6 Ways Alternative Data Reduces CAC in Digital Lending

Explore how alternative credit scoring reduces CAC by improving risk segmentation, fraud filtering, and approval quality.

Most lenders have already optimized ads, funnels, and onboarding. CAC is still stubbornly high.

In my experience, a big part of the leak happens inside the scoring layer. Not because traffic is bad, but because traditional data alone can’t evaluate a meaningful share of applicants.

It’s a credit decisioning issue. When risk teams fix it, CAC drops as a side effect.

Bureau-only credit risk scoring inflates CAC

Bureau data works well for borrowers with established credit histories. The problem is that a significant share of applicants still falls outside that coverage.

I am talking about thin-file and no-file users. In my experience, they can represent 30-45% of incoming applications in emerging markets like Brazil, Mexico, and Indonesia.

For context, even in a mature, credit-history-rich market like the US, scoring gaps still exist.

Around 9.8-10% of Americans are thin-file. And even among people who do have a credit score, about 16.3% are scored as poor.

People with poor credit (300-579) can still get approved. But it is harder, more expensive, and often comes with tighter limits.

And that “poor score” does not always mean the person is truly high-risk. It often means the bureau has limited context.

Bureau-based scoring hits many blind spots that trigger the same outcomes:

- rejecting the application outright

- requesting extra checks and documents

- routing the case to manual review and extending decision time

A rejected applicant is ad spend, creative budget, and conversion effort that produced nothing. An abandoned application is the same. This is how bureau-only decisioning adds to CAC.

Six ways alternative data helps reduce CAC

Customer acquisition cost isn’t just a marketing metric. It’s shaped by underwriting decisions, onboarding friction, fraud exposure, and operational efficiency.

1. Higher approval rates from the same traffic

Many thin-file users are genuinely creditworthy borrowers:

- young professionals

- informal workers

- recent immigrants

- people who've avoided credit products

Alternative data helps fintechs evaluate these applicants using real-world signals.

This includes spending patterns, identity consistency, and digital behavior that indicates stability.

With that added context, lenders can approve a higher share of applicants from the same marketing spend.

Same traffic, more funded customers, lower effective CAC.

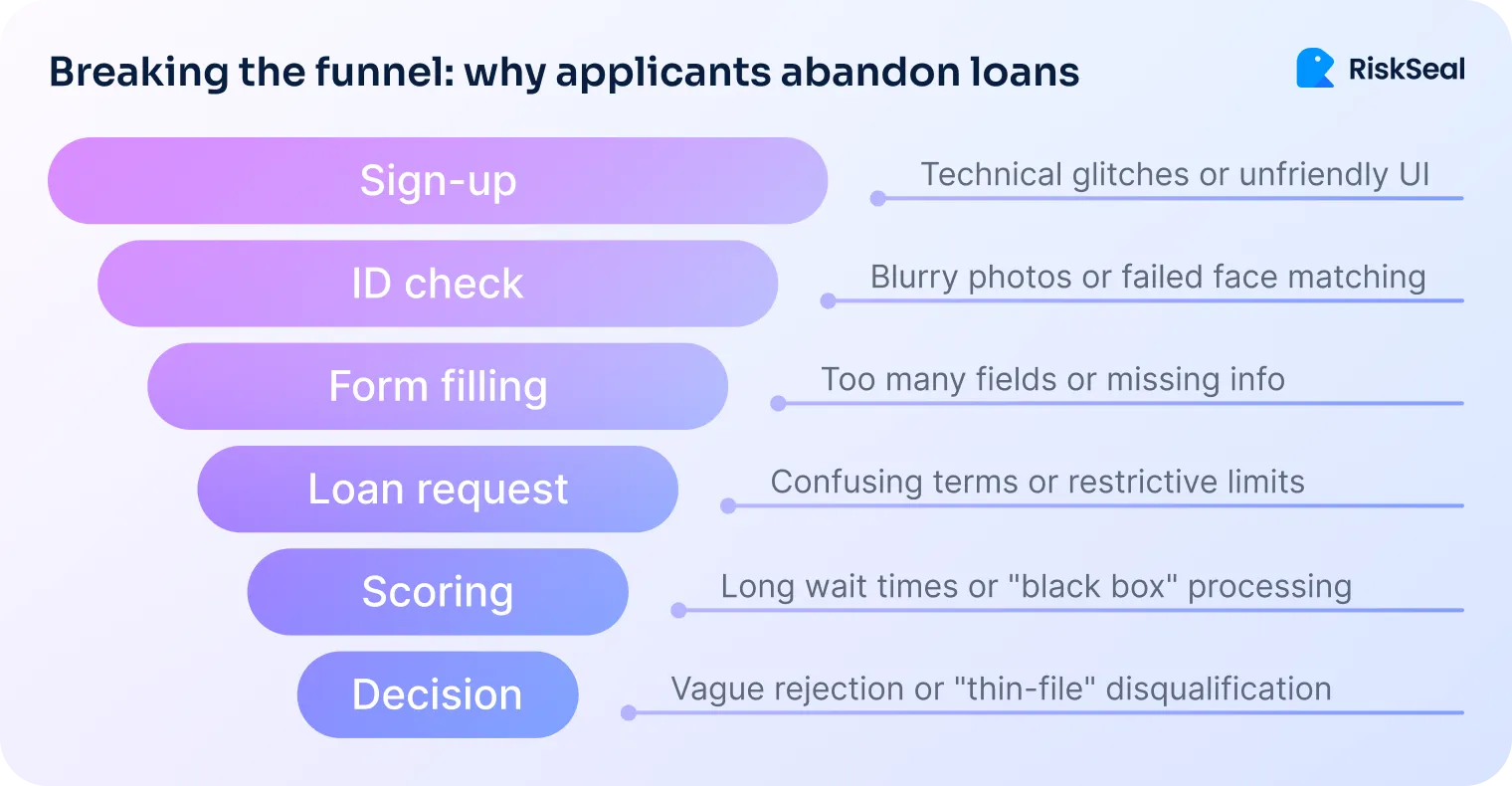

2. Less friction for customers in onboarding

When a traditional scoring flow can't resolve uncertainty, it typically asks the user for more. More documents, more verification steps, more time.

Each added step is a drop-off point.

The user who downloads an app, applies, and then gets asked to upload three months of bank statements often just doesn't come back.

Alternative data reduces that uncertainty.

With a more complete risk picture, lenders can approve low-risk users with fewer manual steps and a much smoother experience.

Shorter onboarding and fewer verification steps mean fewer users drop off before approval.

This strengthens trust and increases satisfaction from the very first interaction.

3. Smarter pre-qualification of applicants

One underused advantage of alternative data is how early in the funnel it becomes available.

Digital footprint signals can be analyzed before a full application is submitted. Sometimes, even before any credit data has been provided at all.

This makes pre-qualification much more accurate.

Marketing teams can filter traffic and avoid pushing users through a full funnel when approval probability is low.

That's a direct reduction in wasted spend. Not through better ad targeting, but through smarter decisioning upstream of the formal application.

4. Lower operational cost per loan

Manual reviews are expensive. Every edge case that can’t be auto-decided consumes underwriting capacity and raises the operational cost per funded loan.

Across thousands of applications a month, it becomes a real cost center. Alternative data reduces cases requiring human intervention.

A scoring model enriched with digital signals can help auto-decide on borderline applicants that a bureau-only model would flag for review.

The result is a lower cost per approved and funded loan, which improves unit economics before you factor in revenue.

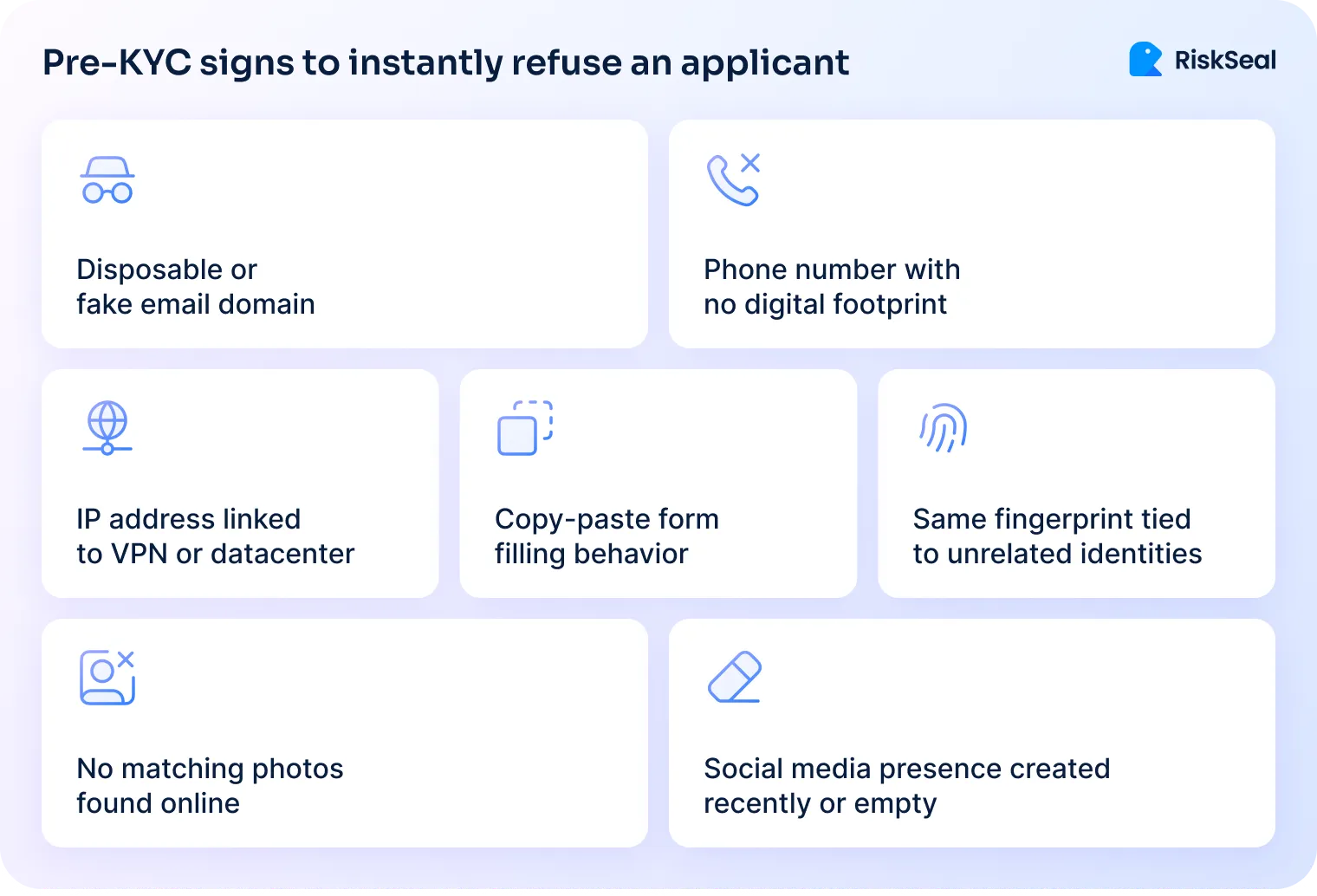

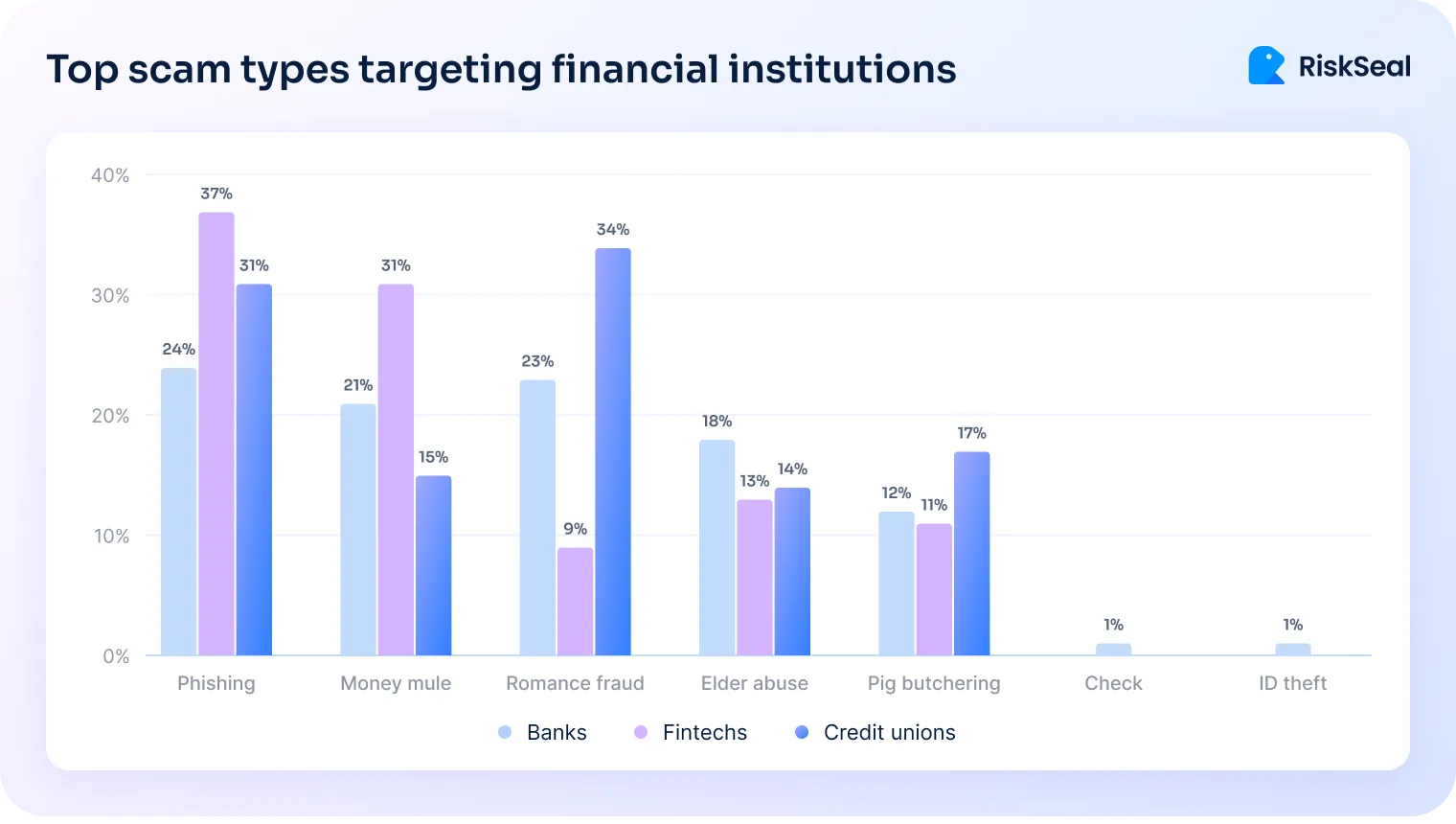

5. Fraud filtered early

Fraud quietly drains acquisition budgets, consuming marketing spend and operational capacity before it ever shows up as a loss.

The landscape is also expanding.

New scam types appear every quarter, targeting financial institutions in different ways (see the breakdown below).

Document fraud is increasingly sophisticated, but long-term digital behavior is harder to fake.

A stolen identity may pass standard checks, yet still lacks consistent footprint signals.

As my colleague Artem Lalaiants, a digital credit scoring expert, puts it: “The strongest anti-fraud clues come from mismatched identifiers – clean bureau files paired with absent online presence or inconsistent device data.”

Alternative data allows catching these patterns early and prevents bad accounts from entering the portfolio at all.

6. Better risk selection and higher LTV

Higher approval rates only help if approved borrowers perform well.

This is where alternative scoring has an often overlooked advantage. It improves approval quality, not just approval volume.

Early digital signals are predictive not just of default risk but of repayment behavior and long-term engagement.

Lenders using alternative data tend to see fewer early delinquencies, lower charge-off rates, and stronger lifetime value from approved cohorts.

For example, some RiskSeal clients have reported default reductions of up to 25% after integration, yet results vary by market and portfolio.

When LTV rises while acquisition cost stays flat, CAC-to-LTV ratios improve significantly.

This turns acquisition spend into a competitive advantage rather than a treadmill.

TL;DR: How alternative data improves CAC across the funnel

The table below summarizes how alternative data impacts CAC at each stage of the lending funnel.

.svg)

.webp)

How RiskSeal helps fintechs reduce CAC

At RiskSeal, our team built the platform to solve a specific gap: confidently scoring applicants who fall outside traditional bureau coverage.

With the right data enrichment approach, many thin-file and first-time borrowers are strong, creditworthy customers.

I keep our team focused on one core advantage – local alternative data that other vendors simply don’t have.

We enrich bureau-based decisioning with high-coverage, market-specific signals.

Our online lending system includes local registrations, regional platforms, paid subscriptions, marketplace behavior, and more.

These signals don’t overlap with bureau data, which means they generate independent model uplift rather than redundancy.

In practice, this leads to consistent outcomes for lending teams:

- Proven uplift in Gini/AUC from non-overlapping local signals

- More approvals without increasing default rates due to more effective segmentation

- Lower operational burden with fewer manual reviews and secondary verifications

When risk teams can identify good borrowers earlier and more accurately, more funded loans come from the same traffic.

CAC improves as a consequence. Not because marketing changed, but because decision quality did.

Better risk signals, lower CAC

In my experience, CAC drops when the risk layer stops leaking value.

I see the strongest fintechs using alternative credit decisioning software to separate “unknown” from “high-risk” earlier in the funnel.

It does not turn every thin-file applicant into an approval. But it does reduce blind rejections, unnecessary document checks, and slow manual reviews.

Alternative data is part of the decisioning infrastructure. And when that layer improves, the economics improve with it.

FAQ

How exactly does alternative data reduce Customer Acquisition Cost (CAC)?

Alternative data reduces CAC by converting a higher percentage of existing traffic into funded loans.

By scoring "thin-file" applicants who would otherwise be rejected or sent to manual review, lenders increase their approval rate without increasing their marketing budget.

Can alternative data help with fraud prevention in digital lending?

Yes, alternative data can significantly improve fraud prevention in digital lending.

It enables data enrichment and contextual analysis. These help lenders spot mismatched identifiers, inconsistent digital behavior, and synthetic profiles that often pass traditional checks.

Is alternative data meant to replace traditional credit bureaus?

No. It is designed to enrich bureau data. It fills "blind spots" by providing independent, non-overlapping signals that traditional bureaus often lack. Especially in emerging markets.

Credit bureaus provide structured repayment history and standardized reporting that lenders rely on. Alternative data adds context: identity consistency, digital behavior patterns, and signals of stability.

Used together, they create a more complete risk picture. Not by replacing what already works, but by strengthening it.

What is the impact of alternative scoring on operational costs?

It lowers the cost per loan by reducing the need for manual underwriting.

By providing a more complete risk profile automatically, the system can auto-decide on "borderline" applicants that would typically require expensive human intervention.

See more

Learn how lenders can prevent model risk, avoid vendor lock-in, and strengthen credit data supply chains using resilient alternative data strategies.

Learn how to grow approvals with risk-adjusted acquisition, better funnel checks, and borrower quality metrics.

Discover global lending trends that can shape credit scoring strategy for successful financial inclusion.