Explore the top 10 AI credit scoring software platforms lenders use in 2026 to make faster decisions and manage risk more accurately.

In 2025, 98% of North American banks used AI in at least one operational process. Credit risk is at the center of that shift.

AI credit score software enables lenders to make faster, more accurate decisions by analyzing real-time data beyond traditional bureaus. The result is better approvals, lower defaults, and scalable growth.

This guide reviews ten options to help fintech teams choose a top provider of generative AI credit scoring decisioning in 2026 that fits their needs.

AI credit scoring software uses machine learning and advanced analytics to assess borrower creditworthiness and predict default risk.

Rather than relying on bureau data alone, an AI credit score blends bureau information with alternative signals to produce more accurate decisions.

Here is what AI is capable of when it comes to credit scoring:

This approach shows how AI changes credit scoring, moving beyond static bureau files to a dynamic risk view built on digital footprint and behavioral data.

Alternative credit scoring enables instant loan approvals while strengthening fraud detection at the point of application.

It also supports ongoing portfolio monitoring and dynamic credit line adjustments as borrower risk changes.

Selecting the right AI-powered credit scoring software requires more than comparing feature lists.

Risk teams need to evaluate how each solution performs in real-world environments – at scale, under regulatory pressure, and across diverse borrower profiles.

1. Data sources and coverage. Strong platforms combine alternative global and local signals to deliver a more accurate and market-relevant risk view.

2. Predictive accuracy. Integrating an AI-powered credit scoring tool should deliver measurable AUC or Gini uplift in the lender’s model across borrower segments.

3. Integration and implementation. Effective solutions integrate easily into existing workflows through APIs, with fast deployment and minimal operational disruption.

4. Explainability and transparency. Lenders must clearly understand what drives each decision, with defensible reason codes and regulator-ready explanations.

5. Compliance and security. The platform should fully support applicable regulations while ensuring secure data handling and fair lending safeguards.

6. Customization and flexibility. Effective tools give lenders control over thresholds and how AI-driven insights are applied within their existing decision frameworks.

7. Speed and scalability. Credit scoring APIs must deliver real-time responses and maintain stable performance during peak application volumes.

8. Cost structure. Pricing should align with portfolio economics and scale efficiently as application volume and lending activity grow.

9. Reporting and analytics. Ongoing visibility into portfolio performance and model behavior is essential for continuous risk optimization.

10. Vendor reputation and support. Proven market experience, customer outcomes, and long-term support reduce operational and execution risk.

These solutions take different approaches to applying AI in credit scoring, from alternative data enrichment to full decisioning and portfolio risk management.

Every lender has a different risk appetite and technical stack.

To help you move beyond the high-level comparison, the following sections dive into the core features, best-use cases, and pricing structures for each vendor.

RiskSeal is an AI credit scoring and data enrichment platform built on proprietary alternative data that most competitors don’t have.

Its signals are designed to be non-overlapping with bureau inputs, giving lenders a clean, incremental Gini uplift when layered into existing models.

RiskSeal combines region-specific alternative credit data with digital footprint signals from widely used global platforms.

This helps lenders see local borrower behavior that traditional bureau-only scoring and standard fraud tools aren’t designed to capture.

RiskSeal credit scoring software is built to sit on top of bureau models, improving decision quality without changing existing workflows.

The API performs especially well for thin-file and first-time borrowers, while still delivering measurable AUC and Gini improvements even in mature markets.

Key features

Best for

Online lenders, neobanks, BNPL providers, and microfinance institutions serving underbanked populations or markets with limited credit bureau coverage.

Pricing

Basic plan starts from $499 per month. For large enterprises with a high volume of transactions, custom pricing is available.

Zest AI is a machine learning platform for large-scale credit underwriting.

It enables lenders to build, validate, deploy, and monitor custom AI credit models with explainability and regulatory compliance built in.

Rather than delivering a standalone score, it helps modernize existing underwriting frameworks.

Key features

Best for

Banks and large financial institutions.

Pricing

Custom, enterprise-level pricing based on deployment scope, model complexity, and support requirements.

Experian PowerCurve is a unified decisioning platform for automated credit risk, fraud, and portfolio management.

It combines bureau, alternative, and internal data to support consistent decisions across the customer lifecycle.

Experian PowerCurve enables lenders to build, deploy, and monitor decision strategies using explainable AI and no-code tools with minimal IT dependency.

Key features

Best for

Traditional banks, credit unions, online lenders, neobanks, and large financial institutions.

Pricing

Entry-level licensing typically starts around £3,500 per month, with final pricing tailored to scale and integration needs.

Scienaptic AI is a credit decisioning platform that combines bureau, alternative, and transactional data.

It helps lenders improve approval rates and risk segmentation through explainable AI.

With a strong focus on financial inclusion and regulatory transparency, it also supports ongoing credit line management and portfolio monitoring.

Key features

Best for

Mid-sized to large lenders, including digital-first banks and fintech lenders.

Pricing

Custom pricing based on deployment model, data sources, and decision volume.

Provenir is a risk assessment platform for building and managing custom models across multiple data sources.

With it, risk teams can design decision flows, test strategies, and compare models in production.

The platform also supports rapid iteration as portfolio performance and market conditions change.

Key features

Best for

Banks, digital lenders and fintechs, telecoms, payments and acquiring providers, e-commerce and marketplaces.

Pricing

Custom pricing based on data usage, decision volume, and selected platform modules.

LenddoEFL is an AI-driven alternative credit scoring platform focused on financial inclusion in emerging markets.

The platform combines behavioral analytics with identity verification and fraud detection to support high-volume lending in underserved segments.

LenddoEFL is designed to remain predictive even in volatile conditions, helping lenders expand access while managing default and fraud risk.

Key features

Best for

Banks, microfinance institutions, NBFCs, and fintech lenders.

Pricing

Custom pricing based on features, data volume, integration requirements, and deployment scale.

FICO® Platform extends the industry’s most widely used credit scoring model with AI and ML capabilities.

It allows lenders to enhance traditional FICO-based decisioning while relying on decades of established credit risk expertise.

FICO® Platform does not replace existing models. Instead, it supports custom analytics and decision optimization within a highly governed environment.

Key features

Best for

Large banks, enterprises, and regulated financial institutions.

Pricing

Custom pricing based on licensing scope, deployment model, and selected capabilities.

CreditVidya is an AI-powered credit underwriting platform that combines digital footprint data with traditional bureau inputs.

It is designed to apply machine learning to creditworthiness assessment, particularly for first-time and underserved borrowers.

CreditVidya supports automation across key stages of the credit lifecycle. This helps lenders improve approval rates, reduce decision times, and manage fraud and default risk more efficiently.

Key features

Best for

Banks, NBFCs, fintech lenders, e-commerce platforms, and digital marketplaces in emerging markets serving thin-file or credit-invisible borrowers.

Pricing

Custom, usage-based pricing depending on data volume, features, and integration requirements.

Oscilar is an AI-powered risk decisioning platform that unifies fraud prevention, credit underwriting, onboarding risk, and AML compliance.

The platform combines real-time analysis, ML, and behavioral biometrics. It applies this data to detect account takeovers, synthetic identities, and first-party fraud.

It also lets teams automate risk workflows using no-code tools, while staying transparent and compliant.

Key features

Best for

Banks, fintechs, and payment providers working in fraud-prone sectors.

Pricing

Custom pricing based on transaction volume, deployment scale, and selected risk modules.

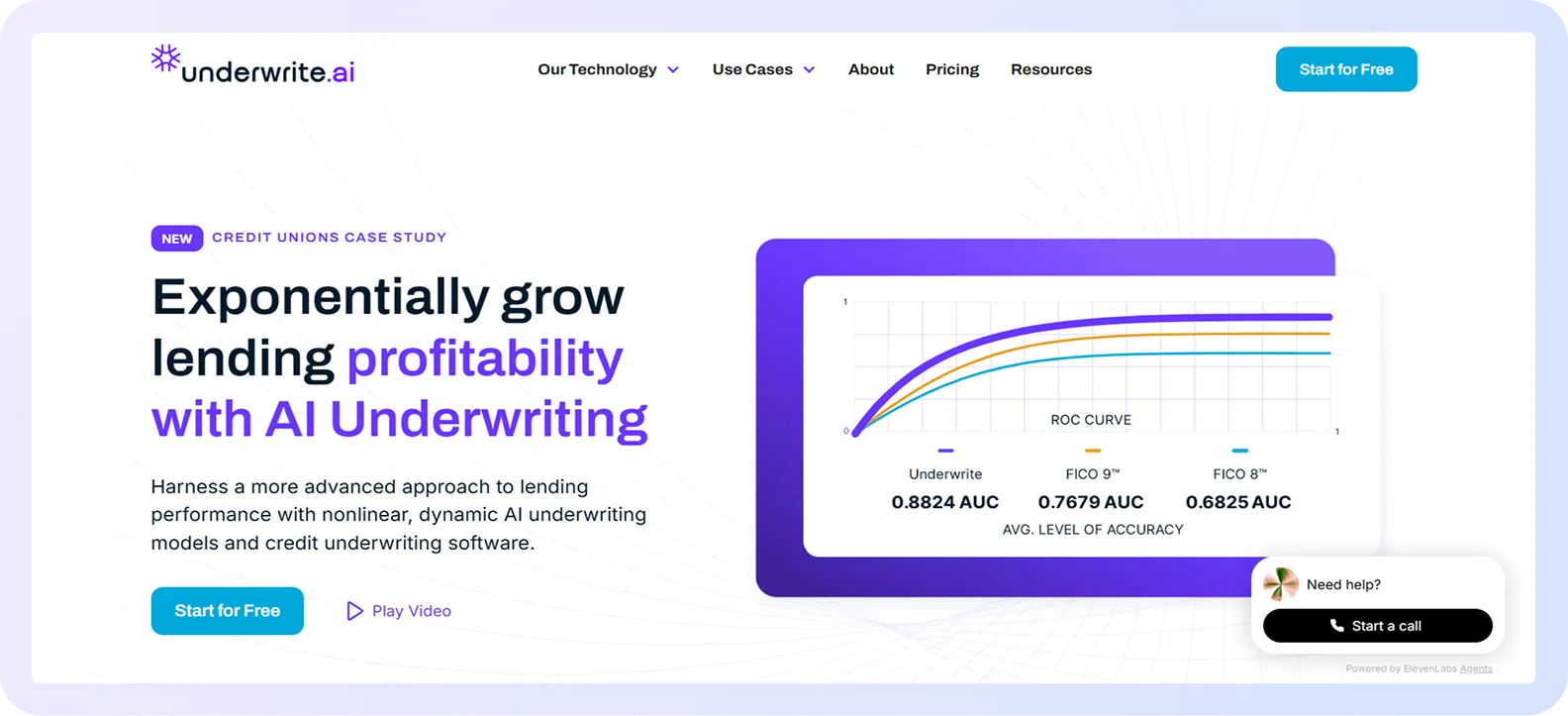

Underwrite.ai is an AI-driven credit assessment platform designed specifically for small business lending.

It evaluates repayment capacity by analyzing cash flow, business performance data, and owner-level information.

By focusing on real-time cash flow and operating performance, Underwrite.ai supports faster, more informed credit decisions for small business loan products.

Key features

Best for

Lenders focused on SMB lending, merchant cash advances, and commercial credit products.

Pricing

Custom pricing based on lending volume, data sources, and deployment requirements.

The fastest-growing lenders treat credit scoring using AI as a strategic profit driver, not just a regulatory obligation.

Focus on solutions that expand your addressable market without diluting risk, especially those that surface predictive signals beyond bureau data.

Test rigorously on live portfolios, measure uplift in approvals and losses, and iterate quickly.

The winners aren’t the ones with the most complex models, but those who turn better data and faster decisions into sustained, scalable growth.

Discover how credit institutions can ensure GDPR compliance when using alternative data for credit scoring.

Discover four practical ways to strengthen consumer credit risk in 2026 with real-time underwriting, alternative data, smarter collections, and compliance-ready AI.

Explore data enrichment with this hands-on guide. Learn onboarding best practices, avoid common pitfalls, and see real use cases.

.svg)

.webp)