Key Traits of High-Value Customers in Digital Lending

Learn to identify high-value borrowers early: pretransaction signals predict lifetime value and reduce default risk.

.webp)

The stable income growth for digital lending organizations directly depends on their ability to proactively identify valued customers.

Today, we will discuss why it is so important to identify such borrowers even before the start of their credit activity, and how to do it as effectively as possible.

The 2026 guide to LATAM digital footprints for credit scoring

What defines a high-value customer in fintech?

Who can be considered the most valuable customer for a lending organization?

Here are the main characteristics of such clients:

1. High level of financial discipline. These borrowers make loan payments on time, demonstrate a low risk of default, and improve their credit score over time.

2. Large volume or frequency of lending. Valuable clients show a stable need for credit, completing large transactions or taking out multiple loans over an extended period.

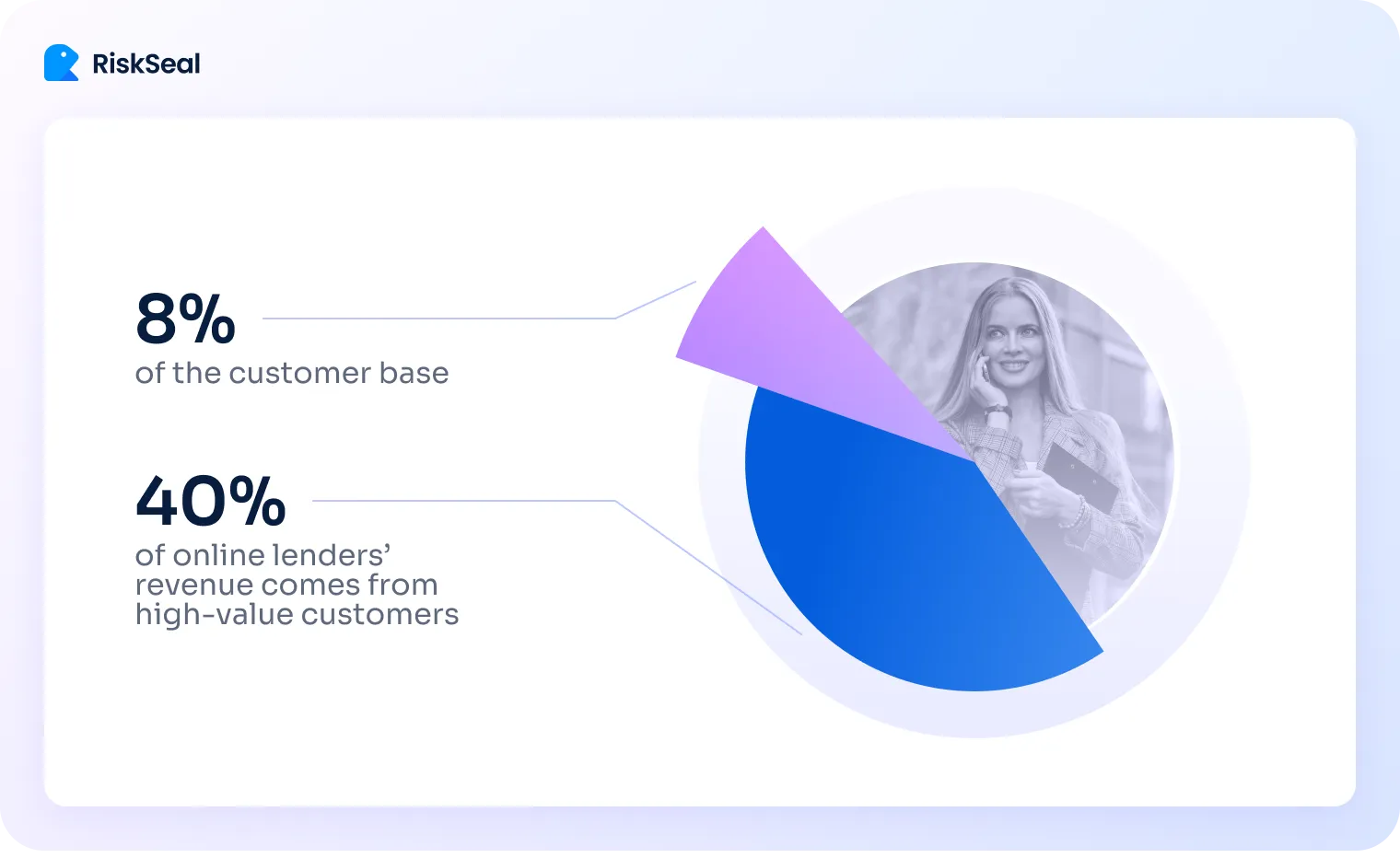

Faster Capital reports that regular clients are vital for online lenders. Although they make up just 8% of customers, they generate 40% of the income.

3. Good profitability adjusted for risk. The lender receives good profit from the interest earned, even accounting for the probability of default.

4. High potential for cross-sales. A high-value customer is often interested in several products. E.g., they may take out a personal loan and later also apply for a credit card.

5. Low risk of fraud. Borrowers with verified identities and standard, non-suspicious behavior are especially valued by fintech companies.

.svg)

Why timing matters: identifying high-value users before the first transaction

Early identification of a high-profile customer is critically important for the successful implementation of a financial organization’s entire lending strategy.

Here’s why this is the case.

Early signals define lifetime value

For lenders, the ability to identify a promising borrower even before the first transaction is a strategic advantage.

When applying to a lending organization, a potential borrower already leaves certain digital footprints:

- Application form data

- Behavior during onboarding

- Method of document upload

- Device and location

- Interaction with the interface

All these signals allow lenders to accurately determine the applicant’s solvency, activation speed, and the company's future income from this client.

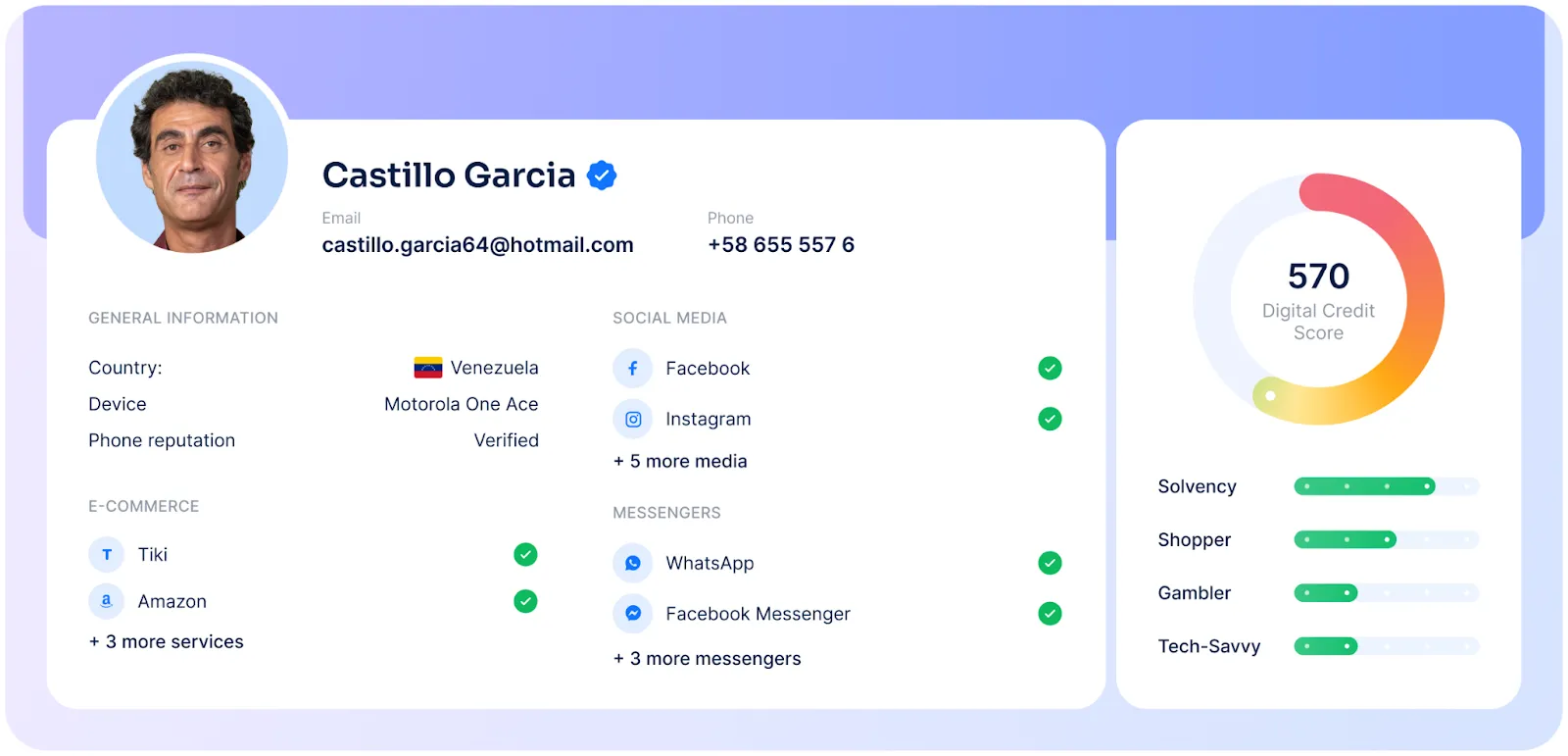

This is exactly how the RiskSeal scoring system works. We specialize in analyzing digital footprints and, based on them, provide lending organizations with a ready-made digital credit scoring number for each borrower.

After receiving this data, credit risk managers can identify “star” clients earlier.

Accordingly, this gives them the opportunity to quickly decide on increasing limits, offering personalized loan conditions, or applying softer verification.

In turn, this increases the share of good clients in the portfolio.

Default risk starts before the loan

Many traditional scoring models take the first transaction as a starting point. However, in practice, borrowers with a high risk of default show alarming behavior patterns even before receiving their first loan.

These include:

- Multiple attempts to register on the platform

- Discrepancies in the provided data

- Bot-like behavioral signals, etc.

For credit risk managers, this is a chance to reduce NPL (non-performing loans) even before the start of credit activity.

Decision speed affects conversion

Identifying a high-value customer even before issuing a loan allows lenders to immediately offer more loyal conditions without delays caused by complex scoring processes.

The result is an increase in the probability of activation and client retention, which is especially important in highly competitive markets.

Why is this so important for lenders? Statistics show that increased customer retention by just 5% can raise an organization's profits by at least 25%.

Moreover, research proves that acquiring a new customer costs companies five times more than retaining an existing one.

That is why, in retail lending, credit risk managers strive to reduce CAC (customer acquisition cost) while simultaneously improving lifetime value. In both cases, the entry point is critical.

From a “reaction” model to a “prediction” model

The shift from reactive risk assessment (based on payment history) to proactive risk assessment is a key trend in the operations of modern lending organizations.

To more accurately segment clients even before the first risk occurs, it is advisable to use alternative data. This approach allows for more precise credit policy adjustments without increasing KYC costs.

With RiskSeal data, our clients save up to 70% of their KYC verification budget thanks to early risk identification.

Real-time signals to identify high-value applicants

Credit scoring using alternative data allows lenders to obtain a wide range of signals for identifying high-value clients.

Let’s take a closer look at it.

Digital footprints

This is a real treasure trove of information about potential borrowers. Digital footprint analysis allows lenders to assess applicants even if they have no credit history.

Key signals include:

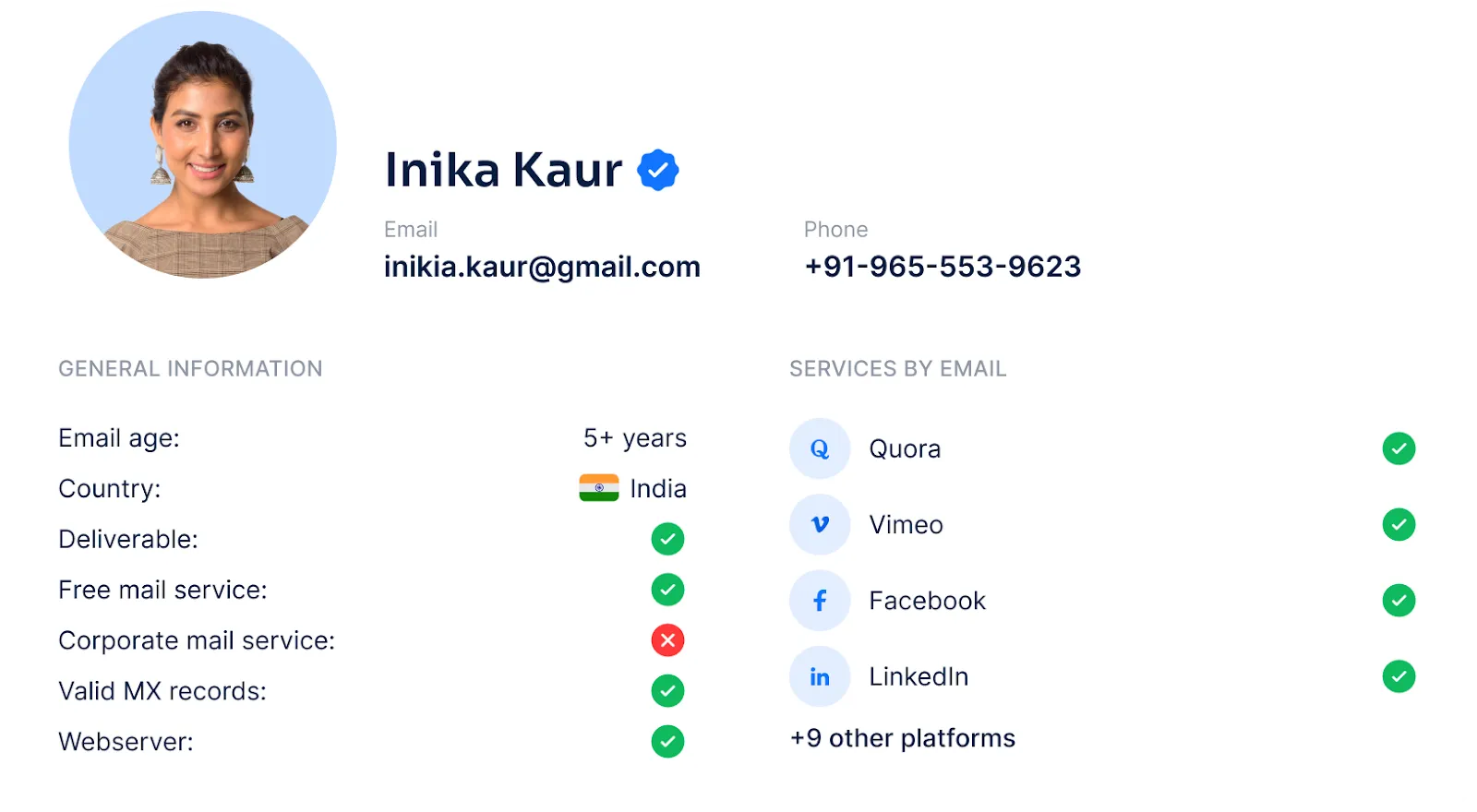

1. Email verification. An email address can provide the lender with many useful insights.

One of them is information about borrower's online accounts. Such verification is possible with an email lookup service like RiskSeal. It helps lenders uncover digital traces linked to the applicant's email.

Each of these profiles contains a lot of publicly available information about the user.

E.g., details about their education and career (on LinkedIn and similar platforms), interests, geolocation tags, and more.

The absence of registrations should raise suspicions for the lender. After all, a digital presence is an essential attribute of modern life.

In addition, you can verify the authenticity and age of the email, as well as check whether it appears in high-risk databases.

2. Phone number analysis. A reverse phone number search engine provides similar information. It helps finding details about a mobile subscriber and verifying whether the number is disposable, virtual, or trustworthy.

Knowing the applicant’s phone number, you can track which platforms they are registered on and which online services and messengers they use.

It is also useful to understand the type of phone number (virtual SIM cards, disposable numbers, etc.), its activity, and whether it appears on spam or fraud blacklists.

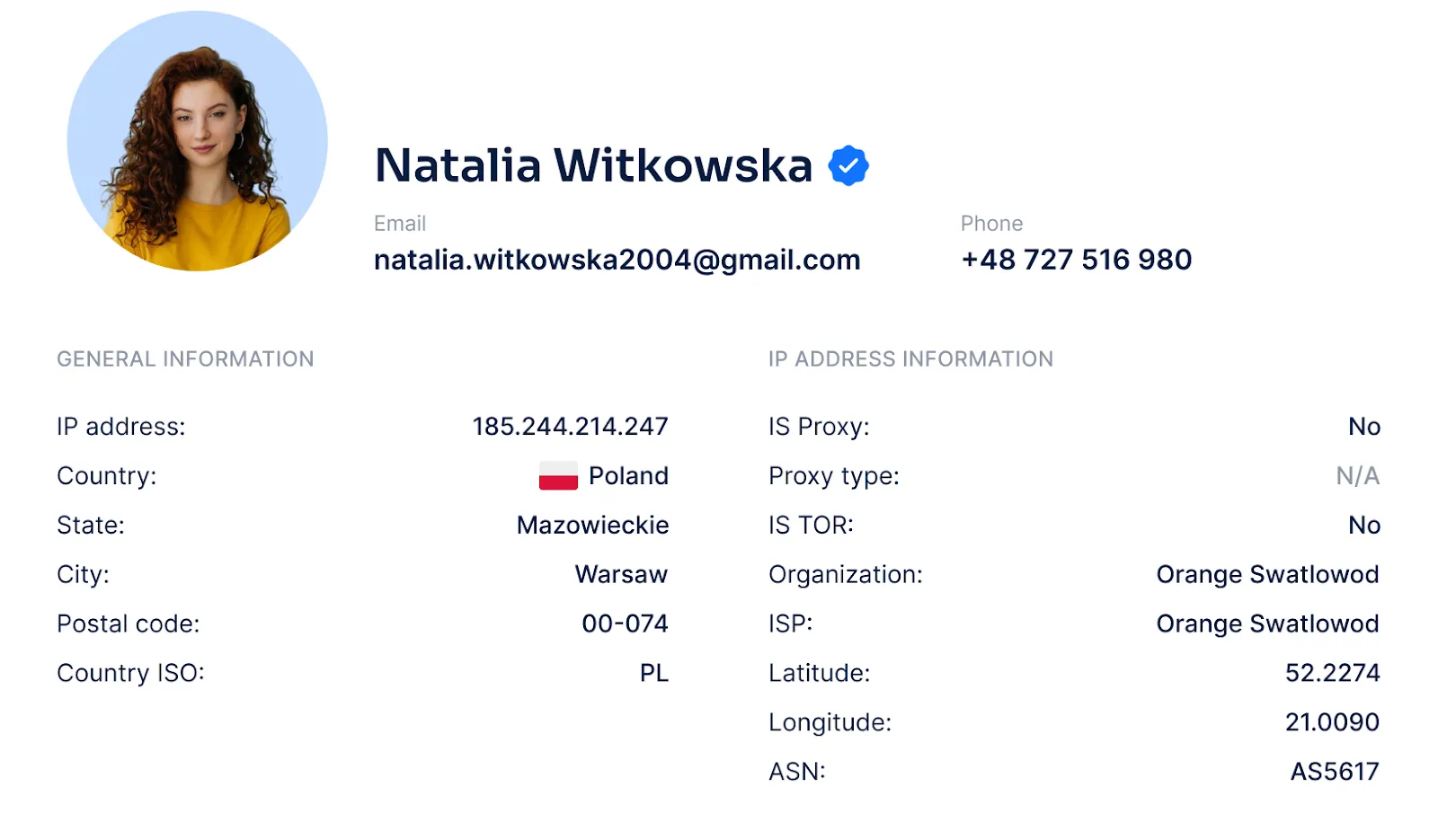

3. IP address analysis. IP address lookup allows you to determine the borrower’s location.

Using it, the lending organization can find out the applicant’s real location and compare it with the information provided in the application.

Any discrepancy discovered is a reason for further verification.

This method also makes it possible to detect the use of anonymizers such as VPNs or proxies.

If you find that the applicant is hiding their real IP address, it is a good reason to suspect fraud.

Identification of creditworthy clients

To identify high-value clients, it is important to pay attention to positive signals indicating the consumer's creditworthiness.

These include:

1. Presence of paid subscriptions. Regular payments for online services indicate financial discipline.

2. Profiles on professional networks. Accounts on LinkedIn and similar platforms can suggest stable employment and income.

3. Use of premium services. Choosing high-quality products may reflect a stable financial situation.

Early detection of potential risks

In addition to identifying positive borrowers, alternative data helps timely recognize potential risks.

Here are the warning signs that should alert the lender:

1. Absence of a digital footprint. A complete lack of online activity may indicate a fake identity.

2. Use of temporary or disposable email addresses. Such addresses are often used by fraudsters.

3. Mismatch between geolocation and provided data. Discrepancies between the stated location and the IP address may indicate attempts at deception.

Top pitfalls to avoid when targeting high-value customers

Sometimes lenders, in trying to recognize valued clients, fail. Why does this happen? Let’s look at the most common problems and how to avoid them.

Pitfall #1. Overreliance on traditional credit data

Even the most reliable, creditworthy borrowers may not have a credit history. This includes young people, recent immigrants, and self-employed individuals.

By relying solely on credit bureau data in credit scoring, you might miss out on promising clients.

RiskSeal’s recommendation. Use data enrichment for credit scoring to build a comprehensive view of the applicant's financial situation.

Pitfall #2. Underestimating behavioral dynamics

Clients change over time.

A person who appears highly valuable today may face financial deterioration within 3-6 months.

RiskSeal’s recommendation. Invest in dynamic scoring models that periodically reassess the credit profile based on fresh data rather than relying on static evaluation.

Pitfall #3. Ignoring early warning signs

The desire to quickly attract “star-like” clients sometimes leads to overlooking risky indicators, such as address and geolocation mismatch, suspicious device activity, or use of disposable email addresses.

RiskSeal’s recommendation. Even for promising clients, conduct basic real-time screening through platforms like RiskSeal to filter out fraudsters and unreliable applicants.

Pitfall #4. Uneven limit distribution

Granting excessively high limits in online lending without proper verification can increase losses in the event of a default.

RiskSeal’s recommendation. Apply the “minimally sufficient credit” principle at the start, increasing limits after confirming a positive payment history.

Pitfall #5. Overcomplicated onboarding with complex checks

Even the best clients are not willing to undergo multi-step, lengthy verification processes.

A complicated process can cause the loss of a high-value user already at the registration stage.

RiskSeal’s recommendation. Speed up your KYC with real-time checks and offer accelerated onboarding paths.

Pitfall #6. Lack of transparent communication

If clients do not understand why they are offered certain terms or limits, their loyalty may decrease.

RiskSeal’s recommendation. Build communication based on clear criteria and explain the benefits for high-value clients. E.g., it is advisable to mention fast limit increases or bonus programs.

How RiskSeal helps in high-value customer identification

RiskSeal provides credit risk officers with a powerful tool to identify creditworthy clients even before the first transaction.

With us, you get:

- Over 400 data points obtained through digital footprint analysis.

- Accurate identification of creditworthy clients.

- Early detection of potential risks.

- Fast application processing (around 5 seconds).

- Up to 70% reduction in KYC costs.

- Improved scoring accuracy (AUC up to 83%).

Take advantage of RiskSeal’s digital scoring system to maximize profits through high-value customers.

Inside the LATAM alternative credit data report

See more

Explore Mexico’s consumer lending market, from major loan types and fintech trends to key providers, risk challenges, and growth opportunities.

Explore how to spot high-risk borrowers. Discover key red flags, alternative credit scoring, and risk mitigation strategies.

Discover four practical ways to strengthen consumer credit risk in 2026 with real-time underwriting, alternative data, smarter collections, and compliance-ready AI.