Back to Glossary

Behavioral Insights

Learn what behavioral insights are in credit decisioning and see how RiskSeal turns financial habits into instant, explainable scores.

Learn what behavioral insights are in credit decisioning and see how RiskSeal turns financial habits into instant, explainable scores.

Lenders can’t rely on slow, static risk checks in a competitive market.

Behavioral insights turn real-time borrower actions into measurable business gains.

They drive higher approval rates, fewer defaults, and faster decision cycles. This directly boosts portfolio performance and profitability.

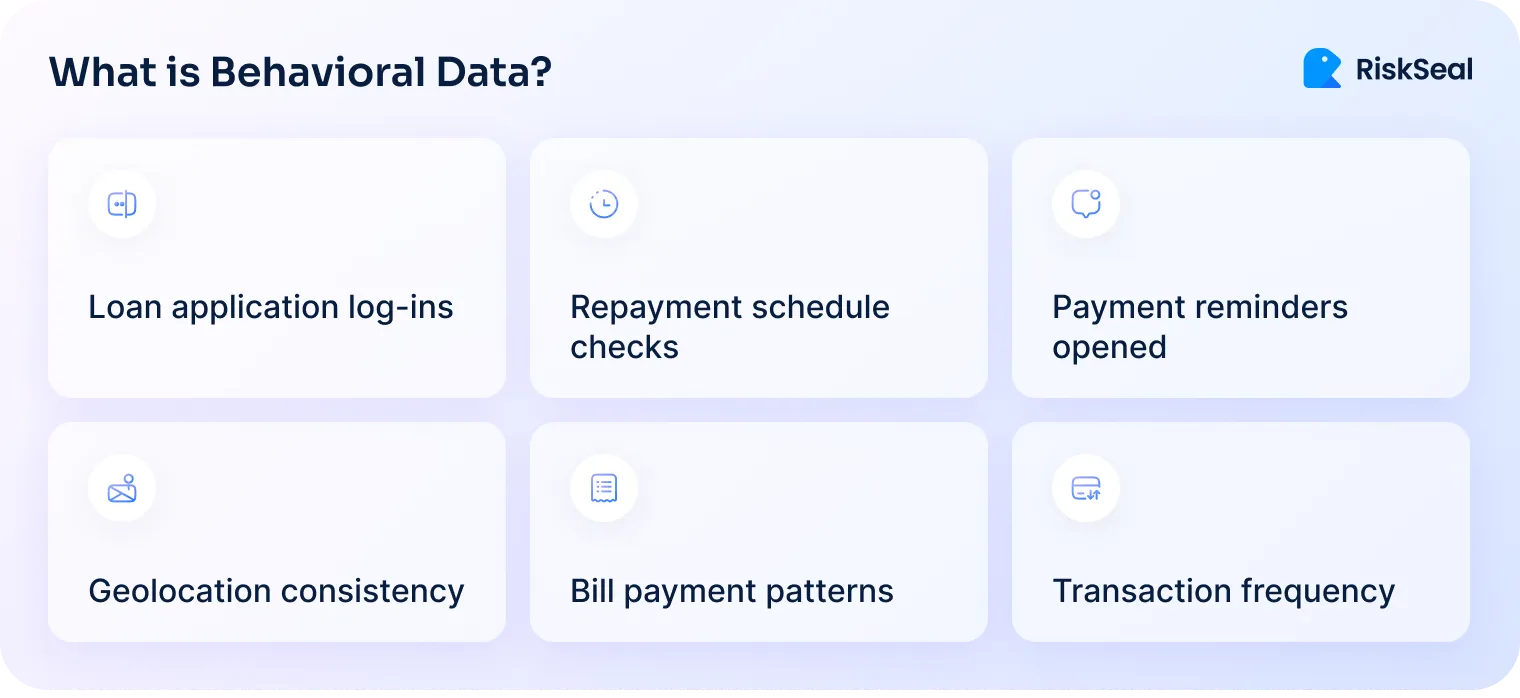

In credit risk assessment, behavioral insights are signals based on real customer actions. They focus on how a person spends, earns, and communicates.

Not just on their past credit history.

This makes behavioral data very different from traditional bureau data. The last one is often static and slow to update.

By analyzing patterns like payment regularity or login behavior, lenders can make fairer, faster, and more accurate decisions.

For lenders, understanding what is behavioural data means gaining a clear picture of who is really behind a loan application.

It’s about building a digital persona of the applicant. And spotting whether their actions signal trustworthiness, financial discipline, and repayment potential.

Key types of behavioral signals include:

By interpreting these patterns, lenders can decide with more confidence whether to approve a borrower.

It also helps tailor offers to customer behavior and reduce the risk of fraud.

While both methods assess creditworthiness, they work very differently.

Traditional credit checks rely on historical data, whereas behavioral insights focus on what’s happening right now.

Such a dynamic assessment allows lenders to make faster, fairer, and more inclusive credit risk evaluation.

For lenders, customer behavior provides a dynamic and current view of a borrower’s reliability. They are especially valuable for “thin-file” applicants and for first-time borrowers.

Credit decisioning with digital footprints, like financial habits, helps lenders identify loan-worthy borrowers.

This lowers the risk of long-term losses and strengthens overall portfolio stability.

Key business benefits include:

For example, subtle drops in engagement or transaction regularity can signal stress before a payment is missed.

Acting early not only protects repayment rates. It also strengthens a lender’s standing in a crowded market.

Behavioral insights are no longer a “nice-to-have” in credit assessment. They’re a competitive advantage. When combined with real-time identity verification, they help lenders approve the right borrowers faster.

RiskSeal captures 400+ digital signals from borrower identifiers like email, phone, and IP. It then turns them into instant, explainable scores enriched with fraud prevention indicators.

This means lenders can:

These capabilities are already helping fintechs enter new markets, serve thin-file borrowers, and protect their portfolios.