From Banks to Marketplaces: How Consumer Credit Is Changing

Discover how tech-first lending models are replacing bureau-only scoring with speed, alternative data, and smarter borrower context.

The loan market is no longer built around one branch, one bureau file, and one bank decision.

Borrowers now find credit inside marketplaces, apps, e-wallets, and platforms they already use. That shift is making lending faster and more accessible.

But it also raises a harder question: how do lenders say yes to more people without losing sight of risk? Let's break it down.

Changing flows: where and how borrowers find funding today

The easiest way to see how consumer credit is changing is to look at where borrowers are currently getting the loans they need.

Consumer credit marketplaces and P2P lending platforms

These platforms connect borrowers with lenders, investors, or other capital providers outside the traditional bank-first model.

While a bank typically makes lending decisions using its own balance sheet and a bureau-centric risk assessment process, a credit marketplace operates differently.

Instead of funding loans directly, the platform acts as an intermediary that matches borrowers with individuals or institutions willing to provide capital. In this model, the marketplace becomes the trust layer between both sides, helping facilitate and manage the entire lending journey.

Many platforms handle application processing, borrower assessment, investor matching, risk grading, fraud checks, loan pricing, and repayment management within a single ecosystem. This creates a more efficient and scalable lending environment for all participants.

For borrowers, the benefit is a faster, more flexible path to funding, often through a fully digital application process.

For lenders and investors, the value comes from access to a broader pool of potential borrowers, supported by platform-level tools for underwriting, risk management, fraud prevention, and portfolio monitoring.

This approach makes credit more accessible. Borrowers who may not fit a bank's standard lending policy can still be assessed, appropriately priced, and matched with a funding source that aligns with their risk profile.

Here are a few examples of how this model already works across different markets:

Afluenta

Afluenta is an Argentine fintech company using AI to power P2P loans. It operates across Argentina, Mexico, and Peru.

Prestadero

A Mexican P2P lending platform. Prestadero connects people who need a loan with people who want to invest.

CLIX

CLIX is a credit marketplace/people-to-people lending platform. Interesting because it focuses on overlooked and credit-invisible borrowers. It is not just selling "faster loans."

It is working towards creating a more open credit ecosystem where borrowers and lenders connect more directly.

auxmoney

A European digital consumer credit platform. Strong example because auxmoney positions itself around assessing borrowers more individually than banks.

Younited

Younited is a digital consumer credit platform with a regulated credit institution model, investor funding angle, APIs, and AI-based instant credit.

These platforms challenge the idea that credit must always flow through one bank and one bureau-based decision. Their real value is matching, trust-building, and flexible access to funding.

Embedded credit marketplaces

Here, the borrower doesn't go looking for a loan. The loan shows up inside a platform they already use.

Credit can be embedded into e-commerce, payroll apps, neobanks, merchant platforms, SaaS tools, gig platforms, and digital wallets.

Lendflow

Embedded credit infrastructure. It helps other platforms add credit products, lender connections, onboarding, and decisioning without building it all from scratch.

Mercado Pago – Meses sin Tarjeta

Mercado Pago's credit line lets Mercado Libre shoppers pay in installments without a credit card. The financing offer appears right at checkout, inside the Credits section they already use.

Addi

A Colombia-born, LATAM-wide BNPL platform. Shoppers can buy in installments without a card, and Addi even runs its own marketplace of partner brands for this.

In each case, credit moves out of a separate banking journey and into the customer's everyday digital experience.

Community lenders built on local trust

Community lenders differ from broad marketplaces because they're built around a specific local, social, nonprofit, or member-based group. The lending model here is relationship-driven, not application-driven.

A traditional lender often treats a borrower as a file. A community lender is more likely to see them as part of a group it already knows.

This category generally splits into two broad types:

- Credit unions – member-owned institutions, often tied to a region or an employer.

- Local microfinance institutions – common in emerging markets, where borrower relationships and local knowledge still carry real weight.

A few real-world platforms show what this looks like in practice.

LiftFund

LiftFund is a U.S. nonprofit CDFI. It supports small business owners who don't qualify for traditional funding, pairing affordable loans with real support services.

Community Forward Fund

A Canadian community finance example. It lends to nonprofits, charities, and social enterprises, with financing built around organizations that serve their own communities.

Community lenders aren't just an alternative distribution channel. Their advantage is local trust. But even relationship-based lending needs stronger data and fraud checks to scale responsibly.

Impact and priority-sector lending platforms

These platforms focus on borrowers and sectors traditional finance often skips. That includes:

- microentrepreneurs

- MSMEs

- informal workers

- rural borrowers

- women (particularly in regions where access to formal financial services remains unequal)

- first-time borrowers and more

Their value is not only access to credit, but direction. They help funding reach people, businesses, and communities that may be economically important but too small, informal, or hard to assess for traditional banks.

For investors, this model also creates a clearer link between capital and impact. Money is not just placed into a loan book. It is directed toward specific sectors, markets, or borrower groups.

A few platforms show what this looks like in practice:

Mannjal

Mannjal represents priority-sector infrastructure built around MSME, agriculture, affordable housing, education, and green lending.

JUMO

JUMO is a plug-and-play infrastructure for data-driven financial products. It powers banks and telcos to reach entrepreneurs across emerging markets.

Tala

Tala is built specifically for thin-file borrowers in informal economies. Its data engine draws on lending performance data covering millions of customers, a genuinely AI-native approach to credit.

M-KOPA

M-KOPA finances smartphones and other assets for everyday earners in Africa through a pay-as-you-go model. Access to a device becomes a path into broader financial inclusion.

Kiva

Kiva fits here given its mission to expand financial access for underserved borrowers, refugees, and entrepreneurs.

Impact-led lending isn't about approving everyone. It's about finding responsible ways to serve people the traditional system fails to see clearly.

What tech-first lenders do differently

The difference is not just a better app or a faster form. The real shift is in how these lenders collect applicant context, assess risk, and decide who deserves access to credit.

1. They use richer borrower context

Tech-first lenders don't stop at bureau data. They look at who a person is and how they actually behave online.

This is where digital footprint analysis comes in. It's not OSINT or surveillance. It's the ethical analysis of consensually shared public information: emails, phone numbers, subscriptions, and web accounts.

For borrowers with no credit history, this data can work as a stand-alone decision tool.

For borrowers who do have a file, it adds real-time context on top of a static bureau record.

Email data shows how old an address is, what domain it uses, and whether it's ever appeared in a breach. Phone data confirms if a number is real, active, and in use on apps like WhatsApp or Telegram.

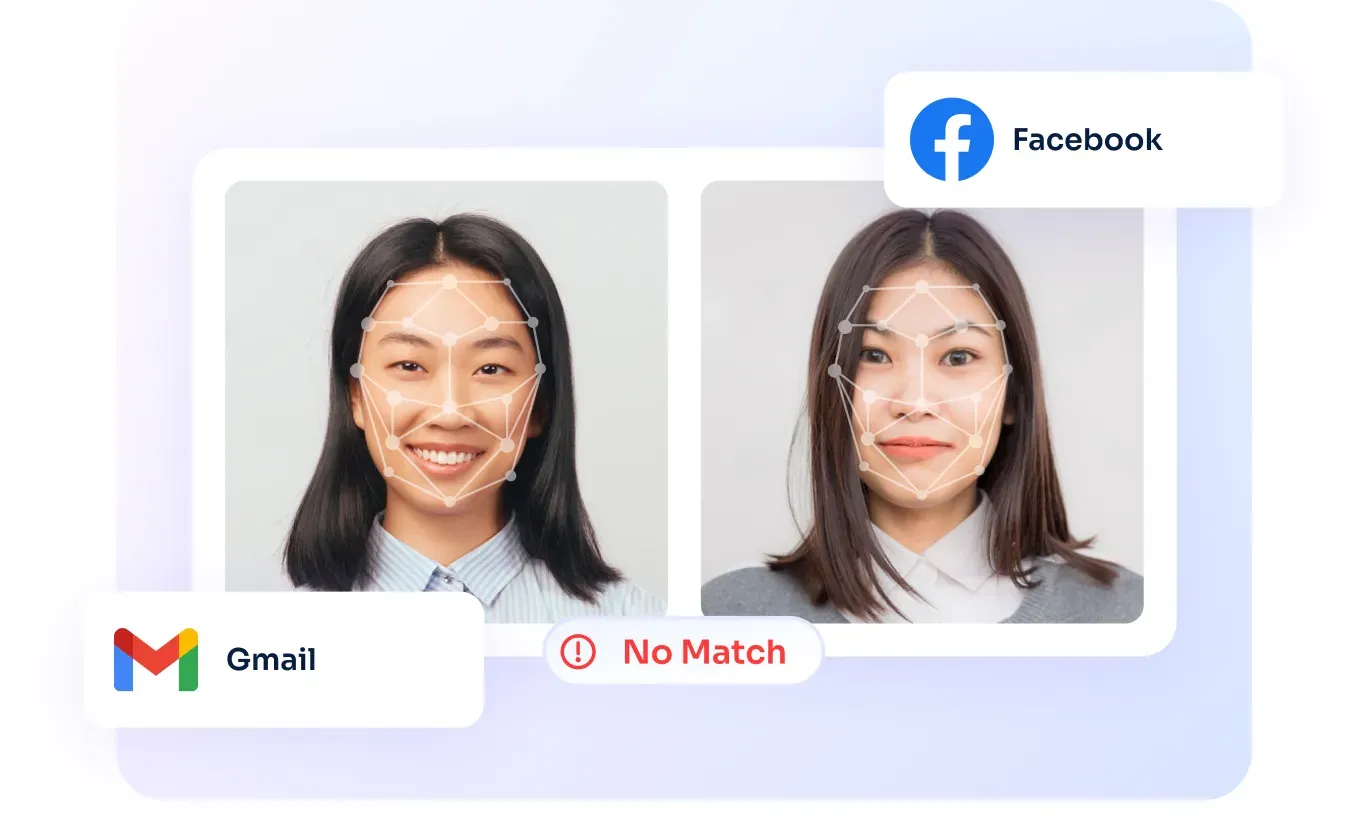

AI-based identity checks, like name matching and face comparison across profiles, confirm the same person shows up consistently everywhere.

Social signals from Facebook, LinkedIn, or Instagram reflect digital maturity and consistency. Shopping activity on Amazon, Mercado Libre, or Walmart shows account age and everyday purchase behavior.

Subscriptions to services like Netflix or Spotify can hint at budgeting habits. Signals from Apple, Google, or Zoho accounts round out the picture of long-term digital engagement.

And IP and network data flag unusual access patterns, like rapid movements across the globe or switching between too many devices.

2. They build decision engines that prioritize the applicant's time

Instant approval used to sound like a marketing exaggeration. For BNPL and many embedded credit products, it is now the baseline expectation.

Getting there takes real work on the back end. Teams need faster data pipelines, cleaner scoring logic, and fraud checks that run in milliseconds, not minutes.

Credit risk assessment has to move at the same speed without cutting corners. That is a harder balance than it sounds, especially under regulatory scrutiny.

Speed only matters if the existing decision engine stays stable while it happens. Ripping out a working system to add new signals is risky, and few credit scoring teams are willing to take it.

Whether new data strengthens the decision engine or complicates it depends heavily on the provider’s integration approach.

A data partner should not only bring valuable additional signals, but also make them easy to test, integrate, and use safely inside the lender’s existing infrastructure.

That kind of layer sits alongside the current engine instead of replacing it. It lets teams validate new data, measure its impact, and expand gradually without touching the core system they already trust.

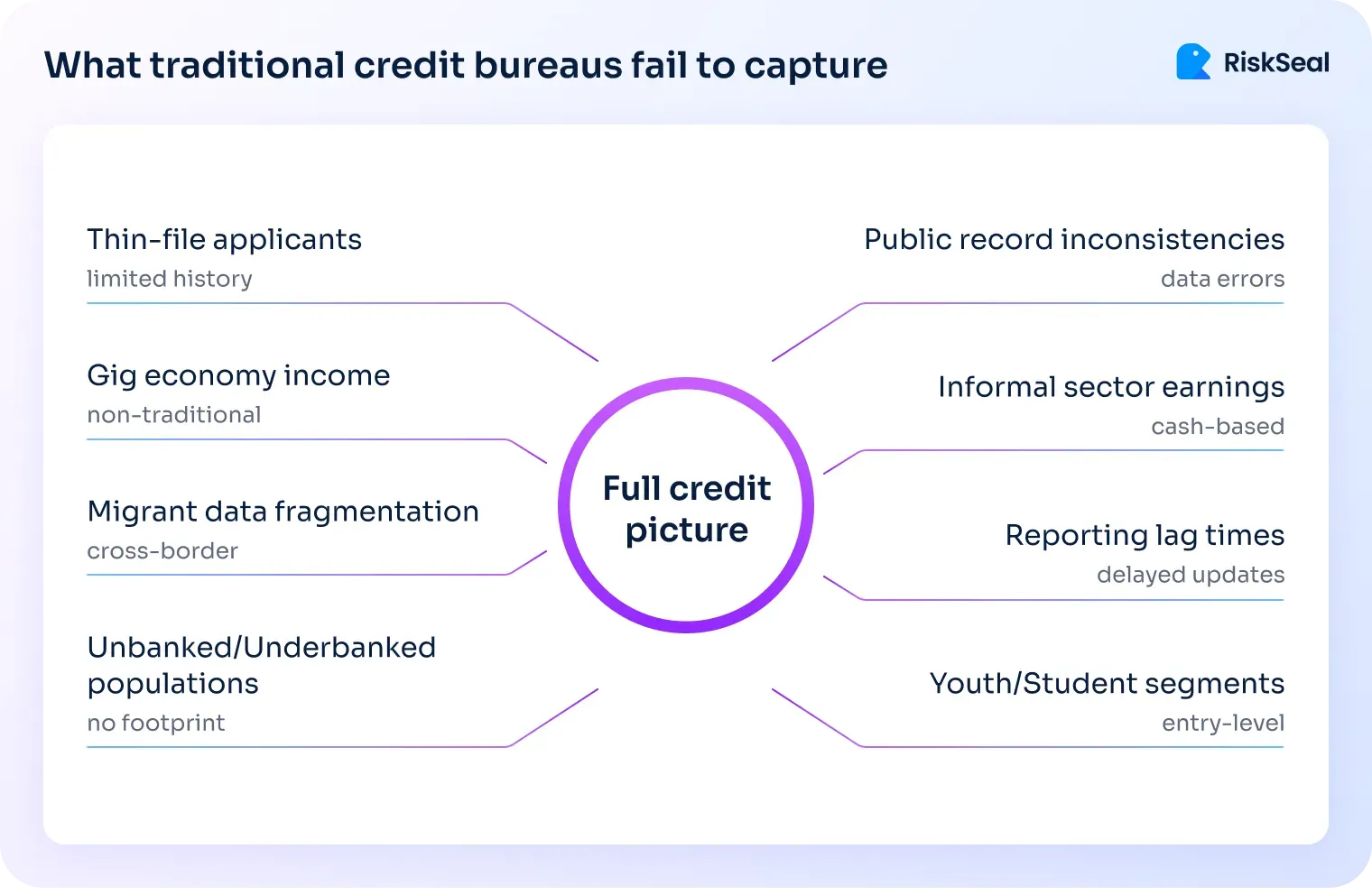

3. They are more open to credit-invisible borrowers

"Credit-invisible" sounds like it means risky. Often, it just means unmeasured.

Plenty of credit-invisible people are genuinely creditworthy, just for different reasons:

- New to credit. Younger borrowers or people early in their financial life simply haven't built a file yet.

- Deliberately debt-averse. Some people avoid going into debt and choose to save up before a purchase, which is discipline, not risk.

- Gig and cash-income workers. Their earnings are real and often stable, but don't always land in a traditional file.

- Recent immigrants. They may have a strong credit history abroad, but no record at all in their new country.

A bureau file can't tell any of these stories apart. It just sees an absence of data.

Traditional lenders, working from bureau data alone, tend to treat all of these people the same way. That usually means outright refusal, or an offer with a much higher interest rate than the person's actual risk would justify.

Tech-first lenders ask a sharper question before deciding. Is this applicant actually risky, or just missing from the file traditional systems rely on?

4. They build around platforms, not branches

Credit is moving into digital ecosystems, not staying tied to physical branches. That's a real shift from product-first, branch-first banking.

I think this shift makes more sense once you look at how people actually spend their day.

Screen time keeps climbing across every age group, and younger generations especially treat their phone as the default interface for almost everything.

Gen Z and younger millennials often spend more hours on a screen daily than older generations spend watching TV. Boomers use fewer hours overall, but even that gap keeps narrowing every year.

People now expect frictionless experiences everywhere, not just in banking. Food arrives with three taps, jobs get applied to from a phone, and nobody wants to fill out a paper form anymore.

That convenience comes at a cost: users are trusting more of their data to apps and websites than ever before. In my experience, that trust is given as a condition of getting anything done quickly. Financial institutions shouldn't waste it. User trust needs to be turned into decisions that feel fast, fair, and genuinely helpful to the person on the other end.

5. They treat risk infrastructure as a growth tool

Better risk data does more than block fraud. It helps lenders approve more good borrowers and lower manual review costs at the same time. It also helps match borrowers to the right product and serve overlooked segments responsibly. Good infrastructure protects lenders, investors, and platforms all at once.

This connects directly to customer acquisition cost, which most teams still treat as a marketing metric. In reality, a rejected applicant is wasted ad spend, and an abandoned application is no better.

Every blind rejection or unnecessary document request pushes a real cost back onto acquisition. Reducing those blind spots, risk infrastructure lowers CAC as a direct side effect, not just a metric.

Higher approval rates from the same traffic also mean CAC drops without touching the marketing budget at all. And when approved borrowers perform better too, lifetime value rises while acquisition cost stays flat, which is the combination every growth team is actually chasing.

How RiskSeal strengthens modern credit scoring infrastructure

I've seen too many good applicants get rejected simply because a model falls flat on people without an extensive bureau file. RiskSeal was built to close exactly that gap.

We help lending platforms add alternative credit data and digital footprint intelligence directly into existing risk workflows.

That means local, region-specific signals pulled from over 450 data points across 200-plus online sources.

Our coverage spans several layers of identity and behavior:

- Email intelligence: validity, age, domain type, and breach exposure

- Phone intelligence: activity status, carrier data, and messaging app presence

- IP and location signals: connection type, location consistency, and risk flags

- Digital identity checks: cross-platform name matching and profile consistency

- Fraud and masking indicators: early signs of synthetic or stolen identities

We turn all of this into an alternative risk score from 0 to 999, with explainable reasoning behind every number. Delivery is API-first, built for real-time decisioning, and integration typically takes just one day. This isn't only for thin-file applicants. Even when a person demonstrates a long credit history, the credit provider still benefits.

Because digital identity signals catch things a static bureau file simply can't, like stolen identities or subtle risk markers such as gambling registrations.

In practice, RiskSeal helps risk teams answer a few core questions:

- Is this applicant real?

- Is their identity consistent across platforms?

- Are there fraud or masking signals?

- Does their digital behavior look stable?

- Is this thin-file borrower actually risky, or just invisible to the bureau?

RiskSeal acts as a real-time alternative data layer. It's not a replacement for bureau data. It's an enrichment layer that turns limited borrower information into usable risk intelligence.

What comes next for smarter lending

Consumer credit is opening up. Borrowers now have more paths to a "yes" than a branch or a bureau file ever offered.

That freedom only holds up if risk visibility keeps pace with it. More access without better data is just a risk in disguise.

The lenders getting this right aren't approving more people blindly. They're seeing borrowers more clearly, thanks to signals a bureau file was never built to capture.

So this isn't really about traditional lending versus riskier lending. It's about finally seeing the borrowers who were there all along.

See more

.webp)

Discover how RiskSeal's digital scoring system uses alternative data sources to generate comprehensive credit profiles for potential borrowers.

Master the credit risk metrics that actually protect your portfolio. Learn how top fintechs track, interpret, and act on risk signals in 2026.

Discover the top risks BNPL providers must tackle, from fraud to thin files, to stay competitive and compliant in 2026.