Digital Credit Scoring Platform for Emerging Markets

API-based solution for real-time credit scoring powered by digital footprint analysis. Used by lenders across LATAM, Asia, Africa, and beyond to reduce risk, expand lending, and approve more reliable borrowers.

Key benefits of using alternative credit score software

Spot creditworthy applicants

Identify solvent customers relying on 400+ real-time signals we deliver.

Detect potential defaulters early

Find suspicious signs that traditional digital credit solutions often miss and flag future defaulters.

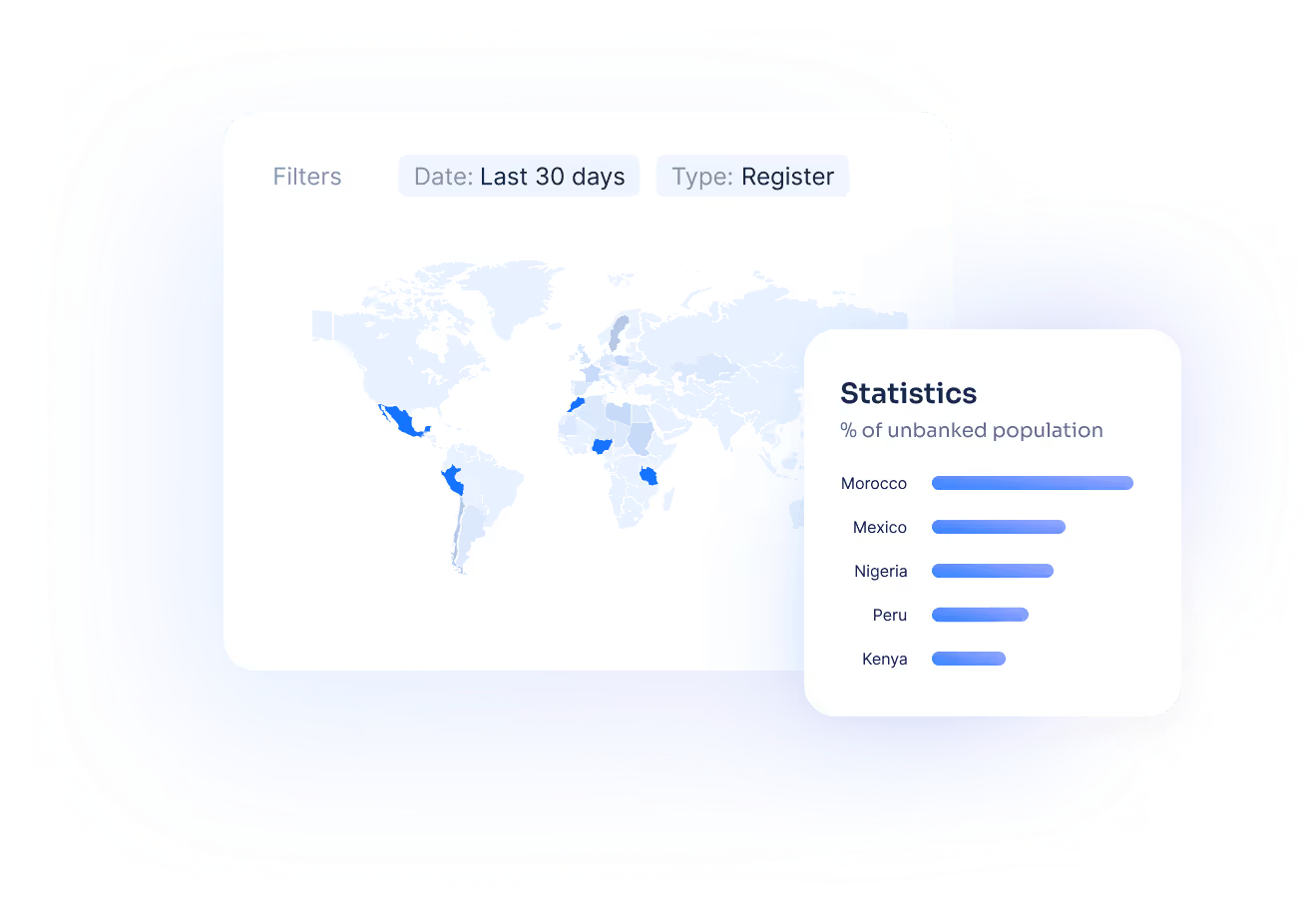

Reach unbanked customers

Let RiskSeal be the bridge between your company and underserved populations.

Lend with confidence in emerging markets. Even when traditional data is limited.

AI-powered software

for credit scoring in real time

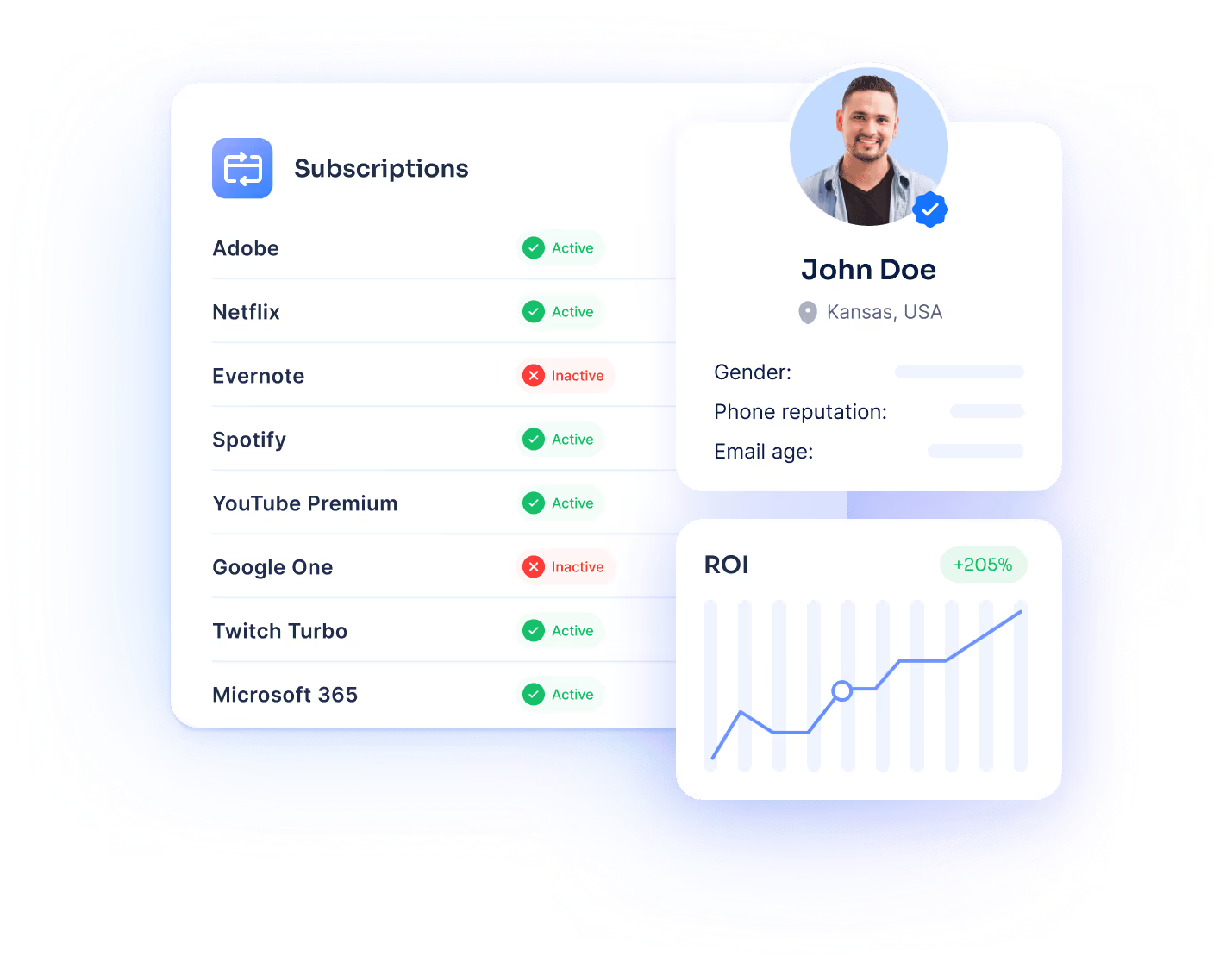

Our Digital Credit Scoring solution analyzes the borrower’s email, phone number, IP address, full name, location, and photo, then evaluates their digital footprint from over 200 online platforms.

With just a single API call, RiskSeal provides lenders with 400+ customer insights, a detailed client profile, and a ready-to-use digital credit score.

Digital identity verification

The real-time authentication of a borrower's identity using online verification methods.

Detailed consumer profile

A 360-degree view of consumer digital footprints, spotlighting lifestyle habits for detailed understanding.

Alternative data points

400+ data points in a digital scoring system to enrich models and cut approval time to seconds.

Region-specific signals

Local online services and market-specific insights enhance borrowers’ evaluation.

Why lenders choose RiskSeal

Approved customer base growth

Identification of trustworthy customers from high-risk ones, even with low or no credit rating.

Proactive default prevention

Stop defaulting loans before they happen and avoid the cost of debt collection, or loss from no repayment.

Credit risk reduction

Real-time, accurate, and extensive data to spot default risk, even in underbanked areas or without access to a credit bureau.

Market Expansion

Enter new markets by using a credit scoring tool to reach unbanked and underbanked populations.

Lower cost of risk

Leverage the predictive capability of AI and ML to improve digital scorecards, decreasing the cost of risk.

Great UX

Shorten the credit decision time from days to seconds with 400+ customer insights delivered in real time.

Industries we empower with real-time credit scoring

Online lending

RiskSeal helps online lenders go beyond traditional checks by using 400+ alternative data signals. Our credit risk rating software enables faster approvals, sharper risk assessment, and higher accuracy in spotting reliable borrowers.

BNPL

Our credit scoring software solution supports BNPL providers with real-time signals to assess creditworthiness and detect synthetic identities. This results in lower delinquency rates and stronger repayment.

Neobanks

RiskSeal’s digital credit scoring solution allows neobanks to evaluate applicants in seconds, flagging high-risk cases early and cutting onboarding costs. This way, more good customers can be approved without friction.

Banks

For traditional banks, RiskSeal enriches credit bureau reports with alternative data. By analyzing digital footprints, our credit scoring software reduces false approvals and increases portfolio resilience.

Client success stories

See how RiskSeal’s unique data sources generate pure Gini uplift, even in emerging markets. Real numbers. Real before/after performance.

.webp)

.webp)

.webp)

FAQ

What is RiskSeal's Digital Credit Scoring Platform?

RiskSeal is a real-time credit scoring platform that helps lenders assess risk by analyzing an applicant’s digital footprint tied to their email address, phone number, IP address, etc.

It converts verified digital and behavioral signals tested across millions of applications into a single Digital Credit Score that predicts repayment behavior.

As credit risk rating software, RiskSeal adds science-backed context where traditional credit data is limited, outdated, or unavailable.

It enables lenders to approve low-risk thin-file applicants, detect synthetic identities through profile consistency checks, and make faster, fairer, more confident lending decisions.

What data will I get by using RiskSeal's digital credit scoring solution?

RiskSeal analyzes over 400 real-time digital signals that show how applicants behave and engage online. These signals help lenders understand identity strength, stability, and financial behavior.

You'll receive insights across 7 key data categories:

1. Email data. Checks if an email is valid, how old it is, what type of domain it uses, whether it was exposed in breaches, and where it is used online.

2. Phone number data. Confirms if a number is real and active, its age, carrier, blacklist status, and use on messaging apps like WhatsApp or Telegram.

3. Social media activity. Public signals from platforms like Facebook, LinkedIn, or Instagram that reflect digital maturity and consistency.

4. Online shopping behavior. Engagement with marketplaces such as Amazon, eBay, Walmart, Mercado Libre, and others. This shows account age and everyday purchase activity.

5. Paid subscriptions. Ongoing use of services like Netflix, Disney+, or Spotify. These patterns can indicate budgeting habits and financial discipline.

6. Web and tech services. Signals from accounts with Apple, Google, Zoho, and similar platforms that show long-term digital engagement.

7. IP and network data. Connection type and location checks that help detect unusual or high-risk access patterns.

RiskSeal also includes AI-based identity checks, such as name matching and face comparison across profile images.

This helps confirm that the same person appears consistently across platforms – a critical defense against synthetic identities and account takeovers.

Together, these signals form a complete picture of an applicant's digital life, revealing patterns that traditional credit bureaus simply cannot see.

How does RiskSeal's Digital Credit Score work?

The Digital Credit Score is a real-time, country-specific model built on behavioral patterns from over 100 million loan applications. Our digital scoring system evaluates both the quantity and quality of an applicant's digital presence turning it into a predictive score from 0 to 999.

What it measures:

-Digital maturity. How long have they used their email, phone, and online accounts?

-Behavioral consistency. Do their devices, IP addresses, and identity elements remain stable over time?

-Financial signals. Do they maintain paid subscriptions, shop online regularly, and show signs of budgeting discipline?

Score ranges help guide decisions:

-0-299. Very high risk, frequent red flags, and mismatched signals.

-300-499. Elevated risk, requires enhanced verification or manual review.

-500-699. Moderate risk, acceptable with standard underwriting checks.

-700-799. Strong profile, solid applicant, minimal friction needed.

-800-899. Excellent profile, highly reliable digital footprint.

-900-999. Outstanding stability, exceptional trust, and consistency.

How accurate is RiskSeal's Digital Credit Score compared to traditional credit bureau scores?

Independent testing on 6+ million applications shows strong, stable predictive accuracy. Our credit score software achieved an AUC of 0.67 using digital data alone, effectively separating higher- and lower-risk borrowers without bureau data.

When combined with traditional bureau scores, performance improves significantly:

-Digital-only model: AUC 0.67

-Bureau-only model: AUC 0.69

-Combined model: AUC 0.73

This uplift proves digital and behavioral data add context that traditional sources miss.

Bureaus often struggle with thin-file or no-file applicants due to limited repayment history. RiskSeal analyzes stability signals that exist without formal credit records, delivering stronger model discrimination, higher approvals in underserved segments, and lower portfolio default rates.

Does RiskSeal support region-specific and local data sources?

Yes. RiskSeal’s software credit scoring approach analyzes both global platforms (Facebook, Instagram, Netflix, Amazon) and region-specific services people use daily.

Local platforms are critical for accurate credit risk assessment because they reflect real behavior within a country. For example:

-Allegro in Poland

-Mercado Libre and Didi Taxi in Mexico

-Shopee in Malaysia

-Namshi in Saudi Arabia

-Rappi in Colombia

-Tokopedia in Indonesia

These signals are difficult to fake. Genuine residents typically use essential local apps, while fraudsters and synthetic identities often show inconsistent activity that doesn’t match local norms.

By continuously expanding regional coverage, RiskSeal helps lenders make more accurate, fair decisions across both mature and emerging markets.

Can RiskSeal integrate with my existing loan processing system?

Yes. RiskSeal is designed as an API-based digital lending platform that works smoothly with your existing decisioning infrastructure.

It integrates via RESTful API with minimal development effort and can be added as an enrichment module to your current workflow.

You don't need to replace your existing credit scoring system – RiskSeal layers on top of it.

Implementation timeline:

-Initial API integration: 1 to 5 business days for technical connection and testing

-Full production deployment: 2 to 4 weeks, depending on internal testing, compliance, and workflow configuration

Our technical team supports you throughout the entire process to ensure integration is simple, fast, and aligned with your operational requirements.

Whether you're using Salesforce, custom-built systems, or specialized lending platforms, RiskSeal fits into your stack as a flexible credit scoring tool without disrupting your existing processes.

Is RiskSeal digital credit solution compliant with privacy regulations?

Yes. RiskSeal is built on privacy-first principles and holds ISO 27001 certification for information security.

We are fully compliant with:

-GDPR (European Union)

-Mexico's LFPDPPP (Federal Law on Protection of Personal Data)

-CCPA (California Consumer Privacy Act)

-Regional data protection laws (across Latin America, Asia, Middle East, and Africa)

All data is collected with user consent, processed lawfully, and stored securely with encryption at rest and in transit.

We do not sell or share personal data with third parties outside the scope of credit assessment.

Privacy and compliance are not add-ons; they are core to how our credit scoring platform operates.

This ensures that as you expand into new markets or face evolving regulations, RiskSeal remains a trusted and compliant partner.

How fast is RiskSeal's real-time credit scoring?

RiskSeal delivers results in approximately 5 seconds per application.

This real-time speed enables:

-Instant approval decisions without manual queuing

-Reduced friction in the customer journey

-Immediate fraud detection before funds are disbursed

Processing time may vary slightly based on regional platform coverage and optional features like facial recognition or enhanced identity verification.

Why real-time matters: Because data is captured at the exact moment of application, you see who the applicant is right now, not weeks or months ago.

This helps catch evolving fraud patterns, respond to changing borrower circumstances, and approve legitimate customers faster.

RiskSeal's credit scoring solution analyzes current behavior at the instant of application, giving you the most accurate, up-to-date risk signal possible.

What outputs does RiskSeal provide?

RiskSeal delivers three primary outputs for every applicant, giving you flexibility in how you use our credit scoring software solutions:

1. Digital Credit Score (0-999). A single, country-specific risk score trained on insights from over 100 million loan applications.

This score predicts repayment behavior at the exact moment of application.

2. Raw signal data. Full access to 400+ individual data points via API – email age, phone carrier type, social profile links, subscription activity, IP geolocation, and more.

This granular data allows you to build custom decision rules or enrich your existing models.

3. Decision flags and risk indicators. Pre-configured alerts for high-risk patterns like “TOR browser detected,” “email found in a spam list,” “invalid phone number,” or “identity mismatch across platforms.”

These flags enable immediate action without deep data analysis.

What results can I expect during a Proof of Concept?

A Proof of Concept runs on your actual loan portfolio – typically 5,000 to 20,000 recent applications – to measure real-world performance before full deployment.

Standard PoC structure:

-Data sharing. You provide 6-12 months of historical application data (anonymized if needed).

-Independent scoring. RiskSeal credit scoring tool evaluates the dataset and returns risk scores and flags.

-Client-side validation. You compare RiskSeal scores to your historical outcomes to see the impact.

Typical results clients observe:

-Model discrimination. +5 to 15 Gini points when RiskSeal signals are added to existing credit models

-Approval rates. 40-80% increase in thin-file segments without raising overall portfolio risk

-Default reduction. 15-25% improvement in portfolio-level default rates due to better segmentation

-Fraud detection. Earlier identification of synthetic identities, account takeovers, and coordinated fraud rings

Timeline. Most PoCs complete in 2-4 weeks.

How do I get started with RiskSeal?

Implementation takes 6-8 weeks across three phases:

Phase 1. Proof of Concept (2-4 weeks)

We score a sample of your past applications to measure approval lift, default reduction, and model accuracy. You provide a secure export of historical applications and outcomes. We deliver a performance report comparing results to your current approach.

Phase 2. API Integration (1-5 business days)

Our team connects RiskSeal’s API to your loan origination system. No system rebuild is required – it adds a data enrichment step to existing workflows.

Phase 3. Production Rollout (2-4 weeks)

Phased deployment, monitoring, and threshold optimization with your risk team.

Requirements: 5,000+ sample records, API access, workflow alignment.

RiskSeal becomes a fully operational credit scoring solution within weeks.

How is RiskSeal different from traditional credit bureaus?

Traditional bureaus and the RiskSeal credit scoring system play complementary roles in credit risk assessment.

Traditional bureaus:

-Rely on historical repayment data (loans, credit cards, utilities).

-Struggle with thin-file and no-file applicants.

-Update slowly and miss real-time behavioral signals.

RiskSeal:

-Analyzes real-time digital footprint and behavioral data.

-Works effectively for thin-file, no-file, and informal workers.

-Captures current stability patterns, even without formal credit history.

Bureaus answer: How was debt managed in the past?

RiskSeal answers: Does the applicant show stability right now?

Our credit scoring software solutions lift predictive accuracy from 0.67-0.69 standalone to 0.73 combined.

What if an applicant doesn't use social media?

Social media is not required to receive a RiskSeal score.

While it’s one signal category, RiskSeal analyzes 400+ signals across email, phone, IP/device data, e-commerce activity, paid subscriptions, web services, and social platforms.

Applicants can score strongly without social accounts. Stability signals may include:

-A years-old email with consistent usage

-A long-term mobile number

-Active subscriptions (Netflix, Spotify, etc.)

-Regular e-commerce activity

-Stable devices and IP addresses

These patterns reflect consistency and genuine digital engagement – often more predictive of repayment than social activity.

RiskSeal’s model evaluates overall signal coherence, not any single platform, ensuring fairness and making our credit scoring solution effective for both highly active and minimally visible digital users.

Won't analyzing digital footprints violate privacy laws?

No. RiskSeal’s credit scoring platform is built to comply with GDPR and regional data protection laws across LATAM, Europe, Asia, the Middle East, and Africa.

We ensure compliance through:

-Explicit consent. Obtained during the loan application process before any analysis begins.

-Public data only. No access to private messages or protected content.

-Legitimate interest. Credit risk assessment and fraud prevention are recognized legal bases.

-Data minimization. Only signals relevant to lending decisions are collected.

-Right to explanation. Applicants can request information about how their data was used.

-Secure processing. Encrypted data, ISO 27001-certified infrastructure, no third-party sales.

Digital credit scoring is a compliant, standard practice that improves inclusion while protecting privacy through transparency and proportional use of data.

How RiskSeal can improve the default ratio?

How does the integration with RiskSeal look like?

Can you provide examples of the digital and social footprint RiskSeal provides?

Does RiskSeal flag bad customers across the region?

.webp)