Credit Scoring in Mexico: Traditional Bureaus, Alternative Data, and Digital Risk Signals

Discover the key trends in Mexico's economic development, their impact on the lending industry, and the role of alternative scoring.

.webp)

Mexico has a functioning credit bureau system. But for a large share of the population, it doesn't produce a usable credit profile. That's the core tension lenders face here.

This article explains how credit scoring works in Mexico, why traditional bureau data leaves significant gaps, and how alternative data help lenders assess borrowers who fall outside the conventional system.

Who this article is for

This article is written for professionals working in lending and credit risk in Mexico or entering the market:

- Fintech lenders and digital lenders

- BNPL providers and neobanks

- Microfinance companies

- Credit risk, fraud prevention, and underwriting teams

- Financial institutions evaluating Mexico as a market

The 2026 guide to LATAM digital footprints for credit scoring

Does Mexico have a credit score system?

Yes, Mexico has a formal credit reporting infrastructure. Two credit bureaus operate in the country: Buró de Crédito and Circulo de Crédito.

Buró de Crédito is the primary bureau and serves as the official credit registry. It collects data from banks, retailers, telecom providers, and other creditors. Lenders query it to access a borrower's credit history and repayment behavior before making a lending decision.

Circulo de Crédito operates as a private bureau and uses FICO-based scoring models. One distinction worth noting: its models can factor in credit history from different family members when evaluating an applicant. This is useful in a market where family financial interdependence is common.

So yes, credit scores in Mexico exist, and credit reports are actively used in traditional lending. The system is real, regulated, and functional. But it's not analogous to the US model, where FICO penetration is near-universal. In Mexico, a significant portion of the adult population simply has no bureau record or has one too thin to generate a reliable score.

Credit bureaus in Mexico: what they cover and where they fall short

Credit bureaus play a critical role for lenders. They aggregate repayment history, outstanding balances, credit inquiries, and defaults into structured reports that feed underwriting decisions.

When a borrower has an active credit history – loans, credit cards, installment agreements – bureau data gives lenders a meaningful signal. Repayment patterns over time are among the strongest predictors of future behavior.

The problem is coverage. According to Mexico's National Institute of Statistics and Geography (INEGI), only around 49% of Mexicans aged 18-70 hold a bank account. Bureau data follows banking access: if someone has never taken a formal loan or held a credit card, there's nothing for the bureau to report.

This creates a structural gap. Many people who are economically active still remain difficult to assess through traditional bureau data alone, including:

- informal workers

- gig economy participants

- rural residents

- recent economic migrants

- younger adults

As a result, large segments of Mexico’s working population are either completely absent from bureau records or have credit profiles that are too sparse to support a standard lending decision.

For lenders, this means one of two outcomes: reject potentially creditworthy applicants by default, or develop supplementary assessment methods.

The second option is where alternative data becomes relevant.

Why traditional credit scoring is limited in Mexico

Mexico's economy has significant informal employment. Roughly 55% of workers operate in the informal sector, according to INEGI. These individuals earn real incomes and manage real financial obligations like rent, utilities, family support, mobile plans. But none of this activity is visible to a credit bureau.

Add to this the widespread preference for cash transactions. Many Mexicans without bank accounts conduct their financial lives entirely in cash. They pay on time, they manage expenses carefully, but they generate no digital or institutional record that traditional credit models can read.

Gig work compounds the issue further. Drivers, delivery workers, and freelancers may have irregular income but stable financial behavior. Standard credit models aren't built to handle non-salaried, non-formal income patterns well.

The result for lenders: thin-file and no-file borrowers aren't necessarily high-risk. They're simply unreadable through conventional channels. That distinction matters.

Treating credit invisibility as a proxy for risk means turning away a large population of potentially reliable borrowers.

I've seen this issue come up repeatedly when speaking with risk teams at digital lenders in emerging markets: the challenge isn't willingness to lend, it's having the right signals to lend responsibly.

The fintech response: alternative credit scoring in Mexico

Mexico's fintech sector has grown in direct response to these access gaps. According to the Finnovista Fintech Radar Mexico, the ecosystem now includes 795 local fintechs alongside 316 foreign players.

Lending is the largest local vertical, with 170 local lending companies, compared to just 35 foreign lenders. This reflects a domestic-led effort to close credit gaps that traditional banks haven't prioritized.

34.5% of fintechs offer products specifically targeting underserved groups. Among local fintechs, that figure rises to 46.2%. Nearly double the rate of foreign players.

AI adoption is accelerating the shift. According to Finnovista, AI integration in Mexico's fintech sector rose from 60% in 2025 to 77% in 2026, with measurable impact: a 54.9% reduction in fraud and a 34.2% increase in revenue among adopters.

Alternative credit scoring doesn't replace bureau data, but complements it. For applicants with a bureau record, alternative data adds texture and context. For thin-file or no-file borrowers, it provides the primary basis for assessment.

The goal is a more complete picture of the borrower: not just repayment history, but identity consistency, financial stability signals, digital presence, and fraud risk indicators.

Traditional vs. alternative credit scoring: a lender's comparison

What alternative data can lenders use in Mexico

Mexico's digital adoption creates a broad surface for alternative data collection. Here's a practical breakdown of the main categories, along with what each can and can't tell a lender.

Phone and email signals

A verified phone number or email address connected to multiple registered services suggests an established digital identity. Signals here include account age, registration patterns, and whether contact details appear in known fraud databases.

Useful for: identity consistency checks, fraud screening.

Limitation: presence alone doesn't indicate repayment behavior.

Telecom signals

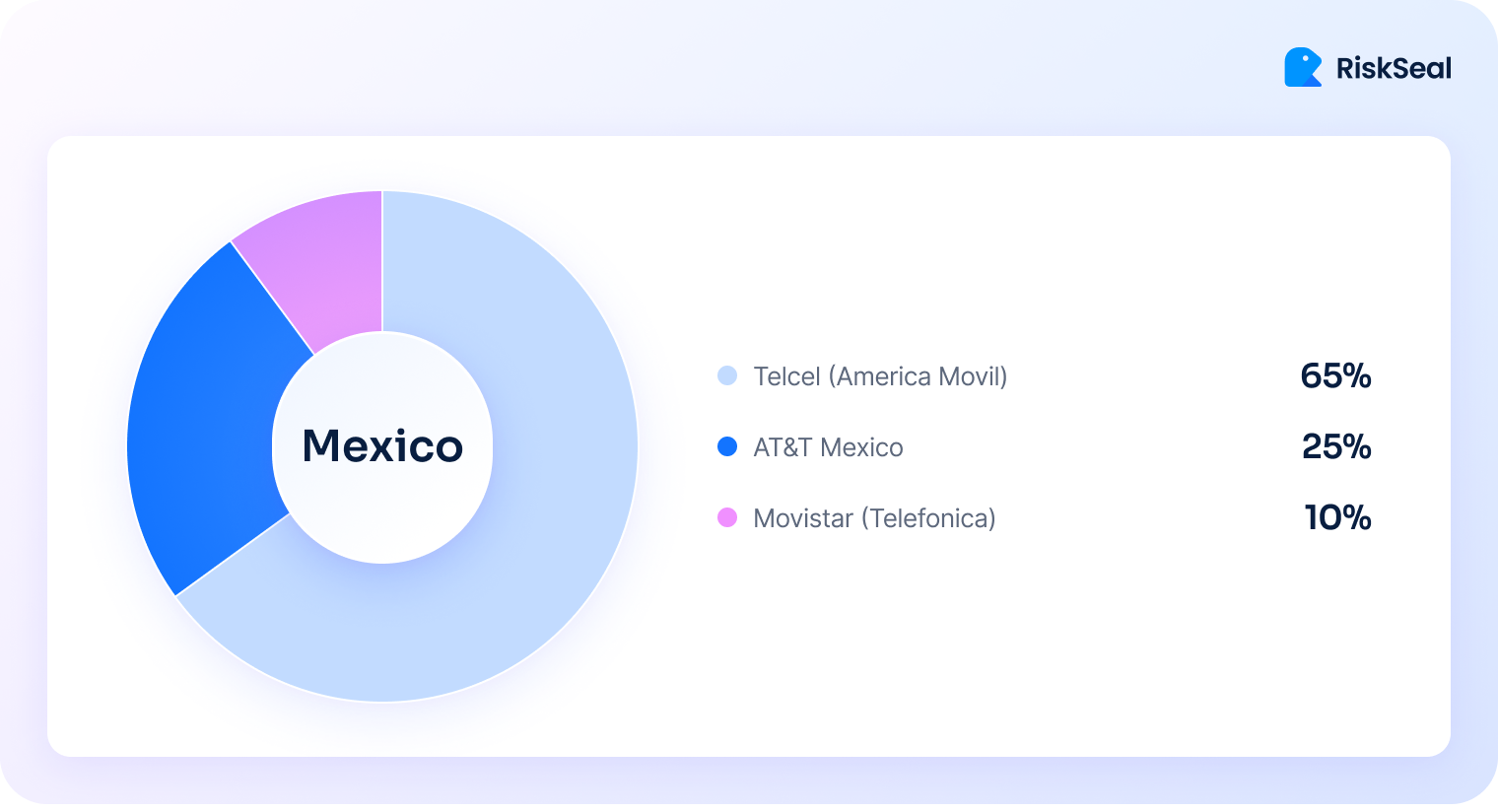

Mobile operator data can indicate income regularity and financial discipline without requiring bank account data. Particularly, prepaid vs. postpaid status, account tenure, and top-up regularity. Telcel and AT&T are the primary carriers in Mexico.

Useful for: income regularity inference, stability signals.

Limitation: limited data-sharing agreements in some cases; must be obtained compliantly.

Network and IP signals

Device type, operating system, location consistency, and IP behavior can surface fraud risk and identity inconsistencies. Mismatches between stated location and IP origin, or device fingerprints associated with fraud patterns, are relevant negative signals.

Useful for: fraud prevention, remote onboarding risk controls.

Limitation: not predictive of creditworthiness on its own.

Digital presence and platform activity

Registration on e-commerce platforms, streaming services, or professional networks suggests financial engagement and consumer activity.

Platforms popular in Mexico, including Netflix, Amazon Prime, and domestic equivalents, provide signals about disposable income and payment regularity.

Useful for: stability indicators, income inference.

Limitation: subscription status can change; requires ongoing data currency.

Delivery and mobility platforms

Active use of platforms like DiDi or Rappi, whether as a customer or a registered driver or courier, provides both behavioral and income-related signals. Driver and courier accounts, in particular, suggest verifiable income activity.

Useful for: gig worker income assessment, activity-based stability signals.

Limitation: income can be irregular; should be combined with other indicators.

Job portal signals

Registered profiles on employment platforms like Indeed or Computrabajo indicate job-seeking activity, employment sector, and in some cases, stated income level. Profile completeness and activity recency are secondary signals.

Useful for: employment status inference, sector-level risk context.

Limitation: self-reported data; needs corroboration.

Utility, rent, and paid services signals

Where available, data on consistent rent or utility payments is among the most credit-relevant alternative signals – it directly mirrors the payment discipline that bureaus measure through formal credit. Subscription payment history follows similar logic.

Useful for: repayment behavior inference for unbanked borrowers.

Limitation: availability depends on data-sharing partnerships with providers.

Compliance and negative signals

Sanctions lists, politically exposed person (PEP) registries, and adverse media monitoring serve as fraud and compliance filters rather than creditworthiness indicators, but they're a necessary layer in any responsible alternative scoring framework.

Useful for: KYC compliance, fraud prevention, regulatory risk management.

Limitation: not a positive creditworthiness signal; a screening layer only.

Digital footprint analysis in Mexico

Mexico's internet penetration makes digital footprint analysis particularly practical here. Statista data shows approximately 96 million internet users in 2023, with projections exceeding 131 million by 2029.

That's a large population leaving consistent, traceable digital activity, even if they've never held a bank account.

The key insight is that digital adoption and financial inclusion don't move in parallel. Someone can be an active internet user, a regular e-commerce shopper, a gig platform worker, and a streaming subscriber. And still be completely invisible to a credit bureau.

That gap is where digital footprint analysis adds real value for lenders. Rather than asking "does this person have a credit history?", it asks: "does this person have a consistent, verifiable digital identity? And what does their online behavior suggest about stability, risk, and fraud exposure?"

For remote onboarding – increasingly standard in digital lending – this matters even more. When there's no in-person verification, digital signals become a primary tool for identity confirmation and early fraud detection.

Local signals are particularly important. A borrower active on DiDi, registered on Computrabajo, and paying a Telcel postpaid plan tells a different story than someone with no verifiable local digital footprint. Platform familiarity with Mexico's specific ecosystem meaningfully increases the signal quality.

I think this is where many international lenders entering Mexico underestimate the complexity: global digital signals are a starting point, but local platform coverage is what makes the difference in signal quality for Mexican borrowers.

How RiskSeal supports alternative credit scoring in Mexico

RiskSeal's role is to complement, not replace, traditional bureau data. For borrowers who do have a bureau record, RiskSeal enriches their profile with digital risk signals. For thin-file or no-file borrowers, it provides the primary digital assessment layer.

The core process: RiskSeal analyzes a borrower's name, phone number, email address, and IP across 200+ online services, returning 400+ data points and a pre-built digital credit score to the lender. This supports credit decisioning, fraud screening, and identity verification within a single workflow.

In Mexico specifically, RiskSeal covers regional platforms from DiDi and Rappi to Telcel, AT&T, Indeed, Computrabajo, and many others alongside global services. This local coverage matters because Mexican borrowers who are invisible to bureaus often have active footprints on domestic platforms.

The output is an enriched borrower profile:

- digital stability indicators

- identity consistency signals

- fraud risk flags

- a composite digital score

All delivered to the lender's team to support underwriting, not to override their judgment. For a detailed breakdown of RiskSeal's alternative data coverage specific to Mexico, see alternative data for Mexican digital lenders.

Inside the LATAM alternative credit data report

FAQ

Does Mexico have credit scores?

Yes. Mexico has a functioning credit scoring infrastructure. The two main credit bureaus are Buró de Crédito and Circulo de Crédito. They collect borrower data and generate credit reports used by banks and financial institutions to evaluate lending applications.

Does Mexico have a credit score system?

It does, though it differs from models like the US FICO system in terms of population coverage. Buró de Crédito operates as the primary bureau, and Circulo de Crédito uses FICO-based methodology with some local adaptations, including the ability to factor in family credit history. Both bureaus serve formal lenders, but coverage gaps are significant. Roughly half the adult population lacks a bureau profile.

What credit bureaus operate in Mexico?

Two main bureaus: Buró de Crédito, the primary official bureau, and Circulo de Crédito, a private bureau using FICO-based models. Both collect data from creditors and financial institutions and provide credit reports to lenders assessing borrower creditworthiness.

What is alternative credit scoring in Mexico?

Alternative credit scoring uses data sources outside traditional credit bureaus to assess borrower risk. This includes telecom records, utility payments, e-commerce activity, digital platform registrations, and digital footprint signals. It doesn't replace bureau data. It supplements it, particularly for applicants who lack a sufficient credit history to generate a reliable bureau score.

Why is traditional credit scoring limited in Mexico?

Coverage is the core issue. Roughly 55% of Mexico's workforce operates informally, and around half of adults don't hold bank accounts. These individuals leave no trace in bureau records, regardless of their actual financial behavior. Thin-file and no-file borrowers aren't automatically high-risk. They're simply unassessable through conventional bureau channels.

What types of alternative data can lenders use in Mexico?

Lenders in Mexico can draw on a range of alternative data categories: phone and email signals, telecom account data, device and IP behavior, digital platform activity (e-commerce, streaming, mobility apps), job portal registrations, utility and subscription payment history, and compliance screening signals. Each category contributes different signals, from identity consistency to income stability to fraud risk.

How does digital footprint analysis support credit scoring in Mexico?

Digital footprint analysis examines a borrower's online presence and activity to assess identity consistency, digital stability, and fraud risk. With around 96 million internet users in Mexico, a large share of the unbanked population maintains an active and traceable digital presence. For remote onboarding and digital credit decisioning, footprint signals fill the gap left by absent bureau records.

Why is alternative credit scoring useful for fintech lenders in Mexico?

According to Finnovista's Fintech Radar, 170 local fintech lenders are operating in Mexico — many of them specifically targeting underserved borrowers. Alternative credit scoring allows these lenders to responsibly extend credit to thin-file applicants, improve approval rates without increasing default risk, and reduce fraud exposure during remote onboarding — all in a market where bureau coverage is structurally incomplete.

What are the risks of using alternative data for credit scoring?

Alternative data comes with real limitations: data quality can vary, not all sources are equally reliable, and some signals are indirect proxies rather than direct repayment indicators. Ethical and compliance considerations matter too. Data must be collected and used in accordance with applicable privacy regulations and with appropriate consent. The strongest approach combines alternative data with bureau checks and human underwriting oversight rather than relying on any single signal type.

How does credit scoring work in Mexico?

There is traditional and alternative credit scoring in Mexico. The former assesses a borrower's creditworthiness based on their credit history, which is provided to banks by Mexico's Official and private credit bureaus.

Alternative credit scoring in Mexico involves evaluating applicants based on non-traditional data that goes beyond credit history and traditional credit ratings.

See more

Learn key behavioral data types, real-world use cases, and benefits for lenders.

.webp)

Explore the urgent need for alternative credit scoring methods in Nigeria, as traditional systems fail to meet the substantial credit demands.

Discover four practical ways to strengthen consumer credit risk in 2026 with real-time underwriting, alternative data, smarter collections, and compliance-ready AI.