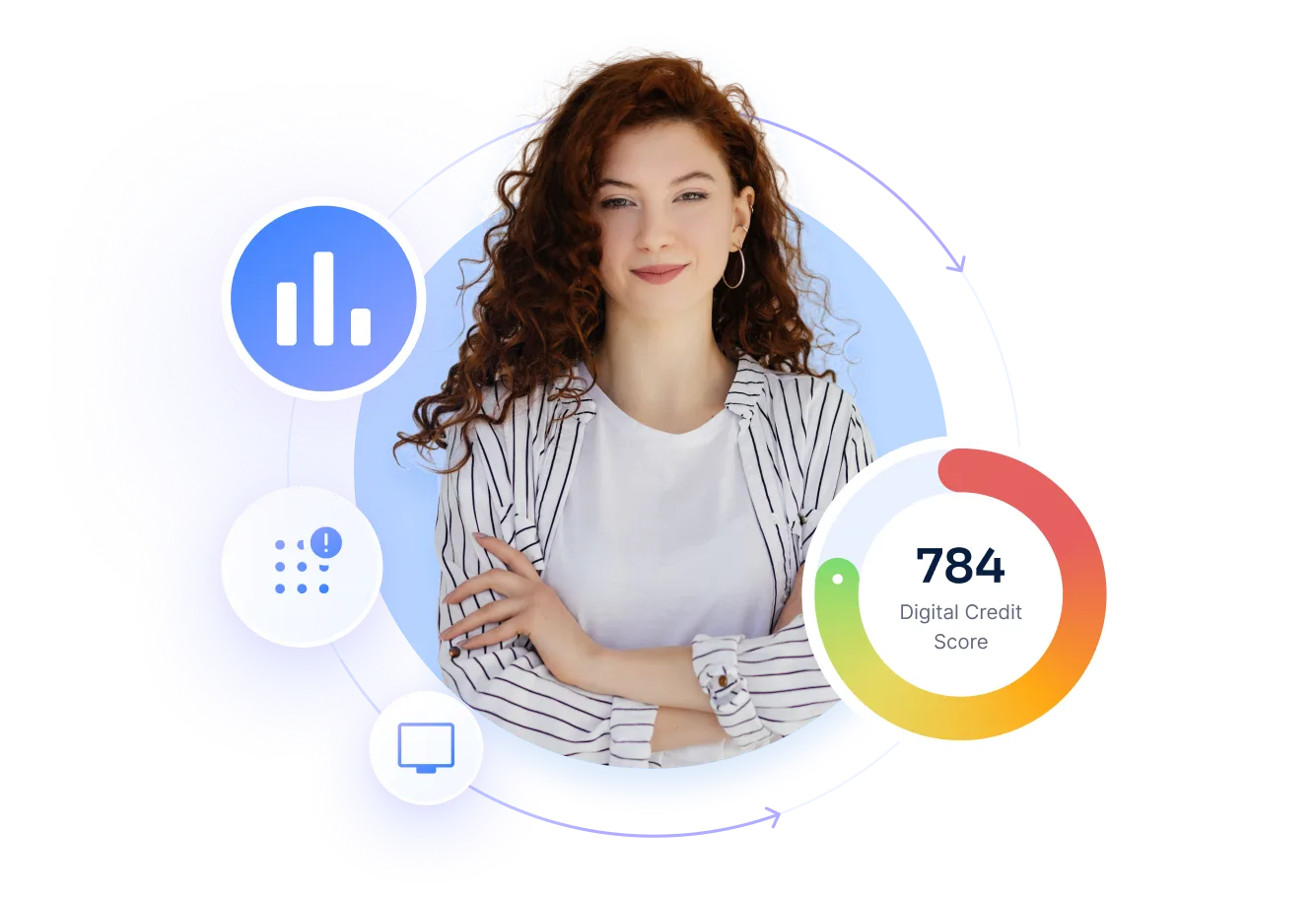

Plataforma de Scoring Crediticio Digital para Mercados Emergentes

Solución basada en API para la calificación crediticia en tiempo real, impulsada por el análisis de la huella digital.

Beneficios clave de utilizar software de calificación crediticia alternativa

Identifique clientes valiosos

Obtenga más de 400 datos de huella digital y evalúe con precisión a clientes solventes usando el puntaje de crédito.

Detect potential defaulters early

Detecta señales sospechosas que las soluciones tradicionales de crédito digital suelen pasar por alto y señala a futuros morosos.

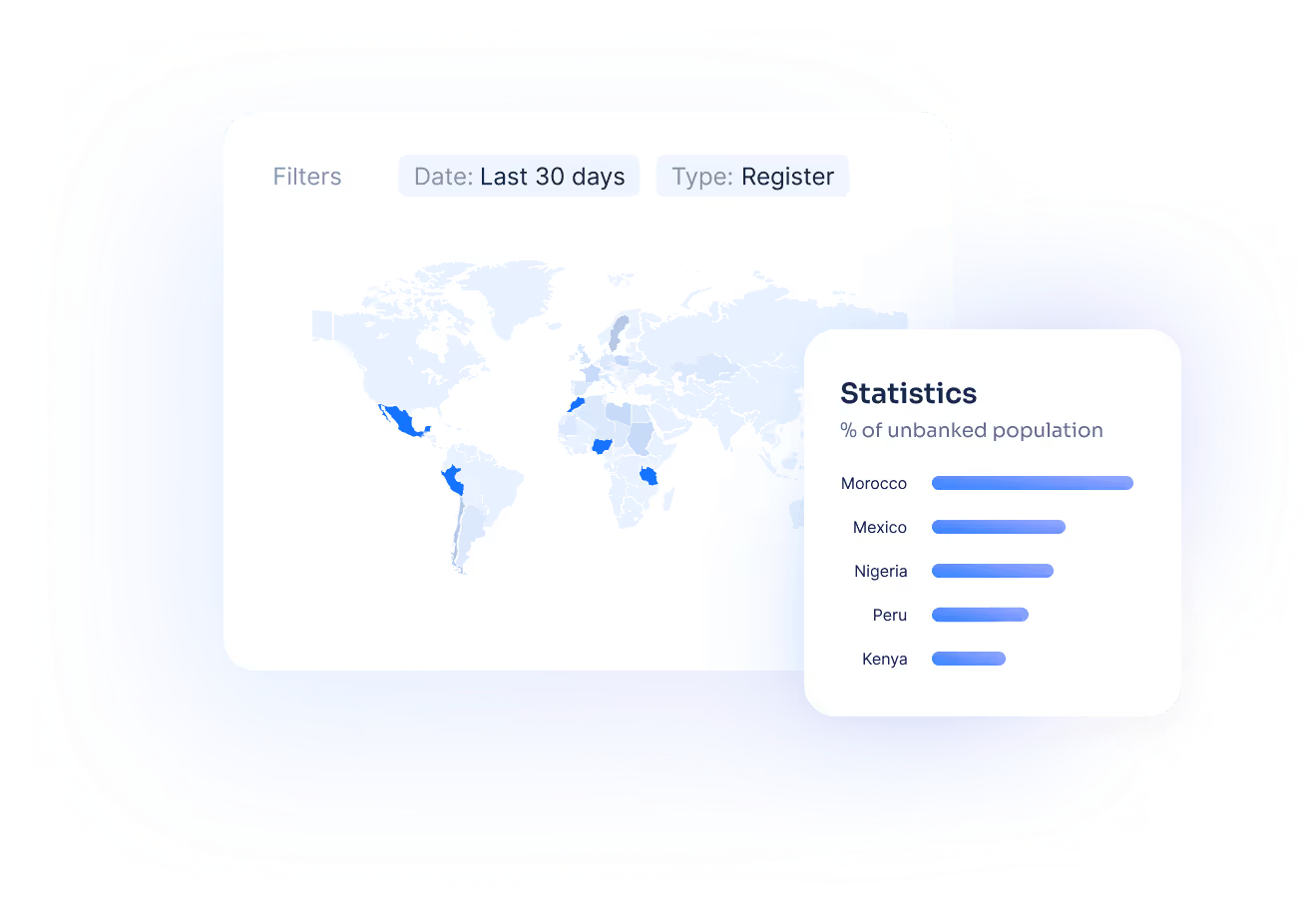

Reach unbanked customers

Acceda a mercados remotos no bancarizados o infrabancarizados y obtenga rápidamente una ventaja competitiva.

Proporcione préstamos con confianza en los mercados emergentes

Software impulsado por IA

para la calificación crediticia en tiempo real

Nuestra solución de Puntaje de Crédito Digital, una plataforma para scoring de créditos avanzada, evalúa la huella digital del prestatario analizando datos como correo, teléfono, IP, nombre, ubicación y foto en más de 200 plataformas en línea.

Con una sola llamada a la API, RiskSeal proporciona a los prestamistas más de 400 datos sobre los clientes, un perfil detallado del cliente y un puntaje de сrédito digital listo para usar.

Verificación de identidad digital

Autenticación en tiempo real de la identidad del prestatario mediante métodos de verificación en línea.

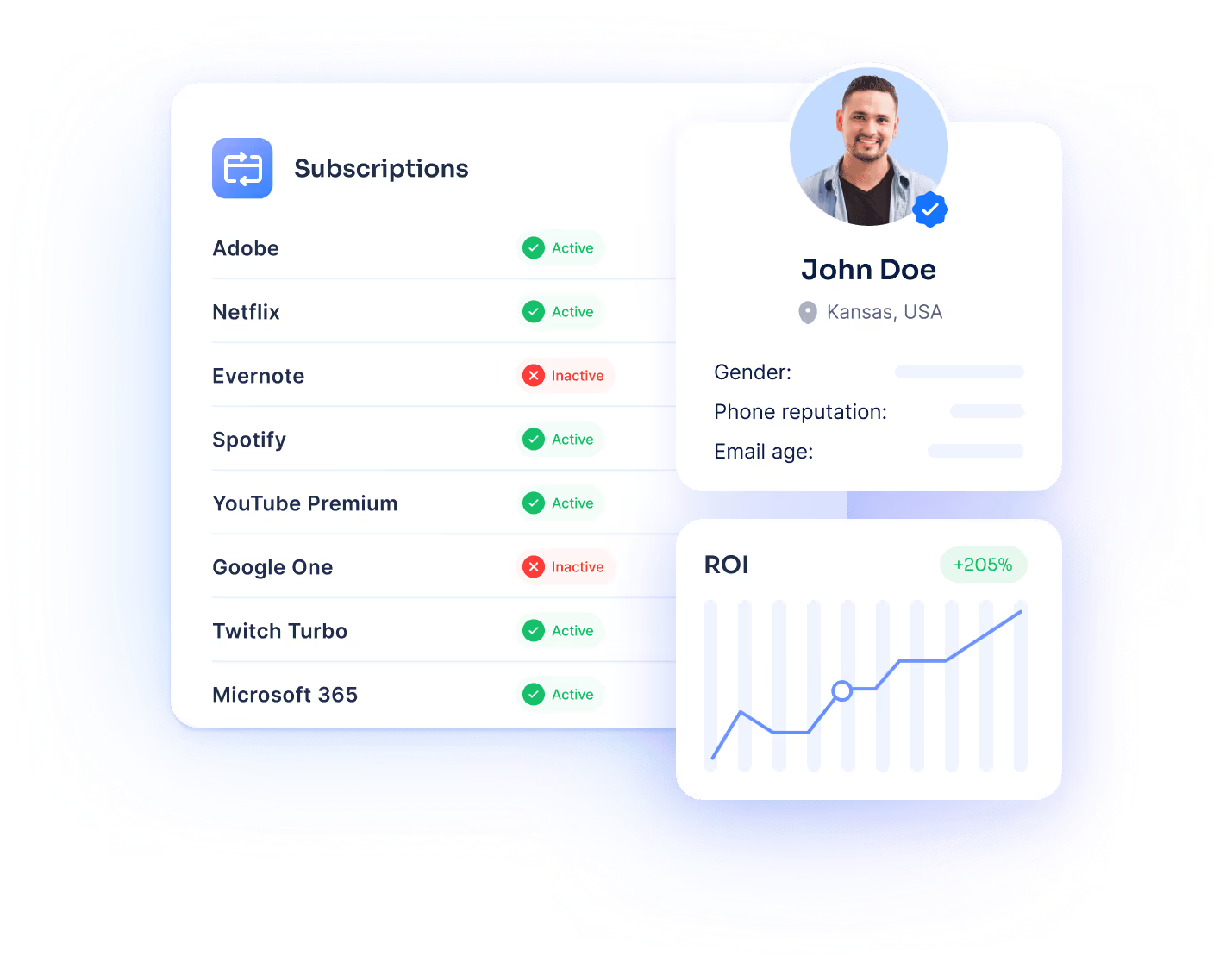

Perfil detallado del consumidor

Una vista de 360 grados de las huellas digitales del consumidor, que resalta sus hábitos de vida para una comprensión detallada.

Puntos de datos alternativos

Más de 400 puntos de datos en un sistema de calificación digital para enriquecer los modelos y reducir el tiempo de aprobación a segundos.

Específico

de la región

Los servicios locales en línea y las perspectivas específicos de cada mercado mejoran la evaluación de los prestatarios.

El impacto de RiskSeal solución

de Puntaje de Crédito Digital

Approved customer base growth

Identification of trustworthy customers from high-risk ones, even with low or no credit rating.

Proactive default prevention

Stop defaulting loans before they happen and avoid the cost of debt collection, or loss from no repayment.

Credit risk reduction

Real-time, accurate, and extensive data to spot default risk, even in underbanked areas or without access to a credit bureau.

Expansión del mercado

Entra en nuevos mercados utilizando una herramienta de calificación crediticia para llegar a poblaciones no bancarizadas y sub-bancarizadas.

Menor coste del riesgo

Aproveche la capacidad predictiva de AI y ML para mejorar las tarjetas de puntuación digital, reduciendo el costo del riesgo.

Gran UX

Reduzca el tiempo de decisión de crédito de días a segundos con más de 300 datos de clientes en tiempo real.

Industrias a las que empoderamos con calificación crediticia en tiempo real

Préstamos en línea

RiskSeal ayuda a los prestamistas en línea a ir más allá de las verificaciones tradicionales utilizando más de 400 señales de datos alternativos.

Compra ahora, paga después (BNPL)

Nuestra solución de calificación crediticia respalda a los proveedores de BNPL con señales en tiempo real para evaluar la solvencia y detectar identidades sintéticas.

Neobancos

La solución de calificación crediticia digital de RiskSeal permite a los neobancos evaluar a los solicitantes en segundos, identificando rápidamente casos de alto riesgo y reduciendo los costos de incorporación.

Bancos

Para los bancos tradicionales, RiskSeal enriquece los informes de las centrales de crédito con datos alternativos. Al analizar huellas digitales, nuestro software de calificación crediticia reduce las aprobaciones erróneas.

Casos de éxito de clientes

See how RiskSeal’s unique data sources generate pure Gini uplift, even in emerging markets. Real numbers. Real before/after performance.

.webp)

.webp)

Preguntas más frecuentes

How is RiskSeal different from traditional credit bureaus?

Traditional bureaus and the RiskSeal credit scoring system play complementary roles in credit risk assessment.

Traditional bureaus:

-Rely on historical repayment data (loans, credit cards, utilities).

-Struggle with thin-file and no-file applicants.

-Update slowly and miss real-time behavioral signals.

RiskSeal:

-Analyzes real-time digital footprint and behavioral data.

-Works effectively for thin-file, no-file, and informal workers.

-Captures current stability patterns, even without formal credit history.

Bureaus answer: How was debt managed in the past?

RiskSeal answers: Does the applicant show stability right now?

Our credit scoring software solutions lift predictive accuracy from 0.67-0.69 standalone to 0.73 combined.

¿Recibiré un Puntaje Digital de Crédito completo?

Sí, lo obtendrá. Nuestro sistema proporciona un puntaje de crédito digital totalmente evaluado que refleja la solvencia de la persona.

When combined with traditional bureau scores, performance improves significantly:

-Digital-only model: AUC 0.67

-Bureau-only model: AUC 0.69

-Combined model: AUC 0.73

This uplift proves digital and behavioral data add context that traditional sources miss.

Bureaus often struggle with thin-file or no-file applicants due to limited repayment history. RiskSeal analyzes stability signals that exist without formal credit records, delivering stronger model discrimination, higher approvals in underserved segments, and lower portfolio default rates.

Is RiskSeal digital credit solution compliant with privacy regulations?

Yes. RiskSeal is built on privacy-first principles and holds ISO 27001 certification for information security.

We are fully compliant with:

-GDPR (European Union)

-Mexico's LFPDPPP (Federal Law on Protection of Personal Data)

-CCPA (California Consumer Privacy Act)

-Regional data protection laws (across Latin America, Asia, Middle East, and Africa)

All data is collected with user consent, processed lawfully, and stored securely with encryption at rest and in transit.

We do not sell or share personal data with third parties outside the scope of credit assessment.

Privacy and compliance are not add-ons; they are core to how our credit scoring platform operates.

This ensures that as you expand into new markets or face evolving regulations, RiskSeal remains a trusted and compliant partner.

Can RiskSeal integrate with existing loan origination or credit decisioning systems?

Yes. RiskSeal is designed as an API-based digital lending platform that works smoothly with your existing decisioning infrastructure.

It integrates via RESTful API with minimal development effort and can be added as an enrichment module to your current workflow.

You don't need to replace your existing credit scoring system – RiskSeal layers on top of it.

Implementation timeline:

-Initial API integration: 1 to 5 business days for technical connection and testing

-Full production deployment: 2 to 4 weeks, depending on internal testing, compliance, and workflow configuration

Our technical team supports you throughout the entire process to ensure integration is simple, fast, and aligned with your operational requirements.

Whether you're using Salesforce, custom-built systems, or specialized lending platforms, RiskSeal fits into your stack as a flexible credit scoring tool without disrupting your existing processes.

What if an applicant doesn't use social media?

Social media is not required to receive a RiskSeal score.

While it’s one signal category, RiskSeal analyzes 400+ signals across email, phone, IP/device data, e-commerce activity, paid subscriptions, web services, and social platforms.

Applicants can score strongly without social accounts. Stability signals may include:

-A years-old email with consistent usage

-A long-term mobile number

-Active subscriptions (Netflix, Spotify, etc.)

-Regular e-commerce activity

-Stable devices and IP addresses

These patterns reflect consistency and genuine digital engagement – often more predictive of repayment than social activity.

RiskSeal’s model evaluates overall signal coherence, not any single platform, ensuring fairness and making our credit scoring solution effective for both highly active and minimally visible digital users.

Won't analyzing digital footprints violate privacy laws?

No. RiskSeal’s credit scoring platform is built to comply with GDPR and regional data protection laws across LATAM, Europe, Asia, the Middle East, and Africa.

We ensure compliance through:

-Explicit consent. Obtained during the loan application process before any analysis begins.

-Public data only. No access to private messages or protected content.

-Legitimate interest. Credit risk assessment and fraud prevention are recognized legal bases.

-Data minimization. Only signals relevant to lending decisions are collected.

-Right to explanation. Applicants can request information about how their data was used.

-Secure processing. Encrypted data, ISO 27001-certified infrastructure, no third-party sales.

Digital credit scoring is a compliant, standard practice that improves inclusion while protecting privacy through transparency and proportional use of data.