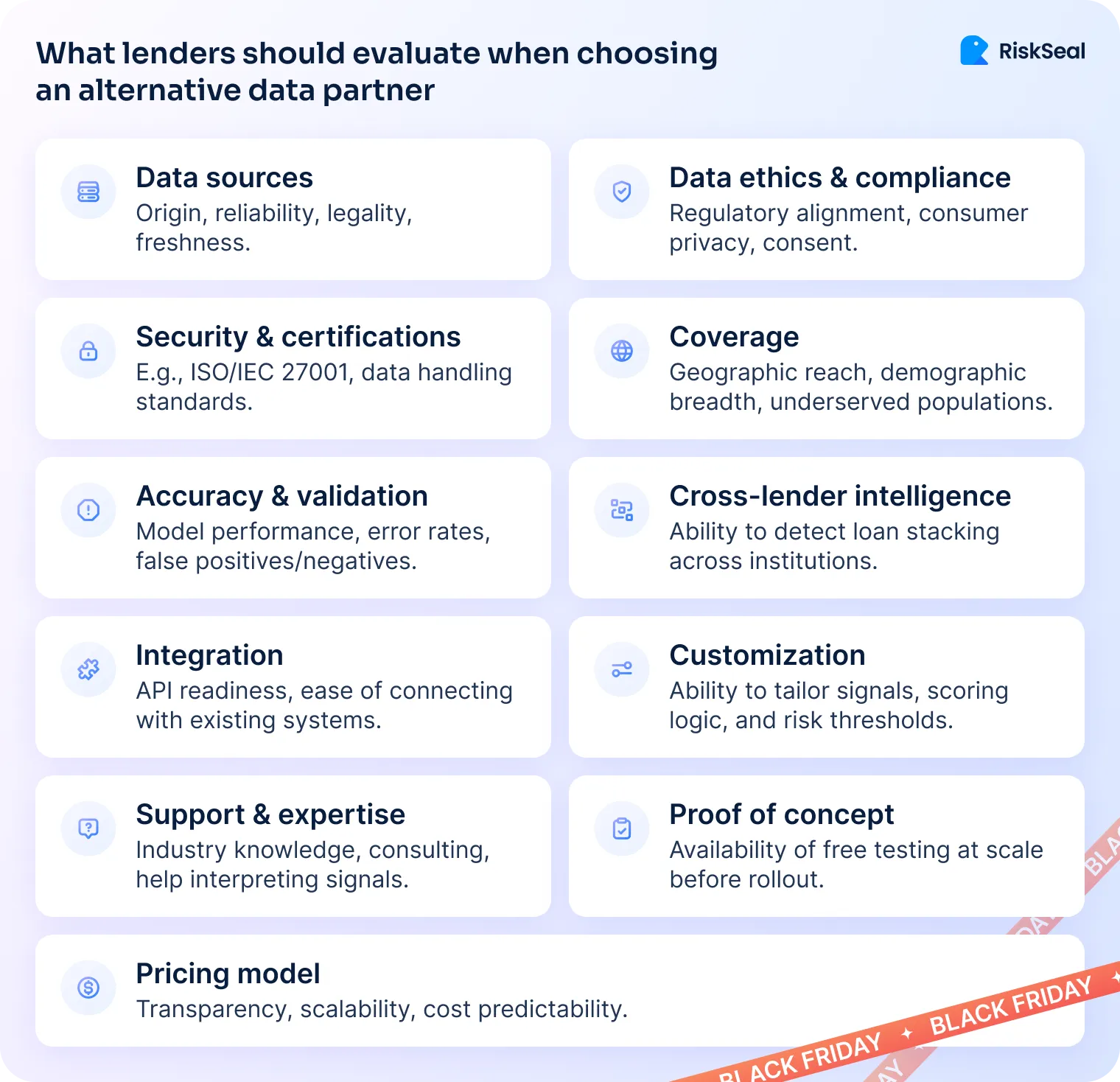

Integrate the right data partner

Even the best signals lose value if they’re hard to apply. Integration should be smooth, fast, and compliant with industry rules.

An experienced provider will offer APIs that connect directly with existing workflows. They’ll also help interpret signals and fine-tune thresholds so lenders can act on insights, not just raw data.

The most valuable partners provide cross-lender intelligence, helping detect loan stacking across institutions in real time.

Choosing a provider with proven expertise ensures the data works for your business, not against it.

RiskSeal’s approach to Black Friday readiness

RiskSeal helps lenders handle high volumes of applications without sacrificing risk control. Our API delivers more than 400 real-time data points analyzed for every applicant.

We track alternative signals automatically, removing the burden from risk teams.

This means lenders get clear, actionable insights without the noise, and can focus on decisions that matter.

RiskSeal is ISO/IEC 27001:2022 certified, ensuring the highest standards of security.

Our platform helps credit providers interpret the data, turning raw signals into actionable insights.

We offer a free proof of concept, so you can see real impact before scaling.

Results we deliver to our partners include:

- 2x increase in approval rates without raising risk exposure

- Up to 25% decrease in default rates

- 98% coverage of underserved borrowers

- 5-second real-time scoring for seamless decisioning at scale

With RiskSeal, lenders can maximize approvals during Black Friday while maintaining strong portfolio health into the new year.

Final thoughts

The annual surge in holiday borrowing and the accompanying fraud attempts are not a surprise. They are a predictable cycle.

For risk teams, this predictability is a key advantage. By moving beyond slow, traditional credit data, you can manage these seasonal patterns proactively.

Leveraging real-time alternative data and adaptive scoring models turns this challenge into a growth opportunity.

It allows you to filter out fraud instantly while confidently approving more creditworthy thin-file applicants.

FAQ

How can a platform like RiskSeal help risk teams prepare lending websites for Black Friday?

RiskSeal shifts teams from reactive to proactive. Instead of relying on delayed bureau data, it uses real-time digital signals to assess risk at the application stage.

Lenders can instantly block fraud, spot synthetic identities, and detect loan stacking across institutions.

The result: more automation, fewer manual reviews, and safer growth through faster approvals.

Why can't traditional credit bureau data alone handle Black Friday's challenges?

Bureau data has two main gaps during peak lending periods.

First is latency: updates often lag 30–60 days, leaving lenders blind to recent borrowing. Second is coverage: it provides little insight into credit-averse or new-to-credit applicants.

The result is lost revenue from unnecessary rejections and weaker risk control when relying on outdated information.

What is the single most important type of risk to monitor during the holiday season?

Loan stacking is the most urgent risk during Black Friday. In a matter of hours, a single borrower can take on multiple loans across different lenders.

Traditional systems don’t catch this in real time. Monitoring digital identifiers like email, phone numbers, device, and IP is the most effective way to prevent cascading defaults.

See more

.webp)

Discover how alternative credit scoring helps BNPL providers mitigate risk and enhance accessibility.

.webp)

Learn how risk scoring enhances lending by assessing credit risk using traditional & alternative data.

.webp)

Discover how social media profiling enhances credit risk management by analyzing digital footprints.