How Email Analysis Helps Lenders Reduce Risk

Dive into how email analysis empowers lenders to reduce defaults, detect fraud, and enhance credit models.

.webp)

Every credit institution aims to reduce loan defaults. Other key priorities include reaching a wider audience and detecting fraud earl.

This is why lenders are increasingly turning to alternative data providers.

They improve their scoring models using various non-traditional data. One important source is the analysis of an applicant’s email.

The role of email risk assessment in credit risk management

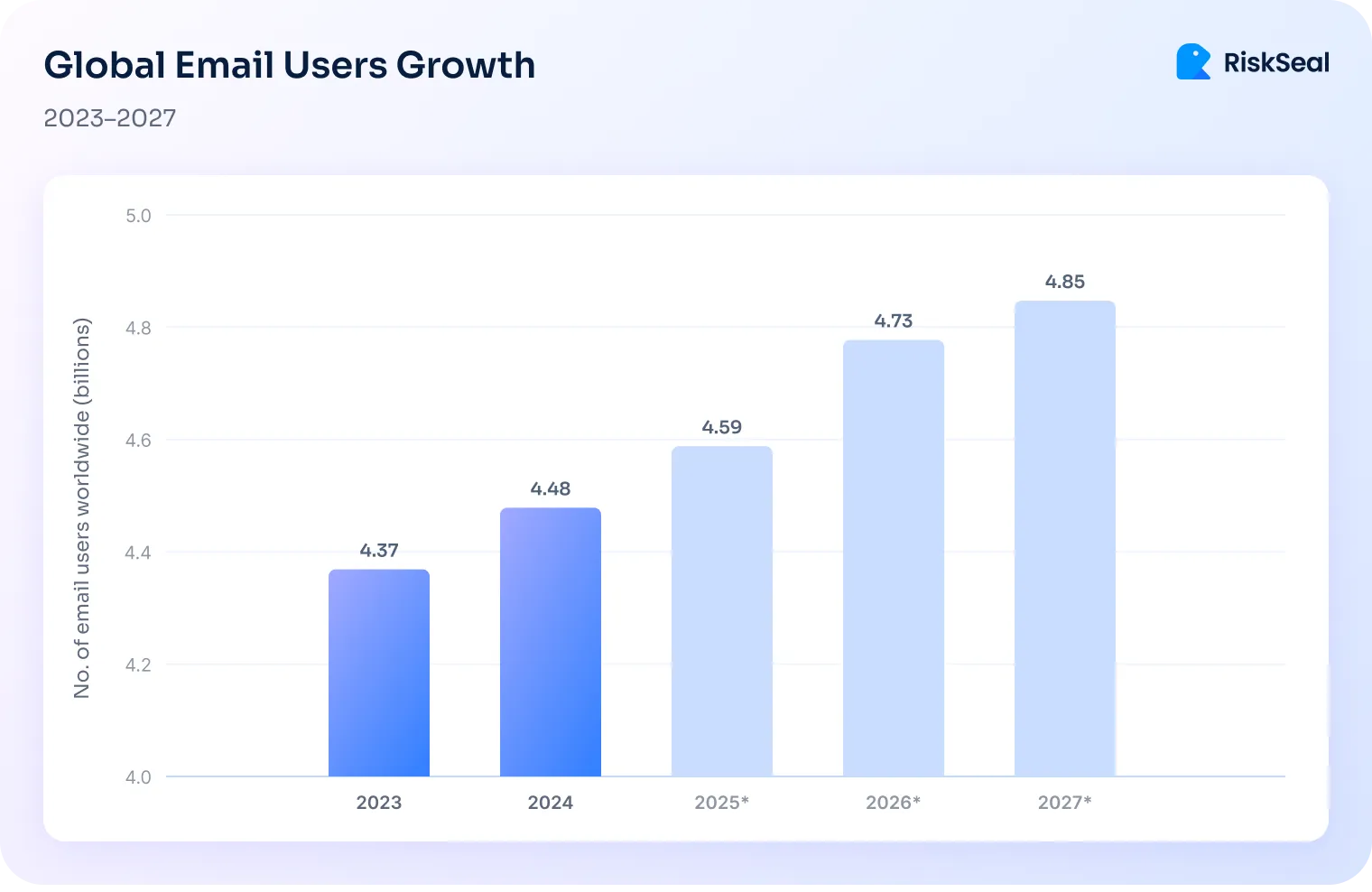

Globally, 4.5 billion people use email:

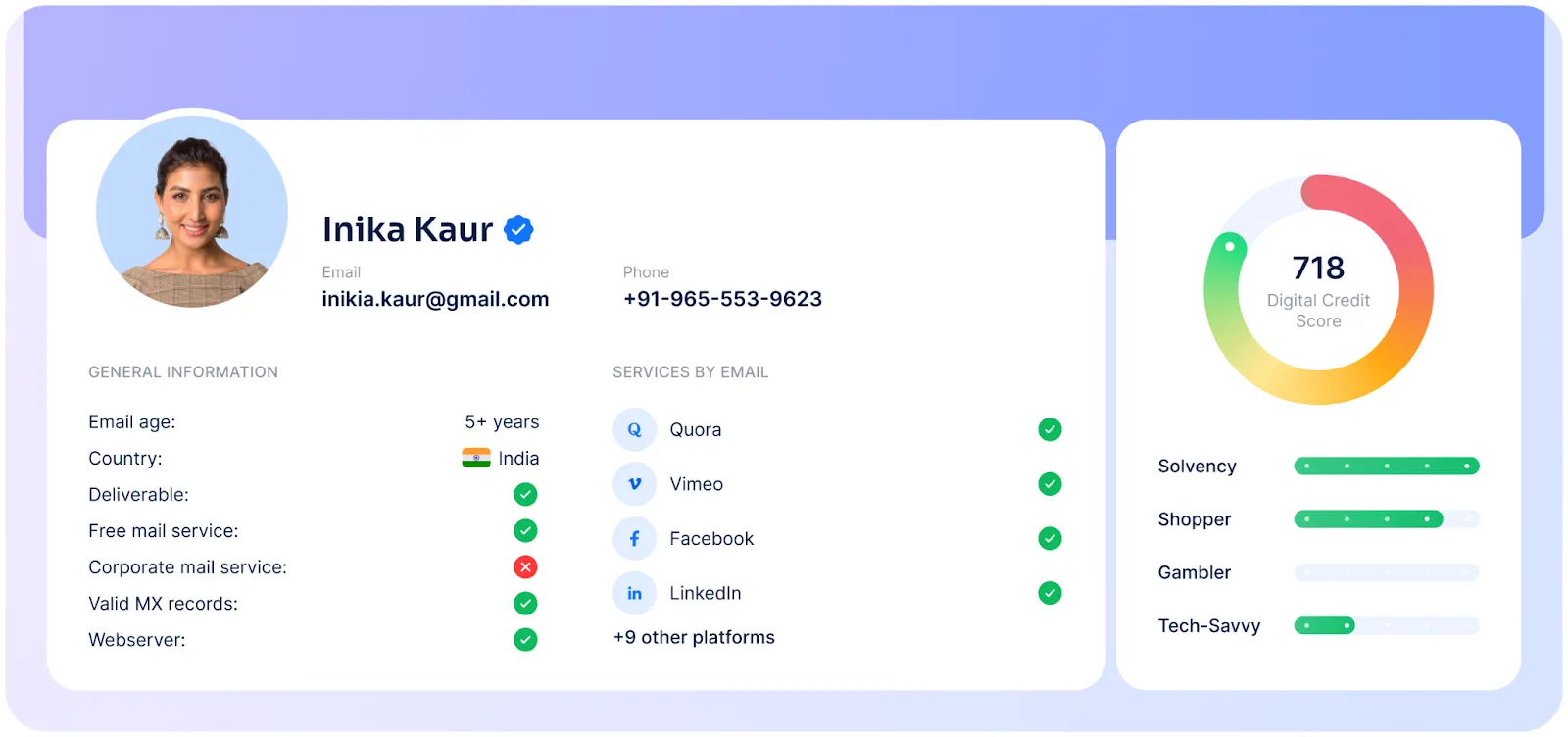

Thanks to email lookup for credit risk assessment, lenders can gather key information on nearly every applicant.

What insights does an email provide?

1. Financial behavior and consumer habits

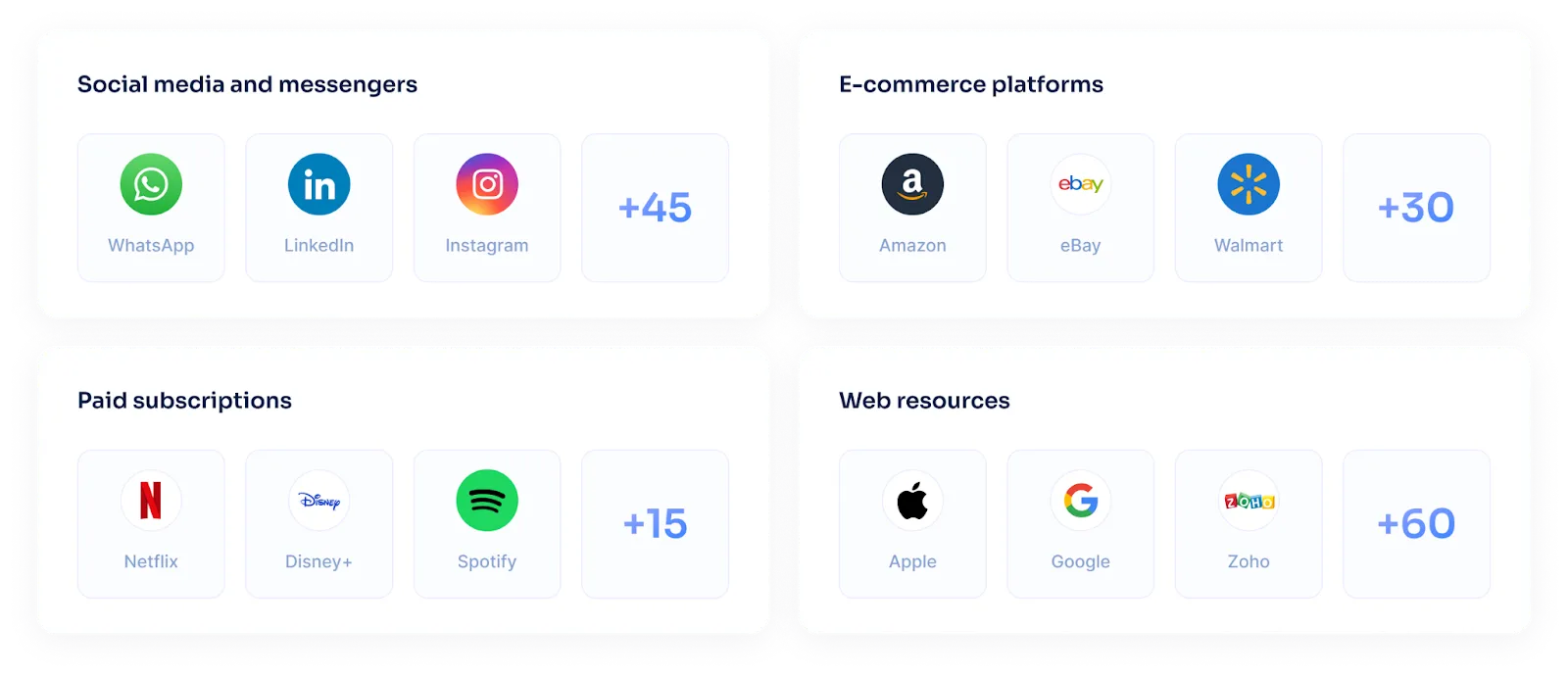

By knowing an applicant’s email, a lender can track their registrations on various online platforms and draw relevant conclusions.

For example, an active account on gambling platforms indicates a person’s inclination toward gambling. This may be perceived as a sign of insufficient borrower reliability.

On the other hand, having paid subscriptions to premium services is a positive indicator. It suggests a high financial status of the consumer.

It is also useful to analyze purchases on e-commerce platforms — their cost, frequency, types of purchased goods, number of abandoned carts, and returns.

All these factors indirectly indicate a person's solvency.

2. Fraud probability

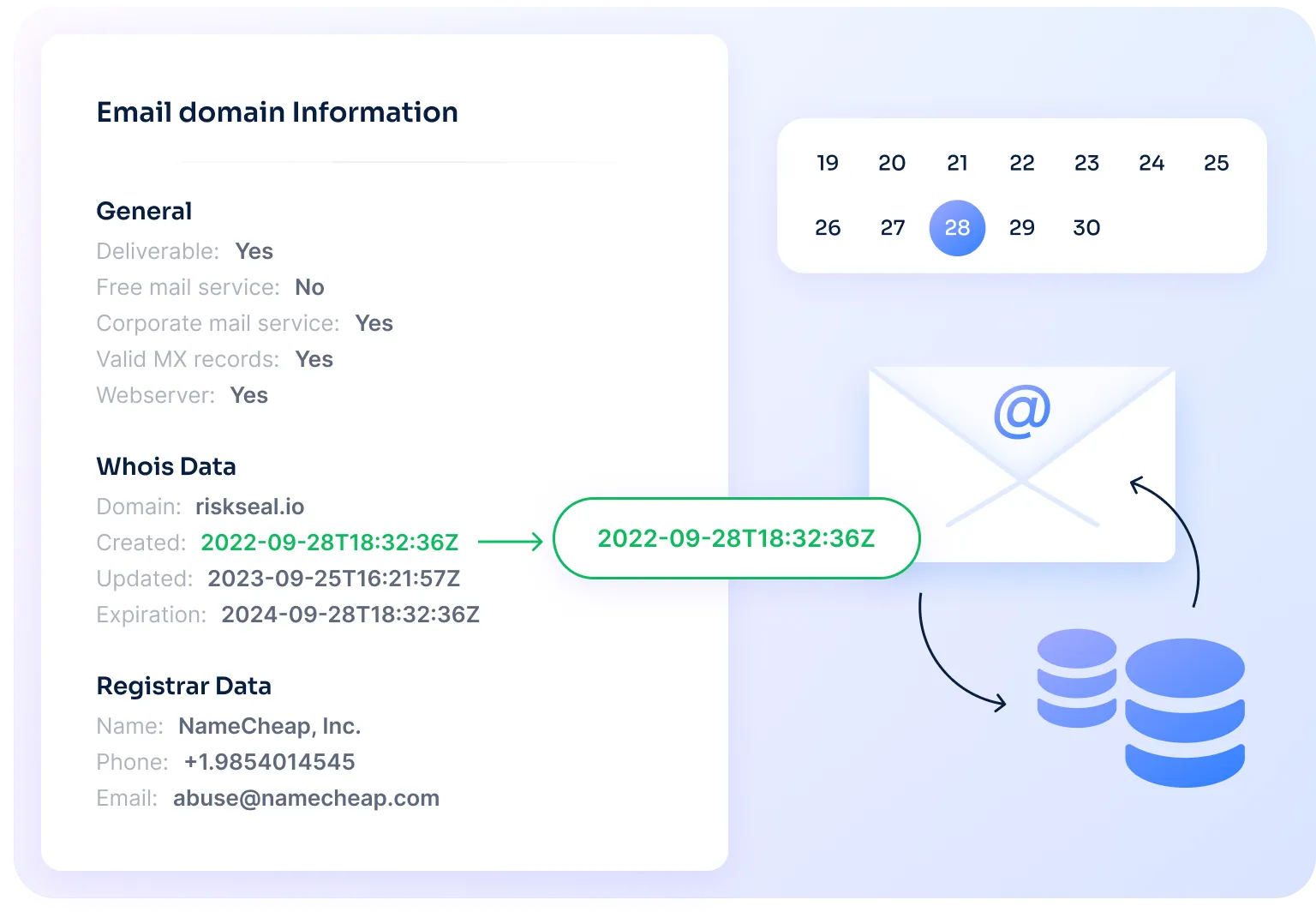

To assess a person’s creditworthiness, an email lookup solution evaluates the type of domain on which the email is registered.

Information about its registration, DNS records, and ownership history is also considered.

The next step is email age estimation, which helps determine when the account was created.

While it is impossible to pinpoint the exact day, there are ways to verify that the address was not created recently.

After all, newly created addresses are often used by fraudsters.

So, how to estimate the age of an email?

1. Check the domain registration date. This can be done using specialized services.

2. Find linked social media accounts. Some of them display the user’s registration date.

3. Check the email for data breaches. If breaches have occurred in the past, it means the email has existed for a long time.

4. Compare all gathered information. For example, cross-check the date of a data breach with the registration date on a social platform.

5. Use Google Dorking. This method involves collecting information from public servers using search engines.

3. User risk level

Analyzing a potential borrower’s email allows assigning them a personalized risk level.

Negatively impacting it are:

- Disposable emails

- Recently created addresses

- Fraudulent email behaviors

Each of these factors may indicate the applicant's criminal intent.

Identifying high-risk credit applicants with email data enrichment

To analyze an applicant’s email, scoring systems use a technology called reverse email lookup.

With this data, the lending provider gathers extensive borrower information from open sources and enhances scoring models.

As a result, the lender can make a well-founded conclusion about the applicant's reliability.

What should be considered?

1. Presence of accounts registered to the email. The average internet user has more than six social network profiles. When considering other online platforms, the number of accounts can reach 100 or more.

Accordingly, a lack of registrations may be a red flag for the lender, while the presence of accounts positively affects the applicant's risk level.

2. Instances of data breaches. Although this factor is generally seen as negative, lenders may interpret it as an element that increases trust in the applicant.

The logic is simple: if an email is associated with data breaches, it means it was created a long time ago and not solely for fraudulent loan applications.

3. Email presence in blacklists. If this fact is detected, the lender should pay closer attention to the borrower.

Being added to blacklists may indicate criminal activity or suggest that fraudsters have taken control of the applicant's email.

Benefits of email address checks for credit risk management

Email risk assessment provides credit institutions with several advantages:

Real-time analysis. Users receive verification results almost instantly, ensuring uninterrupted service for applicants and improving user experience.

For comparison, traditional credit scoring can take several days or even longer to process a loan application.

Improved decision-making process. Lenders report an increase in the number of approved loans while maintaining the quality of their credit portfolio.

Reduced KYC costs. Credit risk assessment using email data allows lenders to filter out the most unreliable applicants as soon as they submit a loan request.

E.g., RiskSeal’s email address checks help reduce a lender’s expenses on the Know Your Customer (KYC) procedure.

Early fraud detection. A high-quality email lookup solution can identify potential fraudsters at an early stage — immediately upon their first interaction with the lender.

This helps reduce the number of fraudulently obtained loans.

Balancing risk mitigation with customer experience

Customer service quality is another important aspect of credit institutions' operations.

Credit risk assessment using email data analysis allows for reducing risk levels while improving the user experience.

Here’s how this is possible:

- Minimizing friction in the loan approval process.

- Automating loan decisions using risk assessments based on artificial intelligence.

- Ensuring compliance with global standards, including GDPR and financial security regulations.

How to implement email risk assessment into credit risk strategy

To seamlessly integrate an email lookup solution into an existing credit risk management system, it’s essential to follow these steps:

Step 1. Choosing the right tool

This process happens in several stages:

- Exploring email risk solutions. Consider specifying key criteria for research, such as pricing, ML capabilities, or industry benchmarks.

- Assessing performance and compatibility. Evaluate solutions’ accuracy, integration capabilities, and scalability.

- Finalizing provider for PoC. Clarify the expected outcomes of the PoC—what metrics will determine success?

For example, we at RiskSeal offer a free PoC.

Step 2. Integrating email analysis with existing credit risk models

What does this procedure involve?

- Aligning email and credit risk factors. Specify how email risk factors contribute to credit risk assessment—are they used for fraud detection, identity verification, or something else?

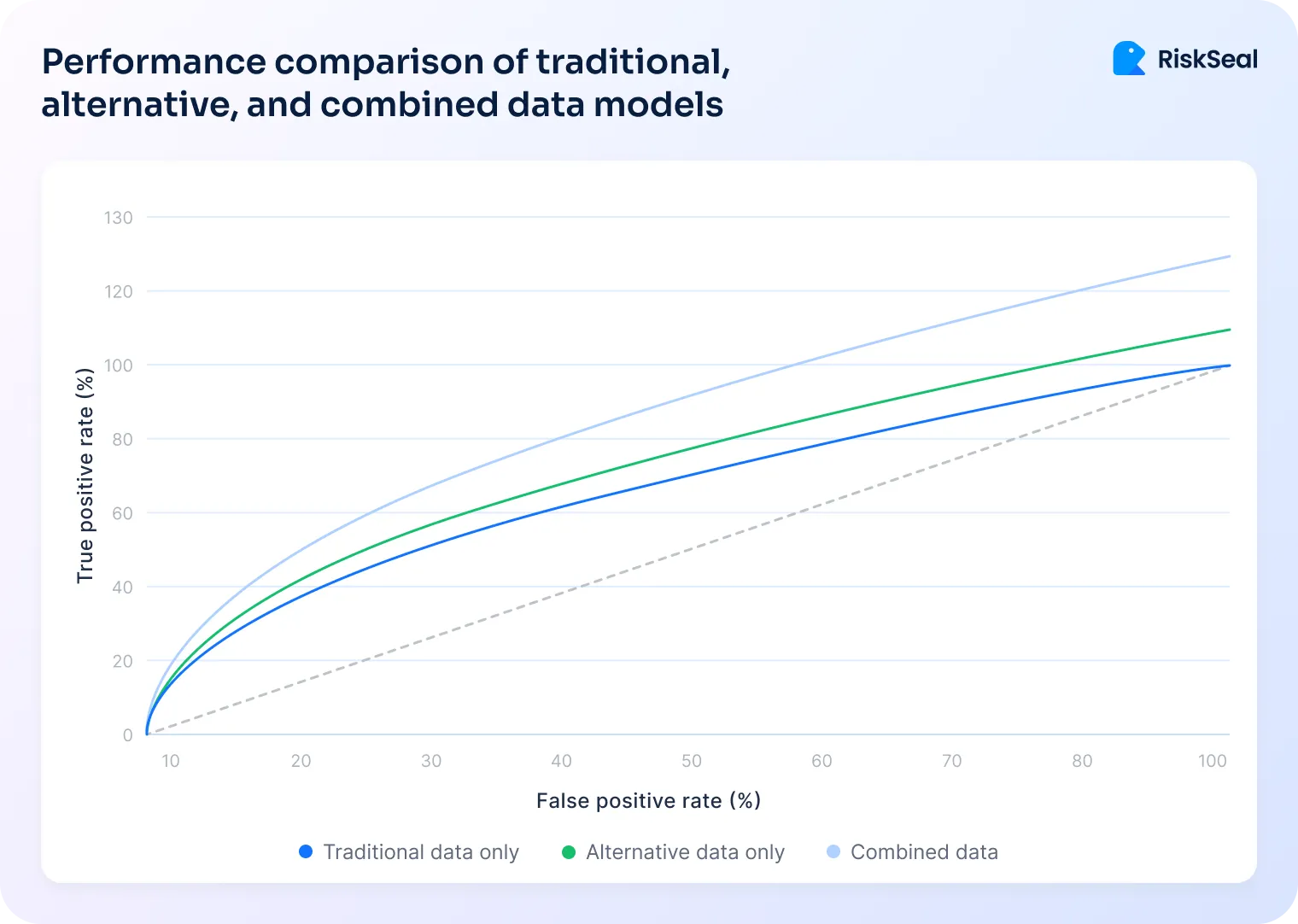

- Integrating email data with financial insights. Combine information obtained through email with traditional financial and behavioral data.

This comprehensive approach demonstrates the most accurate results:

- Optimizing risks. Use machine learning to refine risk predictions.

Step 3. Automating the risk assessment workflow

This step involves the following actions:

- Email insights integration. Incorporating email analysis into automated decision-making.

- Suspicious activity alerts. Establishing real-time monitoring for potential threats.

- Dynamic fraud prevention. Modifying risk thresholds using historical data.

Step 4. Compliance and data security issues

At this stage, it is necessary to ensure:

- Compliance with regulations. Such as GDPR, CCPA, and others, which is a mandatory condition for credit institutions.

- Secure data handling. Ensuring the secure storage and processing of email risk data.

.svg)

.webp)

Email lookup at RiskSeal

RiskSeal ensures seamless integration of email address checks into your credit risk management strategy.

Email account lookup by RiskSeal includes:

- Checking the activity of the email account (email deliverability).

- Detecting social and other accounts linked to the email.

- Analyzing the domain.

- Identifying data breaches, spam distribution, and blacklisting events.

- Verifying the age of the email.

- Identifying disposable email accounts.

With our email lookup solution, lenders can:

1. Improve the effectiveness of credit risk management.

2. Prevent fraud attempts at an early stage.

3. Increase the number of loans granted by improving approval rates.

Key takeaways

To summarize, let’s revisit the main points regarding the role of email data in credit risk management:

- Email is an informative source of alternative data, widely used by modern lenders to assess the creditworthiness of applicants.

- Email address checks help create a complete consumer profile, including their financial capacity and consumer habits, while also detecting fraud signs.

- To successfully implement email data analysis, it is crucial to choose a reliable alternative data provider.

Want to unlock the full potential of reverse email lookup?

Contact a RiskSeal manager to learn about all the possibilities of our scoring system.

See more

Explore how IP address analysis improves credit risk assessment, detects fraud, and reduces loan defaults.

Discover and debunk six common misconceptions about AI in credit scoring and see how RiskSeal helps modern lenders leverage AI safely and effectively.

Learn how to use alternative data to build fairer, more profitable credit models. And stay ahead of regulations.