How to Enrich Scorecards With Reverse Phone Lookup Data. A Step-by-Step Guide

Discover how reverse phone lookup boosts credit risk scoring—verify identity, detect fraud, and assess solvency with just a phone number.

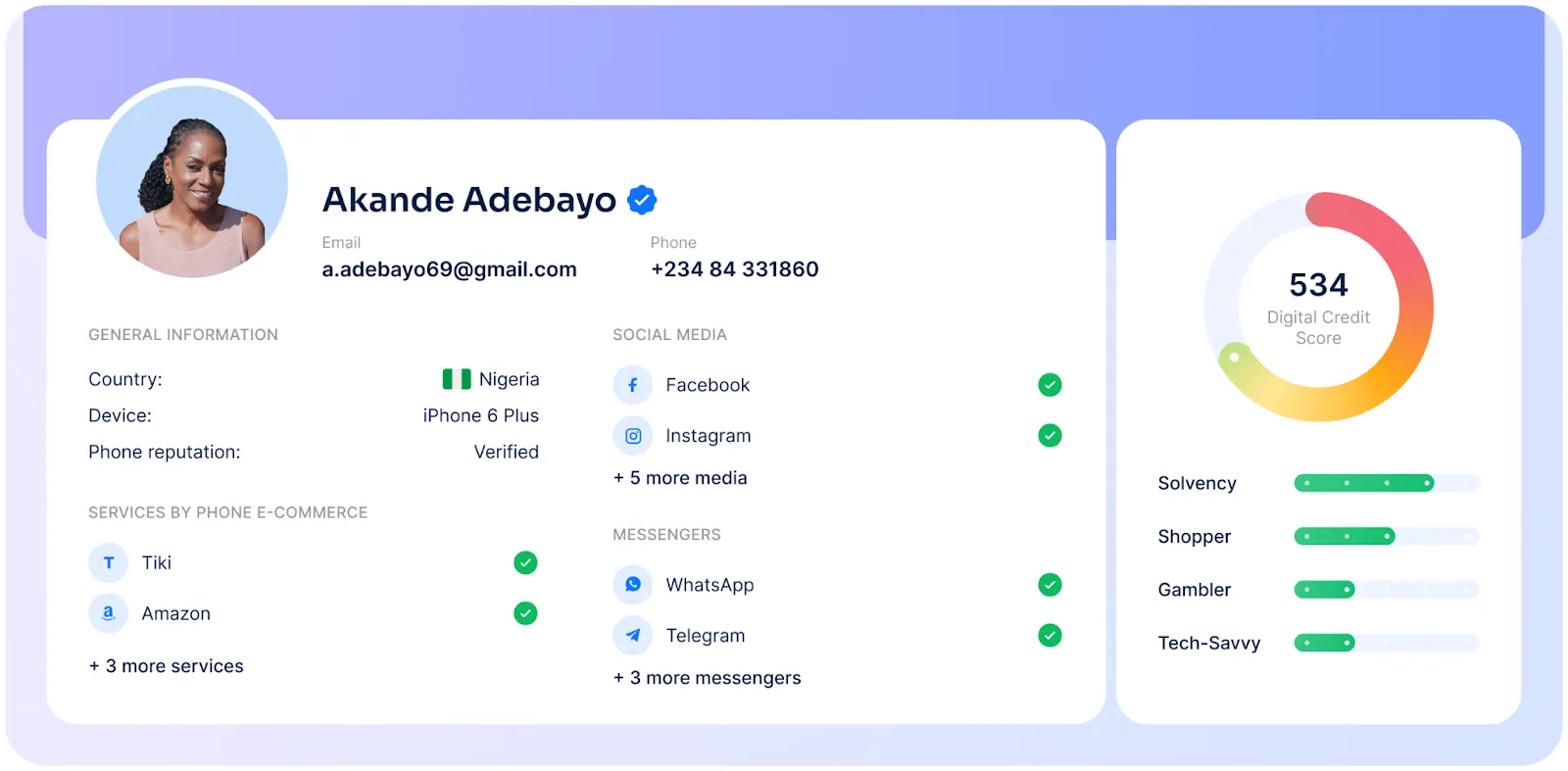

.webp)

When applying for a loan, a potential borrower usually provides their mobile phone number.

If the lender views it solely as a means of contacting a future client, they miss out on numerous opportunities.

After all, it can be used to look up information about a person that is inaccessible through traditional credit scoring.

In this article, we will discuss how enriching scorecards with phone number lookup data can benefit credit institutions.

Use cases of reverse phone lookup in credit risk

Reverse phone lookup is a technique that allows lenders to obtain a wealth of information about a potential borrower using only their mobile phone number.

With its help, credit institutions can enhance the following aspects of their operations:

#1. Risk management

Using reverse phone number search engine helps lenders build a more complete profile of each applicant.

This makes it easier to identify solvent clients and spot high-risk applicants.

This can be achieved through the following checks:

- Social and messenger accounts. Presence of messenger and social media accounts linked to the phone number.

- Digital footprints. The analysis of registrations on various platforms and other activity in the online space.

- Public profile check. Assessment of the number and quality of public profiles.

- Application vs. phone data. Comparison of phone lookup data with the information provided in the borrower's application form.

#2. Identity verification

Credit scoring with phone number lookup makes it possible to determine whether the applicant is truly who they claim to be.

Any discrepancies in the application may indicate potential fraud.

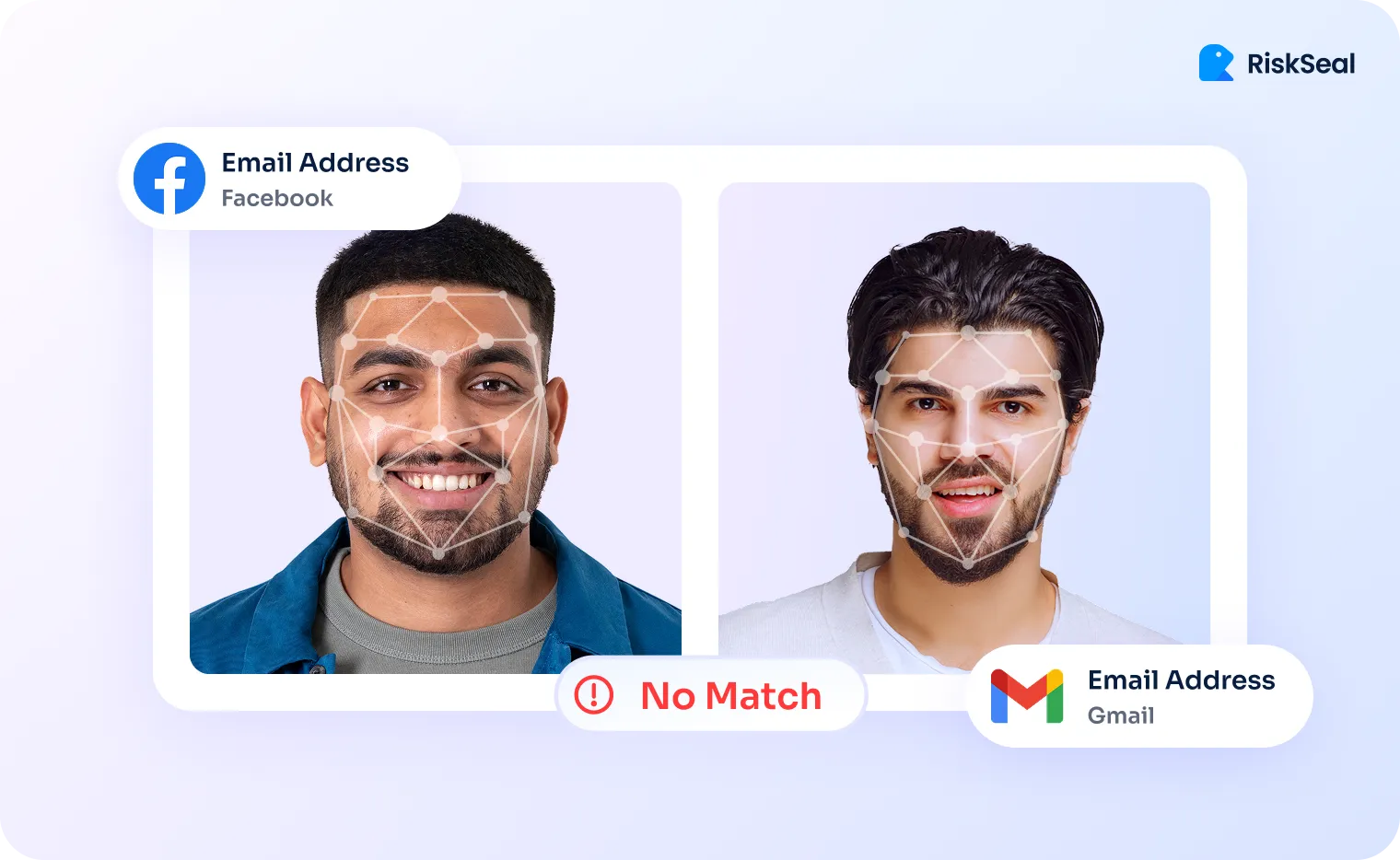

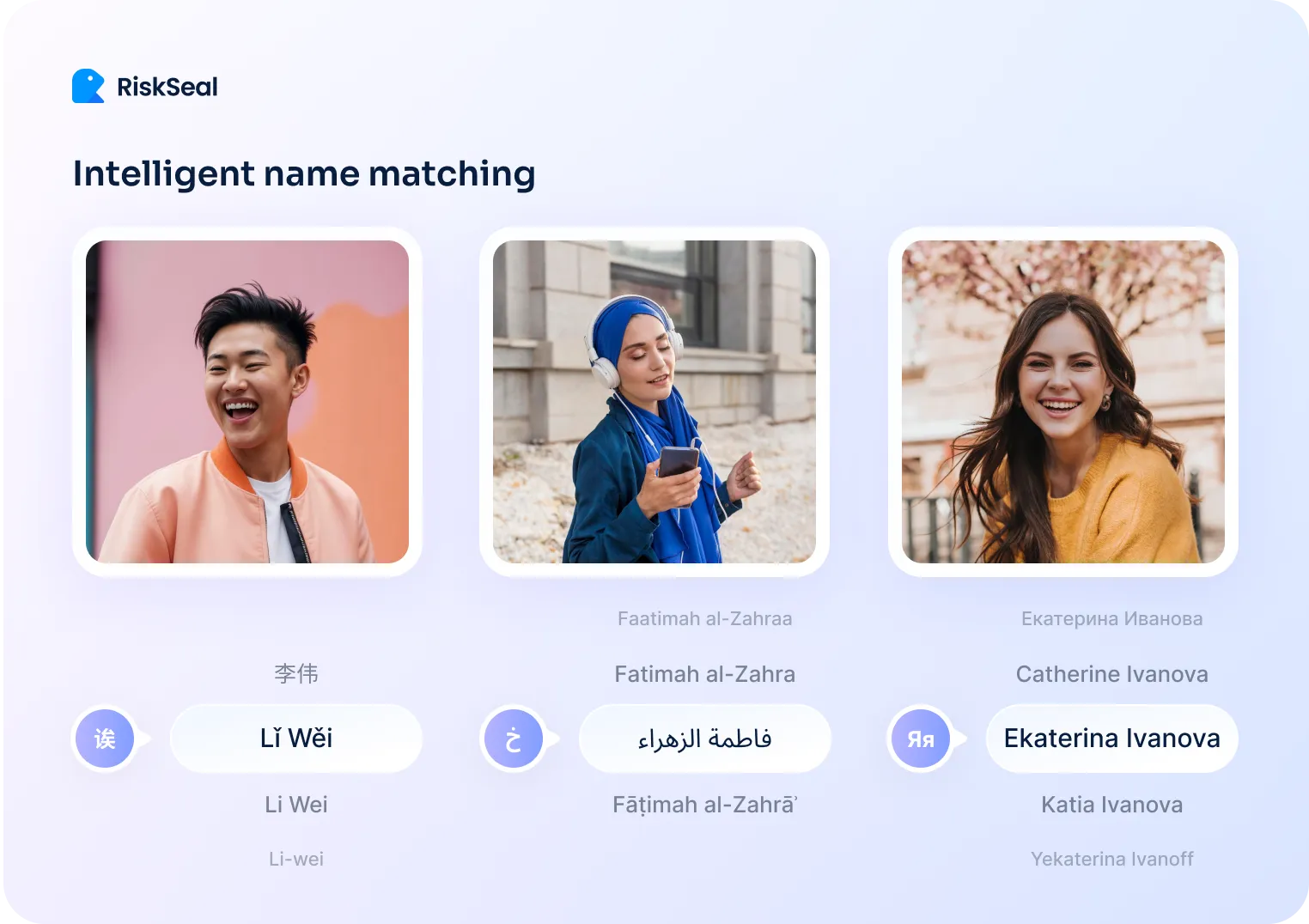

For example, the RiskSeal scoring system uses two types of checks for this:

- Face recognition. Comparing profile pictures in social network accounts and determining their identity.

- Name matching. Identifying inconsistencies in the user's names across different accounts.

#3. Solvency assessment

Thanks to the data obtained through reverse phone reviews, signs of financial instability can be identified.

Such data includes:

- The number and types of accounts linked to the number (paid/free).

- Subscriptions to premium services. For example, having a paid subscription to Netflix or Spotify is a positive sign.

- Regularity of online payments. Purchasing airline tickets, regular shopping on e-commerce platforms, etc., can increase the applicant's digital credit score.

#4. Fraud detection

Phone number lookup technology helps detect suspicious activity and prevent fraudulent loan applications.

The following methods are used for this:

- Flagging temporary contacts. Detection of disposable, virtual, and fake numbers.

- Cross-referencing. Checking the number in fraud databases and spam lists.

- Geo-IP discrepancy alert. This phone number lookup IP check detects mismatches between the country code and IP address.

- Lack of online presence. Absence of a digital footprint.

- SIM takeover indicators. Detection of signs of SIM-jacking (SIM Swap Scam).

- Identity verification. Check for a possible synthetic identity.

5. Pre-KYC verification. According to a recent survey, the cost of a single Know Your Customer (KYC) check ranges from $1,000 to $2,000. This was reported by 62% of respondents:

Reverse phone lookup can significantly reduce these costs. The technology allows the identification of potential fraudsters or defaulters right at the stage of submitting a loan application.

For example, the RiskSeal scoring system rejects 70% of suspicious applications at the preliminary KYC stage, saving its clients' funds.

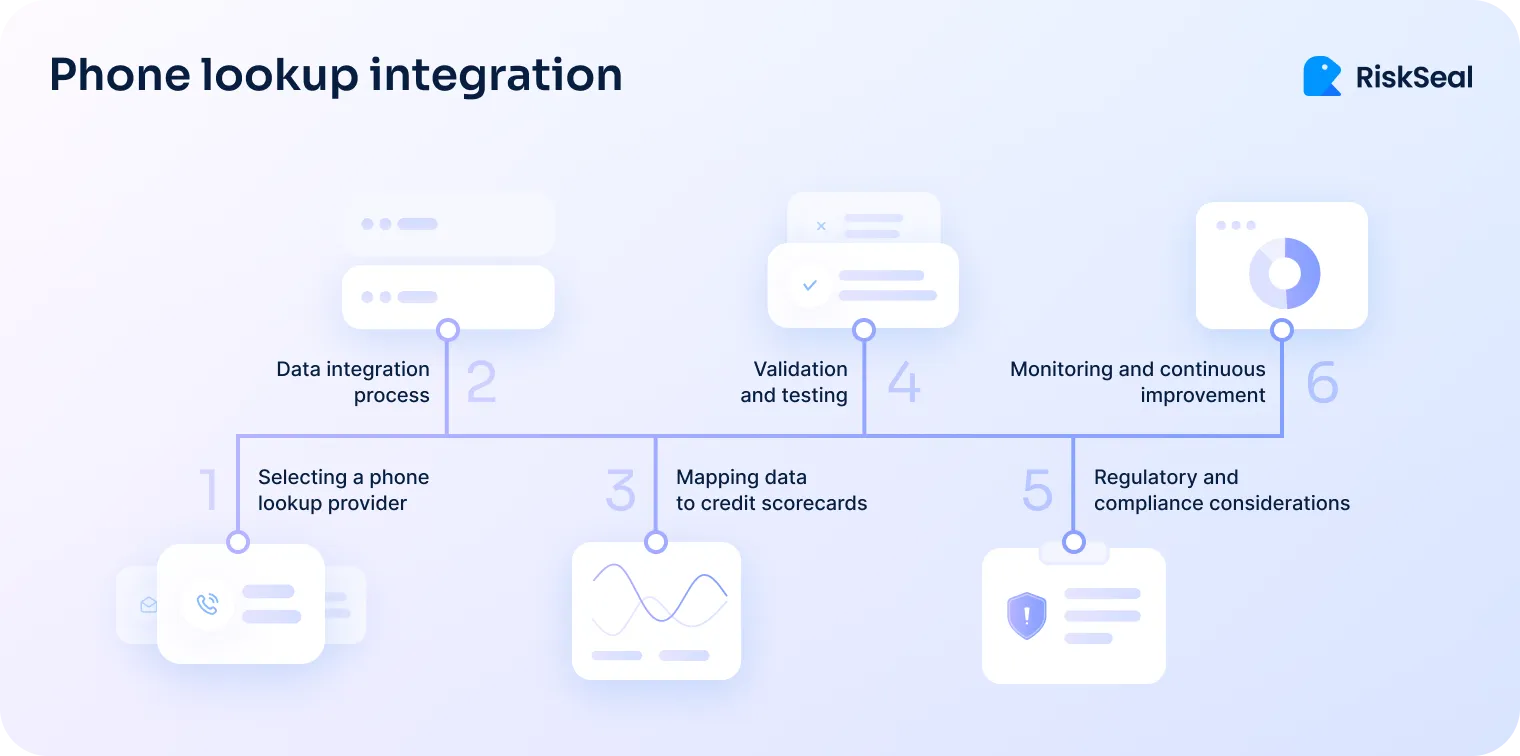

How to integrate phone lookup into the credit risk system

Phone number lookup is added step by step to the credit risk management process.

Here are six steps to follow:

Step #1. Selecting a phone lookup provider

When choosing a phone lookup data provider, several factors should be considered:

Data accuracy and relevance. Ensure that the provider has access to correct phone number information.

This way, you can be confident that your risk assessment is based on real and reliable data.

Reliable API integration. Choose a provider that offers a well-documented and secure API. This will allow real-time automated queries.

Also, you will be able to integrate the data easily into your existing system.

High scalability and performance. Remember that your customer base may grow. Your provider must be able to handle the increasing load.

Also, clarify the system's reliability metrics and the likelihood of delays, as these will affect decision-making speed.

Cost-effectiveness. Consider the price-quality ratio of the provided data. It is also important to check for a free PoC, corporate discounts, and other advantageous offers.

Support and documentation. Good customer support and detailed documentation will simplify the process of integrating the data into your processes.

Reputation and compliance. Study reviews about the alternative data provider and its reputation in the industry.

The provider's willingness to comply with privacy, security, and other regulations is also crucial.

Step #2. Data integration process

Once the provider is selected, you can proceed with integrating the data into your scorecard. This process includes:

Setting up the API connection. Connect to the provider's API and receive phone number information in real time.

Batch processing. Many providers offer this feature when online data lookup is not possible. It involves uploading phone numbers in CSV format for bulk searching.

Data formatting and standardization. To reduce errors, ensure that all phone numbers are provided in a consistent format.

For example, E.164, which includes a “+” prefix, country code, and subscriber number:

Secure data transfer. Use data encryption and secure API key management to meet compliance requirements.

Error tracking and handling. Ensure that your system logs API failures and responds appropriately to them. For example, by triggering a retry.

Integration testing. Before working with real clients, test the API integration in an isolated environment. Make sure the system is receiving correct data and analyzing it accurately.

Step #3. Mapping data to credit scorecards

At this stage, you need to incorporate data types into your credit scoring model that can significantly impact risk assessment.

Authenticity of the number. A phone verify lookup can show if the number is incorrect or disconnected, showing that the applicant is avoiding contact.

The use of so-called burner phones and disposable numbers is also suspicious — these are often used by fraudsters.

Phone type and operator information. IP telephony numbers carry the highest risk. These numbers can be easily and anonymously obtained online, meaning fraudsters may use them to conceal their true identity.

If the number belongs to a mobile operator, assess its reliability and check its history. Are there any fraud-related incidents associated with it in the past?

Landline numbers tied to a physical address are generally considered the most reliable.

User geolocation. Compare the country associated with the operator's code with the address provided in the loan application.

This information can also be compared with the user's established geolocation.

Any discrepancies may indicate fraud and justify assigning the applicant a high-risk level.

Presence in high-risk databases. Check if the number is included in databases related to fraud or spam. Such occurrences should be regarded as serious risk indicators.

Length of number ownership. If possible, find out how long the phone number has been active. Criminals often purchase a new number to carry out their schemes.

Suspicious activity. Some providers allow tracking unusual activity associated with a phone number.

For example, multiple accounts registered to one number or submitting multiple loan applications.

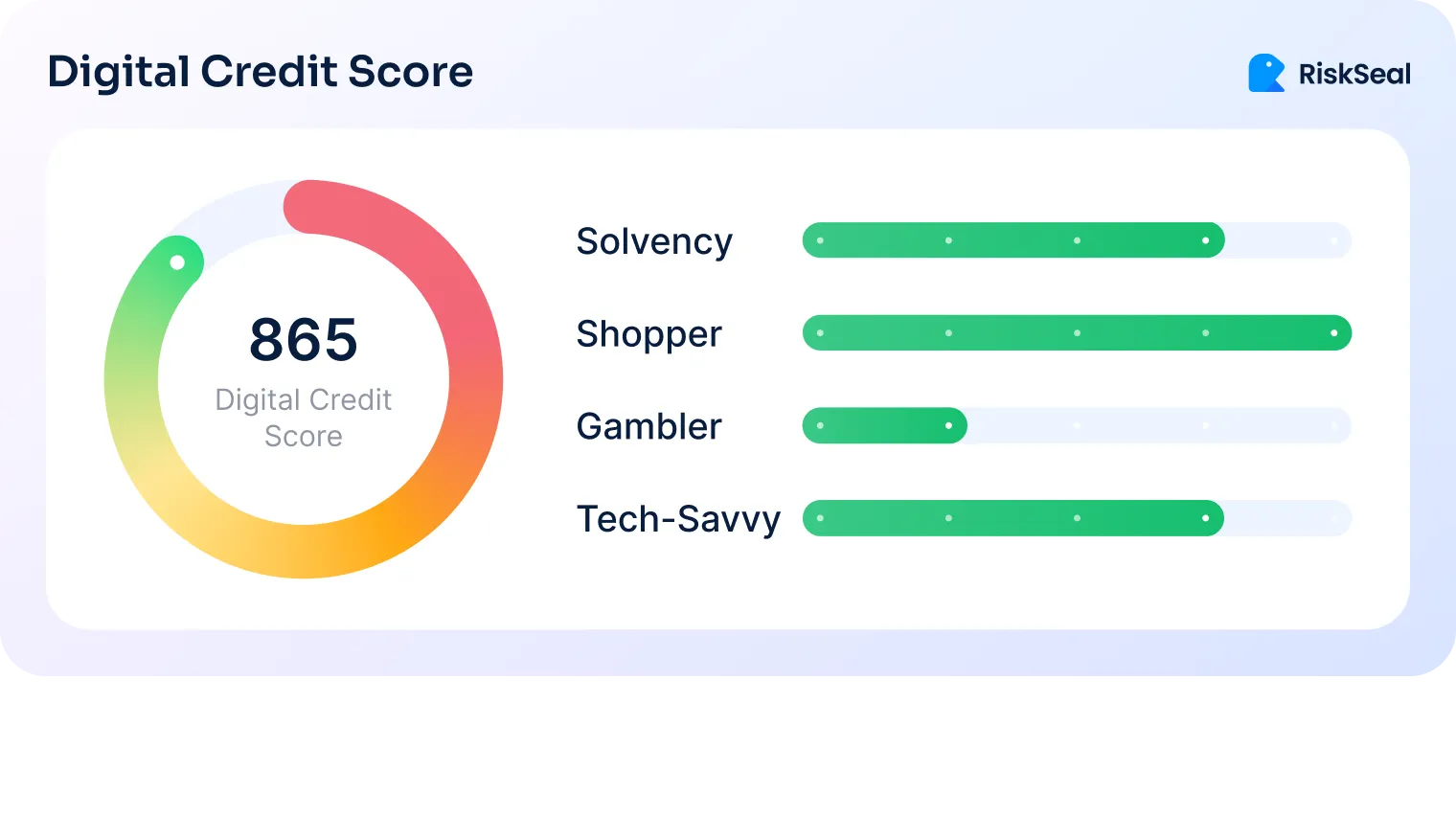

Overall risk assessment. Not all alternative data providers offer this feature. However, if it is available, the lender can see the applicant's overall risk score based on their phone number.

Typically, this is represented as a numerical value on a scale from 1 to 5, 1 to 100, or another range:

Additional creditworthiness assessment. A phone number not only helps identify fraudsters, but its analysis also aids in evaluating applicants with insufficient or no credit history.

This is facilitated by the large number of digital footprints that can be identified through reverse phone lookup. For example, accounts registered under the number on social media and other platforms.

Step #4. Validation and testing

Before fully integrating the changes into your credit scoring system, conduct thorough testing. This consists of several key stages:

Data quality check. Take a sample of phone lookup data and check its accuracy and relevance. The accuracy of decision-making regarding credit applications will depend on this.

Pilot testing. Implement new processes alongside existing ones. This will allow you to compare the effectiveness of traditional scoring and scoring using digital footprint analysis.

System performance monitoring. After enriching the scorecard with new data, check if they could have predicted defaults more accurately for existing loans.

Use historical data for analysis. Assess how well the results align with your expectations.

Performance and load testing. Assess whether the APIs can handle the existing load in your company.

Also, evaluate response times for searches, the presence of delays, etc.

Acceptance testing. Involve your risk and fraud analysts in the testing. Their experience will help evaluate how useful certain data is.

This way, you can integrate only the data that the team finds trustworthy.

Go/No-go check. Set success criteria for the integration of reverse phone lookup. Proceed with deployment only if these criteria are met.

Step #5. Regulatory and compliance considerations

Phone number lookup for fintech requires compliance with certain regulatory requirements. These include:

1. Fair Credit Reporting Act (FCRA). This law applies to companies operating in the United States.

It includes:

- Obtaining user consent for data collection

- Acceptably using the data

- Ensuring the accuracy and relevance of data used for credit application decisions

2. Privacy and data protection legislation. Phone numbers are considered personal data. Therefore, when using phone number lookup, you must comply with relevant laws.

These include GDPR in the EU, CCPA in California, etc.

Step #6. Monitoring and continuous improvement

After the final integration of phone lookup data, it is essential to continuously monitor the performance of your scoring system and improve it over time.

For this, it is important to:

Monitor key performance indicators. These include metrics for default, fraud cases, false positive and false negative results, etc.

This will help ensure the effectiveness of risk assessments.

Adjust the credit scoring model. For example, if you find that certain data allows more accurate fraud detection, increase its weight in the scoring model.

Conversely, overly stringent factors decrease their influence on the final result.

Maintain feedback with the underwriting team. They can confirm or disprove the value of certain data. This information can be used to adjust the models.

Stay updated on data and technology advancements. Maintain contact with your alternative data provide.

Over time, they may implement new features or add new signals to the available data set.

It is also important to regularly update the data to maintain its relevance.

Review the model’s predictive power. Do it regularly, as it may change over time due to factors outside your or the provider’s control.

For example, fraudsters might adapt, or borrower profiles could shift.

Maintain detailed documentation. Record all test results and changes made to the credit scoring models.

This can be useful for future operations and for demonstrating the return on investment to senior management.

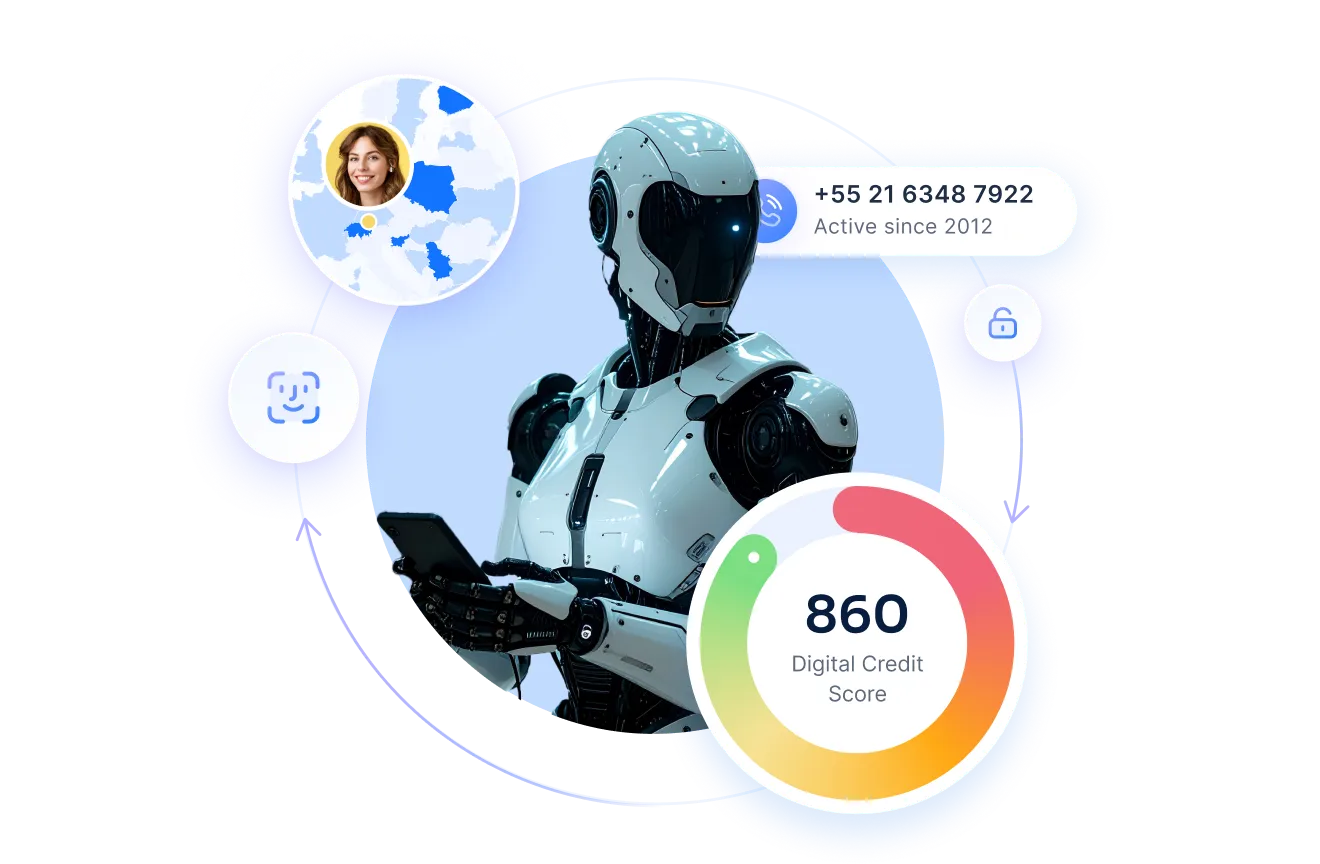

.svg)

Phone number lookup at RiskSeal

Reverse phone lookup is one of the techniques offered by the RiskSeal scoring system to its clients. It is specifically designed for fintech providers and offers them numerous capabilities.

You will also be able to detect invalid and disposable numbers, analyze users’ online activity, and check their geolocation.

This provides the lender with the following advantages:

- Effective risk management. You can quickly create a financial profile of the applicant and assess their solvency as accurately as possible.

- Fast decision-making on loan applications. Thanks to this, our clients report growth in their customer base and improved user experience.

- Reduction in fraud cases. Our checks help you quickly assess a borrower's reliability and get fraud risk alerts right at the loan application stage.

The RiskSeal Digital Credit Scoring system uncovers numerous data points about a person, knowing only their phone number.

For maximum risk management efficiency, we recommend leveraging all the platform’s features. You can combine phone number lookup with other technologies such as email lookup and IP lookup.

To help you assess the effectiveness of collaborating with RiskSeal, we offer a free Proof of Concept (PoC). This test will demonstrate the effectiveness of our solution for your business.

Key takeaways

Look up information about a person via their phone number is an effective way to optimize the credit scoring process.

It allows you to discover numerous alternative data points and integrate them into the credit organization’s scoring model.

This process involves several stages:

1. Selecting a provider of phone number lookup data

2. Integrating the data into the existing credit scoring model

3. Testing the effectiveness of the updated scoring model

4. Ensuring compliance with regulatory requirements

5. Monitoring performance and improving the model

The RiskSeal scoring system provides its clients with a comprehensive set of phone lookup data.

Integrating this data will help you speed up decision-making, reduce the number of fraudulently granted loans, and lower the default rate.

See more

Learn five different methods on how to discover the age of an email account.

Learn how to use alternative data to build fairer, more profitable credit models. And stay ahead of regulations.

Examine how to integrate location insights into your credit scoring models to reduce default rates and gain a competitive advantage.