Consumer lending market in Mexico: loan types, trends, and key players

Explore Mexico’s consumer lending market, from major loan types and fintech trends to key providers, risk challenges, and growth opportunities.

Mexico is one of the most active consumer finance markets in Latin America.

It brings together traditional banks, fintech lenders, BNPL providers, payroll lenders, retailers, and microfinance institutions. Each serves different borrower segments with different risk models and regulatory exposure.

The numbers reflect that activity. The Mexico consumer lending market reached USD 323.4 billion in 2024. It is also projected to grow to USD 532.7 billion by 2033, at a CAGR of 5.2%.

Total consumer credit balances, per Trading Economics, exceeded MXN 2.34 trillion in Q4 2025.

Yet the market remains underdeveloped relative to its size.

Credit card penetration sits at roughly 10% of the population. Around 70% of Mexicans lack traditional credit history. That gap is both a challenge and an opportunity.

This overview covers the structure of the consumer finance market in Mexico, the main product segments, the key players across banks and fintechs, and the practical challenges lenders face when operating here.

The 2026 guide to LATAM digital footprints for credit scoring

Who this overview is for

This article is written for fintech companies, digital lenders, BNPL providers, payroll lenders, and other financial institutions that issue consumer credit or are evaluating the Mexican market.

The focus is on how Mexico’s consumer lending market works from a provider perspective.

It covers market structure, product segments, key players, and lending challenges, rather than individual borrower guidance or loan comparison advice.

The consumer lending market in Mexico: structure and dynamics

Before looking at specific loan products, let’s look at how Mexico’s consumer lending market is structured and why demand is growing.

How Mexico’s consumer lending market is structured

Consumer finance in Mexico is served by a mix of provider types that operate with very different models, risk appetites, and customer bases.

Traditional banks dominate by volume. Seven large banks represent about 80% of the Mexican banking market, with BBVA, Banorte, and Santander alone accounting for over 50% of net income.

Their strength is in secured and payroll-linked products, where default risk is more manageable and ticket sizes justify the cost of origination.

Below that layer sits a large and growing digital lending ecosystem. Mexico's alternative lending market reached $2.05 billion in 2025 and is expected to grow at a CAGR of 13.8% through 2029, reaching approximately $3.44 billion.

Fintechs, neobanks, and embedded finance platforms are absorbing demand that traditional banks don't address:

- thin-file borrowers

- gig workers

- underserved communities in smaller cities

- consumers who want a fully digital experience

Retail financing and BNPL are a separate but overlapping layer. BNPL adoption in Mexico grew 78% in 2024, reaching over 10 million users, driven by limited credit card penetration and strong e-commerce growth.

Platforms like Kueski Pay and Aplazo have expanded rapidly through merchant partnerships, turning point-of-sale credit into a scalable consumer finance channel.

Underbanked consumers and the demand for alternative credit

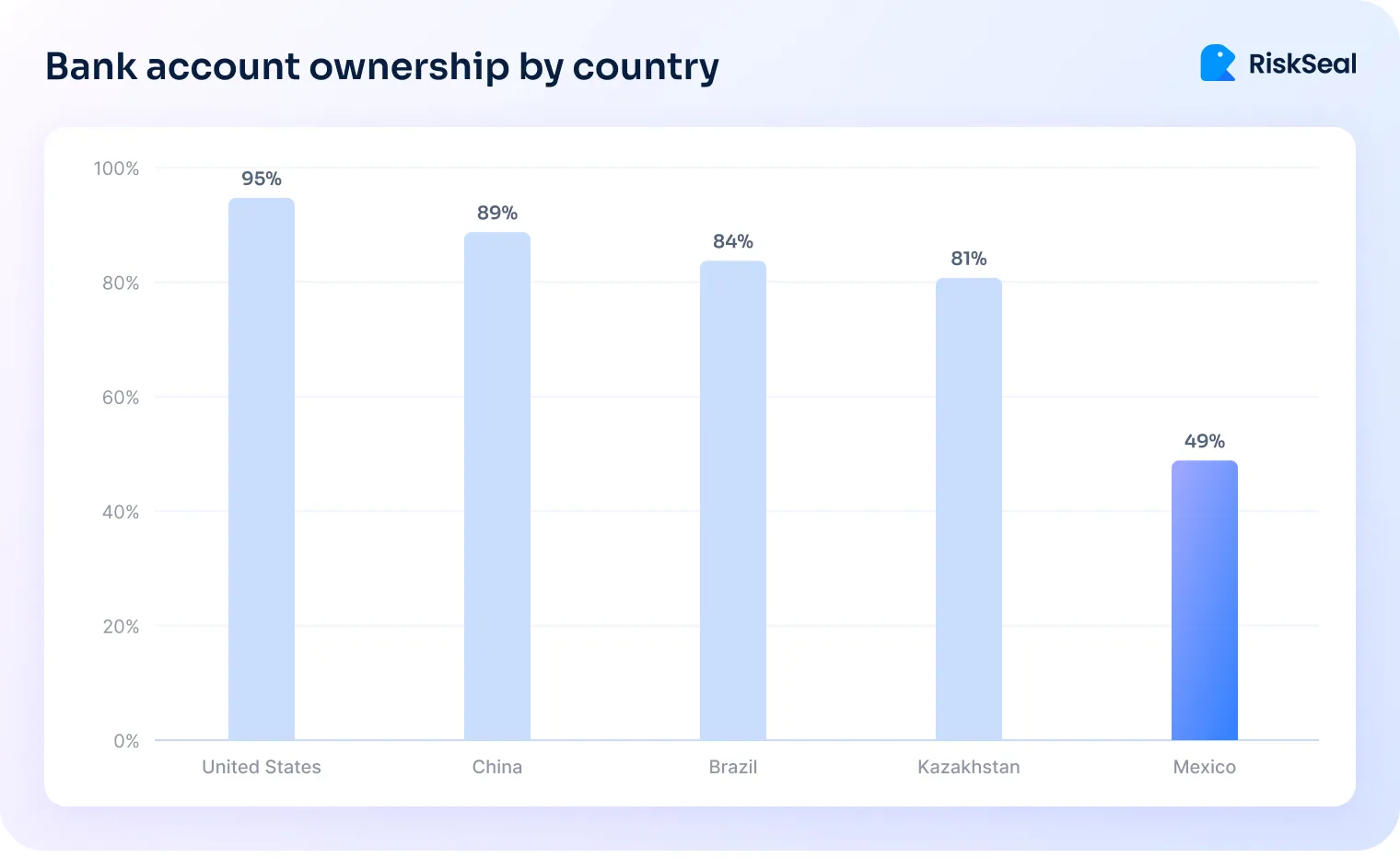

Around 50% of the Mexican population remains unbanked, and even among those with bank accounts, formal credit access is limited.

This creates persistent structural demand for alternative credit. Fintech lenders and microfinance institutions have moved into this space with mobile-first products and non-traditional underwriting.

Fintech firms are creating opportunities through AI-driven behavioral data capture, targeting underbanked populations and expanding credit access.

I've seen this dynamic play out repeatedly in markets with similar profiles: the unbanked aren't simply excluded from credit. They're often actively seeking it, and whoever builds the right risk model first captures a significant share.

What drives fragmentation in Mexico’s lending market

The fragmentation in Mexico's consumer finance market comes from a few structural realities. The country's income distribution is wide, urban-rural gaps are significant, and informal employment remains high.

A payroll lender serving government employees in Mexico City operates in a fundamentally different risk environment than a microlender serving market vendors in Oaxaca.

That diversity of borrower profiles is what keeps the market fragmented and what creates entry points for specialized providers.

Between Q2 2018 and Q2 2024, the total number of transactional and savings accounts in Mexico increased by 37.1%, according to BBVA Research. This shows broadening the formal borrower base.

But growth in accounts doesn't automatically translate to growth in credit access, especially for borrowers without documented income or credit history.

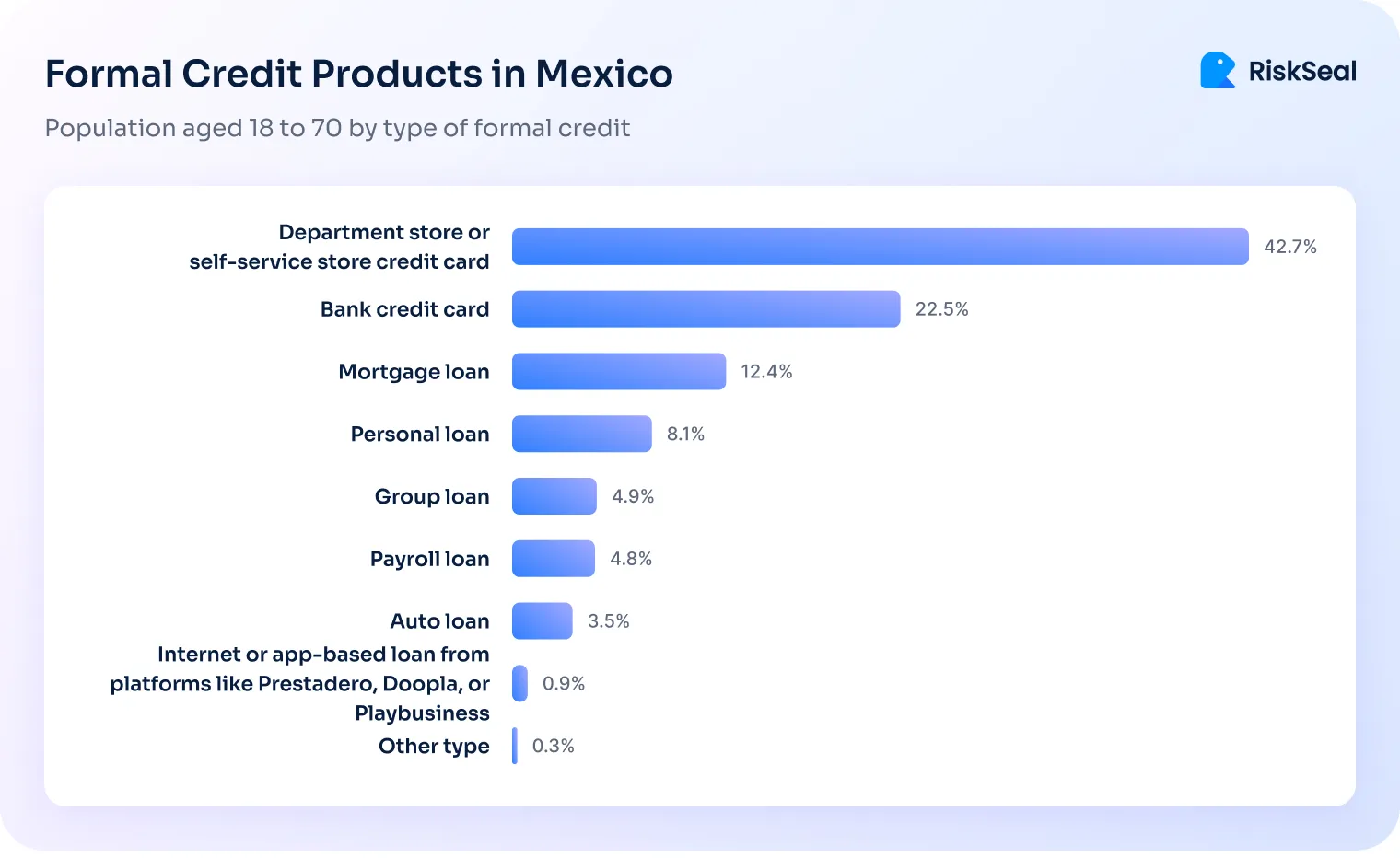

Types of consumer loans in Mexico

The table below compares the main loan types by use case, provider profile, and market role.

Store credit and retail financing

Store credit is the most widely used loan product in Mexico. It covers point-of-sale financing at retailers, issued either as direct merchant credit or through store-affiliated banks.

Store-linked banks like Banco Azteca and BanCoppel have built entire consumer lending businesses around retail relationships.

Their ability to collect payments at physical store locations gives them reach into communities where traditional bank branches are absent.

For lenders, this distribution model keeps acquisition costs low. But the borrower profile often carries elevated credit risk, reflected in higher-than-average delinquency rates at these institutions.

The retail financing segment is also where BNPL is gaining ground, replacing or supplementing traditional store credit with digital installment products.

From a lender's perspective, BNPL in retail adds merchant data to the credit equation – payment behavior at point of sale becomes an underwriting signal.

Credit cards

Mexico had 37.1 million credit card contracts by mid-2025, up from 35.3 million a year earlier. BBVA led with 10.76 million cards, followed by Banamex with over 9.2 million.

The delinquency rate on credit cards remained stable at 3.30% at the end of June 2025.

With credit card penetration at roughly 10% of the population, this segment has significant room to grow.

Digital issuance has accelerated that growth. Neobanks and fintechs are now issuing cards to borrowers who would not have qualified under traditional criteria, using alternative data to make underwriting decisions.

For lenders, credit cards represent a high-margin revolving product with decent default management when underwriting is sound.

The challenge is customer acquisition cost in an increasingly competitive digital market.

Personal loans in Mexico

Personal loans are unsecured, general-purpose credit products. That means higher margins for lenders and higher default exposure.

Personal loans had the highest delinquency rate among bank loan portfolios, at 4.66% at the end of 2024, though this was an improvement from 5.19% in December 2023.

The Mexico personal loans market was valued at USD 60.68 billion in 2025 and is projected to reach USD 96.79 billion by 2033, at a CAGR of 6.1%.

The unsecured nature of personal loans makes borrower assessment critical. Traditional income verification covers a shrinking share of the borrower population.

Gig workers, informal employees, and thin-file applicants require different credit signals to underwrite responsibly at scale.

Payroll loans

Payroll loans are secured by the borrower's salary through automatic deductions, which makes them structurally low-risk for lenders. Default is essentially self-enforcing as long as the employer relationship holds.

This product represents a large portion of bank consumer portfolios – both private banks and public-sector lenders serve this segment.

The challenge for lenders isn't default risk, it's competition. The payroll loan market is well-served and margins have compressed.

Differentiation tends to come from speed, digital access, and supplementary product offers.

Microloans

Microfinance in Mexico serves a large population of borrowers with thin or no credit files, often in informal employment.

The segment is active but carries distinct risk dynamics. Multi-loan exposure is widespread. Many microloan borrowers hold credit with more than one institution simultaneously, which strains repayment capacity.

For lenders entering this segment, portfolio quality management requires close monitoring of borrower indebtedness across institutions.

The ability to assess total debt burden – not just behavior on a single loan – is a meaningful advantage here.

BNPL in Mexico

BNPL has emerged as the fastest-growing segment in Mexico's consumer finance market.

The lending sector is being reshaped by expanding BNPL options, innovative credit scoring methods, and the integration of credit into digital platforms.

Platforms like Kueski Pay and Aplazo operate through merchant partnerships, embedding installment credit into the purchase flow.

BNPL providers are aggressively expanding through merchant partnerships, fueled by a large addressable market of unbanked and underbanked users and a growing digital economy.

From a lender's perspective, BNPL is attractive because it combines short loan terms with transaction-level data.

But it also compresses margins and raises questions about borrower stacking – users taking installment credit across multiple platforms simultaneously.

Auto loans in Mexico

Auto lending is one of the stronger growth segments in Mexico's consumer finance market.

Credit is a standard part of new vehicle purchases, and bank portfolios in this segment have held up well in terms of delinquency.

Credit for durable goods grew by 38.7% year-over-year in September 2024, reflecting resilient demand.

Banks are the primary providers for new vehicle financing. Used vehicle financing is a different risk calculus – collateral valuation is harder to standardize.

This keeps most traditional lenders cautious about this sub-segment.

Mortgage loans

Mortgage lending in Mexico involves both commercial banks and public-sector housing institutions.

The portfolio continues to grow in nominal terms, though origination volumes have been constrained by housing price increases outpacing wage growth.

This is an adjacent segment to unsecured consumer finance.

It matters for understanding the full lending landscape, but it operates under different risk and regulatory rules than the products that drive the consumer credit market.

Pawnshop loans

Pawnshop lending is a collateral-backed, short-term credit product serving borrowers who need fast liquidity and don't meet the requirements for formal credit.

National Monte de Piedad is the dominant player, operating a large national branch network.

This segment is relevant for lenders as context: the volume of pawnshop use reflects unmet demand for small-ticket, fast-turnaround credit that the formal market hasn't fully addressed.

Digital lenders with fast approval processes and flexible terms are effectively competing with pawnshops for some of this demand.

Key trends in Mexico's consumer lending market

Several dynamics are shaping how consumer finance in Mexico develops over the next few years.

Trend #1: Digital lending and mobile-first credit

Smartphone penetration and improving internet connectivity have opened direct-to-consumer credit channels that did not exist a decade ago.

The number of digital loans issued in Mexico has increased by 30% year-on-year, according to CNBV data.

Fully digital origination is becoming a baseline expectation. This includes application, identity checks, approval, and disbursement.

The shift is especially visible among younger borrowers. They expect faster access, fewer physical steps, and a credit experience closer to other digital financial services.

Trend #2: BNPL and embedded finance

Credit is increasingly embedded in commerce and digital platforms. It is no longer sold only as a standalone financial product.

This changes how lenders reach customers. It also changes how they underwrite, price risk, and compete.

The Mexico online loan and BNPL lending market is valued at USD 25 billion. BNPL transaction value is projected to triple from 2025 to 2030.

For lenders, this makes the point of sale a strategic acquisition channel. For merchants, it turns financing into a conversion and retention tool.

Trend #3: Financial inclusion keeps driving growth

The unbanked and underbanked population represents one of the largest addressable markets for consumer lenders in Mexico.

Many of these consumers are not outside the market because they lack demand. They are outside it because traditional underwriting cannot assess them well.

Fintech lenders are using alternative data models to turn previously unserviceable demand into real loan portfolios.

The formal account base is also expanding. Transactional and savings accounts increased by 37.1% over six years.

That does not automatically mean broader credit access. But it does expand the pool of borrowers that lenders can identify, assess, and serve.

Trend #4: Delinquency pressure and risk management

Growth in consumer lending comes with higher credit risk.

Personal loans carry the highest delinquency rate in the banking sector. Lenders serving non-prime segments face even greater exposure to NPLs.

This makes risk management a core competitive advantage.

The challenge is not simply to reduce defaults. It is to balance approval rates, fraud prevention, customer acquisition costs, and portfolio quality.

For digital lenders, this balance is especially important. Small changes in underwriting can quickly affect both growth and profitability.

Trend #5: Nearshoring and employment formalization

Mexico’s role as a manufacturing and logistics hub has strengthened due to supply chain diversification.

Nearshoring can support formal employment growth in industrial regions. It can also expand the number of borrowers with stable income records.

This matters for consumer lending.

More formal employment can increase demand for payroll-linked products, auto loans, credit cards, and other bankable credit products.

It also creates opportunities for lenders that can connect employment signals with credit decisioning.

Traditional banks in Mexico's consumer lending market

Traditional banks dominate consumer lending by volume. In terms of total loan portfolio in December 2024, BBVA led with 25.4%, followed by Banorte with 14.9% and Santander with 11.6%.

Here is how each major institution positions itself in the consumer lending space.

BBVA México

BBVA is the market leader by assets and loan portfolio. It holds the largest share of credit cards, personal loans, and consumer credit overall.

BBVA's loan portfolio grew 15% year-on-year in Q1 2025, with Mexico identified as one of the key drivers.

The bank has invested heavily in digital origination. 66% of new customers acquired in Q1 2025 joined through digital channels.

Its scale gives it strong data advantages and the ability to price risk competitively across segments.

Banorte

Banorte is Mexico's largest domestically owned bank and has a strong position in payroll lending, retail banking, and mortgage.

Banorte registered the lowest NPL ratio among major banks – 0.90% at the end of 2024 – which reflects its conservative underwriting and heavy reliance on payroll-secured products.

It has also expanded digital offerings through its Bineo neobank platform.

Santander México

Santander is present across all consumer lending segments – credit cards, personal loans, and mortgages – and operates in all states.

It held an 11.6% share of total bank loan portfolios at the end of 2024. The bank is investing in digital channels, though it has faced above-average personal loan delinquency in some periods.

Banamex (Citibanamex)

Banamex is one of the largest issuers of credit cards in Mexico with over 9.2 million cards as of mid-2025.

The bank is undergoing a separation from Citigroup, which will refocus it on retail and consumer banking in Mexico. This transition may reshape its positioning in the consumer credit market.

HSBC México

HSBC serves retail and consumer segments across a national branch network. Its lending portfolio includes personal loans, credit cards, and mortgages.

Its NPL ratio stood at 2.30% at the end of 2024, in line with sector averages.

Scotiabank México

Scotiabank competes in consumer lending with personal loans, credit cards, and auto financing.

It has a smaller branch footprint than the top four but continues to operate across major urban markets.

Banco Azteca

Banco Azteca reaches consumers through an extensive physical network of Elektra stores, with a focus on low-to-middle income borrowers.

It is one of the largest players in consumer credit for underserved segments.

Its delinquency profile reflects the risk of this borrower base, but its distribution model gives it access to customers that traditional banks don't reach.

BanCoppel

BanCoppel operates similarly to Banco Azteca – retail-linked, focused on underserved consumers, with a wide physical presence.

Its delinquency rate stood at 6.52% at the end of 2024, above the banking average, consistent with its target segment.

Inbursa

Inbursa is part of Grupo Financiero Inbursa and focuses on consumer and corporate lending.

It has a relatively low NPL profile among mid-sized banks and competes mainly in personal loans and auto financing.

BanBajío

BanBajío operates as a regional community bank and has grown steadily, particularly in central Mexico. It serves consumer and commercial segments with loans and credit cards.

Afirme

Afirme is part of Afirme Grupo Financiero. It provides consumer loans, auto loans, and mortgages, with a regional focus in northern Mexico.

Traditional banks still define the scale and structure of consumer lending in Mexico, but their models leave clear blind spots for many borrowers. This is where alternative credit scoring in Mexico shines.

Key fintech lending companies in Mexico

The Mexico fintech and online lending market is valued at approximately USD 7.5 billion.

Hundreds of active companies are competing on digital experience, underwriting speed, and access for underserved borrowers.

Kueski

Kueski is Mexico's leading BNPL and digital microloan platform, founded in 2012 and based in Guadalajara.

It operates both a short-term personal loan product and Kueski Pay, its BNPL offering embedded in e-commerce and retail.

It is known for fast automated credit decisions and a strong focus on thin-file borrowers.

Klar

Klar is a digital bank offering credit cards, savings, and personal loans. It targets borrowers who have been underserved by traditional banks and uses alternative underwriting.

It is an active player in embedded finance alongside Kueski Pay.

Konfío

Konfío focuses primarily on lending to small and medium-sized businesses using proprietary credit scoring.

While its primary focus is SME credit, it remains part of Mexico’s broader digital lending ecosystem.

Creditea

Creditea operates in personal lending, serving consumers who need fast access to unsecured credit.

It uses digital origination and positions itself as an alternative to traditional bank personal loans for borrowers with limited credit history.

Aplazo

Aplazo is one of Mexico's leading BNPL platforms, focused on retail and e-commerce merchant partnerships. It has scaled rapidly alongside the growth of online commerce in Mexico.

Stori

Stori targets credit card issuance for low-income consumers, including those without credit history.

It uses alternative data vendors to make approval decisions and claims a high approval rate for applicants who would typically be declined by banks.

Albo

Albo is a digital account and card platform offering personal finance management tools alongside a Mastercard-enabled digital account.

It competes with neobanks for the digitally mobile population seeking alternatives to traditional banking.

Clara

Clara focuses on corporate expense management and corporate card issuance for businesses. It serves the embedded finance and B2B payments space rather than retail consumer lending.

Challenges for consumer lenders in Mexico

Mexico’s consumer lending market offers strong growth potential, but lenders have to manage several structural risks before they can scale sustainably.

- Limited credit history. Around 70% of Mexicans lack traditional credit history, which limits the reach of standard bureau-based scoring.

- Underbanked borrowers. Many consumers move between formal and informal income sources, use multiple providers, and lack stable documentation.

- Fragmented borrower data. Credit history, employment data, utility records, and digital behavior often sit in separate silos.

- Fraud and identity risk. Digital origination creates scale, but it also increases exposure to synthetic identities, account fraud, and device-level risk.

- Competition for low-risk borrowers. Formally employed borrowers with strong credit profiles are heavily targeted, which compresses margins.

- Approval versus default risk. Lenders need to approve enough thin-file applicants to grow without allowing default rates to erode portfolio quality.

- Regulatory pressure. CNBV registration, loan-term transparency, credit reporting, and compliance infrastructure create real operating requirements.

- Small-ticket profitability. Microloans and short-term loans can be difficult to scale profitably when CAC is high and default control is weak.

For lenders, the challenge is not only finding demand. It is building the data, risk, fraud, and compliance infrastructure needed to serve that demand profitably.

Consumer lending and alternative credit scoring in Mexico

Many of the challenges described above converge on one operational need: better borrower assessment data.

For lenders working with thin-file or underbanked applicants, traditional credit scoring isn't enough.

Alternative credit scoring in Mexico uses non-traditional signals – digital behavior, device data, social footprints, and more – to assess creditworthiness for borrowers who don't have a formal credit history.

This approach has become central to how fintechs and digital lenders compete in Mexico.

It enables approval decisions on applicants that would otherwise be declined outright, and it improves risk segmentation within the non-prime segment.

For a detailed overview of how alternative credit scoring works in the Mexican market, see our dedicated guide: Alternative credit scoring in Mexico.

How RiskSeal supports consumer lenders in Mexico

RiskSeal works with fintechs, digital lenders, and BNPL providers operating in Mexico's consumer lending market.

We understand the specific pressures in this market – large thin-file populations, fraud risk in digital origination, and the need to make fast credit decisions at scale without compromising portfolio quality.

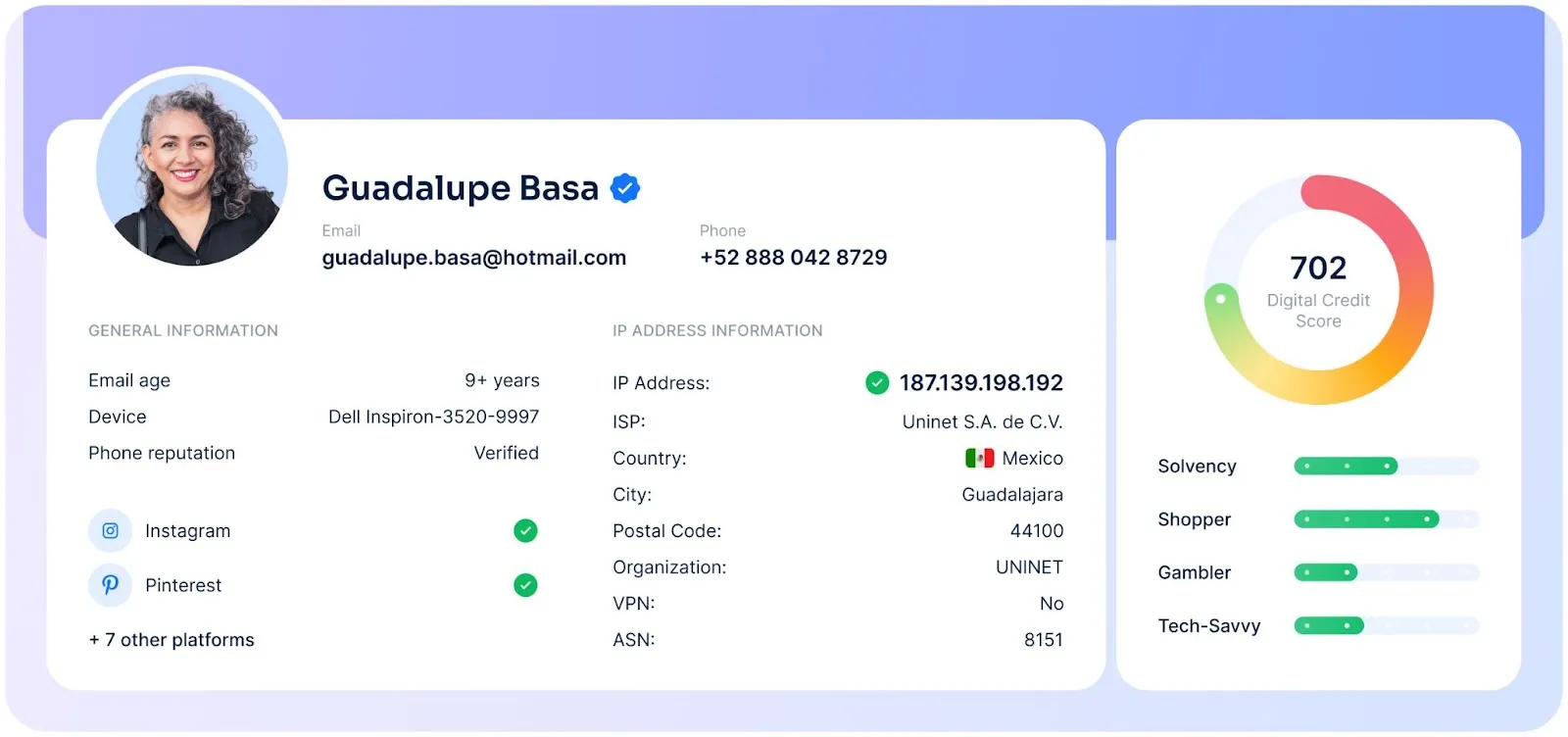

Our scoring system gives lenders 400+ data points on each applicant.

It draws on 200+ digital services, including regional platforms like DiDi, Rappi, Telcel, AT&T, Indeed, and Computrabajo.

This helps build a detailed picture of borrower behavior and credibility. This digital footprint analysis supports credit decisions, fraud detection, and identity verification in a single workflow.

In practice, this means lenders can meaningfully assess the creditworthiness of a much larger share of Mexican applicants. Including those that standard bureau scoring would reject or leave undecided.

If you're building or scaling a consumer lending operation in Mexico, we'd welcome the conversation.

Inside the LATAM alternative credit data report

FAQ

What are the main types of consumer loans in Mexico?

The main product categories are store credit and retail financing, credit cards, personal loans, payroll loans, microloans, auto loans, mortgage loans, pawnshop loans, and BNPL.

Each segment has distinct providers, risk profiles, and borrower bases.

Store credit and payroll loans account for the largest shares of the traditional consumer portfolio, while BNPL and digital personal loans are growing fastest.

Who are the main consumer lending providers in Mexico?

Traditional banks dominate by volume – BBVA, Banorte, Santander, and Banamex together control the majority of formal consumer credit.

Retail-linked banks like Banco Azteca and BanCoppel serve lower-income segments with significant physical distribution.

In fintech, key names include Kueski, Klar, Aplazo, Creditea, and Stori. The market is concentrated at the top but fragmented in the mid and lower tiers.

Why is Mexico attractive for fintech lenders?

Several factors make Mexico a high-priority market: a large underbanked population with unmet credit demand, low credit card penetration, a growing digital-native consumer base, an active regulatory framework for fintechs, and strong e-commerce growth driving BNPL adoption.

The market is large, underpenetrated relative to its population, and structurally suited to alternative lending models.

What challenges do consumer lenders face in Mexico?

The main challenges are limited credit history coverage, underbanked borrowers without formal financial footprints, fraud risk in digital channels, fragmented data infrastructure, pressure on margins in prime segments, rising delinquency in personal loans, and regulatory compliance requirements for digital institutions.

These aren't unique to Mexico, but they're pronounced here given the scale of informal employment and low banking penetration.

How is digital lending changing Mexico's consumer credit market?

Digital lending has expanded access, reduced origination cost, and accelerated the shift away from branch-based credit. CNBV data shows digital loan issuance growing 30% year-on-year.

Fintechs are reaching borrowers in smaller cities and informal employment through mobile-first products. BNPL specifically is reshaping point-of-sale credit.

The consequence for traditional banks is competitive pressure from providers with lower infrastructure costs and faster underwriting – which is why several banks have launched their own digital brands in response.

How can RiskSeal support consumer lenders in Mexico?

RiskSeal provides alternative data-based scoring for consumer lenders operating in Mexico.

Our platform delivers 400+ data points per applicant through digital footprint analysis, enabling lenders to assess thin-file and underbanked borrowers, detect identity fraud, and improve credit decision accuracy.

We cover regional platforms relevant to Mexican borrowers and are built for the specific data landscape of the Mexican market.

See more

.webp)

The development features of the lending sector in India and the role that alternative credit scoring plays in it.

Explore how to spot high-risk borrowers. Discover key red flags, alternative credit scoring, and risk mitigation strategies.

Learn key behavioral data types, real-world use cases, and benefits for lenders.